Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Turkey’s AI infrastructure market reached approximately USD ~ billion based on a recent historical assessment, driven by enterprise AI adoption, hyperscale data center investments, and national digital economy programs. Growth is supported by deployment of GPU clusters, AI-optimized cloud platforms, and high-performance computing facilities across telecom, finance, and public sector applications. Increasing demand for generative AI, analytics automation, and intelligent customer services has accelerated investments in AI servers, storage, and networking infrastructure by domestic and global technology providers.

Istanbul dominates Turkey’s AI infrastructure landscape due to concentration of financial institutions, telecom operators, and major data center campuses supported by international fiber connectivity and cloud interconnection hubs. Ankara follows with strong government and defense AI computing demand linked to national technology programs. Western industrial regions including Izmir and Bursa generate enterprise AI workloads across manufacturing and logistics sectors, reinforcing infrastructure deployment near industrial clusters and research universities supporting AI innovation ecosystems.

Market Segmentation

By Product Type

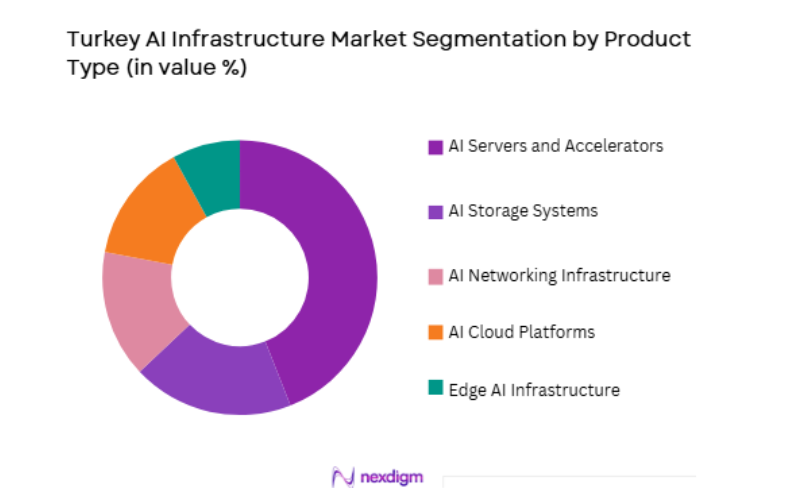

Turkey AI Infrastructure market is segmented by product type into AI servers and accelerators, AI storage systems, AI networking infrastructure, AI cloud platforms, and edge AI infrastructure. Recently, AI servers and accelerators has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Enterprise and cloud providers prioritize GPU-dense compute clusters required for model training and inference workloads. Hyperscale and telecom data centers in Istanbul have concentrated investment in AI-optimized servers, making compute infrastructure the largest spending component across Turkey’s AI ecosystem.

By End-Use Industry

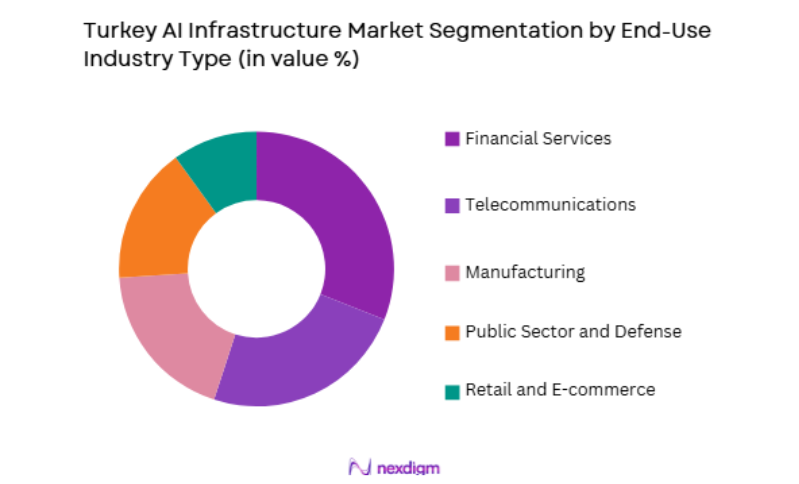

Turkey AI Infrastructure market is segmented by end-use industry into financial services, telecommunications, manufacturing, public sector and defense, and retail and e-commerce. Recently, financial services has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Turkish banks and fintech firms deploy AI for fraud detection, risk analytics, and digital banking automation requiring high-performance compute infrastructure.

Competitive Landscape

Turkey’s AI infrastructure market is moderately concentrated, led by global AI hardware vendors, cloud providers, and domestic telecom-data center operators deploying GPU clusters and AI cloud platforms. Hyperscale partnerships and telecom-cloud integration shape infrastructure expansion, while government technology programs support domestic AI computing capacity. High capital requirements for AI data centers and accelerator hardware reinforce dominance of large multinational suppliers collaborating with Turkish telecom and cloud operators.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Turkey AI Data Center Presence |

| NVIDIA | 1993 | Santa Clara, USA | ~ | ~ | ~ | ~ | ~ |

| Intel | 1968 | Santa Clara, USA | ~ | ~ | ~ | ~ | ~ |

| AMD | 1969 | Santa Clara, USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft Azure | 2010 | Redmond, USA | ~ | ~ | ~ | ~ | ~ |

| Turkcell | 1994 | Istanbul, Turkey | ~ | ~ | ~ | ~ | ~ |

Turkey AI Infrastructure Market Analysis

Growth Drivers

National AI Strategy and Public Sector Digitalization Programs

Turkey’s AI infrastructure expansion is strongly driven by coordinated national artificial intelligence and digital transformation strategies that prioritize domestic computing capacity, public sector AI adoption, and development of sovereign data processing capabilities across government, defense, and strategic industries. National AI roadmaps emphasize creation of high-performance computing centers, public data platforms, and AI research infrastructure to support analytics, automation, and decision systems across ministries and public agencies. Government investment programs have funded establishment of national AI computing clusters and data centers supporting smart city, healthcare analytics, and defense intelligence applications requiring large-scale GPU processing and storage capacity. Public procurement initiatives favor domestic or locally hosted AI infrastructure deployments to ensure data control and cybersecurity compliance, accelerating domestic data center expansion. Integration of AI into e-government services, security monitoring, and administrative analytics platforms has increased sustained demand for AI compute resources within public institutions.

Enterprise AI Adoption Across Finance, Telecom, and Digital Services Economy

Turkey’s private sector digital economy, led by financial services, telecommunications, and e-commerce platforms, is rapidly integrating artificial intelligence into customer analytics, fraud detection, personalization, and network optimization functions that depend on scalable computing and data infrastructure. Turkish banks and fintech firms deploy machine learning models requiring GPU-accelerated compute clusters and high-throughput storage systems for transaction analytics and risk modeling workloads. Telecom operators implement AI-driven network optimization, predictive maintenance, and customer experience analytics that generate continuous data streams requiring AI processing infrastructure. E-commerce and digital service platforms adopt recommendation engines, conversational AI, and demand forecasting systems necessitating cloud-based AI compute capacity. Enterprise adoption of generative AI tools for marketing, customer support, and content automation further expands demand for inference infrastructure across corporate environments.

Market Challenges

High Cost and Import Dependence of AI Accelerator Hardware

Turkey’s AI infrastructure development faces significant constraints arising from reliance on imported GPU accelerators and high-performance computing hardware supplied by a limited number of global semiconductor vendors, exposing infrastructure projects to currency volatility, supply limitations, and geopolitical technology restrictions. AI training and inference systems depend heavily on specialized processors such as GPUs and AI accelerators that are not manufactured domestically, increasing capital costs for Turkish data center operators and enterprises deploying AI clusters. Currency depreciation and import pricing fluctuations elevate procurement expenses for AI servers and networking equipment, reducing affordability of large-scale AI infrastructure expansion. Global supply shortages and export controls affecting advanced AI chips can delay deployment timelines for Turkish AI computing projects. Domestic alternatives in AI hardware manufacturing remain limited, constraining local value creation within the AI infrastructure supply chain. High upfront investment requirements for accelerator-dense data centers increase financial risk for domestic operators with smaller capital bases compared to global hyperscalers.

Skilled AI Infrastructure Engineering and Data Center Expertise Gaps

Expansion of AI infrastructure in Turkey is constrained by shortages of specialized engineering talent required for deployment, operation, and optimization of high-performance computing clusters, AI data centers, and distributed cloud architectures supporting machine learning workloads. AI infrastructure engineering requires expertise in GPU cluster design, parallel computing, high-speed networking, and data center thermal management, skills that remain scarce within Turkey’s workforce relative to demand growth. Universities and technical programs produce software engineers and data scientists, but training in large-scale AI infrastructure and HPC operations is less developed. Competition from global technology firms for experienced AI engineers increases talent retention challenges for domestic operators. Insufficient expertise can delay deployment of AI clusters and reduce performance efficiency of installed infrastructure. Operation of accelerator-dense data centers requires specialized cooling and power optimization knowledge, increasing skill requirements.

Opportunities

Regional AI Data Center Hub Development Bridging Europe and Middle East

Turkey holds strategic geographic positioning between Europe and the Middle East that enables development of AI infrastructure hubs serving regional digital markets requiring localized computing capacity for AI applications, cloud services, and data processing across neighboring economies. Istanbul’s connectivity to international fiber routes and proximity to multiple regional markets makes it suitable for AI data center expansion targeting cross-border cloud and AI workloads. Regional enterprises and service providers lacking domestic AI infrastructure may utilize Turkish facilities for latency-sensitive applications and data processing. Development of regional AI hubs can attract foreign investment and hyperscale partnerships seeking diversified infrastructure locations outside traditional European centers. Government incentives supporting technology zones and data center investments can strengthen Turkey’s role as regional AI computing gateway.

AI Integration in Manufacturing and Smart Industry Transformation

Turkey’s industrial base across automotive, textiles, electronics, and logistics sectors presents substantial opportunity for expansion of AI infrastructure supporting smart manufacturing, predictive maintenance, and industrial automation applications requiring localized high-performance computing and edge-AI systems integrated with production environments. Industrial AI adoption requires real-time data processing from sensors, robotics, and production lines necessitating deployment of on-premise or edge AI infrastructure across factories and logistics hubs. Manufacturing enterprises implementing quality inspection vision systems, demand forecasting, and supply chain optimization models require dedicated compute clusters and AI storage platforms. National industry modernization initiatives encourage adoption of intelligent production technologies that depend on AI processing capabilities.

Future Outlook

Turkey’s AI infrastructure market is expected to expand significantly over the next five years, driven by enterprise AI adoption, national digital strategies, and regional data center investments. Continued deployment of GPU clusters and AI cloud platforms will increase domestic computing capacity. Industrial AI and smart city initiatives will diversify demand.

Major Players

- NVIDIA

- Intel

- AMD

- Microsoft Azure

- Turkcell

- Türk Telekom

- Oracle Cloud

- Google Cloud

- IBM

- Huawei

- Dell Technologies

- Hewlett Packard Enterprise

- Lenovo

- Equinix

- Supermicro

- Financial institutions

Key Target Audience

- Telecommunications operators

- Manufacturing enterprises

- E-commerce platforms

- Defense and security agencies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Cloud service providers

Research Methodology

Step 1: Identification of Key Variables

AI compute capacity, accelerator deployment, data center infrastructure, and enterprise adoption sectors were identified. National AI strategy, telecom infrastructure, and industrial digitalization factors shaping Turkey’s AI infrastructure demand were mapped.

Step 2: Market Analysis and Construction

Primary and secondary data from technology vendors, telecom operators, and policy programs were synthesized to construct Turkey’s AI infrastructure value chain. Segment shares and competitive dynamics were derived through infrastructure deployment analysis.

Step 3: Hypothesis Validation and Expert Consultation

Infrastructure growth drivers and adoption patterns were validated through consultations with AI engineers, cloud architects, and data center specialists. Assumptions were cross-verified with observed Turkish AI deployment trends.

Step 4: Research Synthesis and Final Output

Validated insights were integrated into a structured framework covering segmentation, competition, drivers, challenges, and opportunities. Outputs were reviewed for alignment with Turkey’s digital economy and AI infrastructure development trajectory.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

National AI strategy and digital transformation programs

Expansion of hyperscale and colocation data centers

Enterprise adoption of AI analytics and automation - Market Challenges

High capital costs of AI hardware infrastructure

Energy supply and cooling constraints in data centers

Shortage of advanced AI and HPC engineering talent - Market Opportunities

Sovereign AI cloud and national data platforms

AI edge deployment in smart cities and industry

Public sector AI infrastructure modernization - Trends

Shift toward GPU-accelerated AI data centers

Growth of hybrid AI cloud and edge architectures - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AI Compute Servers (GPU & Accelerator-based Systems)

AI Storage Infrastructure (High-performance Data Lakes)

AI Networking Infrastructure (High-speed Interconnects)

AI Cloud Platforms (AI PaaS & ML Platforms)

AI Edge Infrastructure (On-device & Edge AI Systems) - By Platform Type (In Value%)

Hyperscale Data Center AI Infrastructure

Enterprise On-premise AI Infrastructure

Cloud-based AI Infrastructure

Edge AI Infrastructure

Hybrid AI Infrastructure - By Fitment Type (In Value%)

Greenfield AI Data Center Deployment

Brownfield AI Upgrade of Existing Data Centers

On-premise Enterprise AI Integration

Edge Site AI Enablement - By End User Segment (In Value%)

Large Enterprises & Conglomerates

Government & Public Sector

Telecom & Digital Service Providers

- Market Share Analysis

- Cross Comparison Parameters (AI Compute Capability, Data Center Scale, Sovereign AI Compliance, Industry AI Solutions, Cloud & Edge Integration)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Turkcell

Türk Telekom

Vodafone Turkey

Netaş

KoçSistem

Havelsan

Aselsan

Turkish Aerospace Industries

Huawei

NVIDIA

Intel

IBM

Microsoft

Amazon Web Services

Oracle

- Enterprises investing in AI-ready compute clusters

- Government building national AI data platforms

- Telecom operators deploying edge AI capabilities

- Universities expanding AI research infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now