Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UAE CEP Market reflects strong expansion supported by e-commerce growth, cross-border trade logistics, and advanced urban delivery infrastructure. Based on a recent historical assessment, the market generated approximately USD ~ billion in courier, express, and parcel service revenues according to logistics sector reports from the UAE Telecommunications and Digital Government Regulatory Authority and regional logistics associations. Increasing online retail transactions, rising consumer expectations for fast delivery, and expansion of international parcel shipments continue to drive CEP service demand across domestic and cross-border logistics networks.

Dubai and Abu Dhabi dominate CEP logistics activity due to their advanced logistics ecosystems, extensive airport cargo facilities, and high consumer purchasing activity. Dubai International Airport and Al Maktoum International Airport process large parcel volumes that support international express shipments entering the country. Free zones such as Dubai South and Jebel Ali Free Zone attract global logistics providers that operate parcel sorting centers and regional fulfillment hubs, enabling efficient parcel distribution across the Gulf region and strengthening the UAE’s role as a regional CEP gateway.

Market Segmentation

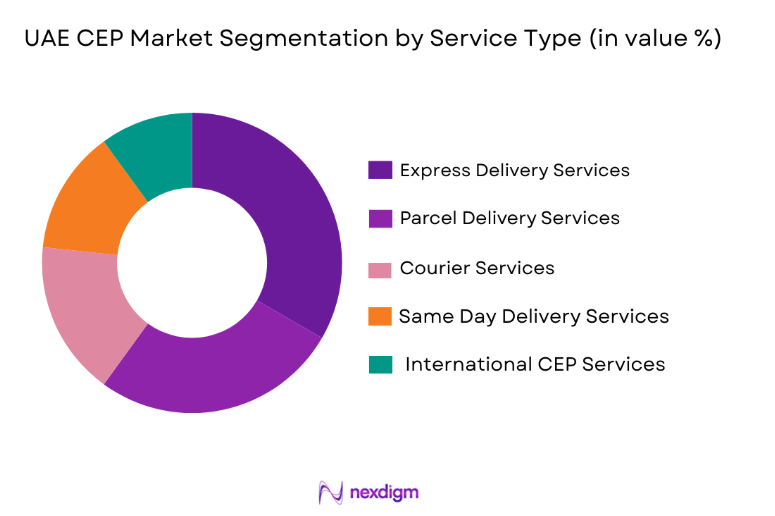

By Service Type

UAE CEP Market is segmented by service type into courier services, express delivery services, parcel delivery services, same day delivery services, and international CEP services. Recently, express delivery services have a dominant market share due to factors such as rising demand for rapid delivery, the growth of e-commerce logistics, and the need for reliable cross-border parcel shipping. Businesses and consumers increasingly prioritize fast shipment speeds for online retail purchases, documents, and urgent cargo, leading to widespread adoption of express delivery networks. Logistics companies invest heavily in advanced parcel sorting centers, real-time shipment tracking platforms, and dedicated air cargo partnerships to support faster delivery cycles. The presence of multinational logistics providers in Dubai and Abu Dhabi further strengthens the express delivery ecosystem by connecting domestic CEP services with international logistics corridors. Strong airport infrastructure and international air cargo connectivity also allow express service providers to maintain shorter transit times for cross-border shipments. E-commerce retailers rely on express logistics to ensure quick delivery of consumer electronics, fashion goods, and pharmaceuticals to customers across urban centers. As consumer expectations continue shifting toward rapid delivery services, express delivery remains the dominant service type driving operational activity in the UAE CEP logistics sector.

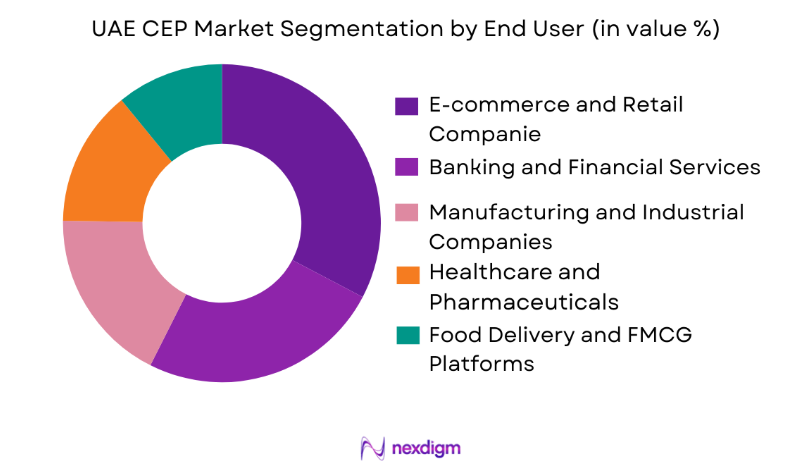

By End User Industry

UAE CEP Market is segmented by end user type into e-commerce and retail companies, banking and financial services, healthcare and pharmaceuticals, manufacturing and industrial companies, and food delivery and FMCG platforms. Recently, e-commerce and retail companies have a dominant market share due to factors such as high online shopping penetration, increasing cross-border retail trade, and growing demand for home delivery services. Online retailers rely heavily on CEP operators to transport consumer goods quickly from distribution centers to residential customers located across major cities. Logistics companies therefore develop extensive last-mile delivery networks and automated parcel sorting hubs to manage high shipment volumes generated by online marketplaces. International retailers also establish fulfillment centers within UAE free zones that require integrated CEP delivery services to distribute imported products across regional markets. The rapid expansion of mobile commerce platforms further strengthens parcel shipment demand as consumers increasingly purchase goods through digital marketplaces. CEP providers collaborate with retailers to integrate logistics technology systems that enable real-time shipment tracking, automated delivery notifications, and efficient route optimization for urban deliveries. As e-commerce activity continues expanding, retail logistics demand remains the dominant contributor to parcel shipment volumes across the UAE CEP logistics sector.

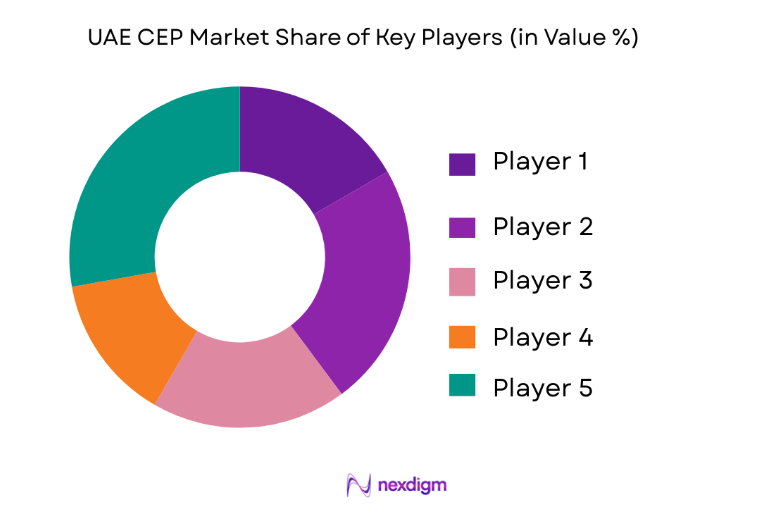

Competitive Landscape

The UAE CEP Market features a competitive environment dominated by global logistics corporations alongside regional parcel delivery providers and digital logistics startups. International operators leverage global delivery networks, advanced parcel tracking systems, and integrated air cargo capabilities to maintain strong service reliability. Regional CEP companies strengthen competitiveness through localized last-mile delivery infrastructure, flexible delivery options, and digital logistics platforms that improve operational efficiency and customer service across rapidly expanding e-commerce supply chains.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Delivery Infrastructure |

| DHL Express | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| FedEx | 1971 | United States | ~ | ~ | ~ | ~ | ~ |

| UPS | 1907 | United State | ~ | ~ | ~ | ~ | ~ |

| Aramex | 1982 | UAE | ~ | ~ | ~ | ~ | ~ |

| Emirates Post | 1909 | UAE | ~ | ~ | ~ | ~ | ~ |

US CEP Market Analysis

Growth Drivers

Rapid Expansion of E-Commerce and Digital Retail Logistics

explanation continues in the same sentence. The UAE has emerged as one of the most advanced e-commerce markets in the Middle East, significantly increasing demand for courier express and parcel logistics services responsible for delivering consumer goods purchased through digital retail platforms. Online retail marketplaces including regional and global platforms handle large volumes of consumer product orders that require reliable parcel transportation from distribution warehouses to residential customers located across urban and suburban regions. CEP operators therefore develop sophisticated last mile delivery networks supported by parcel sorting hubs, digital shipment tracking platforms, and integrated logistics management systems that enable efficient parcel movement across national delivery networks. The growth of mobile commerce applications further strengthens parcel demand as consumers increasingly rely on smartphones to purchase electronics, apparel, cosmetics, groceries, and household goods that require fast doorstep delivery. International retailers also establish fulfillment centers in logistics zones such as Dubai South and Jebel Ali Free Zone to store imported inventory that can be distributed quickly across regional markets using CEP delivery providers. These fulfillment operations generate high parcel shipment volumes requiring integrated logistics coordination between international freight forwarding companies and domestic parcel delivery operators. CEP companies adopt advanced logistics technologies including route optimization algorithms, automated sorting equipment, and real time delivery tracking systems to manage growing parcel volumes efficiently. Consumer expectations for rapid delivery timelines have also increased significantly as online retailers compete to provide faster order fulfillment services within major cities. Logistics providers therefore invest in expanding delivery fleets, parcel locker networks, and pickup drop-off points designed to improve last mile distribution efficiency. The continuous expansion of digital retail activity and cross border e-commerce transactions significantly strengthens parcel shipment demand across the UAE logistics sector.

Development of Advanced Logistics Infrastructure and Smart Delivery Networks

explanation continues in the same sentence. The United Arab Emirates has invested heavily in modern logistics infrastructure including high capacity airports, automated parcel sorting facilities, and integrated logistics zones designed to support efficient cargo movement across domestic and international supply chains. Airports such as Dubai International Airport and Al Maktoum International Airport handle substantial air cargo volumes that enable express parcel shipments connecting international trade routes with domestic CEP delivery networks. Logistics zones such as Dubai South and JAFZA host regional parcel distribution centers where logistics providers consolidate shipments before distributing them through last mile delivery networks. Government infrastructure investments also support development of smart logistics systems integrating digital customs processing, automated cargo handling equipment, and intelligent traffic management systems that improve parcel delivery efficiency. CEP operators benefit from these infrastructure improvements because faster cargo clearance and improved transportation connectivity reduce shipment transit times across supply chains. Parcel delivery companies integrate advanced route optimization software and GPS enabled fleet management platforms that allow delivery drivers to navigate urban areas more efficiently. Logistics firms also deploy automated parcel lockers and pickup stations that allow customers to collect shipments conveniently without requiring home delivery coordination. Smart logistics infrastructure supports growing parcel shipment volumes generated by e-commerce retailers, financial institutions, healthcare providers, and manufacturing companies requiring document or package transportation services. As urban populations continue increasing and online retail activity expands, CEP operators rely heavily on logistics infrastructure modernization to maintain service efficiency. The UAE government’s continued focus on logistics sector development therefore strengthens long term growth prospects for courier express and parcel service providers.

Market Challenges

High Operational Costs Associated with Last Mile Delivery Infrastructure

explanation continues in the same sentence. CEP service providers operating within the United Arab Emirates face significant operational cost pressures associated with maintaining large delivery fleets, parcel sorting facilities, and last mile logistics infrastructure necessary to support rapid parcel distribution across urban areas. Urban delivery operations require significant investments in delivery vehicles, driver recruitment, fuel expenses, warehouse facilities, and digital logistics management systems that coordinate parcel movements across complex supply chains. Rising labor costs and transportation expenses further increase operational expenditure for parcel delivery companies attempting to maintain rapid delivery services within highly competitive logistics markets. Logistics providers must also maintain large parcel sorting centers equipped with automated conveyor systems and barcode scanning technologies capable of processing thousands of shipments daily. Maintaining these logistics facilities requires substantial capital investment as parcel volumes increase with the growth of e-commerce retail activity. CEP operators also face cost pressures when customers demand faster delivery services such as same day or next day shipping because these services require additional logistics coordination and transportation resources. Delivery companies must therefore optimize logistics operations carefully to maintain profitability while offering competitive shipping prices for retailers and consumers. Seasonal fluctuations in parcel shipment volumes during major retail sales events further complicate logistics planning because companies must temporarily expand operational capacity to manage peak demand periods. Investments in advanced logistics technologies such as route optimization systems and automated parcel lockers help reduce operational inefficiencies but also require significant capital expenditure. Managing operational costs effectively remains a major challenge for CEP providers operating within the UAE logistics ecosystem.

Complex Addressing Systems and Urban Delivery Logistics Challenges

explanation continues in the same sentence. Delivering parcels efficiently across urban environments in the United Arab Emirates presents logistical challenges due to varying address formats, high density residential buildings, and rapid urban expansion across major cities such as Dubai and Abu Dhabi. Accurate address identification remains critical for parcel delivery efficiency because incomplete or inconsistent address information can delay shipments or require additional coordination between delivery drivers and customers. Logistics providers therefore rely heavily on GPS based navigation systems and digital mapping platforms that assist drivers in locating delivery destinations within complex urban environments. High rise residential buildings also require additional delivery coordination because drivers must often interact with building security personnel or concierge services before accessing individual apartments. Traffic congestion in densely populated commercial districts can further delay delivery routes, increasing transportation time and operational costs for CEP providers attempting to maintain rapid delivery schedules. Logistics companies must therefore continuously optimize delivery routes and schedule shipments strategically to minimize travel delays within congested urban corridors. The expansion of e-commerce retail activity increases parcel volumes entering urban delivery networks, intensifying pressure on last mile logistics infrastructure. CEP operators invest in parcel lockers, smart delivery points, and customer pickup stations to reduce delivery complexity and improve distribution efficiency. However, implementing these alternative delivery solutions requires infrastructure investment and collaboration with property developers and retail centers. Address standardization initiatives and digital mapping technologies continue improving delivery accuracy but urban logistics complexity remains an ongoing operational challenge for CEP providers.

Opportunities

Adoption of Smart Parcel Locker Networks and Alternative Delivery Solutions

explanation continues in the same sentence. The increasing volume of parcel shipments across the UAE presents significant opportunities for CEP operators to deploy alternative delivery infrastructure designed to improve last mile logistics efficiency and reduce operational costs associated with traditional home delivery services. Parcel locker networks installed within residential complexes, shopping malls, metro stations, and commercial buildings allow customers to collect packages at convenient locations without requiring delivery drivers to coordinate individual home visits. These systems significantly reduce delivery time because drivers can deposit multiple parcels in a single location rather than traveling to numerous residential addresses. Smart lockers also enhance delivery security by storing packages safely until customers retrieve them using digital authentication codes provided through mobile applications. CEP providers integrate parcel locker networks with digital logistics platforms that notify customers automatically when shipments arrive at designated pickup points. Retailers benefit from these alternative delivery systems because faster parcel distribution improves customer satisfaction and reduces failed delivery attempts that often occur when recipients are unavailable. Parcel locker networks also support environmentally sustainable logistics practices because delivery vehicles travel fewer kilometers during distribution routes. As parcel shipment volumes continue rising due to e-commerce expansion, CEP companies investing in smart locker infrastructure can improve operational efficiency while maintaining delivery speed. Governments and logistics operators increasingly collaborate to integrate parcel locker networks into urban infrastructure planning, creating long term opportunities for technology driven delivery solutions. The growing demand for flexible delivery options therefore creates significant growth potential for CEP companies deploying smart parcel distribution systems.

Expansion of Cross Border E-Commerce Logistics Across the Gulf Region

explanation continues in the same sentence. The United Arab Emirates serves as a major logistics gateway connecting international manufacturing centers with consumer markets across the Middle East and North Africa, creating substantial opportunities for CEP companies to expand cross border parcel delivery services. International retailers ship products to UAE logistics hubs where shipments are consolidated and redistributed to customers located across neighboring countries through regional parcel delivery networks. CEP operators coordinate international air cargo shipments, customs clearance procedures, and regional distribution logistics that enable fast delivery of imported goods purchased through online marketplaces. Cross border e-commerce transactions generate increasing parcel volumes because consumers across the Gulf region increasingly purchase products from international retailers offering competitive pricing and product variety. Logistics companies invest in automated parcel sorting facilities and digital customs documentation platforms designed to accelerate cross border shipment processing and reduce delivery delays. Regional free trade zones support cross border logistics operations by providing efficient customs clearance processes and integrated warehouse infrastructure. CEP providers also establish partnerships with international freight forwarding companies that transport imported goods from manufacturing regions in Asia and Europe to distribution hubs located within the UAE. As regional digital commerce activity continues expanding, cross border parcel logistics services become increasingly important for connecting international retailers with Middle Eastern consumers. The strategic geographic location of the UAE therefore positions CEP providers to capture growing parcel shipment demand generated by cross border online retail trade. Expanding cross border logistics capabilities represents a significant opportunity for courier express and parcel companies operating within the UAE logistics sector.

Future Outlook

The UAE CEP Market is expected to experience steady growth as e-commerce activity and cross-border trade continue expanding across the Middle East. Logistics technology innovations such as automated sorting systems, route optimization platforms, and smart parcel lockers will improve delivery efficiency. Government investments in smart mobility and logistics infrastructure will further support parcel distribution networks. Increasing demand for faster delivery services and regional e-commerce fulfillment will strengthen CEP logistics operations.

Major Players

- DHL Express

- FedEx

- UPS

- Aramex

- Emirates Post

- iMile

- ShipaDelivery

- Quiqup

- Fetchr

- Jeebly

- Careem Express

- SMSA Express

- DTDC Express

- First Flight Couriers

- Amazon Shipping

Key Target Audience

- E-commerce companies

- Retail and marketplace platforms

- Logistics and supply chain companies

- Banking and financial institutions

- Healthcare and pharmaceutical distributors

- Manufacturing and industrial companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables including parcel shipment volumes, logistics infrastructure capacity, e-commerce transaction activity, and delivery network coverage are identified to define the operational scope of the UAE CEP Market. These indicators help evaluate the structural drivers influencing courier express and parcel logistics demand across the country.

Step 2: Market Analysis and Construction

Industry data from logistics authorities, airport cargo operators, and courier service providers is analyzed to construct the market structure. Shipment volumes, parcel delivery infrastructure, and logistics network capacity are examined to understand operational dynamics influencing CEP services.

Step 3: Hypothesis Validation and Expert Consultation

Industry insights are validated through consultations with logistics operators, parcel delivery companies, and supply chain professionals who provide operational perspectives regarding delivery networks, logistics technologies, and market demand conditions.

Step 4: Research Synthesis and Final Output

All data inputs are consolidated to produce a comprehensive market assessment combining logistics statistics, infrastructure indicators, and expert analysis. The final report provides structured insights into market dynamics, competitive positioning, and growth opportunities within the UAE CEP logistics sector.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of E-commerce and Omnichannel Retail Logistics

Rising Cross Border Trade and Re-export Shipments

Development of Smart Logistics Infrastructure and Last Mile Networks - Market Challenges

High Last Mile Delivery Costs in Dense Urban Areas

Address Standardization and Delivery Accuracy Issues

Intense Competition and Margin Pressure Among Service Providers - Market Opportunities

Growth in Same Day and On Demand Delivery Services

Expansion of Parcel Locker and Pickup Drop-off Networks

Increasing Adoption of AI Enabled Route Optimization Platforms - Trends

Rapid Adoption of Electric Delivery Fleets

Integration of Real Time Tracking and Customer Notification Systems

Rising Demand for Contactless and Flexible Delivery Options - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Courier Services

Express Delivery Services

Parcel Delivery Services

Same Day Delivery Services

International CEP Services - By Platform Type (In Value%)

Ground Delivery Networks

Air Express Networks

Integrated Fulfillment Platforms

Digital Delivery Platforms

Cross Border Delivery Platforms - By Fitment Type (In Value%)

Business to Business Deliveries

Business to Consumer Deliveries

Consumer to Consumer Deliveries

Domestic Deliveries

International Deliveries - By EndUser Segment (In Value%)

E-commerce and Retail

Banking and Financial Services

Healthcare and Pharmaceuticals

Manufacturing and Industrial

- Market Share Analysis

- CrossComparison Parameters (Delivery Speed, Geographic Coverage, Technology Integration, Pricing Model, Fleet Capacity)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Aramex

DHL Express

FedEx

UPS

Emirates Post

Shipa Delivery

iMile

Quiqup

Jeebly

DTDC Express

SMSA Express

First Flight Couriers

Fetchr

Careem Express

Amazon Shipping

- E-commerce retailers driving high parcel volumes through fast fulfillment needs

- Financial institutions requiring secure document and package delivery services

- Healthcare providers depending on time sensitive sample and medicine transport

- Food and FMCG platforms increasing demand for rapid urban delivery coverage

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now