Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Thailand’s online insurance market reached approximately USD ~ billion in gross written premiums through digital channels based on recent regulatory disclosures from the Office of Insurance Commission and insurer annual statements. Expansion is driven by mobile-first consumer behavior exceeding 90 million mobile subscriptions, widespread digital payments adoption, and insurer investments in instant underwriting and electronic policy issuance platforms integrated with national digital identity verification systems and aggregator distribution ecosystems across standardized motor, health, and travel coverage categories.

Bangkok dominates Thailand’s online insurance activity due to concentration of insurers, fintech firms, and digitally literate salaried populations with high income density and broadband penetration. Secondary dominance emerges in Eastern Economic Corridor provinces such as Chonburi and Rayong supported by industrial employment clusters, expatriate communities, and advanced e-commerce logistics networks. Nationwide adoption is reinforced by Thailand’s role as a regional tourism hub requiring travel and health coverage accessible through multilingual digital insurance platforms for domestic and inbound consumers.

Market Segmentation

By Product Type

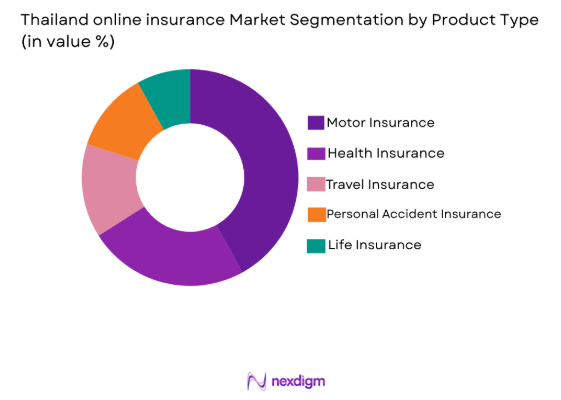

Thailand online insurance market is segmented by product type into motor insurance, health insurance, travel insurance, personal accident insurance, and life insurance. Recently, motor insurance has a dominant market share due to factors such as mandatory vehicle coverage requirements, standardized underwriting structures, and compatibility with digital distribution models that enable instant quotation and policy issuance through aggregators and insurer apps. High vehicle ownership density in urban and industrial regions sustains recurring renewal demand, while telematics-enabled pricing and claim photo assessment simplify online servicing. Consumer familiarity with motor policy comparison portals increases digital conversion relative to complex life products requiring advisory engagement. Insurers prioritize motor lines for online channels due to high transaction volume, predictable risk pools, and regulatory acceptance of electronic documentation, reinforcing structural dominance across Thailand’s digital insurance ecosystem.

By Platform Type

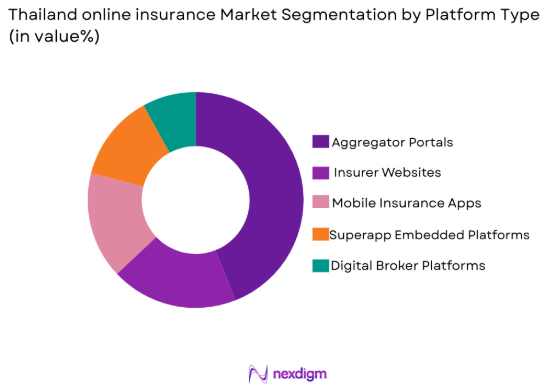

Thailand online insurance market is segmented by platform type into insurer proprietary websites, mobile insurance applications, aggregator portals, superapp embedded platforms, and digital broker platforms. Recently, aggregator portals have a dominant market share due to factors such as multi-insurer comparison capability, price transparency, and consumer trust in independent recommendation interfaces that simplify purchase decisions for standardized policies. Aggregators integrate with insurer underwriting APIs enabling instant pricing across multiple providers, reducing search costs and increasing conversion rates. Strong marketing partnerships with banks, e-commerce platforms, and automotive marketplaces funnel high-intent traffic toward aggregators during vehicle purchase or travel booking journeys. Regulatory recognition of licensed comparison intermediaries and secure digital payment gateways further supports adoption, positioning aggregators as primary digital acquisition channels within Thailand’s online insurance distribution architecture.

Competitive Landscape

Thailand’s online insurance market demonstrates moderate consolidation with leading life and non-life insurers controlling digital underwriting capacity while insurtech aggregators influence customer acquisition and pricing transparency. Large insurers leverage brand trust, capital strength, and legacy policy portfolios transitioning into digital channels, whereas specialized online insurers and aggregators compete on user experience, rapid claims automation, and price comparison visibility. Strategic partnerships between insurers, fintech platforms, and e-commerce ecosystems shape distribution reach and reinforce competitive positioning across standardized product categories.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Digital Channel Share |

| Muang Thai Life Assurance | 1951 | ~ | ~ | ~ | ~ | ~ | ~ |

| AIA Thailand | 1938 | ~ | ~ | ~ | ~ | ~ | ~ |

| Krungthai-AXA Life | 1997 | ~ | ~ | ~ | ~ | ~ | ~ |

| Roojai Insurance | 2016 | ~ | ~ | ~ | ~ | ~ | ~ |

| Sunday Insurance | 2017 | ~ | ~ | ~ | ~ | ~ | ~ |

Thailand Online Insurance Market Analysis

Growth Drivers

Mobile-First Financial Behavior and Nationwide Digital Payment Integration

Thailand’s online insurance expansion is strongly propelled by pervasive smartphone penetration and habitual use of mobile banking, e-wallets, and QR-based payment systems embedded in everyday consumer transactions across urban and semi-urban populations, enabling insurance purchase journeys to integrate seamlessly within existing digital financial ecosystems without requiring physical documentation or agent mediation. Consumers accustomed to app-based financial management increasingly prefer self-service insurance platforms offering instant quotation, policy issuance, and claims submission on handheld devices, reducing friction traditionally associated with insurance acquisition and reinforcing sustained digital channel migration across motor, health, and travel categories. National digital identity and e-KYC infrastructure allow insurers to verify customer credentials remotely and securely, eliminating onboarding barriers and accelerating straight-through underwriting processes suitable for standardized policies with predictable risk structures. Aggregator and superapp partnerships embed insurance offers into ride-hailing, e-commerce, and travel booking interfaces, enabling contextual cross-selling at moments of transactional relevance that elevate conversion efficiency and customer awareness without incremental marketing cost. Insurers benefit from lower acquisition expense ratios and scalable distribution reach through digital channels, encouraging strategic prioritization of online platforms within distribution portfolios and product design frameworks. Behavioral data from mobile usage and transaction histories supports personalized pricing and targeted product recommendations, improving risk segmentation accuracy and enhancing consumer engagement with digital insurance services. Continuous improvements in mobile network coverage and data affordability extend accessibility beyond major metropolitan areas, enabling first-time policyholders in provincial regions to access standardized protection products through smartphones. The convergence of digital payments, identity verification, and platform ecosystems therefore forms a structural growth foundation for Thailand’s online insurance market expansion.

Regulatory Enablement of Electronic Policy Issuance and Digital Intermediary Ecosystems

Thailand’s regulatory environment increasingly legitimizes and accelerates online insurance adoption through recognition of electronic contracts, digital signatures, and remote policy servicing under financial and electronic transaction frameworks administered by national authorities, allowing insurers to issue legally valid policies and endorsements entirely online without physical paperwork or branch interaction. The Office of Insurance Commission provides licensing pathways for digital brokers and comparison platforms, enabling a transparent and competitive intermediary landscape that enhances price discovery and consumer choice while maintaining supervisory oversight and data protection standards across digital distribution channels. Standardization of electronic documentation requirements and acceptance of digital claims evidence such as photographs or telematics data streamline claims settlement cycles, improving customer trust in online insurance servicing reliability and reinforcing retention within digital channels. Regulatory encouragement of insurtech innovation sandboxes enables experimentation with usage-based insurance, microinsurance, and embedded insurance models aligned with Thailand’s digital economy agenda, expanding product relevance across gig workers, SMEs, and tourism-related segments. Integration of national databases such as vehicle registration and healthcare provider networks into insurer underwriting systems reduces manual verification costs and supports automated risk assessment compatible with online distribution scale. Compliance clarity regarding cross-platform data sharing and cybersecurity safeguards facilitates partnerships between insurers, fintech firms, and e-commerce platforms that expand digital reach while maintaining consumer protection. Regulatory endorsement of electronic premium payments and refunds through licensed payment gateways further eliminates transactional barriers in digital insurance journeys. These regulatory enablers collectively reduce operational friction, enhance consumer confidence, and institutionalize online channels as a core pillar of Thailand’s insurance distribution architecture.

Market Challenges

Low Insurance Literacy and Trust Deficit in Digital Claims Reliability

Thailand’s online insurance adoption faces structural constraints from uneven insurance literacy across rural and lower-income populations who lack familiarity with policy terms, coverage scope, and claims procedures, limiting confidence in purchasing insurance without intermediary guidance and reducing digital conversion rates outside metropolitan regions. Consumers often perceive online policies as complex financial contracts requiring human explanation, particularly for health and life coverage involving exclusions and benefit conditions that are difficult to interpret through self-service interfaces alone. Historical skepticism regarding insurer claims settlement fairness reinforces reluctance to transact digitally, as customers fear inadequate post-purchase support or claim rejection without agent advocacy, weakening trust in purely online insurance relationships. Limited experience with digital documentation and claims submission processes further discourages adoption among older demographics who prefer face-to-face interaction for financial services requiring perceived assurance and accountability. Misunderstanding of coverage limits and deductible structures can lead to dissatisfaction during claims events, amplifying negative perceptions of online channels and reducing referral-based growth essential for insurance penetration. Insurers incur additional customer education and service costs to overcome comprehension barriers, diminishing efficiency advantages expected from digital distribution models. Language diversity and regional disparities in digital literacy compound communication challenges when explaining policy features through standardized online interfaces lacking localized contextualization. Consequently, literacy and trust gaps remain a persistent adoption barrier that slows Thailand’s online insurance market expansion beyond digitally fluent consumer segments.

Fragmented Legacy Systems and Integration Complexity Across Insurers

Thailand’s insurance sector contains numerous incumbent insurers operating legacy policy administration and claims systems developed for agent-based distribution models, creating technical fragmentation that complicates integration with modern digital platforms, aggregators, and real-time underwriting engines required for scalable online insurance operations. Disparate data formats, manual underwriting workflows, and non-standardized APIs impede seamless connectivity between insurers and comparison portals, delaying quotation responses and reducing customer experience quality compared with fully digital-native competitors. Modernization initiatives demand substantial capital investment and organizational transformation, including migration to cloud-based architectures and automation of underwriting and claims processes, which smaller insurers may struggle to finance without disrupting existing operations. Integration complexity increases cybersecurity exposure and regulatory compliance burdens as insurers connect multiple external platforms handling sensitive customer data across digital ecosystems. Inconsistent system capabilities also limit insurers’ ability to support usage-based or embedded insurance models that rely on real-time data ingestion from telematics or partner platforms, constraining product innovation within online channels. Operational inefficiencies from legacy environments increase processing time for endorsements and claims even when sales occur online, undermining perceived benefits of digital insurance and affecting customer retention. Vendor dependence during system upgrades introduces implementation risks and timeline uncertainty that delay digital transformation outcomes. These structural IT constraints collectively restrict Thailand’s online insurance scalability and competitive parity across the market.

Opportunities

Expansion of Embedded Insurance Through E-Commerce and Mobility Platforms

Thailand’s rapidly expanding digital commerce and mobility ecosystems present a major opportunity for online insurance providers to integrate contextual coverage offerings directly into consumer transaction journeys such as ride-hailing, vehicle purchase, travel booking, and online retail checkout environments, enabling frictionless policy attachment at the point of need without requiring separate purchase processes. Embedded models leverage platform user data and behavioral analytics to tailor coverage terms and pricing dynamically, improving relevance and conversion while reducing acquisition cost relative to traditional marketing channels. Partnerships between insurers and superapps or marketplaces extend reach to millions of active users with established digital payment credentials, accelerating first-time insurance adoption among younger and gig-economy consumers who may not proactively seek standalone policies. Standardized micro-duration products such as trip, parcel, or device protection align well with online distribution and automated underwriting frameworks, allowing insurers to scale volume with minimal marginal cost. Regulatory acceptance of digital intermediaries and electronic documentation supports embedded distribution legality and operational feasibility across Thailand’s digital economy. Data feedback from embedded transactions enhances risk modeling accuracy and customer lifetime value optimization through cross-sell opportunities into broader insurance portfolios. Platform operators also benefit from incremental revenue and enhanced user engagement, strengthening partnership incentives and ecosystem integration. Embedded insurance therefore represents a structurally scalable growth avenue capable of significantly expanding Thailand’s online insurance penetration.

Development of AI-Driven Personalized and Usage-Based Insurance Products

Advances in artificial intelligence, data analytics, and telematics technologies enable Thailand’s insurers to transition from standardized online products toward personalized and usage-based insurance offerings that align premiums and coverage with individual behavior, health metrics, or asset utilization patterns captured through digital devices and connected platforms. Such personalization increases perceived fairness and value among consumers accustomed to data-driven services, encouraging adoption of digital insurance channels that can deliver dynamic pricing and tailored benefits unavailable in traditional agent-mediated models. Telematics-based motor insurance can reward safe driving behavior recorded through smartphone sensors or vehicle devices, improving risk selection and customer engagement simultaneously within online ecosystems. Health and wellness data integration from wearable devices supports preventive insurance models offering incentives for healthy activity, appealing to younger urban populations engaged with digital health platforms. AI-enabled underwriting and claims automation reduce operational cost and settlement time, enhancing customer satisfaction and trust in online insurance servicing reliability. Personalized recommendation engines on aggregator and insurer platforms can cross-sell complementary coverage based on life-stage or consumption patterns identified through digital footprints. Regulatory innovation sandboxes facilitate experimentation with such data-driven products while ensuring consumer protection and transparency standards. The evolution toward personalized and usage-based insurance thus creates significant differentiation and growth potential for Thailand’s online insurance market.

Future Outlook

Thailand’s online insurance market is expected to sustain robust expansion driven by continued mobile financial integration, embedded insurance proliferation across digital platforms, and insurer investment in AI-enabled underwriting and claims automation. Regulatory support for electronic policy frameworks and insurtech innovation will reinforce digital distribution legitimacy. Demand growth will be supported by rising health awareness, gig-economy coverage needs, and tourism-linked insurance consumption. Competitive dynamics will intensify as aggregators and digital-native insurers expand partnerships and personalized product offerings.

Major Players

- Muang Thai Life Assurance

- Thai Life Insurance

- Bangkok Life Assurance

- Krungthai-AXA Life Insurance

- AIA Thailand

- FWD Life Insurance Thailand

- Allianz Ayudhya Assurance

- Tokio Marine Life Insurance Thailand

- ChubbSamaggi Insurance

- ViriyahInsurance

- DhipayaInsurance

- RoojaiInsurance

- Sunday Insurance

- Frank.co.th

- Rabbit Insurance Broker

Key Target Audience

- Insurance companies

- Insurtech firms

- Digital brokers

- Banking and fintech platforms

- E-commerce andsuperapp operators

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive and mobility platforms

Research Methodology

Step 1: Identification of Key Variables

Key demand, supply, regulatory, technology, and distribution variables influencing Thailand’s online insurance ecosystem were identified through insurer filings, regulatory publications, and digital platform data. Variables included digital premium volumes, channel adoption patterns, platform integration levels, and consumer behavior indicators across product categories.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using bottom-up aggregation of digital premiums reported by insurers and intermediaries, reconciled with regulatory disclosures and platform transaction estimates. Product and platform splits were modeled based on policy counts, average premiums, and channel usage patterns across Thailand.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultation with insurance executives, insurtech platform managers, and regulatory specialists to confirm channel dynamics, technology adoption levels, and competitive positioning. Assumptions regarding digital conversion and embedded insurance growth were stress-tested against operational benchmarks.

Step 4: Research Synthesis and Final Output

Validated data and insights were synthesized into structured market analysis covering size, segmentation, drivers, challenges, opportunities, and competitive landscape. Forecast implications and strategic positioning conclusions were derived from integrated quantitative and qualitative assessment of Thailand’s online insurance ecosystem.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising smartphone penetration and mobile financial behavior enabling direct digital policy purchase

Regulatory support for electronic policy issuance and remote onboarding frameworks

Expansion of embedded insurance through ecommerce and superapp ecosystems

Increasing health awareness and demand for accessible microinsurance products

Insurer investment in AI underwriting and automated claims processing - Market Challenges

Low insurance literacy in rural populations limiting digital conversion

Consumer trust concerns regarding online claims and policy servicing reliability

Fragmented legacy IT systems across insurers hindering digital integration

Price-driven competition reducing profitability in standardized online products

Regulatory compliance complexity for cross-platform digital distribution - Market Opportunities

Expansion of microinsurance for underserved gig and informal workers

AI-driven personalized insurance offerings using behavioral data

Cross-border digital insurance for tourism and expatriate segments - Trends

Growth of embedded insurance in ride-hailing and ecommerce platforms

Adoption of instant underwriting and straight-through claims settlement

Integration of telematics data in motor insurance pricing online

Shift toward subscription and usage-based insurance models

Partnerships between insurers and fintech ecosystems - Government Regulations & Defense Policy

Electronic Transactions Act enabling digital contract validity in insurance

Office of Insurance Commission digital insurance licensing frameworks

National digital identity infrastructure supporting eKYC onboarding

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Life Insurance Policies

Health Insurance Policies

Motor Insurance Policies

Travel Insurance Policies

Personal Accident Insurance Policies - By Platform Type (In Value%)

Insurer Proprietary Websites

Mobile Insurance Applications

Aggregator and Comparison Portals

Superapp Embedded Insurance Platforms

Broker Digital Platforms - By Fitment Type (In Value%)

Standalone Online Policies

Digitally Assisted Policies

Embedded Insurance Products

On-Demand Microinsurance

Subscription-Based Coverage - By EndUser Segment (In Value%)

Individual Retail Consumers

Small and Medium Enterprises

Corporate Employers

Gig Economy Workers

Expatriate Residents - By Procurement Channel (In Value%)

Direct Insurer Digital Sales

Online Aggregators

Digital Brokers

Banking and Fintech Partnerships

Ecommerce Platform Integrations - By Material / Technology (in Value %)

AI-Based Underwriting Engines

Cloud-Native Policy Administration

API Integration Frameworks

Digital Identity and eKYC Systems

Telematics and IoT Data Integration

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Product Range, Digital Platform Capability, Pricing Competitiveness, Claims Automation Level, Distribution Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Muang Thai Life Assurance

Thai Life Insurance

Bangkok Life Assurance

Krungthai-AXA Life Insurance

AIA Thailand

FWD Life Insurance Thailand

Allianz Ayudhya Assurance

Tokio Marine Life Insurance Thailand

Chubb Samaggi Insurance

Viriyah Insurance

Dhipaya Insurance

Roojai Insurance

Sunday Insurance

Frank.co.th

Rabbit Insurance Broker

- Urban salaried consumers demonstrate highest adoption due to digital literacy and income stability

- SMEs increasingly purchase group health and liability coverage via online brokers

- Gig workers adopt micro and on-demand policies aligned with flexible employment

- Expatriates utilize online platforms for language-accessible health and travel coverage

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now