Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Turkey Agricultural Equipment Market reached approximately USD ~ billion based on a recent historical assessment derived from national farm machinery production and sales statistics reported by the Turkish Statistical Institute and agricultural mechanization industry associations. Demand is driven by replacement cycles in a large tractor fleet, expansion of commercial crop production, and government-supported mechanization modernization programs. Domestic manufacturing strength in tractors and implements also sustains aftermarket and export-oriented equipment demand across diverse farming systems.

Major activity clusters are concentrated in Ankara, Konya, Bursa, Izmir, and Manisa due to dense agricultural production and established farm machinery manufacturing ecosystems. Ankara and Sakarya host leading tractor OEM assembly plants, while Konya and Izmir function as core implement manufacturing and distribution hubs. These regions benefit from strong supplier networks, export logistics infrastructure, and mechanized cereal and horticulture farming, supporting sustained equipment utilization and replacement demand across commercial agriculture zones.

Market Segmentation

By Product Type

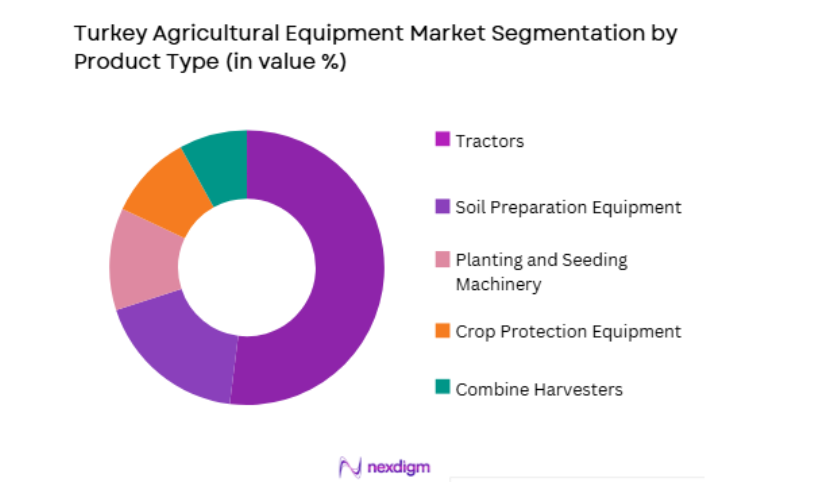

Turkey Agricultural Equipment Market is segmented by product type into tractors, combine harvesters, soil preparation equipment, planting and seeding machinery, and crop protection equipment. Recently, tractors has a dominant market share due to factors such as central role in all farm operations, extensive domestic manufacturing presence, and strong replacement demand from aging fleets across mixed farming systems. Tractors remain the primary mechanization asset in both smallholder and commercial farms, enabling multiple implement applications, transport tasks, and seasonal field operations, ensuring consistently higher sales volumes relative to specialized machinery categories.

By End-User Farm Size

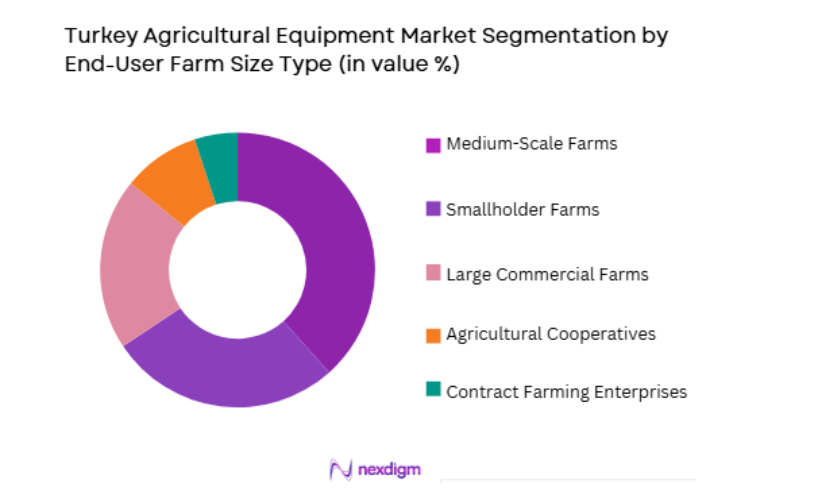

Turkey Agricultural Equipment Market is segmented by end-user farm size into smallholder farms, medium-scale farms, large commercial farms, agricultural cooperatives, and contract farming enterprises. Recently, medium-scale farms has a dominant market share due to factors such as balanced capital capacity, mechanization intensity, and transition toward commercial crop production in cereals and horticulture regions. Medium farms actively upgrade tractor horsepower and implements to improve productivity and labor efficiency, while smallholders rely more on shared machinery and large farms represent fewer but higher-value purchases.

Competitive Landscape

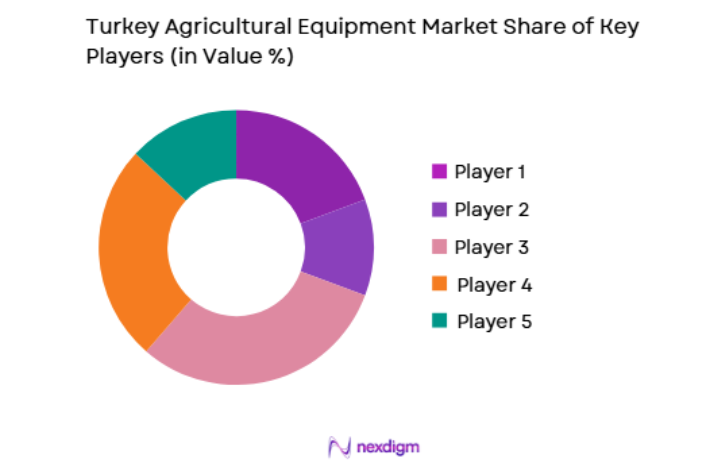

The Turkey Agricultural Equipment Market is moderately consolidated with strong influence from domestic tractor manufacturers and European agricultural machinery brands operating through local production or distribution partnerships. Domestic OEMs dominate tractor production and mid-range equipment segments, while global manufacturers supply high-horsepower tractors and advanced harvesting machinery. Competitive positioning is shaped by dealer network reach, product localization, and financing programs supporting farmer purchases across regional agricultural zones.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Local Manufacturing Presence |

| TürkTraktör | 1954 | Turkey | ~ | ~ | ~ | ~ | ~ |

| Hattat Traktör | 1998 | Turkey | ~ | ~ | ~ | ~ | ~ |

| Tümosan | 1976 | Turkey | ~ | ~ | ~ | ~ | ~ |

| Erkunt Traktör | 2003 | Turkey | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial Turkey | 1998 | Turkey | ~ | ~ | ~ | ~ | ~ |

Turkey Agricultural Equipment Market Analysis

Growth Drivers

Government Mechanization Incentives and Domestic Manufacturing Strength

Turkey Agricultural Equipment Market expansion is strongly supported by national agricultural modernization programs and investment incentives that encourage farmers to upgrade machinery fleets and adopt higher-capacity equipment across key crop regions. Public financing schemes and subsidy-linked credit access enable farmers to replace aging tractors and implements with newer, more efficient machinery produced domestically. Turkey maintains a well-established agricultural machinery manufacturing base, particularly in tractors and soil preparation implements, which reduces acquisition costs and improves equipment availability relative to fully imported markets. Domestic OEM production clusters in Ankara and surrounding regions provide strong supply chain integration for engines, transmissions, and structural components, supporting competitive pricing and aftersales service accessibility. Government policies promoting rural productivity and export-oriented agriculture further stimulate mechanization demand, particularly in cereals, oilseeds, and horticulture segments. Replacement demand from a large installed tractor population generates stable equipment sales independent of new farm expansion. Mechanization incentives also extend to precision farming and modern planting equipment, supporting technology upgrades in commercial agriculture. Domestic manufacturing capability ensures continuous product localization tailored to Turkish crop patterns and terrain conditions, improving adoption efficiency among farmers.

Commercial Farm Consolidation and Productivity Modernization

Turkey Agricultural Equipment Market growth is driven by gradual consolidation of agricultural landholdings and transition toward commercially oriented farming systems requiring higher mechanization intensity and equipment productivity. Medium and large-scale farms increasingly adopt higher horsepower tractors and advanced implements to improve operational efficiency, reduce labor dependence, and support export-quality crop production. Consolidation of fragmented farms through leasing, inheritance aggregation, and cooperative structures enables capital investment in modern machinery fleets previously inaccessible to smallholders. Commercial producers prioritize timely field operations and yield optimization, increasing demand for reliable tractors, planting machinery, and crop protection equipment. Mechanization upgrades support intensive cropping and diversified production, particularly in cereals, fruits, and vegetable cultivation regions. Labor shortages in rural areas further encourage mechanization investment to maintain productivity. Agricultural export competitiveness requires consistent quality and scale, achievable through advanced machinery adoption. Commercial farm management practices emphasize lifecycle cost efficiency, encouraging replacement of outdated equipment with fuel-efficient and precision-capable models. Equipment financing programs aligned with commercial agriculture expansion support capital acquisition. This structural shift toward consolidated and productivity-focused farming therefore strengthens sustained demand for agricultural machinery across Turkey.

Market Challenges

Currency Volatility and Import Dependency for Advanced Machinery

Turkey Agricultural Equipment Market faces significant challenges from macroeconomic currency fluctuations that increase cost of imported agricultural machinery and advanced components required for high-capacity equipment. Although domestic manufacturing covers mid-range tractors and implements, Turkey remains dependent on imports for combine harvesters, precision agriculture systems, and high-horsepower tractors. Exchange rate instability raises acquisition costs and financing burdens for farmers purchasing imported equipment. Price volatility complicates long-term investment planning and discourages machinery upgrades in economically uncertain periods. Import dependence also affects spare parts pricing and availability, increasing maintenance cost for advanced machinery fleets. Domestic OEMs relying on imported components such as transmissions, electronics, and hydraulic systems face cost pressures that may be passed to farmers. Financing institutions incorporate currency risk into lending terms, raising interest rates for equipment loans. Farmers delay replacement cycles during unfavorable currency conditions, reducing market demand stability.

Fragmented Farm Structure and Capital Constraints in Smallholder Segment

Turkey Agricultural Equipment Market growth is constrained by the persistence of fragmented landholdings and limited capital capacity among smallholder farmers who represent a substantial portion of the agricultural population. Small farms often operate at subsistence or semi-commercial levels, reducing ability to invest in modern tractors or mechanized implements. Machinery utilization rates on small plots remain low, weakening economic justification for ownership. Limited collateral and income variability restrict access to formal equipment financing channels. Smallholders frequently rely on aging machinery or shared equipment services, reducing new equipment sales potential. Government mechanization incentives often favor larger or commercially oriented farms capable of co-financing purchases. Fragmentation also limits adoption of large-capacity machinery designed for efficient operation on consolidated fields. Small farm operators prioritize affordability over technology, sustaining demand for low-horsepower or second-hand tractors rather than new equipment. Informal rental arrangements substitute ownership in many rural areas, further constraining market expansion.

Opportunities

Export Expansion of Turkish-Manufactured Tractors and Implements

Turkey Agricultural Equipment Market presents strong opportunity through international expansion of domestically manufactured tractors and implements into emerging agricultural markets across Eastern Europe, Central Asia, Africa, and the Middle East. Turkish agricultural machinery combines competitive pricing with robust engineering suited to similar agro-climatic conditions found in these regions. Export growth increases production scale, reducing unit costs and strengthening domestic industry competitiveness. Government export promotion programs and trade agreements facilitate market entry for Turkish equipment manufacturers. International distribution partnerships and localized assembly operations expand global reach of Turkish brands. Export demand also stimulates innovation and product development aligned with diverse crop systems and terrain requirements. Higher production volumes improve supplier ecosystem development and component localization. Domestic farmers benefit from export-driven cost efficiencies and improved product quality. International market presence enhances brand credibility and technology transfer opportunities. Export expansion therefore represents a major growth avenue reinforcing Turkey’s agricultural machinery sector and supporting long-term domestic market strength.

Adoption of Precision Agriculture and Smart Farming Technologies

Turkey Agricultural Equipment Market holds significant opportunity in integration of precision agriculture technologies and digital farm management systems into tractors and implements used across commercial agriculture regions. GPS-guided steering, variable-rate application, and sensor-based monitoring improve input efficiency and crop yield consistency, appealing to productivity-oriented farmers. Precision farming enables optimized fertilizer, pesticide, and seed usage, reducing operational cost and environmental impact. Government and EU-aligned agricultural sustainability initiatives encourage technology adoption in commercial farming. Domestic manufacturers increasingly integrate precision-ready features into tractors, enabling gradual adoption without full equipment replacement. Commercial farms seeking export-quality production adopt smart machinery to ensure traceability and standardized output. Telematics and remote diagnostics improve fleet management and maintenance efficiency. Data-driven agriculture supports climate resilience and resource optimization in water-constrained regions. Precision equipment demand stimulates higher-value machinery segments and technology partnerships. Integration of digital agriculture therefore offers substantial modernization opportunity for Turkey’s agricultural equipment market.

Future Outlook

The Turkey Agricultural Equipment Market is expected to grow steadily over the next five years supported by mechanization incentives, domestic manufacturing strength, and consolidation of commercial farming operations. Precision agriculture integration and export expansion of Turkish equipment will enhance technology adoption and production scale. Replacement demand from aging machinery fleets will sustain baseline growth. Financing programs and modernization policies will encourage upgrades toward higher-capacity and efficient equipment across key agricultural regions.

Major Players

- Türk Traktör

- Hattat Traktör

- Tümosan

- Erkunt Traktör

- Başak Traktör

- CNH Industrial Turkey

- AGCO Turkey

- John Deere Turkey

- Kubota Turkey

- Claas Turkey

- Same Deutz-Fahr Turkey

- Kverneland Turkey

- Lemken Turkey

- Horsch Turkey

- Alpler Agricultural Machinery

Key Target Audience

- Agricultural equipment manufacturers

- Farm machinery distributors and dealers

- Agricultural cooperatives

- Commercial farming enterprises

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural equipment financing institutions

- Precision agriculture technology providers

Research Methodology

Step 1: Identification of Key Variables

Key variables including tractor fleet size, mechanization intensity, replacement cycles, and domestic manufacturing output were identified using agricultural statistics and industry production data. Technology adoption and farm structure parameters were defined to frame demand drivers.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed by mapping machinery population with equipment sales and replacement demand across farm segments. Regional agricultural production patterns and distribution networks informed segmentation and competitive positioning.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding mechanization drivers, farm consolidation, and import dependency were validated through consultation with agricultural economists, machinery distributors, and farm operators. Findings were cross-checked with industry association publications.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative insights were synthesized into structured analysis covering market size, segmentation, and growth dynamics. Consistency checks ensured alignment with agricultural production trends and mechanization policies to produce the final market outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government incentives supporting farm mechanization modernization

Expansion of commercial agriculture and export crop production

Replacement demand from aging tractor and machinery fleet - Market Challenges

Fragmented farm structure limiting high-capacity equipment adoption

Currency volatility affecting imported machinery pricing

Climate variability impacting farm investment cycles - Market Opportunities

Growth of precision agriculture and smart farming technologies

Export potential of domestically manufactured equipment

Development of agricultural machinery leasing and rental markets - Trends

Shift toward higher horsepower tractors in commercial farming

Increasing adoption of precision planting and spraying equipment

Digital monitoring and telematics integration in farm machinery - Government regulations

Agricultural mechanization subsidy and credit programs

Emission and safety certification requirements for machinery

Import tariff and local manufacturing support policies - SWOT analysis

- Porters 5 forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Tractors

Combine Harvesters

Soil Preparation Equipment

Planting and Seeding Machinery

Crop Protection Equipment - By Platform Type (In Value%)

Wheeled Equipment

Tracked Equipment

Mounted Implements

Trailed Implements

Self-Propelled Machinery - By Fitment Type (In Value%)

Open Station Equipment

Cab Enclosed Equipment

Precision Agriculture Enabled Systems

Heavy Duty Commercial Equipment

Specialty Crop Machinery - By End User Segment (In Value%)

Smallholder Farms

Medium Scale Farms

Large Commercial Farms

Agricultural Cooperatives

- Market Share Analysis

- Cross Comparison Parameters (Equipment Portfolio Breadth, Horsepower Range, Precision Technology Integration, Price Positioning, Dealer Network Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

TürkTraktör

Hattat Traktör

Başak Traktör

Erkunt Traktör

Tümosan

CNH Industrial Turkey

AGCO Turkey

John Deere Turkey

Kubota Turkey

Claas Turkey

Same Deutz-Fahr Turkey

Kverneland Turkey

Lemken Turkey

Horsch Turkey

Alpler Agricultural Machinery

- Smallholder farms maintaining demand for low horsepower tractors

- Commercial farms adopting advanced high-capacity machinery

- Cooperatives enabling shared mechanization access

- Contract farming driving fleet modernization

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now