Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Turkey Medical Tourism Market reached about USD ~ billion based on recent historical assessment, reflecting spending captured through Türkiye’s health tourism and tourism statistics framework. Demand is supported by internationally accredited private hospitals, competitive procedure pricing, extensive airline connectivity, and integrated treatment plus accommodation packages. Additional momentum comes from strong capabilities in hair transplantation, dental care, cosmetic surgery, ophthalmology, and fertility treatment, alongside state backed promotion through national health tourism platforms and authorization systems for cross border care providers.

Istanbul remains the leading hub because it combines the country’s deepest hospital network, multilingual patient coordination teams, large airport capacity, and concentration of premium private providers. Antalya follows through its resort infrastructure and strong elective treatment appeal, while Ankara benefits from advanced tertiary care and large hospital campuses. Izmir also holds importance for dental, aesthetic, and rehabilitation services. These cities dominate because they pair medical capability with hospitality ecosystems, easier international access, and stronger institutional credibility for foreign patients.

Market Segmentation

By Product Type

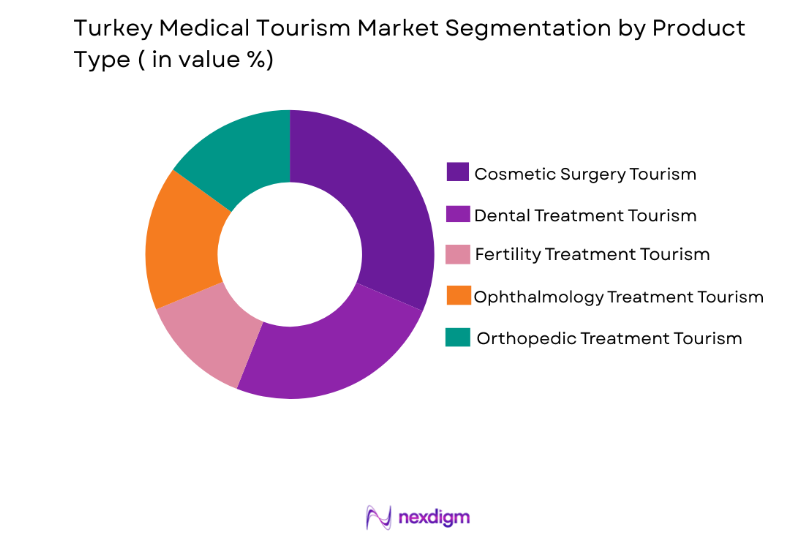

Turkey Medical Tourism Market is segmented by product type into cosmetic surgery tourism, dental treatment tourism, fertility treatment tourism, ophthalmology treatment tourism, and orthopedic treatment tourism. Recently, cosmetic surgery tourism has a dominant market share due to strong international recognition of Turkish surgeons, dense private clinic capacity in Istanbul, shorter waiting times, and bundled service models combining consultation, procedure, hotel stay, and transfers. Hair transplantation and aesthetic procedures also benefit from high digital visibility, patient referrals, and price competitiveness against Western Europe and the Gulf. This sub segment is further strengthened by specialized care pathways, multilingual coordinators, and recovery oriented hospitality services that make elective travel easier for overseas patients.

By Platform Type

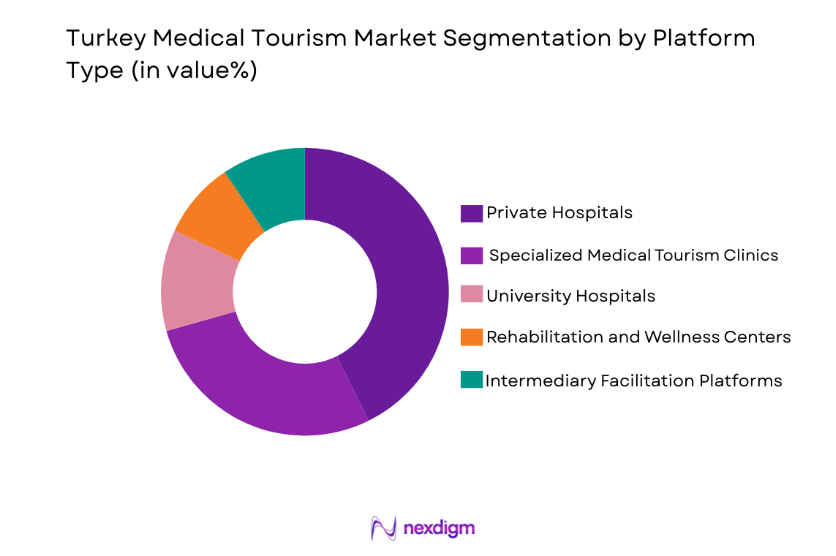

Turkey Medical Tourism Market is segmented by platform type into private hospitals, specialized medical tourism clinics, university hospitals, rehabilitation and wellness centers, and intermediary facilitation platforms. Recently, private hospitals have a dominant market share due to stronger international branding, wider specialty coverage, better accommodation standards, and more mature foreign patient departments. They also tend to hold recognized accreditations, maintain translator networks, and offer faster scheduling for elective procedures than many public institutions. Their scale supports packaged pricing, airport transfer coordination, teleconsultation follow up, and integrated diagnostics under one roof. These advantages make private hospitals the preferred platform for international patients seeking predictable quality, convenience, and end to end treatment management.

Competitive Landscape

Turkey Medical Tourism Market remains moderately consolidated, with large private hospital groups and specialized aesthetic care brands exerting strong influence over international patient acquisition, pricing discipline, clinical reputation, and partnership networks. Istanbul based operators hold a structural advantage because they combine brand familiarity, broader specialty depth, and stronger foreign patient departments. Competition is shaped by accreditation, multilingual coordination, airport accessibility, digital lead generation, and the ability to offer bundled treatment journeys instead of standalone procedures.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | International Patient Services |

| Acibadem Healthcare Group | 1991 | Istanbul, Türkiye | ~ | ~ | ~ | ~ | ~ |

| Memorial Health Group | 2000 | Istanbul, Türkiye | ~ | ~ | ~ | ~ | ~ |

| Medical Park Hospitals Group | 1993 | Istanbul, Türkiye | ~ | ~ | ~ | ~ | ~ |

| Medicana Health Group | 1992 | Istanbul, Türkiye | ~ | ~ | ~ | ~ | ~ |

| Florence Nightingale Hospitals | 1989 | Istanbul, Türkiye | ~ | ~ | ~ | ~ | ~ |

Turkey Medical Tourism Market Analysis

Growth Drivers

Accredited Private Healthcare Capacity and Treatment Affordability

Turkey’s medical tourism market is expanding because internationally focused private hospitals and specialty clinics can deliver complex and elective procedures at prices that remain attractive relative to many Western destinations. This cost advantage is not based only on lower procedure fees, but also on integrated packages that combine consultations, diagnostics, surgery, recovery support, transfers, and lodging into a simpler purchase for foreign patients. The country also benefits from a large physician base with experience in cosmetic surgery, dental care, ophthalmology, bariatrics, and fertility services, all of which are highly relevant to self paying international travelers. Ministry backed authorization rules for international health tourism providers have improved market structure by making credentialing, supervision, and service expectations clearer for overseas patients. Large hospital groups in Istanbul, Ankara, Antalya, and Izmir reinforce this advantage through multilingual coordinators, digital inquiry systems, and faster scheduling than patients often experience in their home systems. Airline connectivity and visa accessibility further reduce friction for patients who want treatment with limited planning time. Together, affordability, provider scale, treatment breadth, and repeat patient referrals continue to widen Turkey’s appeal in cross border healthcare markets.

Government Promotion, Air Connectivity, and Digital Patient Acquisition

Another major growth engine is the way Turkey has aligned destination marketing, aviation access, and online patient acquisition around healthcare travel. National platforms such as HealthTürkiye and ministry led promotion have increased international visibility while giving patients clearer entry points to authorized providers and formal service channels. Istanbul Airport’s global route network and the strength of Turkish Airlines materially improve accessibility from Europe, the Middle East, Central Asia, and Africa, which shortens travel times and supports short stay treatment decisions. Private hospital groups have complemented this by investing in multilingual websites, remote consultations, online quotation systems, and dedicated foreign patient call centers that convert demand more efficiently than traditional referral only models. Social media visibility is especially important in hair restoration, dental aesthetics, and cosmetic procedures, where before and after portfolios and patient testimonials strongly shape provider selection. Tourism infrastructure also matters because recovery can be combined with hotel capacity, companion travel, and post procedure stays in established urban and coastal destinations. These combined capabilities create a smoother patient journey from search to discharge. That continuity supports higher conversion, broader source market reach, and stronger year round international demand for medical travel to Turkey.

Market Challenges

Regulatory Fragmentation and Quality Consistency Across Providers

A central challenge for Turkey’s medical tourism market is maintaining consistent service quality across a rapidly expanding provider base that ranges from flagship hospital groups to smaller clinics and intermediaries. While the Ministry of Health has formal authorization rules for international health tourism, patient experience can still vary in language support, clinical coordination, follow up protocols, infection control transparency, and aftercare arrangements. This inconsistency matters because cross border patients usually pay out of pocket and judge the entire journey, not just the clinical act itself. Reputation can therefore be damaged by weaker operators even when the strongest institutions perform well. The market also depends on clear distinctions between authorized facilities and less structured promotional channels online, where aggressive advertising may blur perceived differences in quality. Coordination between treatment providers, hotels, transport firms, and facilitators is not always standardized, which can create operational gaps during arrival, recovery, or complication management. Stronger audit visibility and patient protection mechanisms remain important. Without tighter consistency, Turkey risks reputational leakage that can slow premium market expansion and weaken trust among high value international patients.

Geopolitical Sensitivity and Dependence on International Travel Flows

Turkey’s medical tourism performance is exposed to shifts in regional politics, airline disruptions, security perceptions, and source market currency pressure that can alter patient flows quickly. Unlike purely domestic healthcare demand, cross border treatment volumes depend on consumer confidence in travel as much as confidence in medicine. A diplomatic dispute, a sudden visa concern, or transport interruption can immediately affect bookings, especially for elective procedures that patients can postpone or redirect to competing destinations. The market is therefore more vulnerable to external shocks than local hospital demand. Source market concentration can deepen that risk when providers rely heavily on a limited set of countries or facilitators for referrals. Exchange rate volatility can help price competitiveness in headline terms, but it can also complicate provider cost structures, imported device pricing, and revenue planning. High exposure to international mobility means hospitals and clinics must continuously invest in diversification, branding, and service resilience. That raises commercial pressure even for established operators with strong clinical reputations and increases long term marketing costs across the entire market.

Opportunities

Expansion of High Value Specialty Packages Beyond Core Aesthetics

A major opportunity lies in moving beyond the strongest elective categories and scaling higher value specialty packages in fertility, orthopedics, cardiology, oncology support services, ophthalmology, and rehabilitation. Turkey already has tertiary care depth and large hospital campuses capable of supporting more complex international cases than the market is currently known for. Broadening the case mix would improve revenue per patient and reduce overreliance on aesthetic procedures that face intense price comparison online. It would also help reposition the destination toward more clinically sophisticated care pathways with stronger physician led referral potential. Integrated packages can be designed around diagnosis, procedure, recovery, interpreter services, companion arrangements, and remote follow up, which is important for patients traveling long distances. Cities such as Ankara and Izmir are well placed to benefit because they can market advanced hospital infrastructure alongside lower congestion than Istanbul. Better specialization branding would strengthen differentiation. Over time, this could raise both credibility and spending intensity across the market while attracting more insurer linked and specialist referral flows.

Digital Aftercare, International Partnerships, and Secondary City Development

Another strong opportunity is the creation of deeper digital aftercare systems and formal overseas partnerships that make Turkey’s medical tourism offering more trusted and scalable. Many international patients worry less about the procedure itself than about continuity of care after returning home, so structured telemedicine follow up, shared records, and documented post treatment pathways can become a major differentiator. This is particularly valuable in dentistry, fertility, bariatrics, and ophthalmology, where staged care or monitoring may continue after travel. Partnership models with foreign clinics, employer programs, diaspora networks, and facilitator platforms can widen referral channels while lowering customer acquisition costs. Secondary cities such as Antalya and Izmir can also capture more demand by pairing strong hospital assets with recovery friendly environments and less congestion than Istanbul. Better geographic spread would reduce concentration risk for the national market. It would also encourage new investment in multilingual staffing, rehabilitation services, and destination-linked care ecosystems. As providers improve these capabilities, they can compete more effectively for patients who prioritize safety, documented outcomes, and smoother recovery experiences.

Future Outlook

Turkey Medical Tourism Market is positioned for continued expansion over the next five years as hospital groups deepen specialty offerings and digital patient management becomes more standardized. Growth is likely to be supported by stronger formalization of authorized providers, wider use of teleconsultation and aftercare tools, and broader international marketing through national platforms. Demand should remain favorable across elective and specialty procedures as treatment affordability, airline connectivity, and bundled service design continue to attract cross border patients. Competitive advantage will increasingly depend on accreditation, clinical outcomes, multilingual service quality, and the ability to extend demand beyond Istanbul into other capable treatment cities.

Major Players

- AcibademHealthcare Group

- Memorial Health Group

- Medical Park Hospitals Group

- Medicana Health Group

- Florence Nightingale Hospitals

- Anadolu Medical Center

- Liv Hospital

- Hisar Hospital Intercontinental

- Dunyagoz Hospitals Group

- Estetik International

- VM Medical Park

- Bayindir Healthcare Group

- Yeditepe University Hospital

- Koc University Hospital

- Istanbul Aesthetic Center

Key Target Audience

- Hospitals and specialty clinic operators

- Medical tourism facilitators and care coordinators

- Private equity investors and venture capitalist firms

- Government and regulatory bodies

- Health insurance and cross border reimbursement providers

- Healthcare technology and telemedicine solution providers

- International patient referral networks and travel platforms

Research Methodology

Step 1: Identification of Key Variables

The study defines Turkey Medical Tourism Market boundaries by treatment type, service platform, patient flow characteristics, and provider structure. Key variables include treatment demand patterns, provider capability, city level concentration, pricing architecture, regulatory authorization, and international patient support systems. Secondary variables such as digital lead generation, accreditation, and travel accessibility are also mapped.

Step 2: Market Analysis and Construction

The market framework is built by combining official tourism and health tourism signals with provider level positioning and treatment category relevance. Segment splits are structured across product type and platform type to reflect actual demand channels in medical travel. Competitive assessment is then layered through hospital group scale, service breadth, and foreign patient reach.

Step 3: Hypothesis Validation and Expert Consultation

Working assumptions are tested against published institutional information, hospital network profiles, and policy level guidance on international health tourism authorization. The validation stage checks whether demand drivers, city dominance patterns, and treatment category leadership align with observable provider capabilities. Contradictions are removed before drafting the final analytical narrative.

Step 4: Research Synthesis and Final Output

All findings are synthesized into a report structure covering overview, segmentation, competition, market analysis, outlook, and buyer relevance. The final output prioritizes consistency between market logic, segment design, and company positioning. This ensures that Turkey Medical Tourism Market conclusions remain decision ready for strategic, investment, and expansion use cases.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Competitive treatment pricing compared with Western Europe and North America

Expansion of internationally accredited hospitals and specialty clinics

Strong government promotion of healthcare tourism and international patient services - Market Challenges

Regulatory compliance complexities for international healthcare services

Dependence on geopolitical stability and international travel flows

Quality standard variation across smaller healthcare providers - Market Opportunities

Expansion of advanced cosmetic and reconstructive surgery services

Growth in integrated wellness and rehabilitation tourism offerings

Rising demand for dental and fertility treatment packages among international patients - Trends

Integration of digital health platforms for international patient management

Increasing partnerships between hospitals and global medical travel agencies - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Cosmetic Surgery Tourism

Dental Treatment Tourism

Fertility Treatment Tourism

Orthopedic Treatment Tourism

Cardiology Treatment Tourism - By Platform Type (In Value%)

Private Hospitals

Specialized Medical Tourism Clinics

Accredited Multispecialty Hospitals

Rehabilitation and Wellness Centers

Integrated Healthcare Campuses - By Fitment Type (In Value%)

Hospital-Based Treatment Packages

Clinic-Based Treatment Packages

Wellness and Rehabilitation Packages

Integrated Medical Travel Packages - By End User Segment (In Value%)

International Patients

Regional Cross-Border Patients

Medical Travel Facilitators

- Market Share Analysis

- Cross Comparison Parameters (Treatment Specialization, Hospital Accreditation Status, International Patient Services, Pricing Packages, Facility Infrastructure, Global Partnerships, Treatment Success Rate)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Acibadem Healthcare Group

Memorial Health Group

Medical Park Hospitals Group

Florence Nightingale Hospitals

Medicana Health Group

Anadolu Medical Center

Liv Hospital Group

Hisar Hospital Intercontinental

Koç University Hospital

Yeditepe University Hospital

Bayindir Healthcare Group

VM Medical Park Hospitals

Estetik International

Dunyagoz Hospitals Group

Istanbul Aesthetic Center

- Rising inflow of international patients seeking cost-effective elective procedures

- Increasing demand from Middle Eastern and European medical travelers

- Growth in partnerships between hospitals and global medical tourism facilitators

- Expanding role of private hospitals in specialized international treatment programs

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now