Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Thailand’s home finance market totals approximately USD ~ billion in outstanding residential mortgage loans, based on a recent historical assessment of central bank housing credit statistics and banking sector disclosures. The market is driven by urban housing demand, expanding middle-income homeownership, and government-supported mortgage access programs. Commercial banks dominate origination through long-tenure housing loans, while property developer financing partnerships and subsidized housing schemes expand credit penetration across first-time buyers and salaried households.

Bangkok leads Thailand’s home finance activity due to concentration of property development, employment density, and financial institution presence, while major provincial hubs including Chonburi, Nonthaburi, and Chiang Mai show strong mortgage demand linked to urban expansion and industrial employment clusters. Eastern Economic Corridor development and transport infrastructure connectivity reinforce metropolitan housing markets. Higher property values, condominium density, and salaried workforce concentration explain the sustained dominance of metropolitan Thailand in housing finance origination.

Market Segmentation

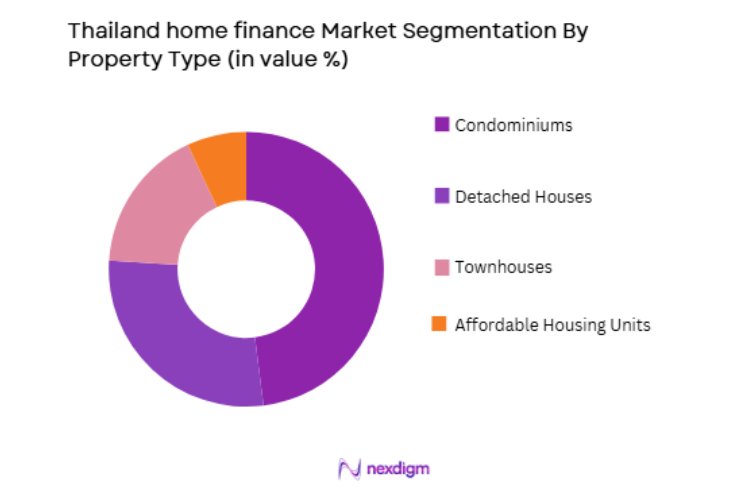

By Property Type

Thailand Home Finance market is segmented by property type into condominiums, detached houses, townhouses, and affordable housing units. Recently, condominiums have a dominant market share due to factors such as urban land scarcity, vertical housing supply concentration, and buyer affordability alignment with mortgage eligibility thresholds. Bangkok’s high-density residential development is overwhelmingly condominium-led, creating a structurally larger mortgageable inventory compared with landed housing. Younger salaried households and first-time buyers favor condominiums due to lower ticket sizes and proximity to employment centers, reinforcing financing demand.

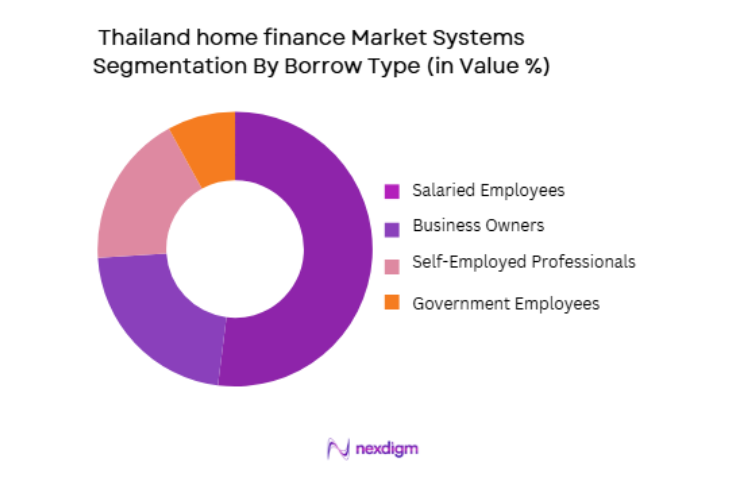

By Borrower Type

Thailand Home Finance market is segmented by borrower type into salaried employees, self-employed professionals, business owners, and government employees. Recently, salaried employees have a dominant market share due to factors such as stable income verification, lower credit risk, and standardized underwriting compatibility with bank mortgage policies. Formal employment documentation and payroll-linked repayment capacity simplify credit assessment, enabling faster loan approval compared with irregular income borrowers. Banks actively target salaried borrowers through employer partnerships and mortgage campaigns tied to workplace clusters.

Competitive Landscape

Thailand’s home finance market is concentrated among large domestic commercial banks with nationwide branch networks and strong deposit bases enabling long-tenure mortgage lending. State-linked housing finance institutions support affordable and subsidized lending segments, while private banks compete through developer partnerships and digital mortgage platforms. Market leaders differentiate through approval speed, developer alliances, and bundled financial products, reinforcing consolidation around top universal banks and government housing lenders.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Mortgage Focus Segment |

| Government Housing Bank | 1953 | Bangkok | ~ | ~ | ~ | ~ | ~ |

| Bangkok Bank | 1944 | Bangkok | ~ | ~ | ~ | ~ | ~ |

| Kasikornbank | 1945 | Bangkok | ~ | ~ | ~ | ~ | ~ |

| Siam Commercial Bank | 1906 | Bangkok | ~ | ~ | ~ | ~ | ~ |

| Krungthai Bank | 1966 | Bangkok | ~ | ~ | ~ | ~ | ~ |

Thailand Home Finance Market Analysis

Growth Drivers

Urbanization-Driven Residential Housing Demand Expansion

Thailand’s continued urban migration toward metropolitan employment centers is structurally increasing demand for financed residential property, particularly in Bangkok and surrounding provinces where land scarcity and high property prices necessitate mortgage financing for most homebuyers across income tiers. Expanding service-sector employment and industrial corridor development are concentrating populations in urban regions requiring formal housing solutions supported by bank lending. Condominium development aligned with transit infrastructure and workplace proximity is generating large volumes of mortgage-eligible housing stock, reinforcing credit demand. Government infrastructure investments improve connectivity and expand suburban residential zones, further stimulating financed home purchases. Rising household formation among younger urban populations is increasing first-time homebuyer demand requiring mortgage access. Financial institutions actively promote mortgage products to capture urban housing growth, including preferential rates and developer tie-ups. Property ownership remains a primary wealth objective among Thai households, sustaining long-term demand for housing finance. Urban property value appreciation expectations also encourage leveraged home acquisition through mortgages.

Government-Supported Housing Credit Accessibility Programs

Thailand’s policy emphasis on homeownership affordability through subsidized lending schemes, tax incentives, and state-backed housing finance institutions is significantly expanding mortgage access among lower- and middle-income households, directly supporting home finance market growth across previously underserved borrower segments. The Government Housing Bank and public sector lending initiatives provide preferential interest rates and extended tenures enabling households with moderate incomes to qualify for housing loans. Targeted programs for first-time buyers and affordable housing projects increase mortgage penetration in entry-level housing segments. Fiscal incentives related to housing purchases further encourage financed home acquisition. Public-private developer collaborations linked to subsidized credit schemes accelerate loan origination in designated housing zones. Regulatory frameworks supporting housing finance stability and consumer protection reinforce borrower confidence in mortgage commitments. State-supported refinancing and restructuring programs also maintain repayment sustainability, preserving loan portfolios. Affordable housing supply expansion aligned with financing access ensures continuous mortgage demand creation.

Market Challenges

Household Debt Saturation and Borrower Affordability Constraints

Thailand’s elevated household debt levels relative to income are constraining incremental mortgage borrowing capacity across large portions of the population, limiting expansion of housing finance despite ongoing residential demand in urban and suburban markets. Many households already carry consumer credit, auto loans, and existing housing debt, reducing eligibility for additional mortgage commitments under prudential lending standards. Banks maintain conservative debt-service thresholds to manage systemic credit risk, restricting approval rates for new applicants. Wage growth has not consistently matched property price increases, weakening affordability ratios for prospective buyers. Rising interest rate environments increase repayment burdens, further constraining borrower qualification. Informal employment and income volatility among many households complicate mortgage underwriting. Developers face slower sales absorption when credit access tightens, indirectly reducing loan origination volumes. Household leverage sensitivity to economic cycles increases credit risk perception among lenders. These affordability and indebtedness constraints structurally moderate Thailand’s home finance market growth trajectory.

Property Market Cyclicality and Collateral Value Volatility Risks

Thailand’s residential property market exhibits cyclical fluctuations in supply, pricing, and demand that directly affect mortgage lending stability, collateral valuation confidence, and lender risk exposure across housing finance portfolios. Periods of condominium oversupply in urban markets can depress property prices and reduce collateral coverage ratios for outstanding loans. Valuation uncertainty during market downturns increases credit risk and provisioning requirements for lenders. Developers may delay or cancel projects during weak demand phases, reducing mortgageable inventory. Regional property markets dependent on tourism or industrial cycles show pronounced demand volatility affecting loan origination patterns. Economic shocks impacting employment or income levels can increase mortgage delinquency risk. Financial institutions respond by tightening credit standards during downturns, suppressing new lending. Borrowers may face negative equity conditions if property values decline significantly. These cyclical dynamics introduce structural risk and volatility into Thailand’s home finance market performance.

Opportunities

Digital Mortgage Platforms and Automated Credit Underwriting Adoption

Thailand’s banking sector is rapidly digitizing mortgage origination and credit assessment processes, creating significant opportunities to expand home finance access, reduce approval times, and lower operational costs while improving borrower experience across urban and emerging housing markets. Online mortgage applications, digital document verification, and automated credit scoring systems streamline loan processing for salaried borrowers with standardized financial profiles. Integration of property valuation databases and digital land registry systems enhances collateral assessment accuracy. Mobile banking ecosystems allow borrowers to track loan status and manage repayments conveniently. Digital channels also expand reach into younger and geographically dispersed homebuyer segments. Banks leveraging data analytics can better assess risk among non-traditional borrowers. Reduced processing costs enable competitive interest pricing and broader loan accessibility. Developer-bank digital integration accelerates pre-approved financing at property sales points. Technology-enabled mortgage ecosystems are positioned to drive Thailand’s home finance market modernization and expansion.

Expansion of Affordable Housing Finance through Public-Private Partnerships

Collaborative housing development and financing models between government agencies, developers, and financial institutions present substantial opportunities to scale affordable homeownership and mortgage penetration across underserved Thai households lacking access to conventional housing finance products. Public-private partnerships can align subsidized land allocation, affordable construction, and preferential mortgage terms to reduce entry barriers for low-income buyers. Government credit guarantees or interest subsidies can mitigate lender risk in affordable segments. Large-scale housing projects integrated with transport infrastructure enable cost-efficient urban expansion. Financial institutions participating in such programs gain portfolio diversification and social lending incentives. Structured financing pools and securitization of affordable mortgages can enhance capital availability. Community-based housing finance initiatives extend reach into semi-urban regions. Rising policy emphasis on inclusive housing supports sustained financing demand. These partnership-driven models offer a major growth pathway for Thailand’s home finance market.

Future Outlook

Thailand’s home finance market is expected to expand steadily over the next five years supported by urban housing demand, digital mortgage adoption, and government-backed affordability initiatives. Metropolitan expansion and infrastructure connectivity will sustain financed property purchases. Technology-enabled underwriting will broaden borrower access. Affordable housing programs and developer partnerships will increase loan origination. Demographic household formation trends will continue reinforcing long-term mortgage demand.

Major Players

- Government Housing Bank

- Bangkok Bank

- Kasikornbank

- Siam Commercial Bank

- Krungthai Bank

- Bank of Ayudhya

- TMBThanachart Bank

- UOB Thailand

- CIMB Thai Bank

- Land and Houses Bank

- Kiatnakin Phatra Bank

- ICBC Thailand

- Standard Chartered Thailand

- HSBC Thailand

- Sumitomo Mitsui Banking Corporation Thailand

Key Target Audience

- Commercial banks

- Housing finance institutions

- Property developers

- Investments and venture capitalist firms

- Insurance companies

- Mortgage technology providers

- Government and regulatory bodies

- Real estate investment trusts

Research Methodology

Step 1: Identification of Key Variables

Key variables including outstanding mortgage credit, housing supply composition, borrower demographics, lending standards, and property price dynamics were identified. Data sources included central bank housing credit statistics, banking disclosures, and real estate transaction indicators to define Thailand’s housing finance baseline.

Step 2: Market Analysis and Construction

Mortgage credit volumes were mapped across borrower and property segments, linking housing stock distribution with financing penetration ratios. Institutional lending channels and policy programs were integrated to construct Thailand’s home finance market size and segmentation structure.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on borrower affordability, urban housing demand, and credit accessibility were validated against banking practices, property market studies, and policy frameworks. Cross-verification ensured alignment with Thailand’s household debt conditions and housing finance regulations.

Step 4: Research Synthesis and Final Output

Quantitative mortgage data and qualitative housing market insights were synthesized into a structured model covering size, segmentation, drivers, and risks. Analytical integration ensured consistency with Thailand’s financial system and residential property dynamics to produce the final market assessment.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Urbanization and Housing Demand Expansion in Metropolitan Thailand

Government Incentives and Affordable Housing Schemes

Digital Mortgage Processing and Fintech Lending Integration - Market Challenges

Household Debt Burden and Mortgage Affordability Constraints

Interest Rate Volatility and Loan Servicing Risk

Regulatory Lending Caps and Credit Assessment Tightening - Market Opportunities

Expansion of Affordable Housing Finance and Subsidized Loans

Growth in Green Housing and Energy-Efficient Mortgage Products

Digital End-to-End Mortgage Origination and Approval - Trends

Shift Toward Fixed and Hybrid Rate Mortgage Structures

Rising Demand for Online Mortgage Application Channels - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Fixed Rate Home Loans

Floating Rate Home Loans

Hybrid Rate Home Loans

Islamic Home Financing

Refinancing and Top-Up Loans - By Platform Type (In Value%)

Bank-Originated Mortgages

Non-Bank Housing Finance Companies

Digital Mortgage Platforms

Government Housing Programs

Cooperative Housing Finance Schemes - By Fitment Type (In Value%)

Owner-Occupied Home Financing

Investment Property Financing

Self-Build Housing Loans

Renovation and Extension Financing - By End User Segment (In Value%)

First-Time Homebuyers

Upgraders and Second-Home Buyers

Property Investors

- Market Share Analysis

- Cross Comparison Parameters (Loan Tenure Range, Interest Rate Structure, LTV Ratio, Approval Turnaround Time, Digital Application Capability, Prepayment Flexibility, Income Assessment Method, Property Eligibility Scope, Refinancing Options, Government Subsidy Integration)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Government Housing Bank

Bangkok Bank Housing Loan

Kasikornbank Home Loan

Siam Commercial Bank Home Loan

Krungsri Home for Cash

TMBThanachart Mortgage

Kiatnakin Phatra Housing Loan

UOB Thailand Home Loan

CIMB Thai Home Financing

LH Bank Home Loan

ICBC Thai Housing Loan

Standard Chartered Thailand Mortgage

HSBC Thailand Home Loan

Land and Houses Securities Mortgage

Thanachart Housing Finance

- Increasing First-Time Buyer Participation in Urban Housing

- Growing Investor Interest in Rental Residential Assets

- Mortgage Accessibility Needs of Informal and Self-Employed Workers

- Demand for Renovation Financing in Aging Housing Stock

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now