Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Turkey home finance market recorded approximately USD ~ billion in outstanding residential mortgage balances, according to data published by the Central Bank of the Republic of Türkiye and the Banking Regulation and Supervision Agency, expressed in USD equivalent terms. The market is driven by urban housing demand, state-supported housing loan campaigns, participation bank financing models, and expanding residential construction activity supported by domestic commercial banks.

Istanbul dominates home finance activity due to high population density, elevated property transaction volumes, and the concentration of commercial banks and participation banks. Ankara and Izmir follow due to administrative importance, urbanization, and infrastructure investment. Rapid residential development in metropolitan regions and government-backed housing initiatives reinforce lending flows. Türkiye benefits from a centralized banking system and digitized credit evaluation processes supporting mortgage origination and refinancing.

Market Segmentation

By Product Type

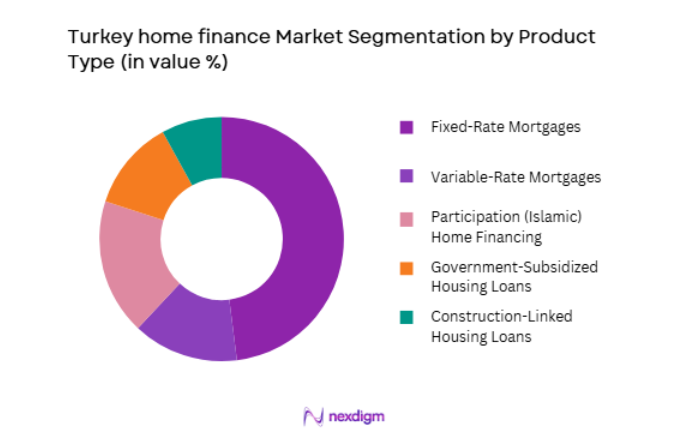

Turkey home finance market is segmented by product type into Fixed-Rate Mortgages, Variable-Rate Mortgages, Participation (Islamic) Home Financing, Government-Subsidized Housing Loans, and Construction-Linked Housing Loans. Recently, Fixed-Rate Mortgages has a dominant market share due to borrower preference for predictable repayment structures amid inflationary pressures and interest rate fluctuations. Consumers prioritize installment stability to manage household budgeting in volatile macroeconomic conditions. Commercial banks actively promote fixed-rate structures during state-supported housing campaigns. Strong brand presence of large banks and structured underwriting models reinforce their adoption.

By Lender Type

Turkey home finance market is segmented by lender type into State-Owned Banks, Private Commercial Banks, Participation Banks, Housing Development Administration Financing, and Non-Bank Financial Institutions. Recently, State-Owned Banks has a dominant market share due to their strong capital backing, government-linked housing initiatives, and large branch networks across urban and semi-urban regions. State banks often lead subsidized mortgage campaigns supporting first-time buyers and middle-income households. Access to low-cost funding and sovereign support enhances competitive pricing flexibility.

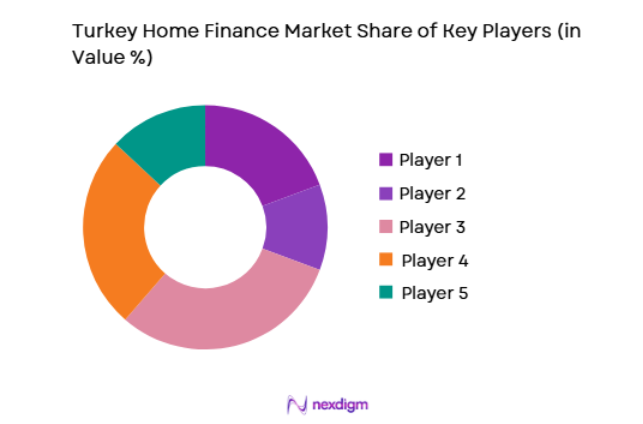

Competitive Landscape

The Turkey home finance market is dominated by large state-owned and private commercial banks with extensive nationwide branch networks and strong deposit funding bases. Participation banks hold a growing presence in Shariah-compliant housing finance, while non-bank lenders maintain limited penetration. Competitive intensity is influenced by periodic government-backed mortgage campaigns and interest rate adjustments. Consolidation dynamics are shaped by capital adequacy requirements and access to central bank liquidity mechanisms.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Mortgage Loan Book (USD) |

| Ziraat Bankası | 1863 | Ankara, Türkiye | ~ | ~ | ~ | ~ | ~ |

| Türkiye İş Bankası | 1924 | Istanbul, Türkiye | ~ | ~ | ~ | ~ | ~ |

| Garanti BBVA | 1946 | Istanbul, Türkiye | ~ | ~ | ~ | ~ | ~ |

| Halkbank | 1933 | Ankara, Türkiye | ~ | ~ | ~ | ~ | ~ |

| VakıfBank | 1954 | Istanbul, Türkiye | ~ | ~ | ~ | ~ | ~ |

Turkey Home Finance Market Analysis

Growth Drivers

Government-Backed Housing Campaigns and Public Lending Incentives

Strong government intervention in housing finance through subsidized credit campaigns represents a primary growth driver of the Turkey home finance market. State-owned banks frequently launch low-rate mortgage programs targeting first-time buyers and middle-income households, stimulating transaction volumes in residential real estate markets. Publicly supported housing initiatives linked to the Housing Development Administration create additional financing demand. These campaigns temporarily reduce borrowing costs, accelerating loan disbursements and refinancing activity. Developers align project launches with subsidized credit periods, strengthening property sales momentum. Public confidence in state-backed institutions increases borrower participation during campaign cycles. Regulatory coordination between fiscal authorities and banking supervisors ensures liquidity provision to sustain lending expansion. Media-driven awareness of state programs enhances borrower outreach. This structured policy-driven financing environment significantly shapes mortgage growth dynamics across Türkiye’s housing sector.

Urbanization and Demographic Housing Demand Expansion

Rapid urban migration toward major metropolitan regions continues to drive structural demand for residential housing finance across Türkiye. Growing household formation, supported by a young population profile, increases demand for mortgage-backed property ownership. Infrastructure investments in transportation, healthcare, and education expand urban residential zones, encouraging new housing developments requiring financing solutions. Middle-income families increasingly pursue apartment ownership in organized housing complexes. Real estate developers respond with large-scale projects aligned with urban transformation initiatives. Banking institutions expand branch presence and digital channels in high-growth regions to capture mortgage demand. Participation banks contribute to inclusive financing through Shariah-compliant structures. Rising rental costs motivate households to shift toward ownership models supported by mortgage financing.

Market Challenges

Macroeconomic Instability and Interest Rate Volatility Exposure

The Turkey home finance market faces persistent challenges from macroeconomic volatility and fluctuating benchmark interest rates that directly affect mortgage affordability and credit risk management. Inflationary conditions can elevate nominal lending rates, increasing repayment burdens for borrowers. Rapid interest rate adjustments influence demand cycles and refinancing patterns. Currency depreciation affects construction material costs, indirectly influencing property prices and loan-to-value dynamics. Banks must recalibrate credit scoring and stress-testing models to manage portfolio risk. Elevated uncertainty may reduce long-term borrowing commitments among households. Funding costs for lenders can rise during periods of liquidity tightening. Volatility may discourage foreign capital inflows into real estate financing structures. These macroeconomic variables collectively introduce risk considerations that constrain stable expansion of mortgage lending activity.

Regulatory Controls and Credit Allocation Restrictions

The Turkey home finance market operates under prudential regulations governing credit growth, loan-to-value ratios, and capital adequacy that can limit expansion flexibility. Supervisory authorities may introduce targeted restrictions on mortgage lending to control inflationary pressures or manage financial stability. Changes in reserve requirements and liquidity rules influence banks’ capacity to extend long-term housing loans. Compliance costs increase with evolving reporting and consumer protection standards. Participation banks must adhere to additional Shariah governance frameworks. Regulatory interventions aimed at macroeconomic stabilization may periodically restrict certain borrower segments. Banks adjust underwriting criteria in response to supervisory guidance, potentially tightening credit access. Such regulatory dynamics create operational constraints while maintaining systemic resilience within the Turkish financial system.

Opportunities

Expansion of Participation Banking and Shariah-Compliant Housing Finance

Increasing demand for participation-based financial services presents substantial opportunities for growth within the Turkey home finance market. Participation banks provide asset-backed murabaha and ijara structures that align with Islamic finance principles. Growing consumer awareness of Shariah-compliant products broadens the addressable borrower base. Regulatory recognition of participation banking strengthens institutional credibility. Integration of digital application systems enhances accessibility to compliant housing finance. Developers collaborate with participation banks for structured project financing solutions. Cross-border capital flows from Gulf countries may support participation lending expansion. Differentiated branding strategies attract conservative investor segments. This specialized financing niche strengthens diversification and resilience within the broader mortgage ecosystem.

Digital Mortgage Platforms and Automated Credit Analytics

Technological modernization across Turkey’s banking sector creates opportunities to enhance mortgage processing efficiency and borrower accessibility. Automated credit scoring tools reduce approval timelines and operational costs. Digital document verification and remote onboarding simplify application procedures. Mobile banking platforms enable real-time loan tracking and installment management. Data analytics improve risk segmentation and portfolio monitoring. Integration with property valuation databases enhances underwriting accuracy. Fintech partnerships expand distribution channels for younger demographics. Cybersecurity upgrades reinforce trust in online transactions. These digital innovations position Turkey’s home finance providers to scale lending operations efficiently while improving customer experience and operational transparency.

Future Outlook

The Turkey home finance market is expected to experience gradual structural growth over the next five years, supported by urban housing demand and continued public sector involvement in mortgage campaigns. Digital transformation within retail banking will further streamline loan origination. Participation banking expansion is anticipated to diversify financing structures. Regulatory oversight will remain central to balancing credit growth with financial stability objectives across the housing finance ecosystem.

Major Players

- ZiraatBankası

- Türkiye İş Bankası

- Garanti BBVA

- Halkbank

- VakıfBank

- Yapı Kredi

- QNB Finansbank

- DenizBank

- TEB

- Akbank

- Albaraka Türk

- Kuveyt Türk

- Türkiye Finans

- ING Türkiye

- Şekerbank

Key Target Audience

- First-time homebuyers

- Real estate developers

- Construction companies

- Participation banks

- Mortgage brokers

- Housing cooperatives

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key indicators including outstanding mortgage balances, lender segmentation, product types, regulatory controls, and housing transaction volumes were identified through official central bank and supervisory publications.

Step 2: Market Analysis and Construction

A bottom-up evaluation of residential lending volumes across state-owned and private banks was conducted to structure the overall Turkey home finance market framework.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary conclusions were validated through consultation with banking professionals, credit risk managers, and housing finance specialists to ensure regulatory and operational alignment.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative findings were consolidated into a structured analytical report integrating segmentation, competitive positioning, and forward-looking evaluation.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government Backed Housing and Urban Transformation Projects

Expansion of Participation Banking and Islamic Finance

Rising Urbanization and Residential Construction Activity - Market Challenges

High Interest Rate Environment and Inflationary Pressure

Currency Volatility Impacting Borrower Confidence

Tightened Credit Assessment and Lending Standards - Market Opportunities

Growth in Sharia Compliant Home Financing Products

Digitalization of Loan Origination and Approval Processes

Increased Demand for Energy Efficient Housing Finance - Trends

Shift Toward Participation Banking Mortgage Products

Growing Use of Digital Mortgage Application Channels - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Conventional Mortgage Loans

Participation Banking Home Financing

Fixed Rate Housing Loans

Variable Rate Housing Loans

Government Supported Housing Finance Programs - By Platform Type (In Value%)

State Owned Banks

Private Commercial Banks

Participation Banks

Mortgage Brokerage Firms

Digital Lending Platforms - By Fitment Type (In Value%)

Purchase Financing

Refinancing Solutions

Construction Linked Housing Finance

Urban Transformation Financing - By End User Segment (In Value%)

First Time Home Buyers

Middle Income Households

Real Estate Investors

- Market Share Analysis

- Cross Comparison Parameters (Interest Rate Structure, Participation Profit Share Model, Loan to Value Ratio, Repayment Tenure Flexibility, Government Subsidy Eligibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Ziraat Bankasi

Halkbank

VakifBank

Isbank

Garanti BBVA

Yapi Kredi

Akbank

QNB Finansbank

DenizBank

Turkiye Finans Participation Bank

Kuveyt Turk Participation Bank

Albaraka Turk Participation Bank

Emlak Katilim Bankasi

TEB Bank

ING Bank Turkey

- Increasing Demand for Fixed Installment Stability

- Preference for Government Supported Housing Schemes

- Rising Interest in Participation Based Financing Models

- Greater Sensitivity to Interest Rate Fluctuations

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now