Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Turkey Semiconductor Infrastructure Market reached approximately USD ~ billion based on a recent historical assessment, supported by fabrication equipment procurement, cleanroom construction, and compound semiconductor processing capacity expansion. Public semiconductor investment programs exceeding USD ~ billion across high-technology manufacturing, alongside automotive electronics demand and defense avionics chip initiatives, have accelerated infrastructure spending across wafer processing, packaging, and fab utilities ecosystems.

Istanbul, Ankara, and Kocaeli dominate Turkey Semiconductor Infrastructure Market due to concentration of electronics manufacturing clusters, defense semiconductor programs, and national research fabrication facilities. Istanbul hosts semiconductor design and equipment integration firms, Ankara anchors defense microelectronics and research fabs, while Kocaeli supports automotive electronics manufacturing supply chains, creating localized demand for wafer processing infrastructure, packaging lines, and advanced semiconductor facility engineering services.

Market Segmentation

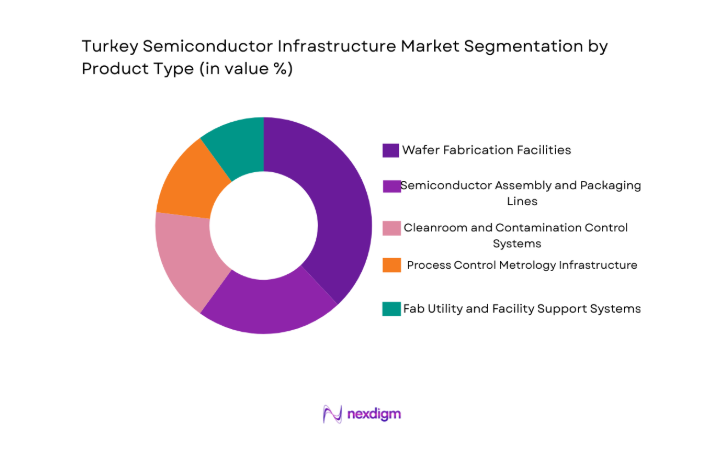

By Product Type

Turkey Semiconductor Infrastructure Market is segmented by product type into wafer fabrication equipment infrastructure, semiconductor assembly and packaging lines, cleanroom and contamination control systems, process control and metrology infrastructure, and fab utilities and facility support systems. Recently, wafer fabrication equipment infrastructure has a dominant market share due to factors such as national semiconductor localization initiatives, defense microelectronics fabrication programs, advanced node pilot line deployment, and growing compound semiconductor wafer processing investments, which collectively prioritize capital-intensive lithography, deposition, etch, and wafer handling infrastructure across domestic semiconductor manufacturing ecosystems.

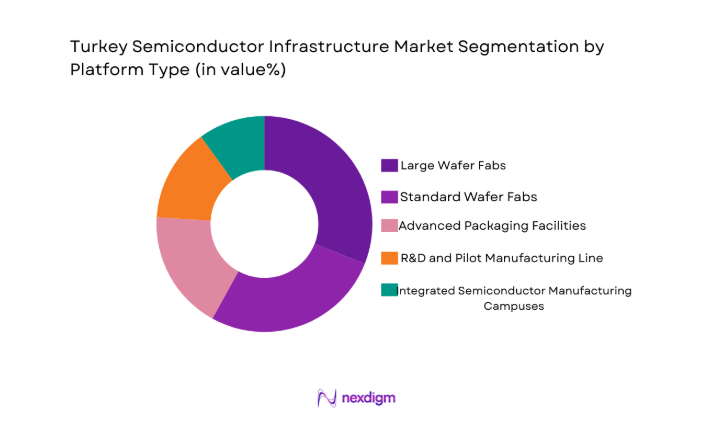

By Platform Type

Turkey Semiconductor Infrastructure Market is segmented by platform type into 200mm wafer fabrication facilities, compound semiconductor fabs, advanced packaging and test facilities, R&D and pilot manufacturing lines, and integrated semiconductor manufacturing campuses. Recently, compound semiconductor fabs have a dominant market share due to factors such as rising automotive power electronics demand, defense radar and RF chip programs, national investment in silicon carbide and gallium nitride processing, and regional positioning in power semiconductor supply chains supporting electrification and energy infrastructure technologies.

Competitive Landscape

Turkey Semiconductor Infrastructure Market exhibits moderate concentration with defense-linked electronics firms, semiconductor materials suppliers, and industrial automation providers shaping infrastructure deployment. Domestic players collaborate with global semiconductor equipment vendors and engineering contractors to deliver fabrication, packaging, and facility solutions, while government-supported semiconductor initiatives strengthen local ecosystem integration and strategic technology autonomy across infrastructure segments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Semiconductor Infrastructure Role |

| ASELSAN | 1975 | Ankara | ~ | ~ | ~ | ~ | ~ |

| TUBITAK BILGEM | 1983 | Gebze | ~ | ~ | ~ | ~ | ~ |

| Vestel | 1984 | Manisa | ~ | ~ | ~ | ~ | ~ |

| Nanografi | 2011 | Ankara | ~ | ~ | ~ | ~ | ~ |

| Schneider Electric Turkey | 1990 | Istanbul | ~ | ~ | ~ | ~ | ~ |

Turkey Semiconductor Infrastructure Market Analysis

Growth Drivers

National Semiconductor Localization and Strategic Autonomy Programs

Turkey Semiconductor Infrastructure Market expansion is strongly driven by state-led semiconductor localization initiatives that prioritize domestic fabrication capability, compound semiconductor processing, and defense electronics microchip production across national technology programs. Government industrial strategies have identified semiconductor manufacturing as a critical technology domain essential for supply-chain resilience, national security electronics, and advanced industrial competitiveness, leading to large-scale public investment commitments directed toward wafer processing infrastructure, cleanroom engineering, and advanced packaging capacity. Defense avionics, radar systems, and secure communications technologies require trusted semiconductor production environments, which has accelerated domestic fabrication pilot lines and compound semiconductor wafer processing facilities supported by defense procurement agencies and national research institutes. Automotive electrification trends and power electronics demand in Turkey’s manufacturing sector have reinforced the need for silicon carbide and gallium nitride fabrication infrastructure, further aligning industrial demand with localization policies focused on reducing imported semiconductor dependency. Public-private semiconductor programs encourage collaboration between domestic electronics firms, engineering contractors, and international semiconductor equipment providers to establish integrated fabrication ecosystems spanning materials, wafer processing, and packaging. Infrastructure spending is also supported by technology transfer agreements enabling adoption of advanced lithography, deposition, and metrology systems within local fabrication facilities, strengthening domestic process capability. Regional supply-chain diversification trends across Europe and Eurasia have increased Turkey’s strategic relevance as a semiconductor manufacturing and packaging location, reinforcing policy-driven infrastructure expansion. National semiconductor roadmaps emphasize vertically integrated infrastructure from materials to packaging, ensuring sustained capital deployment into fabrication equipment, cleanrooms, and utilities systems across the decade.

Defense Electronics and Automotive Power Semiconductor Demand Expansion

Turkey Semiconductor Infrastructure Market growth is significantly influenced by the expanding domestic defense electronics sector and the country’s large automotive manufacturing base, both of which require specialized semiconductor fabrication and packaging infrastructure aligned with high-reliability applications. Defense programs involving radar, guidance systems, electronic warfare, and secure communications technologies depend on compound semiconductor devices and RF microchips that require gallium nitride and silicon carbide wafer processing infrastructure, thereby stimulating investment in specialized fabrication tools, epitaxy systems, and metrology capabilities. Concurrently, automotive electrification and advanced driver electronics production in Turkey’s vehicle manufacturing ecosystem have intensified demand for power semiconductors and sensor chips, encouraging development of compound semiconductor fabs and advanced packaging facilities suited for automotive qualification standards. Infrastructure investments are therefore increasingly directed toward wafer processing lines capable of handling wide-bandgap materials and power device architectures, along with packaging systems optimized for thermal management and reliability performance. Defense procurement programs provide stable long-term demand signals that justify capital-intensive fab deployment, while automotive export supply chains support scalable semiconductor packaging capacity within industrial clusters such as Kocaeli and Bursa. Collaboration between automotive OEM suppliers, defense electronics manufacturers, and semiconductor research institutes has created integrated demand channels that reinforce infrastructure utilization across fabrication and packaging platforms. As a result, semiconductor infrastructure development aligns with dual-use technology strategies where defense and mobility electronics share fabrication ecosystems, maximizing capacity utilization and technological advancement. These sectoral demands collectively sustain continuous infrastructure modernization and expansion across Turkey’s semiconductor manufacturing landscape.

Market Challenges

Dependence on Imported Semiconductor Equipment and Materials Supply Chains

Turkey Semiconductor Infrastructure Market faces structural constraints arising from reliance on imported semiconductor manufacturing equipment, specialty chemicals, lithography systems, and high-purity materials essential for fabrication and packaging operations. Advanced semiconductor production requires precision lithography tools, deposition reactors, etch systems, and metrology instruments primarily produced by global technology leaders outside Turkey, creating procurement cost pressures and supply-chain vulnerabilities for domestic infrastructure projects. Import dependence also extends to silicon wafers, compound semiconductor substrates, and photolithography materials that are critical for wafer processing, limiting domestic value addition and increasing exposure to international trade restrictions or export control regimes affecting semiconductor technologies. Infrastructure deployment timelines are affected by equipment sourcing complexity, technology licensing requirements, and limited local servicing capabilities for high-precision semiconductor tools, which collectively raise operational risks for emerging fabrication facilities. Currency volatility and import financing costs further amplify capital expenditure burdens in a sector already characterized by multibillion-dollar facility investments, constraining the pace of infrastructure scaling. Domestic semiconductor ecosystem maturity remains early stage relative to global leaders, reducing bargaining power in equipment procurement and limiting technology transfer opportunities necessary for advanced node manufacturing capability. Local materials production initiatives exist but remain insufficient to fully substitute imported semiconductor-grade substrates and chemicals, prolonging dependency cycles. These factors collectively challenge sustainable infrastructure expansion and competitiveness within global semiconductor manufacturing value chains.

Skilled Semiconductor Engineering Workforce Constraints and Technology Capability Gap

Turkey Semiconductor Infrastructure Market development is impeded by shortages of highly specialized semiconductor engineers, process technologists, and fabrication facility experts required for advanced semiconductor manufacturing operations. Semiconductor fabrication involves complex process integration across lithography, deposition, etch, and metrology stages that demand deep technical expertise typically cultivated within mature semiconductor ecosystems, which Turkey is still developing. Limited availability of experienced fab engineers and semiconductor materials scientists affects infrastructure commissioning, yield optimization, and process stability in emerging domestic fabrication facilities, potentially delaying production readiness and reducing operational efficiency. Academic and vocational training pipelines in microelectronics and semiconductor manufacturing remain relatively small compared to global semiconductor hubs, constraining talent supply for expanding infrastructure programs. Technology capability gaps also exist in advanced node process integration, EUV lithography adoption, and heterogeneous packaging technologies, requiring extensive international collaboration and technology transfer arrangements that may be restricted by geopolitical or intellectual property considerations. Workforce constraints extend to cleanroom facility engineering, semiconductor equipment maintenance, and process automation specialists essential for fab operations. As infrastructure capacity expands, talent scarcity risks underutilization of installed fabrication and packaging assets, affecting economic viability of semiconductor investments. Bridging these capability gaps requires sustained education investment, industry partnerships, and long-term skill development strategies aligned with semiconductor manufacturing complexity.

Opportunities

Regional Compound Semiconductor Manufacturing Hub for Power Electronics and RF Devices

Turkey Semiconductor Infrastructure Market has a significant opportunity to position itself as a regional manufacturing hub for compound semiconductor devices serving automotive electrification, renewable energy, and defense RF electronics markets across Europe and Eurasia. Compound semiconductor materials such as silicon carbide and gallium nitride are increasingly critical for high-efficiency power conversion, electric mobility, radar, and telecommunications systems, creating strong demand for specialized wafer processing and packaging infrastructure. Turkey’s automotive production base and defense electronics sector provide anchor demand for power and RF semiconductors, enabling economies of scale for compound semiconductor fabs and associated materials supply chains. Infrastructure investment in epitaxy reactors, wide-bandgap wafer processing lines, and high-temperature packaging facilities can support both domestic consumption and export markets within regional supply chains seeking diversification from traditional semiconductor manufacturing geographies. Geographic proximity to European electronics manufacturers and customs union trade access strengthens Turkey’s potential role as a near-shore compound semiconductor supplier. Government semiconductor localization incentives and technology partnership programs further enhance the attractiveness of establishing compound semiconductor fabrication clusters within existing industrial zones. Collaboration with global semiconductor equipment and materials firms can accelerate technology adoption and capability maturity in wide-bandgap processing. As power electronics demand grows across electrification and energy infrastructure sectors, Turkey can leverage integrated demand channels to scale compound semiconductor infrastructure sustainably.

Advanced Packaging and Semiconductor Assembly Ecosystem Serving Regional Electronics Manufacturing

Turkey Semiconductor Infrastructure Market can capitalize on the expanding need for advanced semiconductor packaging, testing, and assembly services across Europe, Middle East, and Central Asia by developing a competitive regional OSAT and packaging infrastructure ecosystem. Semiconductor packaging increasingly determines device performance through heterogeneous integration, thermal management, and miniaturization technologies, creating demand for advanced packaging facilities beyond traditional semiconductor manufacturing hubs. Turkey’s strong electronics manufacturing base in consumer electronics, appliances, automotive electronics, and telecommunications equipment provides natural demand for localized semiconductor packaging services integrated with device production supply chains. Investment in advanced packaging technologies such as wafer-level packaging, system-in-package integration, and high-reliability automotive packaging can position domestic infrastructure providers as regional service partners for electronics OEMs seeking supply-chain resilience. Proximity to European markets enables reduced logistics time and cost compared with Asian packaging hubs, enhancing competitiveness for time-sensitive electronics production. Engineering procurement construction firms and industrial automation providers in Turkey can support turnkey packaging facility deployment and utilities integration, strengthening ecosystem capability. Government technology programs encouraging semiconductor assembly and testing localization further reinforce investment feasibility. As semiconductor device complexity grows, advanced packaging infrastructure offers scalable entry into higher value semiconductor manufacturing segments without requiring leading-edge wafer fabrication nodes.

Future Outlook

Turkey Semiconductor Infrastructure Market is expected to expand steadily over the next five years as national semiconductor localization policies translate into fabrication, packaging, and materials facility deployment across industrial clusters. Growth will be supported by compound semiconductor adoption, defense electronics demand, and automotive power semiconductor production requirements. Infrastructure modernization through automation and advanced process technologies will enhance domestic manufacturing capability. Regulatory incentives and regional supply-chain diversification trends will further strengthen investment momentum.

Major Players

- ASELSAN

- TUBITAK BILGEM

- Vestel

- Nanografi

- Schneider Electric Turkey

- Meteksan

- Tualcom

- Karel

- MilSOFT

- Plan S

- Arcelik

- Empa Electronics

- PAVOTEK

- Yongatek

- ASELSAN Microelectronics

Key Target Audience

- Semiconductor device manufacturers

- Automotive electronics OEMs

- Defense and aerospace companies

- Electronics manufacturing service providers

- Government and regulatory bodies

- Industrial automation suppliers

- Venture capital and investment firms

- Semiconductor materials producers

Research Methodology

Step 1: Identification of Key Variables

Key variables such as fabrication capacity, infrastructure investment flows, semiconductor end-use demand, and technology adoption were identified through secondary industrial datasets and policy documentation. Market boundaries and infrastructure components were defined across fabrication, packaging, materials, and utilities segments.

Step 2: Market Analysis and Construction

Segmental infrastructure demand was constructed by mapping semiconductor value chain activities to domestic industrial clusters and end-use sectors. Capital expenditure patterns and facility deployment indicators were synthesized to estimate market structure and segmentation.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding infrastructure dominance, platform adoption, and regional demand drivers were validated through expert interviews and industry benchmarks. Technology trends and policy impacts were cross verified with semiconductor ecosystem stakeholders.

Step 4: Research Synthesis and Final Output

Validated data and qualitative insights were integrated into structured market models describing segmentation, competitive landscape, and growth dynamics. Final outputs were synthesized into standardized market reporting formats ensuring analytical consistency.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

National semiconductor localization initiatives

Government incentives for fabrication facilities

Defense electronics and avionics demand

Automotive power semiconductor expansion

Regional supply chain nearshoring trends - Market Challenges

High capital requirements for fab infrastructure

Dependence on imported semiconductor equipment

Limited advanced node manufacturing capability

Skilled semiconductor engineering shortages

Scale constraints of domestic semiconductor demand - Market Opportunities

Development of compound semiconductor fabs

Regional semiconductor packaging hub positioning

Public private partnerships for fabrication plants - Trends

Shift toward compound semiconductor materials

Growth of advanced packaging facilities

Adoption of AI enabled fab automation

Expansion of defense semiconductor infrastructure

Integration with regional electronics supply chains - Government Regulations & Defense Policy

National semiconductor investment incentives

Strategic technology localization programs

Defense electronics domestic sourcing mandates - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Wafer Fabrication Equipment Infrastructure

Semiconductor Assembly and Packaging Lines

Cleanroom and Contamination Control Systems

Process Control and Metrology Infrastructure

Fab Utilities and Facility Support Systems - By Platform Type (In Value%)

200mm Wafer Fabrication Facilities

Compound Semiconductor Fabs

Advanced Packaging and Test Facilities

R&D and Pilot Manufacturing Lines

Integrated Semiconductor Manufacturing Campuses - By Fitment Type (In Value%)

Greenfield Fab Installations

Brownfield Capacity Expansions

Modular Semiconductor Production Units

Facility Retrofit and Modernization

Turnkey Fab Infrastructure Projects - By End User Segment (In Value%)

Integrated Device Manufacturers

Defense and Aerospace Semiconductor Programs

Automotive Electronics Semiconductor Producers

Research Institutes and Semiconductor Labs

Electronics Manufacturing Service Providers - By Procurement Channel (In Value%)

Direct OEM Procurement

Engineering Procurement Construction Contracts

Government Supported Strategic Programs

Technology Transfer Partnerships

Distributor and Integrator Channels - By Material / Technology (in Value %)

Silicon Wafer Processing Infrastructure

Gallium Nitride and Silicon Carbide Processing

Advanced Lithography and Patterning Systems

Advanced Packaging Interconnect Technologies

AI Driven Fab Automation and Control Systems

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Technology Node Capability, Wafer Size Support, Fab Scale, Automation Level, Localization Strategy, Packaging Capability, Defense Compliance, EPC Integration, R&D Collaboration)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

ASELSAN Microelectronics

TUBITAK BILGEM Semiconductor Technologies

ASELSAN Chip Manufacturing

Vestel Semiconductor Solutions

Arcelik Semiconductor Systems

Yongatek Microelectronics

Nanografi Semiconductor Materials

Meteksan Semiconductor Technologies

Tualcom Semiconductor Systems

MilSOFT Microelectronics

TAI Semiconductor Systems

Plan S Semiconductor Engineering

Karel Electronics Semiconductor Division

Empa Electronics Semiconductor

PAVOTEK Microelectronics

- Defense and aerospace programs driving fab demand

- Automotive electronics firms expanding power chip capacity

- Research institutes developing pilot fabrication lines

- Electronics manufacturers localizing semiconductor supply

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now