Download PDF

Download PDFMarket Overview

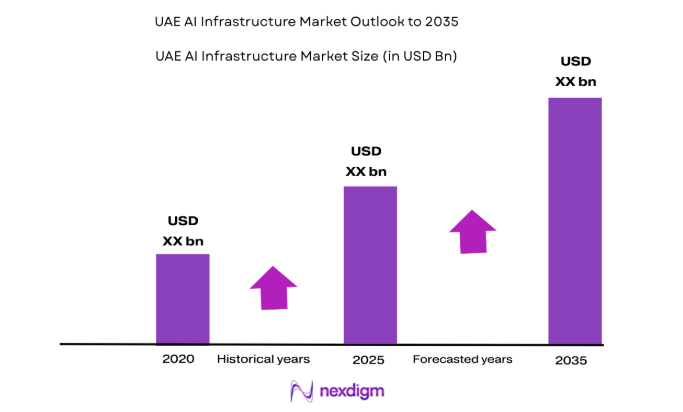

The UAE AI infrastructure market is valued at approximately USD ~ billion based on a recent historical assessment, driven by sustained sovereign investments in national AI strategy programs, hyperscale data center construction, and accelerated enterprise digitalization across government, finance, healthcare, and energy sectors. Public funding initiatives such as the UAE National AI Strategy and state-backed technology investment vehicles have catalyzed GPU cluster deployments, cloud AI platforms, and advanced compute facilities, positioning the country as a regional AI infrastructure hub.

Abu Dhabi and Dubai dominate the UAE AI infrastructure market due to concentrated hyperscale data center ecosystems, sovereign wealth technology investments, and strong enterprise AI adoption across finance, energy, aviation, and smart city programs. Abu Dhabi’s leadership stems from government-backed AI research institutions and large sovereign compute deployments, while Dubai benefits from multinational cloud region presence, advanced connectivity infrastructure, and regional headquarters of global technology firms supporting AI platform and data center expansion.

Market Segmentation

By Product Type

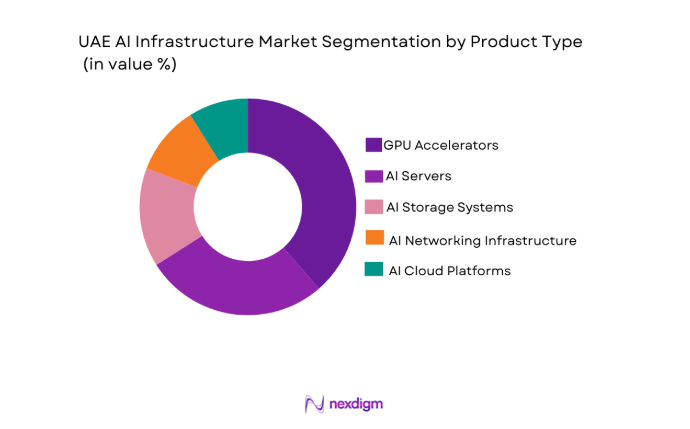

UAE AI Infrastructure market is segmented by product type into AI servers, GPU accelerators, AI storage systems, AI networking infrastructure, and AI cloud platforms. Recently, GPU accelerators have a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or enterprise preference. Large language model training, sovereign AI initiatives, and hyperscale data center expansion require high-performance parallel compute clusters where GPUs provide superior throughput for deep learning workloads. Major deployments by government AI labs, energy companies, and hyperscale cloud providers rely heavily on GPU-based systems, while AI servers and storage follow GPU procurement cycles. Vendor concentration around NVIDIA-based ecosystems and strong software stack compatibility further reinforces GPU dominance in national AI compute strategies.

By Platform Type

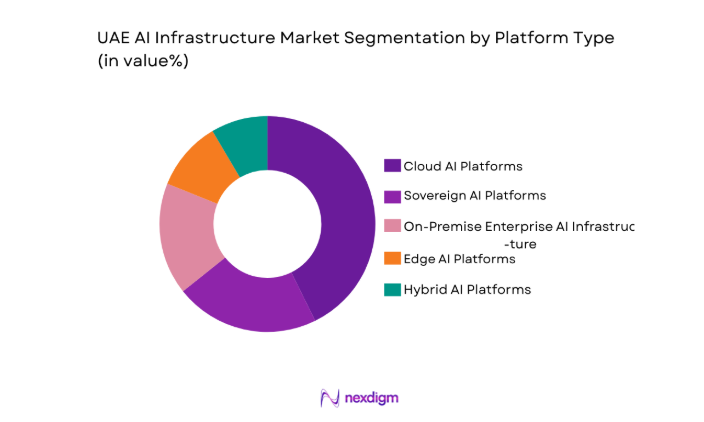

UAE AI Infrastructure market is segmented by platform type into cloud AI platforms, on-premise enterprise AI infrastructure, sovereign AI platforms, edge AI platforms, and hybrid AI platforms. Recently, cloud AI platforms have a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or enterprise preference. Enterprises across finance, aviation, retail, and public services increasingly deploy AI workloads through hyperscale cloud regions hosted in the UAE to access scalable GPU clusters, managed AI services, and advanced development ecosystems without high capital expenditure. Multinational cloud providers and sovereign cloud initiatives provide compliant, high-performance AI environments aligned with national data regulations, while hybrid and on-premise platforms remain smaller due to higher deployment complexity and cost.

Competitive Landscape

The UAE AI infrastructure market exhibits moderate consolidation with strong influence from global GPU, server, and cloud hyperscale providers collaborating with sovereign technology entities and regional data center operators. Market leadership is shaped by access to advanced semiconductors, hyperscale cloud platforms, and government-aligned AI programs, creating high entry barriers for smaller vendors while fostering strategic partnerships between international technology firms and national infrastructure investors.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Sovereign AI Partnerships |

| NVIDIA | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | USA | ~ | ~ | ~ | ~ | ~ |

| Amazon Web Services | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Huawei | 1987 | China | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | USA | ~ | ~ | ~ | ~ | ~ |

UAE AI Infrastructure Market Analysis

Growth Drivers

National Sovereign AI Investment Programs

The UAE government has established one of the world’s most capital-intensive sovereign artificial intelligence strategies, allocating multibillion-dollar funding through national technology investment entities, research institutions, and digital transformation initiatives that directly finance AI infrastructure procurement, hyperscale data center construction, and GPU cluster deployment across sectors. Public AI strategies mandate domestic compute capacity development to ensure technological sovereignty, secure data governance, and national competitiveness in advanced analytics and autonomous systems, creating sustained baseline demand for high-performance AI servers, accelerators, and networking equipment across public and quasi-public institutions. Sovereign AI laboratories and research universities require large-scale training infrastructure for language models, climate simulations, and defense analytics, generating continuous procurement cycles independent of private enterprise spending volatility. Government-backed cloud platforms supporting smart city, healthcare, mobility, and energy analytics rely on centralized AI compute hubs, reinforcing hyperscale infrastructure growth and long-term utilization stability. Public sector digital transformation mandates across ministries and state-owned enterprises further accelerate AI workload migration to national compute platforms, expanding infrastructure scale and geographic redundancy requirements. Strategic international partnerships with global semiconductor and cloud providers facilitate technology transfer, local capacity building, and co-investment in regional AI compute campuses aligned with national industrial policy. Sovereign wealth funds investing in global AI technology ecosystems strengthen domestic deployment pipelines by securing hardware supply chains and preferential infrastructure partnerships. Regulatory prioritization of domestic AI capability development ensures continued funding visibility and long-term infrastructure demand stability across economic cycles. National security, defense analytics, and cyber intelligence applications create high-performance compute requirements that cannot be outsourced externally, reinforcing local infrastructure expansion. Combined, these sovereign AI investment programs create structurally anchored demand that positions the UAE AI infrastructure market as one of the most policy-driven and capital-supported globally.

Hyperscale Cloud Region Expansion and Enterprise AI Adoption

The UAE hosts multiple global cloud regions and hyperscale campuses serving Middle East, Africa, and South Asia digital workloads, positioning the country as a regional AI compute hub where multinational cloud providers deploy large GPU clusters and AI-optimized infrastructure to support generative AI services, analytics platforms, and enterprise machine learning workloads. Rapid enterprise AI adoption across finance, energy, aviation, telecom, retail, and logistics sectors drives demand for scalable compute resources that hyperscale infrastructure uniquely provides through elastic GPU provisioning, high-speed networking, and AI software ecosystems. Financial institutions implement AI for risk analytics, fraud detection, and customer intelligence, requiring secure high-performance compute environments hosted in local data centers compliant with national data regulations. Energy companies deploy AI for reservoir modeling, predictive maintenance, and autonomous operations, generating large simulation workloads suited to hyperscale GPU clusters. Aviation and mobility sectors implement computer vision, optimization, and predictive analytics applications demanding scalable AI infrastructure. Multinational technology firms establish regional headquarters and AI development centers in the UAE to leverage connectivity, regulatory clarity, and digital infrastructure, further expanding compute demand concentration. Cloud AI services supporting startups and digital enterprises reduce barriers to AI adoption, increasing workload diversity and utilization rates across hyperscale facilities. Edge and enterprise deployments still rely on centralized hyperscale training and model development infrastructure, reinforcing its dominant market role. Continuous cloud region expansion driven by regional digital growth ensures sustained capacity additions and infrastructure investment cycles. The convergence of hyperscale expansion and enterprise AI adoption creates a reinforcing demand loop that accelerates infrastructure scale, utilization, and technological sophistication in the UAE AI infrastructure market.

Market Challenges

Dependence on Advanced Semiconductor Supply Chains

The UAE AI infrastructure market relies heavily on imported high-performance GPUs, AI accelerators, and advanced semiconductor components sourced primarily from a limited number of global suppliers, creating structural vulnerability to geopolitical export controls, supply allocation priorities, and manufacturing constraints that can restrict hardware availability and delay infrastructure deployment timelines. Advanced AI chips are produced using highly specialized fabrication processes concentrated in a few global facilities, meaning supply disruptions or policy restrictions can directly constrain domestic compute expansion regardless of capital availability. Export licensing requirements and technology transfer regulations associated with advanced AI semiconductors introduce procurement uncertainty for sovereign and enterprise buyers planning large GPU cluster investments. High global demand for AI hardware from major economies intensifies competition for limited supply, potentially diverting shipments toward larger markets with domestic semiconductor industries. Infrastructure planning cycles depend on predictable hardware access, and supply volatility can lead to stranded data center capacity or underutilized facilities awaiting accelerator installation. Vendor concentration around specific GPU architectures limits substitution flexibility and increases dependency on single-vendor ecosystems for both hardware and software compatibility. Long lead times for specialized cooling, power, and networking equipment integrated with AI accelerators further compound supply risk exposure. Strategic stockpiling and forward procurement contracts partially mitigate shortages but increase capital lock-in and inventory risk. Domestic semiconductor manufacturing capabilities remain limited, preventing local substitution or vertical integration in the near term. This structural dependence on advanced semiconductor supply chains represents a persistent constraint on UAE AI infrastructure expansion speed and resilience.

High Energy Consumption and Cooling Infrastructure Requirements

AI infrastructure, particularly hyperscale GPU clusters and training supercomputers, consumes extremely high electrical power densities and generates substantial thermal loads that require advanced cooling technologies, redundant energy supply, and specialized facility engineering, significantly increasing capital and operational costs for data center development in the UAE environment. AI training clusters can require tens of megawatts of continuous power and advanced liquid or immersion cooling systems to maintain stable operating temperatures, creating complex infrastructure design and construction challenges. Electricity supply reliability, grid capacity expansion, and energy cost management become critical factors influencing data center site selection and scalability in a rapidly growing AI compute market. The UAE climate, characterized by high ambient temperatures, increases cooling energy requirements compared to temperate regions, raising operating costs and engineering complexity for large AI facilities. Integration of renewable energy or energy-efficient cooling technologies requires additional investment and technical expertise to align sustainability goals with performance demands. Water usage for cooling processes introduces environmental and regulatory considerations in a region with limited natural freshwater resources. Infrastructure upgrades such as substations, transmission lines, and backup generation capacity are necessary to support large-scale AI campuses, extending project timelines. Energy efficiency optimization becomes essential to maintain economic viability of hyperscale AI operations amid rising compute intensity. Operators must balance performance, sustainability, and cost constraints while scaling infrastructure. These energy and cooling requirements create significant barriers to entry and expansion in the UAE AI infrastructure market.

Opportunities

Regional AI Compute Hub for Middle East and Africa

The UAE’s advanced connectivity infrastructure, political stability, investment capacity, and regulatory clarity position it uniquely to serve as the primary AI compute hub for Middle East and Africa digital economies, enabling cross-border AI service delivery, cloud hosting, and regional model training workloads that extend infrastructure demand beyond domestic consumption. Many neighboring countries lack hyperscale data center ecosystems or sovereign AI compute capacity, creating demand for regional hosting and processing services located in the UAE. Multinational cloud providers use UAE regions to serve regional enterprises requiring low-latency AI services and compliant data residency. Regional governments and enterprises outsource AI workloads to UAE facilities due to technological maturity and operational reliability. AI startups across Middle East and Africa leverage UAE cloud AI platforms for model training and deployment. Cross-border digital trade and AI service exports create sustained compute utilization growth independent of domestic market size. Regional disaster recovery and redundancy requirements increase demand for geographically distributed UAE facilities. Telecommunications connectivity through submarine cables enhances regional data routing efficiency into UAE AI campuses. Sovereign investment funds promote UAE as a digital infrastructure gateway for emerging markets. International partnerships with African and Middle Eastern technology initiatives further expand compute hosting demand. This regional hub positioning offers substantial long-term growth opportunity for UAE AI infrastructure providers.

Integration of AI Infrastructure with National Smart City and Industry 4.0 Programs

The UAE’s large-scale smart city, autonomous mobility, digital healthcare, and Industry 4.0 initiatives require continuous AI processing for sensor data, predictive analytics, automation control, and real-time decision systems, creating sustained demand for both centralized and distributed AI infrastructure integrated with national digital transformation programs. Smart city platforms generate massive urban data streams from cameras, IoT sensors, transportation systems, and utilities requiring AI analytics hosted in national compute centers. Autonomous mobility and logistics networks depend on AI training and simulation environments for safety optimization and route intelligence. Industrial automation and robotics adoption across manufacturing and energy sectors require AI inference and training infrastructure. Digital healthcare initiatives using imaging analytics and genomics generate high-performance compute workloads. Government digital twins and urban simulation programs rely on large-scale AI modeling. Integration of edge AI with centralized training infrastructure expands hybrid deployment demand. Continuous smart infrastructure expansion ensures recurring compute requirements across sectors. National digital platforms standardize AI adoption across public services, increasing infrastructure utilization. Industry 4.0 adoption by state-owned enterprises reinforces sovereign AI compute demand. The convergence of smart city and industrial AI initiatives creates long-term structural growth opportunities for UAE AI infrastructure.

Future Outlook

The UAE AI infrastructure market is expected to expand steadily as sovereign AI programs, hyperscale cloud investments, and regional digital demand converge to increase compute capacity deployment. Continued GPU cluster expansion, advanced cooling technologies, and renewable-powered data centers will shape infrastructure evolution. Regulatory support for domestic AI capability and data governance will sustain investment momentum. Enterprise AI adoption across sectors will further deepen infrastructure utilization and regional hub positioning.

Major Players

- NVIDIA

- Microsoft

- Amazon Web Services

- Huawei

- Dell Technologies

- Oracle

- IBM

- Lenovo

- Hewlett Packard Enterprise

- G42

- Equinix

- Khazna Data Centers

- Alibaba Cloud

- Cisco

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hyperscale cloud providers

- Data center operators

- Telecommunications companies

- Energy sector digitalization units

- Financial institutions

- Sovereign wealth funds

Research Methodology

Step 1: Identification of Key Variables

Key variables such as AI compute capacity, GPU deployment scale, hyperscale data center investment, sovereign AI funding, and enterprise AI adoption indicators were identified through technology infrastructure frameworks and national digital strategy analysis. Demand drivers and supply constraints were mapped across public and private sectors.

Step 2: Market Analysis and Construction

Market structure was constructed by integrating hardware deployment data, data center capacity indicators, sovereign investment programs, and enterprise AI adoption metrics. Segmentation and competitive positioning were derived from infrastructure type, deployment scale, and technology provider presence across the UAE.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on infrastructure dominance, deployment trends, and growth drivers were validated using industry expert perspectives from AI infrastructure architects, data center operators, and cloud platform specialists. Cross-verification ensured alignment with national AI strategies and regional digital infrastructure trends.

Step 4: Research Synthesis and Final Output

Validated findings were synthesized into structured market insights covering segmentation, competitive landscape, drivers, challenges, and opportunities. Quantitative and qualitative evidence was integrated to produce a coherent outlook reflecting UAE AI infrastructure dynamics and strategic positioning.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Sovereign AI Investment Programs and National Compute Capacity Expansion

Hyperscale Cloud Region Development and Regional Hosting Demand

Enterprise AI Adoption Across Finance Energy and Government

National Digital Transformation and Smart City Initiatives

Regional AI Hub Positioning for Middle East and Africa - Market Challenges

Dependence on Imported Advanced AI Semiconductors

High Power Consumption and Cooling Infrastructure Costs

Limited Domestic Semiconductor Manufacturing Capability

Specialized AI Infrastructure Talent Shortage

Data Sovereignty and Regulatory Compliance Complexity - Market Opportunities

Regional AI Compute Hosting for Emerging Markets

Integration with Smart City and Industry 4.0 Systems

Public Private Partnerships in AI Infrastructure - Trends

Expansion of Sovereign AI Data Centers

Adoption of Liquid Cooling in Hyperscale Facilities

Deployment of Exascale AI Supercomputers

Convergence of Cloud and Sovereign AI Platforms

Growth of Edge AI Integrated with Centralized Training - Government Regulations & Defense Policy

National AI Strategy and Sovereign Compute Mandates

Data Residency and Cloud Sovereignty Regulations

Cybersecurity and Critical Infrastructure Protection Policies - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AI Training Servers

AI Inference Servers

GPU Accelerators

AI Storage Systems

AI Networking Infrastructure - By Platform Type (In Value%)

Cloud AI Platforms

Sovereign AI Platforms

On-Premise Enterprise AI Infrastructure

Edge AI Platforms

Hybrid AI Platforms - By Fitment Type (In Value%)

Hyperscale Data Center Deployment

Enterprise Data Center Deployment

Edge Facility Deployment

Sovereign AI Campus Deployment

Colocation AI Deployment - By EndUser Segment (In Value%)

Government and Public Sector

Financial Services Institutions

Energy and Utilities Companies

Telecommunications Providers

Technology and Digital Enterprises - By Procurement Channel (In Value%)

Direct OEM Procurement

Hyperscale Cloud Procurement

Government Tender Procurement

System Integrator Procurement

Colocation and Managed Service Procurement - By Material / Technology (in Value %)

GPU-Based Compute Architecture

ASIC AI Accelerators

High-Performance NVMe Storage

High-Speed InfiniBand Networking

Liquid Cooling Infrastructure

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Compute Performance, Energy Efficiency, Cooling Technology, Deployment Scale, AI Software Stack Compatibility, Sovereign Compliance, Networking Bandwidth, Storage Throughput, Total Cost of Ownership)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

NVIDIA

Microsoft

Amazon Web Services

Huawei

Dell Technologies

Google

Oracle

IBM

Lenovo

Hewlett Packard Enterprise

G42

Khazna Data Centers

Equinix

Alibaba Cloud

Cisco

- Government entities leading sovereign AI compute investments

- Financial institutions deploying AI for analytics and risk modeling

- Energy sector adopting AI for simulation and optimization

- Telecom operators enabling AI cloud and edge services

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now