Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UAE Bone SPECT Equipment market is expected to grow significantly, driven by the increasing demand for advanced imaging technologies and a rising healthcare infrastructure. With a market size estimated to reach approximately USD ~ million, this growth is propelled by factors such as increasing awareness of bone diseases, adoption of early detection technologies, and government funding initiatives in the healthcare sector. Moreover, private sector investments in diagnostic equipment further support market expansion.

In terms of geographic dominance, Dubai and Abu Dhabi are at the forefront due to their well-established healthcare infrastructure, with many state-of-the-art diagnostic centers. These cities benefit from high healthcare spending and a significant expatriate population seeking quality medical services. Additionally, the UAE government’s initiatives to modernize healthcare facilities and attract international health investments play a pivotal role in maintaining their leadership in the Bone SPECT Equipment market.

Market Segmentation

By Product Type

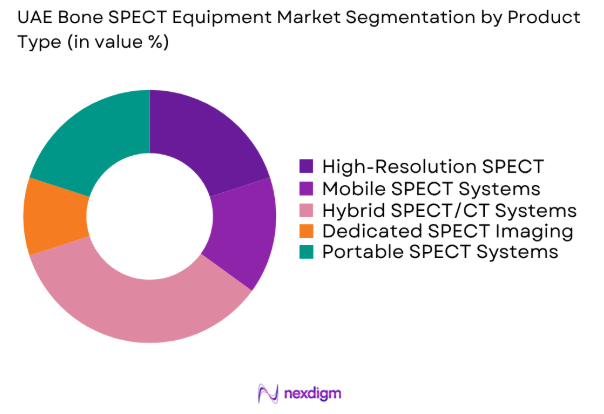

The UAE Bone SPECT Equipment market is segmented by product type into high-resolution SPECT systems, mobile SPECT systems, hybrid SPECT/CT systems, dedicated SPECT imaging systems, and portable SPECT systems. Recently, hybrid SPECT/CT systems have dominated the market share, driven by their ability to provide precise imaging, combining the advantages of both SPECT and CT scans for better diagnostic capabilities. The high demand for multi-functional, hybrid imaging systems, especially in urban areas with advanced healthcare infrastructure, has positioned this sub-segment as a market leader.

By Platform Type

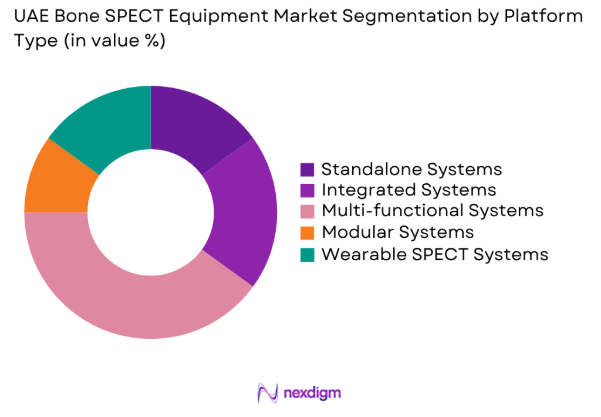

The UAE Bone SPECT Equipment market is also segmented by platform type into standalone systems, integrated systems, multi-functional systems, modular systems, and wearable SPECT systems. Among these, multi-functional systems have gained the most traction in the market due to their versatility in performing a wide range of diagnostic tests beyond bone imaging. These systems offer improved functionality, cost-efficiency, and space-saving features, especially in hospitals and diagnostic imaging centers, contributing to their market dominance.

Competitive Landscape

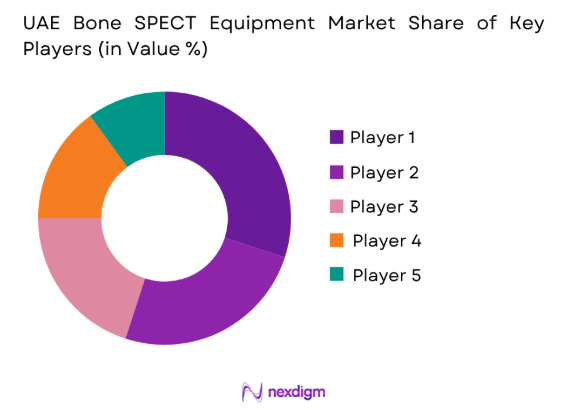

The competitive landscape of the UAE Bone SPECT Equipment market is characterized by a few key players that dominate the market. These companies maintain a strong presence through their advanced technological offerings, strategic partnerships, and high-quality services. Competition is increasing as new entrants develop innovative systems that integrate SPECT with other imaging modalities. Major players in the market continue to expand their presence through mergers, acquisitions, and technological innovation.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Market-specific Parameter |

| GE Healthcare | 1892 | USA | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | Germany | ~ | ~ | ~ | ~ | ~ |

| Philips Healthcare | 1891 | Netherlands | ~ | ~ | ~ | ~ | ~ |

| Toshiba Medical Systems | 1930 | Japan | ~ | ~ | ~ | ~ | ~ |

| Medtronic | 1949 | USA | ~ | ~ | ~ | ~ | ~ |

UAE Bone SPECT Equipment Market Analysis

Growth Drivers

Government Healthcare Investments

The UAE government’s focus on modernizing healthcare infrastructure is a key growth driver for the Bone SPECT Equipment market. Increased funding for cutting-edge diagnostic technologies, such as Bone SPECT systems, enables healthcare providers to offer advanced services and improve patient outcomes. As part of the Vision 2030 initiative, the government has significantly ramped up investments in medical technology to enhance healthcare delivery. These efforts concentrate on upgrading imaging facilities and promoting the adoption of state-of-the-art systems like Bone SPECT. The strategic push for modernization is driving the growth of the market, ensuring that healthcare providers have access to the latest diagnostic tools to meet rising patient needs.

Technological Advancements in Imaging

Advancements in medical imaging technology are significantly shaping the Bone SPECT Equipment market. The integration of SPECT with CT (Computed Tomography) to create hybrid imaging systems offers more precise and rapid diagnoses, increasing their demand. Additionally, the incorporation of AI and machine learning into Bone SPECT systems improves diagnostic accuracy and efficiency. These innovations enhance the overall capabilities of Bone SPECT, making it an essential tool for healthcare providers. As a result, many healthcare facilities are investing heavily in these technologies to maintain a competitive advantage, ensuring they provide superior diagnostic services and meet the growing need for advanced imaging solutions.

Market Challenges

High Initial Investment

A major challenge for the Bone SPECT Equipment market is the high initial capital investment required for advanced systems. The costs associated with purchasing, installing, and maintaining SPECT equipment can be prohibitive, especially for smaller clinics and healthcare providers with limited budgets. This financial burden creates a barrier to market adoption, particularly in rural or less-developed areas where healthcare facilities struggle to secure funding. Consequently, many healthcare providers are hesitant to adopt these advanced imaging technologies, which slows the overall expansion of the market. Addressing these financial challenges is crucial to improving market penetration and encouraging broader adoption of Bone SPECT systems.

Regulatory Barriers and Certification Delays

Regulatory approval processes for medical imaging equipment, such as Bone SPECT systems, can significantly delay the introduction of new technologies to the market. In the UAE, these systems must undergo rigorous scrutiny and obtain certification from health authorities before being allowed for sale. The lengthy and complex approval process can create uncertainty for manufacturers and hinder their ability to introduce new products promptly. This delay in product availability can slow market growth by limiting the number of advanced systems accessible to healthcare providers. As a result, the adoption rate of innovative Bone SPECT technologies is constrained, affecting the overall expansion of the market. Streamlining regulatory processes could help accelerate the availability and acceptance of advanced medical imaging solutions.

Opportunities

Growing Demand for Early Diagnosis

The increasing demand for early diagnosis of bone-related diseases, including osteoporosis, arthritis, and cancer, presents substantial opportunities for the Bone SPECT Equipment market. Healthcare providers are increasingly aware of the importance of early and accurate diagnoses to improve patient outcomes, which drives the adoption of advanced diagnostic technologies. Bone SPECT systems offer a non-invasive, highly effective method for detecting bone abnormalities, making them a preferred choice for diagnostic centers. The rising emphasis on early detection, coupled with the effectiveness of Bone SPECT in diagnosing complex bone diseases, is expected to lead to a significant increase in the market share of these systems, fueling their broader adoption in the coming years.

Expansion of Diagnostic Imaging Centers

The expansion of diagnostic imaging centers across the UAE, especially in underserved areas, offers significant growth opportunities for the Bone SPECT Equipment market. The increasing number of outpatient facilities and imaging centers has spurred a demand for advanced diagnostic tools, such as Bone SPECT systems, to meet the growing need for efficient and accurate bone disease detection. These centers play a crucial role in improving healthcare access and providing faster diagnoses, particularly in regions where specialized healthcare services were previously limited. As a result, the adoption of Bone SPECT equipment is expected to rise in smaller cities and rural areas, broadening market penetration and driving further growth in the coming years.

Future Outlook

The future outlook for the Bone SPECT Equipment market in the UAE is optimistic, with projected growth driven by technological innovations and continued government support. As advancements in imaging technologies, particularly hybrid SPECT/CT systems, become more widespread, the demand for accurate diagnostic tools will increase. Additionally, the government’s Vision 2030 initiative to modernize healthcare services will further accelerate the adoption of cutting-edge diagnostic equipment. The market is expected to witness significant growth in both urban and rural healthcare facilities over the next five years, fueled by increasing investments and a rising need for early disease detection.

Major Players

- GE Healthcare

- Siemens Healthineers

- Philips Healthcare

- Toshiba Medical Systems

- Medtronic

- Hitachi Medical Systems

- Canon Medical Systems

- Mindray

- Spectrum Dynamics

- United Imaging Healthcare

- Planar Systems

- Neusoft Medical Systems

- Varian Medical Systems

- CTI Molecular Imaging

- Emory Healthcare

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hospitals

- Diagnostic Imaging Centers

- Orthopedic Clinics

- Research Institutes

- Rehabilitation Centers

- Healthcare Providers

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying the essential factors that influence market growth, including technological advancements, regulations, demand patterns, and regional trends.

Step 2: Market Analysis and Construction

Data collection from credible industry reports, interviews with key market players, and statistical analysis help to construct the market landscape, assessing current trends and future forecasts.

Step 3: Hypothesis Validation and Expert Consultation

Through consultations with healthcare experts and industry leaders, the initial market hypothesis is validated, ensuring the findings are relevant and applicable to current market conditions.

Step 4: Research Synthesis and Final Output

The final market report is synthesized, consolidating all findings into actionable insights for stakeholders, offering a comprehensive overview of market dynamics, trends, and future predictions.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Technological Advancements in Imaging

Rising Healthcare Investment

Aging Population and Chronic Disease Prevalence - Market Challenges

High Initial Investment Costs

Technological Complexity and Maintenance

Limited Reimbursement Policies - Market Opportunities

Increasing Demand for Early Diagnosis

Government Healthcare Programs and Initiatives

Expansion of Diagnostic Imaging Centers - Trends

Integration with AI and Machine Learning

Increased Adoption of Hybrid Imaging Systems

Rising Popularity of Point-of-Care Diagnostics - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

High-Resolution SPECT Systems

Mobile SPECT Systems

Dedicated SPECT Imaging Systems

Hybrid SPECT/CT Systems

Portable SPECT Systems - By Platform Type (In Value%)

Standalone Systems

Integrated Systems

Multi-functional Systems

Modular Systems

Wearable SPECT Systems - By Fitment Type (In Value%)

Hospital-based Systems

Clinic-based Systems

Mobile Fitment Systems

Homecare Fitment Systems

Ambulatory Surgery Center Systems - By End User Segment (In Value%)

Hospitals

Diagnostic Imaging Centers

Research Institutes

Clinics

Rehabilitation Centers - By Procurement Channel (In Value%)

Direct Sales

Distributors

Online Sales

Group Purchasing Organizations

Government Tenders

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User, Technological Advancements, Pricing Strategy, Regional Presence, Market Penetration, Product Customization, Regulatory Compliance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

GE Healthcare

Siemens Healthineers

Philips Healthcare

Toshiba Medical Systems

Canon Medical Systems

Mindray

Medtronic

Hitachi Medical Systems

Spectrum Dynamics

Planar Systems

Neusoft Medical Systems

Varian Medical Systems

United Imaging Healthcare

CTI Molecular Imaging

Emory Healthcare

- Diagnostic Imaging Centers

- Multi-Specialty Hospitals

- Oncology Treatment Centers

- Orthopedic Clinics

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now