Download PDF

Download PDF Download PDF

Download PDFMarket Overview

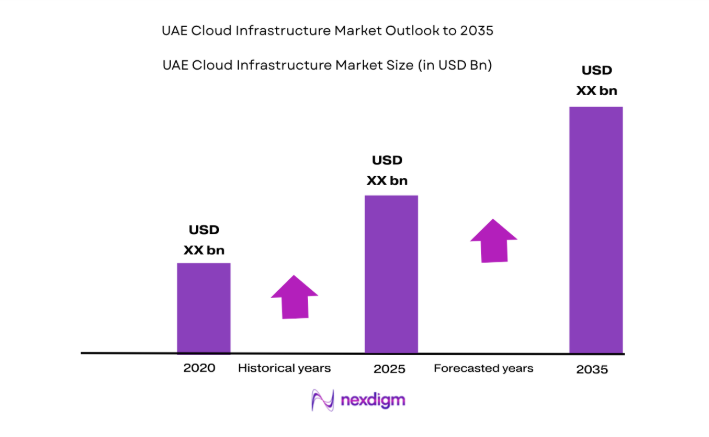

Based on a recent historical assessment, the UAE cloud infrastructure market is valued at approximately USD ~ billion, supported by sustained hyperscale data center investments and national digital transformation programs. Government cloud-first mandates, sovereign cloud initiatives, and enterprise migration from on-premise IT environments are accelerating demand for compute, storage, and networking infrastructure across public and hybrid cloud deployments within regulated sectors and digital services ecosystems.

Dubai and Abu Dhabi dominate the UAE cloud infrastructure market due to concentration of hyperscale data centers, financial institutions, and government digital platforms requiring sovereign hosting. These emirates host major cloud regions and carrier-neutral facilities supported by robust fiber connectivity, regulatory clarity, and enterprise headquarters presence, while free-zone technology clusters and smart city programs create sustained enterprise and public sector cloud infrastructure demand.

By Product Type

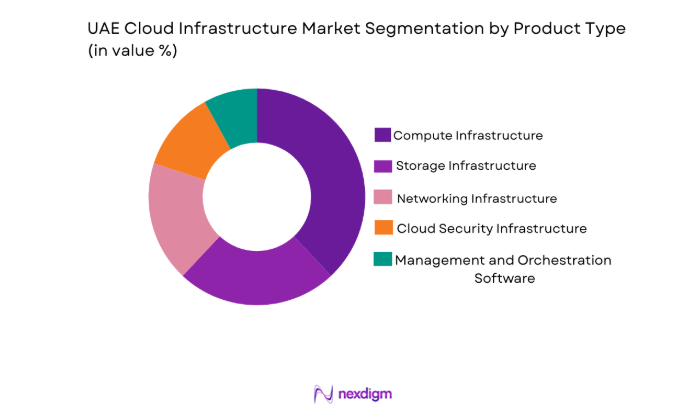

UAE Cloud Infrastructure Market is segmented by product type into compute infrastructure, storage infrastructure, networking infrastructure, cloud security infrastructure, and management and orchestration software. Recently, compute infrastructure has a dominant market share due to hyperscale data center expansion, enterprise workload migration, and AI-driven processing requirements demanding scalable virtual machines and high-performance processing clusters. Public sector platforms, financial applications, and digital services rely heavily on elastic compute capacity, reinforcing sustained demand across hyperscale and sovereign cloud environments.

By Platform Type

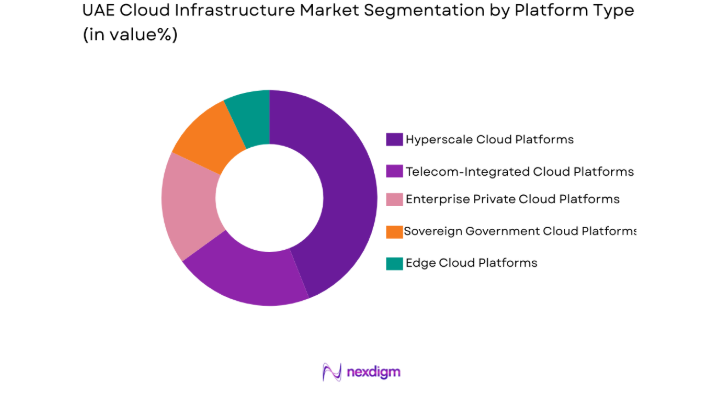

UAE Cloud Infrastructure Market is segmented by platform type into hyperscale cloud platforms, telecom-integrated cloud platforms, enterprise private cloud platforms, sovereign government cloud platforms, and edge cloud platforms. Recently, hyperscale cloud platforms have a dominant market share due to localized global cloud regions, advanced service ecosystems, and large-scale enterprise migration to standardized public cloud architectures. Availability of AI, analytics, and container services within regional hyperscale environments accelerates adoption across government and enterprise sectors, consolidating infrastructure consumption within hyperscale platforms.

Competitive Landscape

The UAE cloud infrastructure market is moderately consolidated, with hyperscale providers and regional telecom operators controlling large-scale capacity and enterprise relationships. Global cloud platforms influence technology standards and pricing models, while local operators leverage sovereign hosting, connectivity integration, and regulatory alignment to retain enterprise and government workloads. Strategic partnerships between hyperscalers and telecom providers shape regional infrastructure expansion and hybrid cloud delivery models.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | UAE Data Center Presence |

| Amazon Web Services | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | USA | ~ | ~ | ~ | ~ | ~ |

| Google Cloud | 2008 | USA | ~ | ~ | ~ | ~ | ~ |

| e& (Etisalat) | 1976 | UAE | ~ | ~ | ~ | ~ | ~ |

| Oracle | 1977 | USA | ~ | ~ | ~ | ~ | ~ |

UAE Cloud Infrastructure Market Analysis

UAE Cloud Infrastructure Market Analysis

Growth Drivers

National Sovereign Cloud and Digital Government Infrastructure Expansion

UAE federal and emirate governments are implementing sovereign cloud architectures to ensure data residency, cybersecurity assurance, and digital service scalability across national platforms, driving sustained demand for localized hyperscale infrastructure deployments and secure cloud environments. Government cloud-first procurement policies require ministries and agencies to migrate legacy systems into certified sovereign environments, increasing compute, storage, and secure networking consumption across public infrastructure layers. Nationwide digital identity, payments, licensing, and smart city platforms rely on resilient cloud backbones with high availability requirements, stimulating multi-region data center investments within UAE territory. Regulatory frameworks mandating local hosting for sensitive financial, healthcare, and citizen data create structural demand for sovereign and hybrid cloud infrastructure operated within national jurisdiction. Public sector AI adoption programs, including analytics, automation, and digital twins for urban management, require scalable GPU-enabled cloud environments, increasing hyperscale capacity investments. Cross-government shared services platforms centralize infrastructure procurement, accelerating large-scale cloud adoption across multiple agencies simultaneously. Digital public service demand growth, including online transactions and mobile government services, drives continuous infrastructure scaling requirements. National cybersecurity strategies emphasizing zero-trust architectures and secure cloud hosting further strengthen sovereign cloud infrastructure expansion. These coordinated regulatory, digitalization, and service delivery drivers collectively anchor long-term cloud infrastructure growth within UAE public sector ecosystems.

Hyperscaler Regional Data Center Localization and Enterprise Migration Momentum

Global cloud providers have established regional data centers within the UAE to reduce latency, comply with residency regulations, and capture enterprise workloads, creating strong localized infrastructure expansion and accelerating enterprise cloud migration across industries. Enterprises previously constrained by data sovereignty concerns now transition mission-critical workloads into local hyperscale environments, increasing demand for compute clusters, high-performance storage, and software-defined networking infrastructure. Availability of advanced services such as AI platforms, analytics engines, and container orchestration within UAE-hosted regions encourages organizations to modernize applications and migrate legacy IT estates into scalable cloud architectures. Telecom operators partner with hyperscalers to integrate connectivity, edge computing, and hybrid cloud solutions, expanding enterprise cloud accessibility across sectors. Financial institutions and regulated enterprises adopt multi-cloud architectures anchored in localized hyperscale regions to meet compliance and resilience requirements. Rapid digital service deployment expectations among enterprises favor elastic cloud infrastructure over traditional on-premise hardware procurement cycles. Regional content platforms, streaming services, and e-commerce ecosystems require scalable infrastructure hosted within proximity to users, reinforcing hyperscale demand. Developer ecosystems and startup environments adopt native cloud platforms hosted locally, increasing infrastructure consumption across innovation sectors. These dynamics position localized hyperscale capacity expansion as a primary structural driver of UAE cloud infrastructure growth.

Market Challenges

High Energy Consumption and Data Center Sustainability Constraints

Large-scale cloud infrastructure expansion in the UAE requires substantial electrical power and cooling capacity, creating operational cost pressures and sustainability challenges in a region characterized by high ambient temperatures and energy-intensive cooling requirements. Data centers must deploy advanced cooling technologies and redundant power architectures to maintain reliability, increasing capital expenditure and operational complexity for infrastructure operators. Sustainability commitments and carbon reduction targets necessitate renewable energy integration and energy efficiency optimization across data center operations. Limited availability of cost-effective renewable power at required scale can constrain sustainable infrastructure expansion pace. High energy intensity directly affects cloud service pricing structures and total cost of ownership for enterprise customers. Regulatory expectations for environmentally responsible infrastructure add compliance requirements for operators. Cooling water consumption and thermal management challenges further complicate site selection and infrastructure design. Operators must invest in innovative cooling and energy optimization technologies to maintain competitiveness. These sustainability and energy constraints represent a structural challenge influencing UAE cloud infrastructure economics and expansion planning.

Data Sovereignty Fragmentation and Multi-Jurisdiction Compliance Complexity

UAE cloud infrastructure providers must navigate evolving data protection regulations, sector-specific residency requirements, and cross-border data transfer controls that vary across industries, creating compliance complexity for infrastructure design and service delivery models. Financial, healthcare, and government sectors impose distinct data localization and security requirements that necessitate segmented infrastructure environments and specialized certifications. Multi-cloud and hybrid architectures must ensure workload isolation and regulatory alignment across different jurisdictional mandates. Enterprises operating regionally face challenges aligning UAE sovereignty requirements with global cloud strategies and cross-border operations. Certification, auditing, and compliance management increase operational overhead for infrastructure providers. Regulatory evolution requires continuous infrastructure adaptation and documentation processes. International enterprises may hesitate to migrate sensitive workloads until compliance clarity is fully established. Telecom and cloud operators must invest in sovereign cloud variants and specialized environments to meet sector mandates. These fragmented regulatory requirements create structural complexity in UAE cloud infrastructure deployment and service standardization.

Opportunities

AI and High-Performance Computing Cloud Infrastructure Expansion

Rapid adoption of artificial intelligence, machine learning, and advanced analytics across government and enterprise sectors in the UAE is creating demand for specialized cloud infrastructure equipped with GPU clusters, high-speed interconnects, and optimized storage architectures capable of supporting computationally intensive workloads. National AI strategies and smart city initiatives require scalable AI training and inference environments hosted within sovereign cloud frameworks. Enterprises across finance, energy, logistics, and retail sectors are deploying AI-driven applications that depend on elastic high-performance cloud compute capacity. Hyperscalers and regional providers can expand differentiated AI infrastructure offerings to capture emerging workloads. Development of regional AI research ecosystems and innovation hubs further increases HPC infrastructure demand. Edge AI and real-time analytics applications in urban management and industrial automation require distributed cloud compute nodes integrated with central hyperscale regions. Sovereign AI cloud platforms present opportunities for specialized secure infrastructure deployments. These dynamics position AI-optimized cloud infrastructure as a major growth opportunity in UAE cloud markets.

Industry-Specific Sovereign Cloud Platforms and Verticalized Infrastructure Services

Increasing regulatory and operational specialization across sectors such as finance, healthcare, government, and energy is creating opportunities for cloud providers to develop verticalized sovereign cloud platforms tailored to sector compliance, security, and performance requirements within UAE jurisdiction. Sector-specific certifications, security controls, and data governance frameworks enable differentiated infrastructure offerings with higher value positioning. Financial cloud platforms with embedded compliance and transaction processing optimization address banking workload migration needs. Healthcare sovereign clouds supporting patient data security and clinical applications enable digital health infrastructure expansion. Government community clouds can centralize secure public service infrastructure across agencies. Energy sector digital twins and industrial analytics platforms require specialized high-reliability cloud environments. Telecom-integrated industry clouds enable low-latency applications across verticals. Managed sovereign cloud services for regulated industries create recurring infrastructure demand. These verticalized sovereign infrastructure models represent a strategic opportunity for UAE cloud providers to capture sector-specific digital transformation workloads.

Future Outlook

The UAE cloud infrastructure market is expected to experience sustained expansion driven by hyperscale data center capacity growth, sovereign cloud adoption, and enterprise digital transformation acceleration. AI-enabled infrastructure, edge cloud integration, and industry-specific sovereign platforms will shape technology evolution. Regulatory emphasis on data residency and cybersecurity will reinforce localized infrastructure investments. Government digitalization and smart city initiatives will continue anchoring long-term demand across public and regulated sectors.

Major Players

- Amazon Web Services

- Microsoft

- Google Cloud

- Oracle

- IBM

- e& (Etisalat)

- du

- Alibaba Cloud

- Huawei Cloud

- SAP

- Dell Technologies

- Hewlett Packard Enterprise

- VMware

- Equinix

- KhaznaData Centers

Key Target Audience

- Cloud infrastructure providers

- Telecom operators

- Data center developers

- Banking and financial institutions

- Healthcare providers

- Government and regulatory bodies

- Investments and venture capitalist firms

- Digital service enterprises

Research Methodology

Step 1: Identification of Key Variables

Key demand drivers, infrastructure capacity indicators, regulatory frameworks, and enterprise adoption variables relevant to UAE cloud infrastructure were identified through secondary data mapping and sectoral analysis across hyperscale, telecom, and sovereign cloud ecosystems.

Step 2: Market Analysis and Construction

Market sizing and segmentation were constructed by integrating infrastructure capacity data, enterprise cloud adoption patterns, hyperscaler regional deployment information, and sectoral demand indicators to establish deployment and end-user structures.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market structures and growth assumptions were validated through expert insights from cloud architects, telecom infrastructure specialists, enterprise IT leaders, and regulatory stakeholders within UAE digital infrastructure ecosystems.

Step 4: Research Synthesis and Final Output

Validated datasets and qualitative insights were synthesized into structured market analysis covering segmentation, competitive positioning, growth dynamics, and future outlook aligned with UAE cloud infrastructure development trajectories

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

National Sovereign Cloud and Data Residency Mandates

Hyperscale Data Center Localization and Expansion

Enterprise Digital Transformation and Cloud Migration Acceleration

AI and High Performance Computing Workload Growth

Smart City and Digital Government Platform Expansion - Market Challenges

High Energy Consumption and Cooling Cost Intensity

Regulatory Compliance and Data Sovereignty Fragmentation

Cybersecurity Risk and Infrastructure Protection Complexity

Skilled Cloud Infrastructure Workforce Constraints

Interoperability Challenges in Multi Cloud Environments - Market Opportunities

AI Optimized Sovereign Cloud Infrastructure Platforms

Industry Specific Regulated Cloud Environments

Edge Cloud Expansion for Real Time Digital Services - Trends

Hybrid and Multi Cloud Architecture Adoption

AI Native Cloud Infrastructure Integration

Telecom and Hyperscaler Partnership Models

Sustainable and Green Data Center Technologies

Edge and Distributed Cloud Deployment Growth - Government Regulations & Defense Policy

National Data Residency and Sovereign Hosting Regulations

Cybersecurity and Critical Infrastructure Protection Policies

Government Cloud First and Digital Transformation Mandates - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Compute Infrastructure Systems

Storage Infrastructure Systems

Networking Infrastructure Systems

Cloud Security Infrastructure Systems

Cloud Management and Orchestration Systems - By Platform Type (In Value%)

Hyperscale Cloud Platforms

Telecom Integrated Cloud Platforms

Enterprise Private Cloud Platforms

Sovereign Government Cloud Platforms

Edge Cloud Platforms - By Fitment Type (In Value%)

Public Cloud Deployments

Private Cloud Deployments

Hybrid Cloud Deployments

Multi Cloud Deployments

Sovereign Cloud Deployments - By EndUser Segment (In Value%)

Government and Public Sector Entities

Banking and Financial Institutions

Telecommunications and Digital Service Providers

Retail and E Commerce Enterprises

Healthcare and Life Sciences Organizations - By Procurement Channel (In Value%)

Direct Hyperscaler Procurement

Telecom Operator Cloud Contracts

System Integrator Led Procurement

Government Tender Procurement

Managed Service Provider Procurement - By Material / Technology (in Value %)

Virtualized Compute and Hypervisor Technologies

Software Defined Storage Technologies

Software Defined Networking Technologies

AI Accelerated GPU Infrastructure

Container and Kubernetes Platforms

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Cloud Service Portfolio, Data Center Capacity, Sovereign Compliance Capability, AI Infrastructure Capability, Telecom Integration, Regional Presence, Pricing Model Flexibility, Managed Services Depth, Industry Vertical Solutions)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Amazon Web Services

Microsoft Azure

Google Cloud

Oracle Cloud

IBM Cloud

Alibaba Cloud

Huawei Cloud

e& Enterprise

du Cloud

Khazna Data Centers

Equinix

SAP Cloud

Dell Technologies Cloud

Hewlett Packard Enterprise GreenLake

VMware Cloud

- Government digital platforms driving sovereign cloud demand

- Financial sector compliance accelerating localized cloud adoption

- Telecom operators integrating connectivity and cloud services

- Enterprise sectors migrating mission critical workloads to cloud

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now