Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Thailand’s last-mile delivery market is valued at approximately USD ~ billion based on a recent historical assessment, driven by rapid e commerce growth, rising consumer expectations for fast delivery, and increased adoption of digital retail platforms. Expanding urban population density, investments in logistics infrastructure, and development of technology-enabled delivery management systems further strengthen the market. The growth of modern retail, online grocery platforms, and consumer electronics sales accelerates parcel volumes, creating sustained demand for last-mile delivery services and integrated urban distribution networks.

Major last-mile delivery operations are concentrated in Bangkok, Chiang Mai, and Phuket due to dense population centers, commercial activity, and strong transportation connectivity. Bangkok serves as the primary logistics hub with extensive road networks, access to major airports, and proximity to large retail markets. Chiang Mai functions as a key regional hub for northern Thailand, supporting both B2C and B2B delivery networks. Phuket’s tourism driven logistics needs create high demand for parcel and express deliveries. These urban centers attract leading delivery providers due to operational efficiency, infrastructure accessibility, and high parcel throughput potential.

Market Segmentation

By Service Type

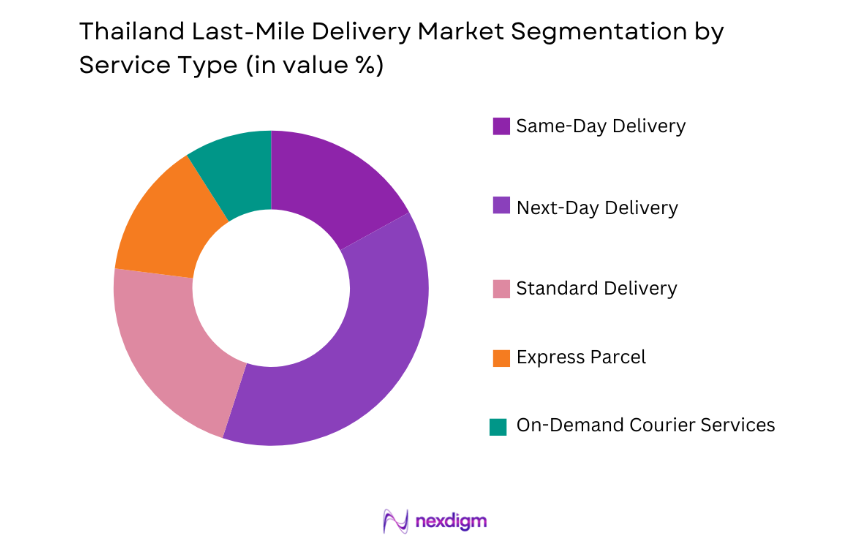

Thailand Last-Mile Delivery Market is segmented by product type into same-day delivery, next-day delivery, standard delivery, express parcel, and on-demand courier services. Recently, next-day delivery has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Consumers increasingly demand rapid delivery for online purchases, and retailers prioritize next-day services to enhance customer satisfaction. Urban logistics hubs, micro fulfillment centers, and automated sorting facilities enable efficient processing and timely dispatch. Technology integration, route optimization, and tracking systems support operational reliability. Major urban centers facilitate high-volume operations. Strategic investment in next-day delivery services strengthens market competitiveness and scalability for both e commerce and retail networks.

By End User Industry

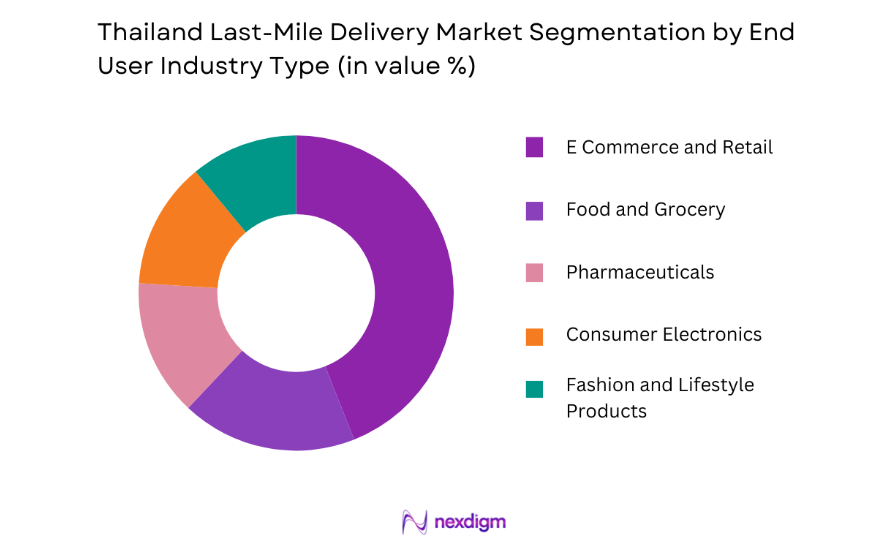

Thailand Last-Mile Delivery Market is segmented by product type into e commerce and retail, food and grocery, pharmaceuticals, consumer electronics, and fashion and lifestyle products. Recently, e commerce and retail has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. The rapid growth of online marketplaces, mobile commerce applications, and omnichannel retail strategies drives high parcel volumes. Last-mile providers leverage urban hubs, route optimization, and technology platforms to ensure timely deliveries. Investments in micro fulfillment centers and digital tracking enhance operational efficiency. E commerce demand is consistent across metropolitan and regional areas, creating scalable business opportunities. Consumer expectations for rapid and reliable delivery reinforce the dominance of e commerce and retail as the primary end user segment.

Competitive Landscape

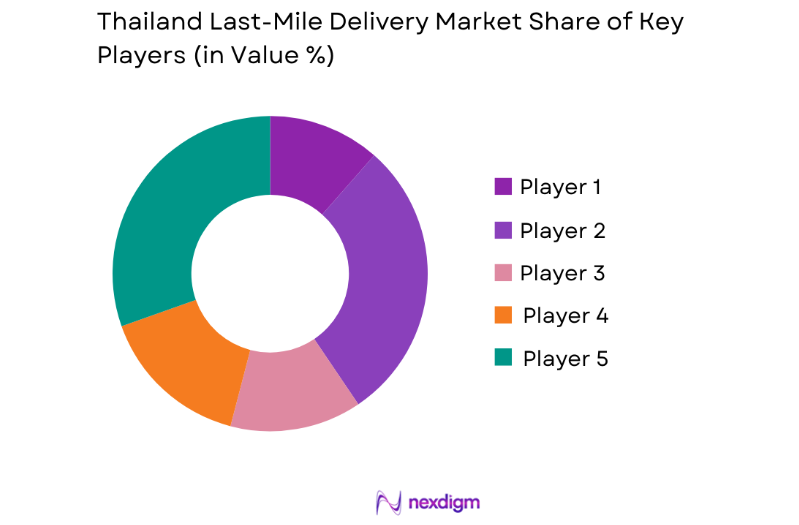

The Thailand last-mile delivery market is moderately fragmented with both multinational and domestic operators competing through technology adoption, service differentiation, and urban distribution network expansion. Strategic partnerships with e commerce platforms, retailers, and logistics providers enhance operational coverage. Companies invest in fleet expansion, micro fulfillment centers, and digital tracking solutions to increase delivery efficiency and customer satisfaction. The competitive landscape is characterized by consolidation among large players and innovative solutions targeting urban and regional delivery networks.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Size |

| J&T Express | 2015 | Indonesia | ~ | ~ | ~ | ~ | ~ |

| Ninja Van | 2014 | Singapore | ~ | ~ | ~ | ~ | ~ |

| Kerry Express | 2002 | Thailand | ~ | ~ | ~ | ~ | ~ |

| Lalamove | 2013 | Hong Kong | ~ | ~ | ~ | ~ | ~ |

| GrabExpress | 2013 | Singapore | ~ | ~ | ~ | ~ | ~ |

Thailand Last-Mile Delivery Market Analysis

Growth Drivers

Rapid Expansion of E Commerce and Omnichannel Retail Networks

Thailand Last-Mile Delivery Market growth is significantly driven by the rapid expansion of e commerce and omnichannel retail networks, which create high parcel volumes and increase the demand for urban delivery solutions. Online marketplaces, mobile commerce platforms, and omnichannel retailers rely heavily on last-mile providers to manage inventory dispatch, order fulfillment, and timely delivery to end consumers. Urban population density in Bangkok, Chiang Mai, and Phuket enables efficient routing and high-volume delivery operations. Investment in micro fulfillment centers, automated sorting facilities, and AI-based route optimization systems enhances operational efficiency and reduces delivery times. Technology integration allows providers to track parcels in real time, improving customer satisfaction. Strategic partnerships with e commerce platforms and retailers ensure consistent parcel flows and revenue stability. Growing consumer expectations for next-day and same-day delivery further strengthen the demand for advanced last-mile services. Expansion into regional urban clusters supports broader market coverage and service scalability. Providers leverage predictive analytics to manage seasonal peaks and optimize resource allocation. Integration with digital payment systems improves operational efficiency and transparency. Investments in environmentally friendly fleets reduce operational costs and align with government sustainability initiatives. Continuous enhancement of service quality, route planning, and delivery management tools maintains market competitiveness. High-volume e commerce deliveries drive capital investments in technology, micro hubs, and logistics infrastructure. Urban density enables consolidation of delivery operations, reducing transportation cost per parcel. Omnichannel expansion strengthens customer loyalty and repeat purchases. The convergence of digital retail growth, urban logistics infrastructure, and technology adoption drives sustainable last-mile market expansion. Providers increasingly focus on integrated solutions combining warehousing, dispatch, and delivery management to optimize operational performance. Urban logistics planning, micro hub deployment, and technology adoption are central to supporting rapid parcel movement and meeting consumer expectations.

Increasing Consumer Demand for Rapid Delivery and Real-Time Tracking

Thailand Last-Mile Delivery Market experiences strong growth due to increasing consumer demand for rapid delivery services and real-time shipment tracking across metropolitan and regional areas. Consumers expect same-day or next-day delivery for online purchases, which drives logistics providers to expand fleets, optimize routes, and invest in urban distribution hubs. Technology platforms offering GPS tracking, automated notifications, and delivery time estimates enhance transparency and customer satisfaction. Retailers and e commerce operators prioritize partnerships with reliable last-mile providers to maintain service quality and improve customer retention. Expansion of mobile commerce applications and urban digital infrastructure supports operational scalability and efficiency. High-frequency deliveries require advanced sorting facilities, inventory management systems, and fleet optimization tools. Consumer preference for convenience, speed, and reliable tracking encourages providers to adopt innovative delivery methods, including crowd-sourced drivers, electric vehicles, and AI-assisted dispatch. Real-time monitoring allows for proactive exception management and improves service reliability. Investment in route optimization and data analytics reduces operational costs and enhances delivery accuracy. Urban population density facilitates higher delivery volumes with reduced transit times. Technology adoption in tracking, routing, and notifications supports consistent performance across high-demand periods. Digital integration enables seamless coordination between warehouses, dispatch centers, and delivery personnel. Providers focus on minimizing delivery errors, optimizing fleet utilization, and ensuring timely order fulfillment. Expansion of regional micro hubs allows faster access to secondary cities and suburban markets. Consumer-driven demand for speed, transparency, and reliability continues to propel growth in last-mile services. Strategic technology implementation enhances both operational efficiency and customer experience. Market growth is fueled by rising digital retail adoption and elevated expectations for service quality. Continuous monitoring, route optimization, and predictive analytics improve delivery performance. Investment in advanced technology platforms strengthens competitiveness and positions providers to meet evolving consumer expectations. Digital transformation ensures scalability, efficiency, and high-quality service delivery. Expansion of delivery capacity, fleet technology, and operational planning drives sustainable growth in Thailand Last-Mile Delivery Market.

Market Challenges

Traffic Congestion and Urban Logistics Bottlenecks

Thailand Last-Mile Delivery Market faces challenges due to heavy traffic congestion and urban logistics bottlenecks, particularly in Bangkok and other metropolitan centers. Congested roads increase delivery times, operational costs, and fleet fuel consumption. Limited parking and loading areas constrain vehicle maneuverability and delay parcel drop-offs. Logistics providers must invest in route optimization software, GPS tracking, and real-time traffic monitoring to mitigate delays. Delivery scheduling and workforce allocation require careful planning to maintain service quality. Infrastructure limitations in secondary cities further impact operational efficiency. Seasonal peaks and urban growth exacerbate congestion challenges. Coordination between distribution hubs and last-mile fleets is critical for timely delivery. High urban density increases risk of delays, missed deliveries, and customer dissatisfaction. Implementation of micro hubs, e bikes, and alternative delivery methods partially alleviates bottlenecks. Technology adoption, including dynamic routing and predictive analytics, supports operational efficiency. Traffic congestion reduces productivity and limits fleet scalability. Providers must balance speed, cost, and service reliability in dense urban areas. Strategic partnerships with local authorities improve urban logistics coordination. Delivery route optimization and dynamic scheduling mitigate congestion impact. High traffic volumes increase labor requirements and operational expenditure. Optimization of vehicle capacity and scheduling improves cost-effectiveness. Urban logistics planning remains essential for maintaining competitive service standards. Investment in intelligent transportation solutions enhances last-mile delivery efficiency and reliability.

High Operational Costs and Workforce Constraints

Thailand Last-Mile Delivery Market is challenged by high operational costs and limited availability of skilled delivery personnel. Rising fuel prices, vehicle maintenance, and urban congestion increase cost per parcel delivered. Recruitment, training, and retention of delivery staff, including drivers and warehouse personnel, require significant investment. Peak season demand creates additional labor and fleet utilization pressures. Providers must adopt technology, route optimization, and automated sorting systems to reduce dependence on manual labor. Labor shortages affect service reliability and on-time delivery performance. Operational cost pressures limit profitability and ability to expand service coverage. Regulatory compliance and safety standards add additional operational complexity. Maintaining a large urban fleet increases insurance, maintenance, and management costs. Investments in driver training and workforce management systems mitigate skill gaps. Labor turnover and limited staffing reduce operational consistency and efficiency. Outsourcing and crowd-sourced delivery models help address workforce constraints. Cost management strategies, including energy-efficient fleets, are essential to maintain competitive pricing. Fleet capacity planning ensures optimal utilization while minimizing idle resources. Operational efficiency is critical to manage last-mile service costs and customer satisfaction. Technology integration in workforce allocation, performance monitoring, and task automation improves productivity. Investment in mobile workforce management platforms reduces operational delays and labor inefficiencies. Efficient operational design mitigates cost and workforce challenges while supporting service quality.

Opportunities

Expansion of Micro Fulfillment Centers and Urban Distribution Hubs

Thailand Last-Mile Delivery Market presents opportunities through the expansion of micro fulfillment centers and urban distribution hubs that enable faster deliveries, reduce transit times, and improve parcel processing efficiency. Strategic placement of these hubs in metropolitan and suburban areas allows providers to optimize routing and fleet utilization. Integration with e commerce platforms and retail networks ensures consistent parcel volumes. Investments in automation, sorting technologies, and real-time tracking enhance operational efficiency and service reliability. Expansion into secondary cities strengthens regional market coverage. Collaboration with retailers and logistics providers enables scalable and cost-effective delivery operations. Micro hubs reduce operational bottlenecks and facilitate same-day and next-day delivery services. Technology adoption enhances visibility, route planning, and customer communication. Urban hubs support sustainable growth and optimize last-mile service capacity. Consolidation of warehousing, sorting, and dispatch in micro hubs reduces handling time. Strategic hub deployment improves fleet efficiency and resource allocation. Data analytics enable predictive planning and high-volume throughput management. Integration with digital payment and tracking systems enhances customer experience. Micro fulfillment centers allow agile response to peak demand periods. Co-location with retail and e commerce partners improves operational synergy. Urban logistics efficiency drives market competitiveness and profitability. Expansion of hub networks strengthens service reliability, scalability, and customer satisfaction. Investment in micro fulfillment infrastructure supports long-term Thailand Last-Mile Delivery Market growth.

Integration of Advanced Technology and Digital Delivery Platforms

Thailand Last-Mile Delivery Market benefits from opportunities arising from integrating advanced technology and digital delivery platforms, enhancing efficiency, transparency, and customer experience. AI-based route optimization, GPS tracking, and predictive analytics improve delivery speed and reduce operational costs. Mobile applications allow real-time parcel monitoring, notifications, and flexible delivery options. Automation in sorting centers and integration with warehouses enhance throughput capacity. Data-driven insights enable predictive demand forecasting and resource allocation. Digital platforms improve coordination between couriers, dispatch centers, and e commerce partners. Technology adoption ensures compliance with service level agreements and customer expectations. Real-time monitoring reduces delays, enhances operational decision-making, and strengthens accountability. Digital integration facilitates seamless urban and regional delivery operations. Fleet management systems optimize vehicle usage and reduce fuel consumption. Cloud-based solutions allow centralized control over delivery operations. Technology-enabled communication with customers improves satisfaction and trust. Analytics support continuous improvement and process optimization. Automation reduces manual errors and increases operational efficiency. Integration with retail and e commerce platforms expands service coverage and scalability. Digital platforms enable scalable solutions for peak demand periods. Technology adoption enhances competitiveness and market positioning. Predictive analytics and automated systems ensure timely, reliable delivery. Advanced technology and digital solutions provide long-term growth potential for Thailand Last-Mile Delivery Market.

Future Outlook

Thailand Last-Mile Delivery Market is expected to grow steadily over the next five years due to continued e commerce expansion, increasing consumer expectations for fast delivery, and investments in digital and technology-enabled logistics platforms. Micro fulfillment hubs, urban distribution centers, and advanced routing technologies will enhance service efficiency. Strategic partnerships with retailers and e commerce operators will strengthen operational scalability. Regulatory support and urban infrastructure development will facilitate improved last-mile delivery services and nationwide coverage.

Major Players

- J&T Express

- Ninja Van

- Kerry Express

- Lalamove

- GrabExpress

- DHL eCommerce

- FedEx

- UPS

- Amazon Logistics

- Shopee Xpress

- Aramex

- Qxpress

- Best Express Thailand

- SCG Express

- Thai Post

Key Target Audience

- E commerce retailers

- Logistics and delivery service providers

- Food and grocery distributors

- Retail and supermarket chains

- Pharmaceutical distribution companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables include parcel volume growth, urban population density, e commerce adoption, technology integration, delivery fleet capacity, and consumer expectations for last-mile services affecting the Thailand Last-Mile Delivery Market.

Step 2: Market Analysis and Construction

Market construction involves analyzing shipment volumes, operator revenues, fleet size, urban hub distribution, and service types to develop segmentation, market size estimation, and competitive landscape.

Step 3: Hypothesis Validation and Expert Consultation

Research hypotheses are validated through consultations with last-mile delivery providers, e commerce logistics managers, industry analysts, and government agencies overseeing urban logistics and transportation infrastructure.

Step 4: Research Synthesis and Final Output

Collected data, expert insights, and secondary research are synthesized into a structured report covering Thailand Last-Mile Delivery Market size, segmentation, competitive landscape, growth drivers, challenges, opportunities, and future outlook.

- Executive Summary

- Thailand Last-Mile Delivery Market OverviewResearch Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid Growth of E-commerce and Online Retail

Urban Population Density Supporting Efficient Delivery Networks

Adoption of Digital Tracking and Route Optimization Technologies - Market Challenges

High Capital and Operational Costs for Fleet and Infrastructure

Traffic Congestion and Urban Delivery Constraints

Regulatory Compliance for Urban Logistics Operations - Market Opportunities

Expansion of Electric Vehicle and Sustainable Delivery Fleets

Partnerships Between Retailers and Specialized Last-Mile Providers

Integration of AI for Predictive Delivery and Demand Planning - Trends

Increased Adoption of Autonomous Delivery Vehicles

Integration of Smart Lockers and Micro-Distribution Hubs - Government Regulations

Urban Transport Licensing and Compliance

Data Privacy and Consumer Protection Laws

Incentives for Green and Sustainable Logistics - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Parcel Sorting and Handling Systems

Delivery Fleet Management Platforms

Route Optimization and Tracking Software

Automated Locker Systems

Temperature-Controlled Delivery Solutions - By Platform Type (In Value%)

Land Delivery Platforms

Air Delivery Platforms

Electric Vehicle Delivery Platforms

Integrated Urban Distribution Platforms - By Fitment Type (In Value%)

On-premise Delivery Solutions

Cloud-based Delivery Solutions

Hybrid Delivery Solutions

Modular Distribution Systems - By End User Segment (In Value%)

E-commerce Retailers

Food and Grocery Delivery Services

Logistics Service Providers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Fitment Type, End User Segment, Fleet Size, Technology Adoption, Geographic Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Ninja Van Thailand

SingPost Logistics Thailand

DHL eCommerce Thailand

FedEx Thailand

UPS Thailand

GrabExpress Thailand

Lalamove Thailand

J&T Express Thailand

Shopee Xpress Thailand

Amazon Logistics Thailand

Kerry Logistics Thailand

SF Express Thailand

Aramex Thailand

DB Schenker Thailand

Qxpress Thailand

- E-commerce Retailers Expanding Same-Day and Express Delivery Options

- Food Delivery Platforms Increasing Last-Mile Service Reach

- Consumers Demanding Faster and Trackable Deliveries

- Retailers Outsourcing Delivery Operations to Specialized Providers

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now