Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Thailand Industrial Automation market is experiencing significant growth driven by technological advancements in robotics, artificial intelligence, and Internet of Things (IoT) solutions. Market size is projected to reach USD ~ billion, with demand primarily fueled by the growing need for automation in manufacturing processes, increasing labor costs, and the push for higher operational efficiency across industries. The rapid adoption of automation technologies is transforming industries such as automotive, electronics, and food and beverage, contributing to this surge in demand.

Countries like China, the United States, and Germany continue to dominate the industrial automation landscape due to their advanced manufacturing capabilities and technological infrastructure. These regions benefit from strong industrial ecosystems, a high degree of automation integration, and substantial investments in research and development. Their leadership is driven by government policies supporting automation, significant industrial output, and a highly skilled workforce in automation technologies, allowing them to maintain dominance in the market.

Market Segmentation

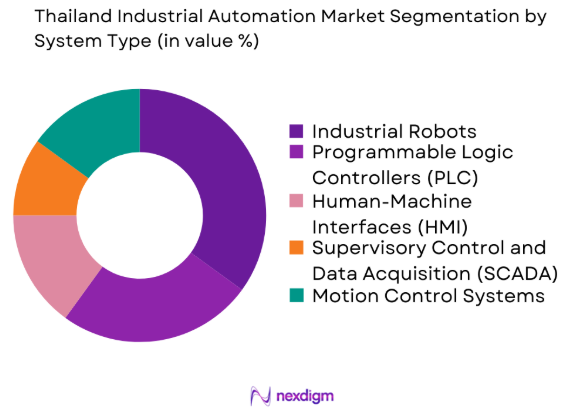

By System Type

The industrial automation market is segmented by system type into industrial robots, programmable logic controllers (PLC), human-machine interfaces (HMI), supervisory control and data acquisition (SCADA), and motion control systems. Recently, industrial robots have gained a dominant market share due to their high adaptability in various industries such as automotive, electronics, and consumer goods. As companies seek to improve efficiency and reduce costs, the demand for robotics, especially in assembly lines and material handling, continues to increase. Industrial robots are often preferred for their precision, speed, and ability to work in hazardous environments, further propelling their market share dominance.

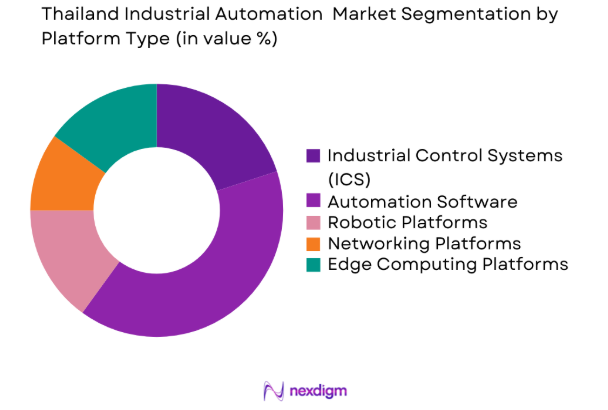

By Platform Type

The market is segmented by platform type into industrial control systems (ICS), automation software, robotic platforms, networking platforms, and edge computing platforms. Automation software has recently emerged as the dominant sub-segment, driven by the increasing need for software that can manage complex processes and integrate IoT, AI, and big data analytics. With the rise of Industry 4.0, the demand for software solutions that offer scalability, real-time monitoring, and control has skyrocketed. These platforms enhance the performance of automated systems, driving widespread adoption in industries like manufacturing and energy.

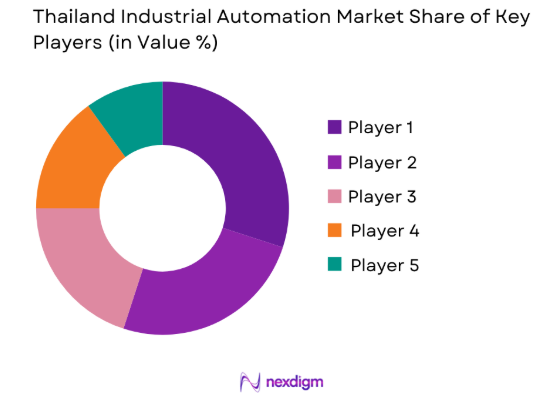

Competitive Landscape

The competitive landscape in the industrial automation market is highly concentrated, with several global players leading the industry. These major companies are engaging in mergers and acquisitions to expand their product offerings and geographical reach. Consolidation is a key strategy, enabling firms to enhance their technological capabilities and improve operational efficiency. Leading players in the market include Siemens AG, Rockwell Automation, and ABB, who continually invest in automation solutions, R&D, and customer support services to maintain a competitive edge.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Market-Specific Parameter |

| Siemens AG | 1847 | Germany | ~ | ~ | ~ | ~ | ~ |

| Rockwell Automation | 1903 | United States | ~ | ~ | ~ | ~ | ~ |

| ABB | 1883 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Honeywell International | 1906 | United States | ~ | ~ | ~ | ~ | ~ |

| Mitsubishi Electric | 1921 | Japan | ~ | ~ | ~ | ~ | ~ |

Thailand Industrial Automation Market Analysis

Growth Drivers

Technological Advancements in Robotics

Robotics’ increasing role in manufacturing is a key growth driver in the industrial automation market. The integration of robots into production lines, particularly in industries like automotive and electronics, has significantly enhanced productivity. Robotics technology improves operational efficiency, reduces human error, and supports continuous production, making it indispensable for companies aiming to stay competitive. Advancements in robotic arms, sensors, and machine learning algorithms have made robots more adaptable, precise, and cost-effective. These innovations have expanded the scope of robotic applications, from assembly lines to quality control, leading to greater adoption across various industries. As businesses seek to optimize their operations, robotics is becoming an integral part of modern manufacturing processes.

Government Policies Supporting Automation

Governments around the world are increasingly supporting industrial automation through subsidies, grants, and favorable policies designed to reduce labor costs and boost productivity. These initiatives are particularly prominent in manufacturing hubs, where automation is considered essential for maintaining global competitiveness. Countries such as Germany and Japan have introduced strategic plans that encourage the integration of AI, robotics, and automation technologies across key industries. This government backing is fostering a conducive environment for the growth of the industrial automation sector. By offering financial incentives and creating policies that promote innovation, governments are helping businesses overcome financial barriers to adoption, ultimately driving the expansion and advancement of automation technologies across various industries.

Market Challenges

High Initial Capital Investment

A major challenge in the industrial automation market is the high capital investment needed for automation technologies. Small and medium-sized enterprises (SMEs) often struggle to justify the upfront costs of acquiring robotic systems, PLCs, and automation software, especially when they have not yet realized a return on investment. The financial burden of implementing these systems can be overwhelming, particularly for businesses with limited capital or operating on tight margins. Although the long-term advantages of automation, such as improved efficiency and reduced labor costs, are clear, these initial financial barriers present a significant hurdle for adoption. Overcoming this challenge requires solutions that reduce the cost of entry for SMEs and enable them to access automation technologies more affordably.

Lack of Skilled Workforce

As industries adopt automation technologies, the demand for skilled professionals to design, operate, and maintain these systems has increased. However, there is a significant shortage of workers with expertise in robotics, AI, and IoT, preventing companies from fully utilizing automation’s potential. This skills gap restricts the successful implementation of automation solutions and hinders businesses from scaling their operations efficiently. The lack of qualified personnel poses a challenge for companies looking to stay competitive in an increasingly automated world. To address this issue, investing in training and educational programs is essential to develop a skilled workforce capable of meeting the growing demands of the automation industry and ensuring long-term success.

Opportunities

Rise of Industry 4.0

The shift toward Industry 4.0, marked by the integration of IoT, AI, and automation, offers substantial growth prospects for the industrial automation market. As industries embrace these advanced technologies, the need for automation solutions that can seamlessly integrate with IoT and AI platforms is growing. Companies seek solutions that enable real-time data analytics, predictive maintenance, and autonomous operations to enhance efficiency. This transition is fueling demand for automation technologies capable of supporting Industry 4.0 objectives, such as improving manufacturing processes, boosting productivity, and ensuring flexibility in production systems. The adoption of these technologies is essential for optimizing operations, maintaining competitiveness, and driving digital transformation in the manufacturing sector.

Growth in Emerging Markets

Emerging economies in the Asia-Pacific region, particularly India, China, and Southeast Asia, are witnessing rapid industrialization and urbanization, which presents significant growth opportunities for the industrial automation market. As these countries continue to invest heavily in infrastructure, manufacturing, and technological advancements, the demand for automation technologies is anticipated to increase. The focus on improving productivity, reducing operational costs, and enhancing efficiency across various industries is driving businesses in these regions to adopt advanced automation solutions. With the expansion of industrial sectors and the shift towards smarter manufacturing practices, these emerging markets are becoming key targets for automation companies seeking to capitalize on the growing need for efficient and scalable automation systems.

Future Outlook

The future of the industrial automation market is promising, with strong growth expected over the next five years. The market will benefit from continuous technological advancements in robotics, AI, and IoT, coupled with increased regulatory support for automation initiatives. As more industries embrace automation for greater efficiency, the demand for robotic systems, automation software, and smart sensors will rise. Government policies will play a key role in driving adoption, and new applications in emerging markets will further fuel growth. Continued innovation in smart manufacturing and robotics will shape the market’s future, with automation becoming more accessible to businesses of all sizes.

Major Players

- Siemens AG

- Rockwell Automation

- ABB

- Honeywell International

- Mitsubishi Electric

- Emerson Electric Co.

- Schneider Electric

- Yokogawa Electric Corporation

- Omron Corporation

- Beckhoff Automation

- Fanuc Corporation

- Bosch Rexroth

- KUKA Robotics

- Panasonic Corporation

- Hitachi Ltd

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Manufacturing enterprises

- Industrial automation solution providers

- Technology integrators

- System integrators

- Engineering firms

- End-user industries

Research Methodology

Step 1: Identification of Key Variables

We identify critical market variables, including market size, growth drivers, and challenges, to structure the research framework.

Step 2: Market Analysis and Construction

In-depth analysis is performed on industry trends, key players, and emerging technologies to develop market forecasts and segmentations.

Step 3: Hypothesis Validation and Expert Consultation

We validate our research hypothesis by consulting industry experts, key players, and stakeholders in the industrial automation field.

Step 4: Research Synthesis and Final Output

We synthesize all findings and compile them into a comprehensive report with actionable insights, trends, and forecasts.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased Government Investment in Automation Technologies

Technological Advancements in Robotics and AI

Rising Demand for Operational Efficiency - Market Challenges

High Initial Investment Costs

Lack of Skilled Workforce in Automation Technologies

Technological Integration and Interoperability Issues - Market Opportunities

Expansion of Industry 4.0 in Manufacturing

Adoption of IoT in Automation Systems

Increased Demand for Predictive Maintenance Solutions - Trends

Shift Towards Automation in Small and Medium Enterprises (SMEs)

Integration of AI and Machine Learning in Manufacturing Processes

Growing Popularity of Autonomous Systems in Logistics - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Industrial Robots

Programmable Logic Controllers (PLC)

Supervisory Control and Data Acquisition (SCADA)

Human Machine Interface (HMI) Systems

Motion Control Systems - By Platform Type (In Value%)

Industrial Control Systems (ICS)

Automation Software

Robotic Platforms

Networking Platforms

Edge Computing Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Integrated Solutions

Modular Solutions - By End User Segment (In Value%)

Manufacturing Sector

Oil & Gas Industry

Automotive Industry

Pharmaceutical Industry

Food & Beverage Industry - By Procurement Channel (In Value%)

Direct Procurement

Private Sector Procurement

Government Tenders

Third-party Distributors

Online Bidding Platforms

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Regional Demand, Technological Innovation, Cost Structure, Adoption Rate, Regulatory Compliance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

ABB

Siemens AG

Rockwell Automation

Schneider Electric

Mitsubishi Electric

Honeywell International

Yokogawa Electric Corporation

Omron Corporation

Fanuc Corporation

Bosch Rexroth

KUKA Robotics

Panasonic Corporation

Hitachi Ltd

Beckhoff Automation

Emerson Electric Co.

- Adoption of Automation in Thai Manufacturing

- Regulations Shaping Industrial Automation in Thailand

- Growth of Automation in Thai Automotive Sector

- Government Push for Automation in Healthcare Sector

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now