Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UAE Agrochemical market has witnessed considerable growth, driven by the expanding agricultural sector, which is valued at approximately USD ~ billion. The market is fueled by the increasing demand for crop protection solutions, enhanced by the UAE’s push for self-sufficiency in food production. Agrochemicals, including fertilizers, pesticides, and herbicides, are crucial to improving yield in the region’s arid climate, thereby enabling more efficient farming practices. Additionally, the focus on agricultural technology and sustainability further propels the market’s expansion, with modern practices such as precision farming gaining traction.

The market is dominated by key players in both developed and emerging regions, with strong dominance from cities like Dubai and Abu Dhabi. These regions benefit from extensive investments in infrastructure and technology, enhancing their agricultural capabilities. Additionally, proximity to international trade routes bolsters access to global agrochemical products. The UAE government has supported this development through various initiatives aimed at boosting the agricultural sector, including subsidies and research grants. The integration of green technologies and the country’s drive for food security also contribute to the growth momentum.

Market Segmentation

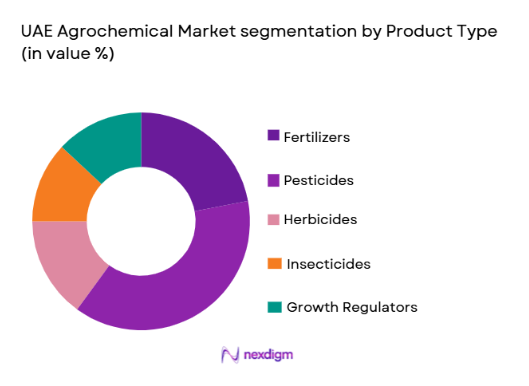

By Product Type:

UAE Agrochemical market is segmented by product type into fertilizers, pesticides, herbicides, insecticides, and growth regulators. Recently, the pesticide sub-segment has a dominant market share due to factors such as the growing demand for crop protection solutions and increasing awareness about pest-related diseases that affect agriculture. Pest management is a key concern for farmers, and the region’s hot climate exacerbates pest infestations, leading to a high demand for effective pesticides.

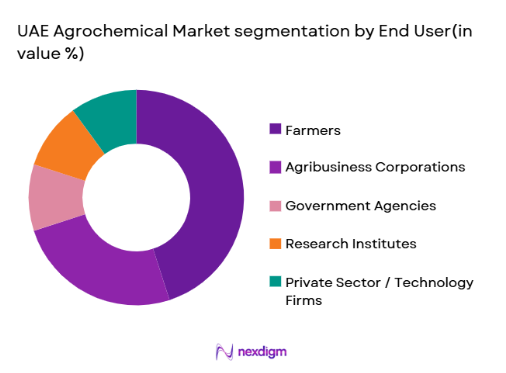

By End User:

UAE Agrochemical market is segmented by end-user into farmers, agribusiness corporations, government agencies, research institutes, and private sector / technology firms. Farmers, especially in regions with high crop production demands, have the highest market share, owing to their reliance on agrochemical products to improve crop yields and protect crops from pests and diseases. As UAE focuses on food security, local farmers remain the primary consumers of agrochemical products.

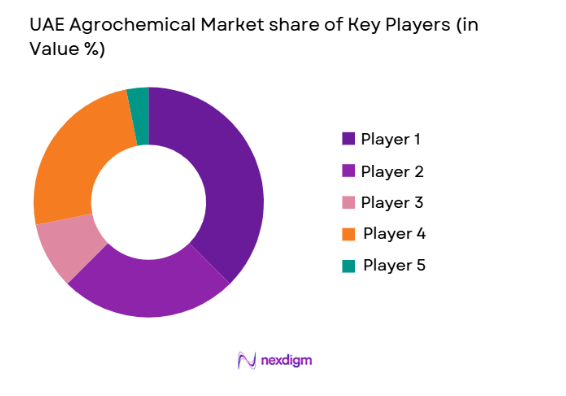

Competitive Landscape

The competitive landscape of the UAE Agrochemical market is characterized by consolidation, with several global and regional players dominating the market. These companies have made significant investments in research and development, which has strengthened their market positions. The competition is fierce, and companies are increasingly focusing on product innovation, sustainable practices, and regulatory compliance to maintain their dominance. Major players are strategically expanding their presence in the UAE due to the favorable market environment and demand for advanced agrochemical products.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Additional Parameter |

| BASF | 1865 | Germany | ~ | ~ | ~ | ~ | ~ |

| Dow AgroSciences | 1897 | USA | ~ | ~ | ~ | ~ | ~ |

| Syngenta | 2000 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Bayer CropScience | 1863 | Germany | ~ | ~ | ~ | ~ | ~ |

| UPL | 1969 | India | ~ | ~ | ~ | ~ | ~ |

UAE Agrochemical Market Analysis

Growth Drivers

Increased agricultural demand:

The UAE has experienced a surge in the demand for agrochemical products due to the expansion of agricultural activities in the region. As the country focuses on achieving self-sufficiency in food production, agrochemicals such as fertilizers, pesticides, and herbicides play an essential role in boosting crop yields. The UAE government has rolled out various policies and subsidies to support local farmers in adopting these technologies. The integration of advanced irrigation systems and soil management practices further amplifies the demand for agrochemicals. Another critical factor is the growing focus on improving the quality of crops to meet both domestic and international market standards, driving the adoption of agrochemical solutions.

Technological advancements in farming practices:

Precision farming, which relies on advanced agrochemical products for targeted application, has gained significant traction in the UAE. This technology allows farmers to optimize the use of fertilizers and pesticides, reducing waste and increasing efficiency. As more farms adopt precision agriculture techniques, the demand for specialized agrochemicals increases. The UAE has invested in developing smart agriculture technologies that incorporate drones, sensors, and data analytics to monitor crop health. These innovations help farmers make informed decisions about agrochemical application, further boosting the market’s growth.

Market Challenges

Environmental concerns:

The use of agrochemicals, particularly pesticides and fertilizers, raises environmental concerns due to their impact on soil health, water contamination, and biodiversity. The UAE, with its fragile desert ecosystem, faces the challenge of managing the environmental impact of agrochemicals. Stricter regulations are being enforced to mitigate these effects, pushing companies to develop environmentally friendly solutions. However, the shift towards sustainable practices may lead to higher costs for producers and farmers, potentially limiting the growth of the agrochemical market. Despite these challenges, demand for crop protection products continues to rise, posing a complex dilemma for the market.

Regulatory barriers:

The UAE has stringent regulations in place for the use of agrochemicals, which often results in delays in product approvals and restrictions on certain chemicals. These regulatory hurdles can impede market growth, as companies may need to invest additional resources to meet compliance requirements. For instance, the UAE’s focus on sustainability and food safety means that agrochemical companies must continually innovate and ensure that their products align with the country’s policies. While this creates a competitive advantage for companies investing in sustainable solutions, it also poses challenges for firms attempting to introduce new products into the market.

Opportunities

Green agrochemicals

: With growing environmental concerns and a strong push for sustainability, the market for eco-friendly agrochemicals has opened up in the UAE. Green agrochemicals, such as organic fertilizers and biopesticides, are gaining traction among farmers who seek safer alternatives to traditional chemicals. These products offer significant growth potential, particularly as the UAE works towards achieving food security and sustainability goals. The development of eco-friendly solutions presents a long-term opportunity for agrochemical companies to differentiate themselves in the competitive landscape. As regulatory frameworks evolve to support environmentally responsible products, the demand for green agrochemicals will likely increase.

Expansion of organic farming:

Organic farming is steadily gaining ground in the UAE as consumers increasingly demand pesticide-free food products. Agrochemical companies have an opportunity to tap into this market by offering organic farming solutions, including natural pesticides and fertilizers. The rise in organic food production is fueled by both consumer preferences for healthier, chemical-free products and government initiatives to support organic farming practices. Companies that can provide specialized organic agrochemicals stand to benefit from the growing demand in the UAE’s agricultural sector, especially as the government ramps up efforts to promote sustainable farming practices.

Future Outlook

The UAE Agrochemical market is expected to see steady growth over the next five years, driven by the adoption of advanced farming technologies, sustainability initiatives, and increased demand for food security. The regulatory landscape will continue to evolve, supporting eco-friendly agrochemical solutions and promoting sustainability in farming practices. The shift towards organic farming and precision agriculture will further shape market dynamics, creating new opportunities for agrochemical companies. Additionally, technological advancements in agrochemical application methods will enable better resource management and higher crop yields, contributing to the market’s positive growth trajectory.

Major Players

- BASF

- Dow AgroSciences

- Syngenta

- Bayer CropScience

- UPL

- FMC Corporation

- Monsanto

- DuPont

- Sumitomo Chemical

- Nufarm

- Arysta LifeScience

- ADAMA Agricultural Solutions

- Agrium

- Haifa Group

- The Mosaic Company

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agribusiness companies

- Farmers and farming cooperatives

- Agricultural technology developers

- Large-scale agricultural producers

- Retailers of agrochemical products

- Supply chain distributors

Research Methodology

Step 1: Identification of Key Variables

The first step in the research process involves identifying the key variables that drive the UAE Agrochemical market. These include market size, growth trends, regulatory factors, and demand patterns.

Step 2: Market Analysis and Construction

The next step is to gather data from primary and secondary sources, including government reports, industry publications, and market surveys. This data is used to build a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

This step involves validating the market model by consulting with industry experts and stakeholders to ensure that assumptions and trends align with current market conditions.

Step 4: Research Synthesis and Final Output

Finally, the collected data and insights are synthesized into a final report, which includes key findings, market segmentation, and actionable recommendations for stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Agricultural Demand

Increased Focus on Food Security

Technological Advancements in Agrochemical Production

Government Support for Sustainable Farming

Growing Trend of Precision Farming - Market Challenges

High Cost of Raw Materials

Environmental Impact of Agrochemicals

Stringent Regulatory Frameworks

Dependency on Weather Conditions

Market Fragmentation - Market Opportunities

Growing Adoption of Eco-friendly Agrochemicals

Emerging Markets for Agricultural Biotechnology

Expansion of Organic Farming - Trends

Integration of AI and IoT in Agrochemical Applications

Rise in Organic Agrochemical Production

Focus on Sustainable Farming Practices

Development of Biodegradable Agrochemicals

Growth in the Demand for Specialty Crops - Government Regulations & Defense Policy

Regulations on Pesticide Use

Environmental Sustainability Standards

Subsidies for Sustainable Agricultural Practices - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Fertilizers

Pesticides

Herbicides

Insecticides

Growth Regulators - By Platform Type (In Value%)

Field Crops

Fruit & Vegetables

Turf & Ornamentals

Nursery

Plantations - By Fitment Type (In Value%)

On-field Applications

Indoor Applications

Commercial Applications

Hydroponics Applications

Greenhouse Applications - By EndUser Segment (In Value%)

Farmers

Agribusiness Corporations

Government & Regulatory Agencies

Research Institutes

Private Sector / Technology Firms - By Procurement Channel (In Value%)

Direct Procurement

Retailers

Distributors

Online Platforms

Third-party Procurement - By Material / Technology (In Value%)

Biological Agrochemicals

Synthetic Agrochemicals

Nano-based Agrochemicals

Organic Agrochemicals

Chemical Blends

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Material / Technology, Regulatory Landscape, Competitive Intensity, Market Growth, Profit Margins)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

BASF

Dow AgroSciences

Syngenta

Bayer CropScience

Monsanto

Adama Agricultural Solutions

Nufarm

Sumitomo Chemical

UPL

FMC Corporation

Zhejiang Materials Industry Group

Anhui Shijia Agrochemical

China National Chemical Corporation

Haifa Group

The Mosaic Company

- Farmers’ Demand for Cost-Effective Solutions

- Government Agencies’ Role in Regulation

- Adoption of Biotech by Agribusiness Corporations

- Private Sector’s Investment in Agrochemical Research

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now