Download PDF

Download PDFMarket Overview

Turkey cloud infrastructure market reached approximately USD ~ billion based on a recent historical assessment, driven by enterprise digitization programs, domestic data center investments, and expanding consumption of scalable compute and storage services across finance, telecom, retail, and public institutions. Hyperscale cloud deployments, hybrid architecture adoption, and regulatory data localization requirements strengthened infrastructure demand, while growth in digital payments, streaming, and e commerce platforms increased utilization of virtualized and containerized infrastructure environments across sectors.

Istanbul and Ankara dominate Turkey cloud infrastructure deployments due to dense fiber connectivity, concentration of financial institutions, government agencies, and large enterprises, and proximity to major data center clusters supporting national digital services. Istanbul’s role as a regional interconnection hub linking Europe and Asia attracts hyperscale availability zones and colocation campuses, while Ankara’s government cloud and defense IT ecosystems sustain sovereign infrastructure demand. Izmir and Bursa are emerging secondary nodes as industrial digitalization and regional enterprise cloud adoption expand.

Market Segmentation

By Product Type

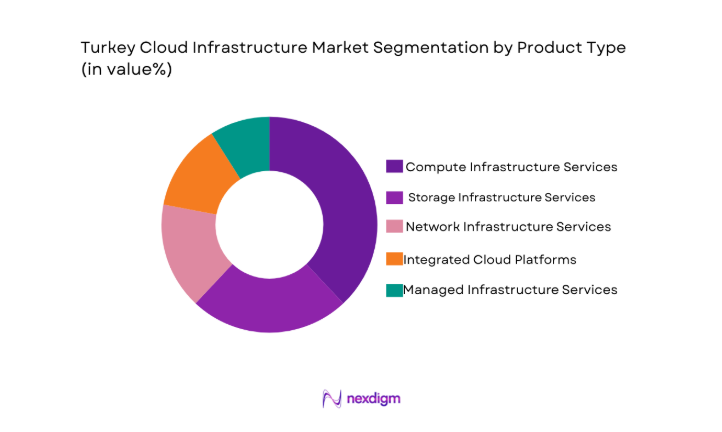

Turkey cloud infrastructure market is segmented by product type into compute infrastructure services, storage infrastructure services, network infrastructure services, integrated cloud platforms, and managed infrastructure services. Recently, compute infrastructure services has a dominant market share due to factors such as enterprise migration of mission critical workloads, virtualization expansion, hyperscale data center capacity growth, and strong demand for scalable processing environments supporting analytics, artificial intelligence, financial transactions, and digital platforms across telecom, banking, retail, and public sector ecosystems.

By Platform Type

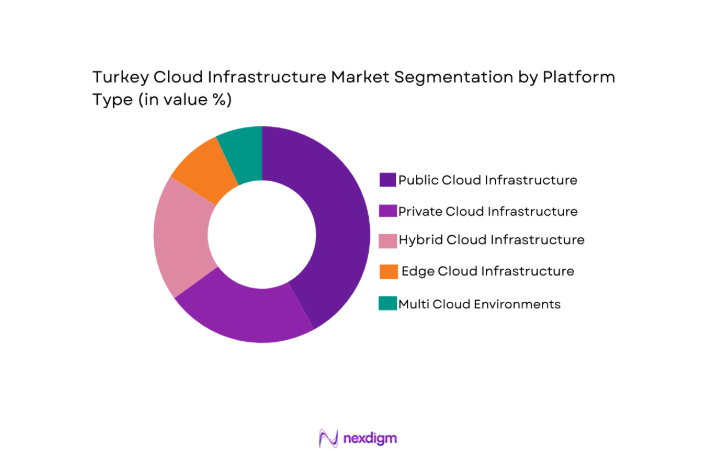

Turkey cloud infrastructure market is segmented by platform type into public cloud infrastructure, private cloud infrastructure, hybrid cloud infrastructure, edge cloud infrastructure, and multi cloud environments. Recently, public cloud infrastructure has a dominant market share due to factors such as hyperscaler regional availability zones, pay as you use consumption models, rapid enterprise onboarding, elastic scalability requirements, and strong adoption among financial services, digital commerce, and software sectors seeking high availability, geographic redundancy, and cost optimized infrastructure without capital investment constraints.

Competitive Landscape

Turkey cloud infrastructure market shows moderate consolidation where telecom operators and global hyperscalers control large scale infrastructure capacity while domestic data center firms and managed service providers support localized and regulated deployments. Partnerships between telecom carriers and hyperscalers shape national availability zones, and enterprise adoption is influenced by provider ecosystems, compliance readiness, and service breadth across compute, storage, and networking platforms.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Local Data Center Presence |

| Turkcell | 1994 | Istanbul, Turkey | ~ | ~ | ~ | ~ | ~ |

| Türk Telekom | 1995 | Ankara, Turkey | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | Redmond, USA | ~ | ~ | ~ | ~ | ~ |

| Amazon Web Services | 2006 | Seattle, USA | ~ | ~ | ~ | ~ | ~ |

| Google Cloud | 2008 | Mountain View, USA | ~ | ~ | ~ | ~ | ~ |

Turkey Cloud Infrastructure Market Analysis

Growth Drivers

National Data Localization and Sovereign Cloud Policies

Turkey cloud infrastructure market expansion is strongly supported by regulatory frameworks requiring sensitive financial, governmental, and personal data to be hosted within national borders, compelling enterprises and public institutions to adopt domestically located cloud infrastructure rather than offshore hosting environments. These regulations encourage hyperscale providers and telecom operators to build local availability zones, increasing domestic infrastructure capacity and reducing latency for critical applications. Financial services institutions, payment processors, and public digital platforms require compliant hybrid cloud architectures that combine private and public infrastructure hosted in certified Turkish data centers. Sovereign cloud frameworks also support defense, healthcare, and e government workloads that must remain under national jurisdiction and controlled operational governance. Public procurement guidelines prioritize certified local providers, creating sustained demand for national cloud platforms and government community clouds. Localization mandates also incentivize domestic colocation investment and interconnection hubs linking enterprises to compliant cloud zones. Enterprises transitioning from legacy IT to cloud environments must select providers meeting national certification and residency requirements, reinforcing domestic infrastructure utilization. International hyperscalers partner with Turkish telecom operators and data center firms to meet localization compliance, accelerating national infrastructure development. The regulatory environment therefore acts not only as a compliance driver but also as a structural catalyst for long term domestic cloud infrastructure expansion across sectors.

Enterprise Digital Transformation and Hybrid Cloud Adoption

Turkey cloud infrastructure demand is driven by large enterprises and mid market firms modernizing IT architectures to support digital platforms, analytics, and customer facing services that require scalable and resilient infrastructure environments. Organizations migrating from on premise hardware to virtualized and containerized workloads adopt hybrid cloud models combining private compliance controlled environments with public cloud scalability. Financial institutions deploy hybrid cloud to support digital banking, fraud analytics, and regulatory reporting systems. Telecom operators transform into digital service providers delivering cloud platforms, IoT services, and content distribution supported by scalable infrastructure. Retail and e commerce firms require elastic compute capacity for seasonal demand peaks and omnichannel operations. Manufacturing and logistics sectors integrate cloud infrastructure with automation and industrial analytics platforms. Hybrid cloud orchestration and multi cloud connectivity increase demand for network and software defined infrastructure layers. Managed cloud services are adopted to address skills shortages and operational complexity. These digital transformation programs require continuous infrastructure scaling and modernization, sustaining long term cloud infrastructure investment across Turkey’s enterprise ecosystem.

Market Challenges

Currency Volatility and Capital Intensive Infrastructure Investment

Turkey cloud infrastructure development requires large upfront investment in data centers, servers, networking hardware, and energy systems typically priced in foreign currency, exposing providers to exchange rate risk and cost escalation. Fluctuating currency values increase procurement costs for imported infrastructure equipment and hyperscale technologies, complicating pricing stability for cloud services sold in local currency. Domestic providers face financial pressure to maintain competitive pricing while covering rising capital and operational expenditure. Hyperscalers entering the market must evaluate long term currency exposure and hedging strategies when establishing regional facilities. Enterprise customers may delay migration or scale decisions due to uncertain cloud pricing linked to infrastructure costs. Financing of large data center campuses becomes more complex in volatile macroeconomic conditions. Energy costs, also influenced by currency fluctuations, further increase operational expenses for infrastructure providers. Smaller domestic operators may struggle to sustain expansion or modernization without foreign investment or partnerships. These financial uncertainties create structural barriers to rapid infrastructure scaling despite strong demand growth across sectors.

Skilled Cloud Engineering and Cybersecurity Workforce Shortage

Turkey cloud infrastructure adoption is constrained by limited availability of experienced professionals capable of designing, deploying, and operating complex hybrid and multi cloud environments and securing them against advanced threats. Enterprises migrating workloads require architects, DevOps engineers, and cloud security specialists who understand virtualization, container orchestration, and software defined infrastructure technologies. Domestic providers must recruit and retain highly trained personnel to maintain hyperscale grade service reliability and compliance. Public sector digitalization initiatives also compete for skilled workforce resources, intensifying talent shortages. Cybersecurity expertise is critical due to increased attack surface associated with cloud adoption and national critical infrastructure hosting. Skills gaps slow migration timelines and increase reliance on managed service providers. Training and certification programs have not yet matched the pace of infrastructure deployment expansion. International providers entering the market face localization requirements that limit external staffing flexibility. Workforce shortages therefore restrict operational scalability and increase service costs across the cloud infrastructure ecosystem.

Opportunities

AI and High Performance Computing Infrastructure Expansion

Turkey cloud infrastructure market has significant growth potential through deployment of specialized compute clusters and accelerated processing environments supporting artificial intelligence, machine learning, and advanced analytics workloads across finance, manufacturing, healthcare, and public research sectors. Enterprises increasingly require GPU enabled infrastructure and parallel processing platforms for predictive modeling, automation, and data intensive applications. Universities and research institutions demand high performance computing resources for scientific simulations and innovation programs. National digital transformation strategies prioritize AI capability development, encouraging domestic infrastructure investment. Hyperscale providers can introduce specialized AI cloud zones with optimized networking and storage architectures. Telecom operators can integrate edge AI infrastructure for real time analytics and 5G services. Domestic data center firms can differentiate through HPC hosting and colocation services. Government funding for digital innovation programs can stimulate demand for advanced compute infrastructure. As AI adoption accelerates across industries, demand for high density compute environments will expand Turkey’s cloud infrastructure capacity and technological sophistication.

Edge Cloud Infrastructure for 5G and Industrial Digitalization

Turkey cloud infrastructure market will expand through deployment of distributed edge computing nodes supporting low latency applications in manufacturing, logistics, smart cities, and telecom services. 5G networks require localized compute resources near users and devices to enable real time processing for automation, robotics, and connected systems. Industrial sectors adopting Industry 4.0 technologies need edge infrastructure integrated with factory operations and sensor networks. Telecom operators can monetize 5G by offering edge cloud platforms to enterprises. Smart transportation, energy management, and urban monitoring applications require regional edge data processing capacity. Edge nodes complement central cloud data centers by reducing latency and bandwidth usage. Domestic providers can deploy micro data centers across industrial regions such as Bursa and Izmir. Government smart city initiatives and industrial digitalization policies support distributed infrastructure investment. Expansion of edge cloud ecosystems will therefore create new infrastructure segments and broaden Turkey’s cloud deployment architecture beyond centralized hyperscale facilities.

Future Outlook

Turkey cloud infrastructure market is expected to expand steadily over the next five years as enterprises deepen digital transformation and AI adoption increases compute demand. Continued hyperscale investment and domestic data center expansion will strengthen national capacity and resilience. Regulatory support for localization and sovereign cloud will sustain public and financial sector adoption. Growth of 5G and industrial digitalization will drive edge infrastructure deployment across regions.

Major Players

- Turkcell

- Türk Telekom

- VodafoneTurkey

- Microsoft

- Amazon Web Services

- Google Cloud

- Oracle

- Huawei Cloud

- Alibaba Cloud

- Equinix

- Digital Realty

- Radore

- MedNautilus

- KoçSistem

- SabancıDx

Key Target Audience

- Cloud service providers

- Telecom operators

- Financial institutions

- Government and regulatory bodies

- Large enterprises

- Industrial manufacturing firms

- Digital commerce platforms

- Investments and venture capitalist firms

Research Methodology

Step 1: Identification of Key Variables

Key demand and supply variables including infrastructure capacity, enterprise adoption patterns, regulatory drivers, and provider ecosystems were mapped to define the Turkey cloud infrastructure market boundaries and structural components.

Step 2: Market Analysis and Construction

Data from provider disclosures, infrastructure deployments, enterprise IT spending, and sector digitalization indicators were synthesized to construct market sizing, segmentation, and competitive structure across cloud platforms and technologies.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including cloud architects, telecom infrastructure specialists, and enterprise IT leaders validated adoption trends, technology drivers, and deployment patterns shaping Turkey’s cloud infrastructure evolution.

Step 4: Research Synthesis and Final Output

Validated insights were integrated into structured market analysis covering segmentation, competitive landscape, growth drivers, challenges, and opportunities to produce an evidence based Turkey cloud infrastructure market assessment.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid enterprise digital transformation initiatives

Expansion of domestic data center capacity

Government cloud first and localization policies - Market Challenges

Currency volatility affecting infrastructure investments

Data sovereignty and compliance complexity

Skills shortages in cloud engineering - Market Opportunities

Localization driven sovereign cloud offerings

AI and high performance computing infrastructure demand

Edge infrastructure for 5G and IoT services - Trends

Hyperscaler regional data center expansion

Shift toward platform based infrastructure services

Increasing managed cloud outsourcing - Government Regulations & Defense Policy

Data localization and personal data protection requirements

National cybersecurity and critical infrastructure standards

Public sector cloud procurement frameworks - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Compute Infrastructure Services

Storage Infrastructure Services

Network Infrastructure Services

Integrated Cloud Platforms

Managed Infrastructure Services - By Platform Type (In Value%)

Public Cloud Infrastructure

Private Cloud Infrastructure

Hybrid Cloud Infrastructure

Edge Cloud Infrastructure

Multi Cloud Environments - By Fitment Type (In Value%)

Greenfield Cloud Deployments

Legacy System Migration

Cloud Native Deployments

Containerized Infrastructure

Virtualized Infrastructure - By End User Segment (In Value%)

Large Enterprises

Small and Medium Enterprises

Public Sector Organizations

Telecom and Digital Service Providers

Financial Institutions - By Procurement Channel (In Value%)

Direct Vendor Contracts

Managed Service Providers

System Integrators

Cloud Marketplaces

Telecom Bundled Services - By Material / Technology (in Value %)

Virtualization and Hypervisor Technologies

Software Defined Networking

Software Defined Storage

Container Orchestration Platforms

AI Enabled Infrastructure Automation

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Service Portfolio Breadth, Data Center Footprint, Hybrid Cloud Capability, Security Certifications, Pricing Models, Industry Solutions, Managed Services Depth, Local Partnerships, SLA Performance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Turkcell

Türk Telekom

Vodafone Turkey

Microsoft

Amazon Web Services

Google Cloud

Oracle

Huawei Cloud

Alibaba Cloud

Equinix

Digital Realty

Radore

MedNautilus

KoçSistem

SabancıDx

- Enterprises prioritizing scalable digital platforms

- Public sector cloud modernization programs

- Telecom operators monetizing cloud services

- Financial institutions adopting compliant hybrid cloud

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now