Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UAE Cold Chain Logistics market demonstrates strong structural growth due to increasing pharmaceutical distribution, expanding food retail supply chains, and rising temperature-controlled transportation requirements across healthcare and food industries. Based on a recent historical assessment, the UAE cold chain logistics sector generated approximately USD ~ billion in revenue supported by advanced refrigerated warehousing infrastructure, integrated transportation networks, and strict compliance with pharmaceutical storage standards defined by regulatory authorities including the UAE Ministry of Health and the Emirates Authority for Standardization and Metrology.

Dubai and Abu Dhabi dominate the UAE Cold Chain Logistics market because they serve as major international trade gateways and host advanced logistics infrastructure, specialized pharmaceutical distribution hubs, and large-scale food import terminals. Dubai’s Jebel Ali Port and Al Maktoum International Airport facilitate high volumes of temperature-controlled imports and exports, while Abu Dhabi’s Khalifa Industrial Zone supports pharmaceutical and food logistics infrastructure. The presence of global logistics companies, modern cold storage facilities, and integrated supply chain technology platforms strengthens operational efficiency and distribution capabilities.

Market Segmentation

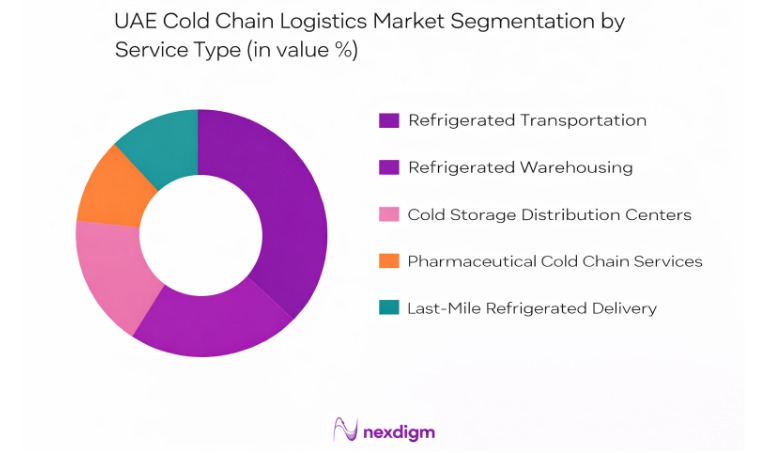

By Service Type

UAE Cold Chain Logistics market is segmented by service type into refrigerated transportation, refrigerated warehousing, cold storage distribution centers, pharmaceutical cold chain services, and last-mile refrigerated delivery. Recently, refrigerated transportation has a dominant market share due to strong demand for temperature-controlled movement of pharmaceuticals, vaccines, seafood, dairy products, and perishable foods across the UAE’s urban consumption centers. Expanding grocery retail networks, pharmaceutical imports, and rising e-commerce grocery deliveries require highly reliable refrigerated vehicle fleets and optimized route management systems. Logistics operators continue investing in temperature-controlled truck fleets, IoT-enabled monitoring systems, and real-time logistics management platforms to maintain strict compliance with pharmaceutical storage regulations and food safety standards. Increasing cross-border pharmaceutical trade through air cargo terminals further increases the reliance on refrigerated transportation infrastructure connecting ports, airports, distribution centers, and retail outlets across the UAE.

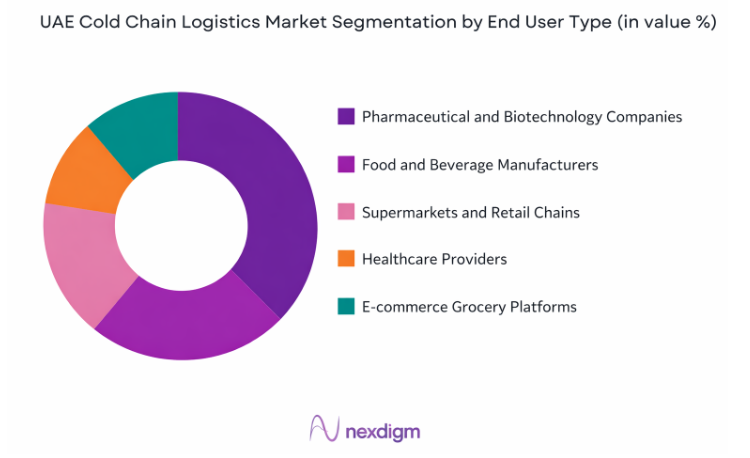

By End User Industry

UAE Cold Chain Logistics market is segmented by end user type into pharmaceutical and biotechnology companies, food and beverage manufacturers, supermarkets and retail chains, healthcare providers, and e-commerce grocery platforms. Recently, pharmaceutical and biotechnology companies have a dominant market share due to strict temperature control requirements for vaccines, biologics, insulin products, and specialized medicines. Pharmaceutical distributors depend heavily on validated cold storage facilities, temperature-controlled transport systems, and certified handling procedures to maintain drug stability throughout the supply chain. The UAE functions as a regional pharmaceutical distribution hub connecting global manufacturers to Middle Eastern, African, and Asian healthcare markets. Large hospital networks, clinical laboratories, and national vaccination programs further increase demand for pharmaceutical-grade logistics services, strengthening the role of specialized cold chain infrastructure supporting regulated healthcare product distribution.

Competitive Landscape

The UAE Cold Chain Logistics market features a moderately consolidated competitive environment where global logistics companies and regional supply chain providers compete through infrastructure investments, advanced refrigeration technologies, and integrated logistics platforms. International operators leverage global transportation networks and pharmaceutical compliance expertise, while regional companies focus on localized distribution capabilities and last-mile delivery networks. Strategic partnerships with pharmaceutical manufacturers, food importers, and retail chains strengthen market positioning while digital logistics platforms enhance supply chain visibility and temperature monitoring capabilities.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Cold Storage Capacity |

| DHL Supply Chain | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| CEVA Logistics | 2007 | France | ~ | ~ | ~ | ~ | ~ |

| Agility Logistics | 1979 | Kuwait | ~ | ~ | ~ | ~ | ~ |

| Aramex | 1982 | UAE | ~ | ~ | ~ | ~ | ~ |

UAE Cold Chain Logistics Market Analysis

Growth Drivers

Expansion of Pharmaceutical Distribution and Vaccine Logistics Infrastructure

Explanation continues in the same sentence. The UAE has become a major pharmaceutical distribution hub connecting manufacturers across Europe, Asia, and North America with healthcare markets throughout the Middle East and Africa. Pharmaceutical manufacturers rely heavily on validated cold chain logistics networks capable of maintaining stable temperature ranges during storage and transportation to preserve drug efficacy and safety. National healthcare systems import a wide range of temperature sensitive medical products including vaccines, insulin, biologics, and specialized therapies that require strict compliance with international pharmaceutical logistics standards. Logistics providers therefore invest heavily in pharmaceutical-grade refrigerated warehouses, temperature-controlled air cargo containers, and monitoring technologies designed to maintain compliance with Good Distribution Practice requirements. International pharmaceutical manufacturers often use the UAE as a regional logistics gateway due to its advanced port infrastructure, international air cargo capacity, and efficient customs clearance procedures. Global healthcare supply chains increasingly rely on reliable temperature monitoring systems that provide real time data on storage conditions and shipment environments. Hospitals, laboratories, and pharmaceutical distributors depend on specialized cold chain logistics infrastructure to ensure the safe delivery of critical medical supplies. Continuous expansion of healthcare infrastructure across the Middle East further increases demand for pharmaceutical cold chain logistics services that operate through UAE distribution hubs. As pharmaceutical innovation introduces more temperature sensitive therapies and biologic drugs, logistics providers must continuously upgrade refrigeration technologies and supply chain monitoring capabilities.

Growth of Temperature-Controlled Food Supply Chains Driven by Urban Consumption Patterns

The UAE imports a substantial share of its food supply due to limited domestic agricultural production, which significantly increases reliance on advanced cold chain logistics systems that maintain food quality and safety during international transport and domestic distribution. Perishable food products including dairy products, seafood, meat, frozen foods, fruits, and vegetables require carefully controlled storage temperatures throughout transportation and warehousing operations. Large supermarket chains, food distributors, and hospitality companies therefore depend on reliable refrigerated supply chains that connect global suppliers with retail outlets and restaurants. Urban population growth and high consumer demand for imported food products further increase the importance of temperature controlled logistics networks supporting the national food supply system. Major logistics hubs located near ports and airports operate large refrigerated storage facilities designed to preserve food products before distribution across the country. Online grocery platforms have also accelerated demand for last mile refrigerated delivery systems that transport perishable foods directly to residential customers. Logistics companies invest in advanced refrigeration technologies, route optimization software, and digital temperature monitoring solutions to improve food supply chain efficiency. Food safety regulations require strict temperature compliance throughout the distribution process, encouraging continuous modernization of cold storage facilities and refrigerated transport fleets. As the UAE continues expanding food imports to support its growing population and tourism sector, the importance of reliable cold chain logistics infrastructure continues to increase across the national supply chain network.

Market Challenges

High Operational Costs Associated with Energy Intensive Refrigeration Infrastructure

Cold chain logistics operations require large scale refrigeration infrastructure that consumes significant amounts of electricity to maintain stable temperature environments inside warehouses, transportation containers, and refrigerated vehicles. Operating these temperature controlled environments continuously across storage facilities and transportation fleets creates high operational costs for logistics providers. Electricity consumption remains one of the largest cost components within cold chain logistics operations due to the need for constant refrigeration across storage and transport infrastructure. Logistics companies must therefore invest heavily in energy efficient refrigeration technologies and facility design in order to manage operational expenses. The UAE’s hot desert climate further increases energy requirements because refrigeration systems must work harder to maintain internal storage temperatures despite extreme external heat conditions. Maintaining pharmaceutical and food safety compliance also requires redundant cooling systems, backup power infrastructure, and advanced monitoring technologies that further increase operational costs. Temperature monitoring systems, digital tracking platforms, and automated refrigeration controls require ongoing maintenance and technical support that add additional cost pressures to cold chain logistics operations. Logistics companies must also invest in skilled personnel trained in refrigeration system maintenance and pharmaceutical logistics compliance. High capital investment requirements for cold storage infrastructure and specialized refrigerated vehicle fleets create additional financial barriers for new market entrants. These operational challenges require logistics providers to continuously optimize energy efficiency, infrastructure utilization, and logistics network planning in order to maintain profitability while delivering reliable temperature controlled supply chain services.

Limited Availability of Skilled Cold Chain Logistics Workforce and Technical Expertise

Cold chain logistics operations require specialized technical expertise to manage refrigeration systems, temperature monitoring technologies, pharmaceutical compliance protocols, and complex supply chain coordination processes. Logistics companies depend on skilled technicians capable of maintaining refrigeration equipment, monitoring storage conditions, and ensuring compliance with international pharmaceutical distribution standards. However, the availability of trained professionals with expertise in cold chain logistics remains limited across many regional markets including the UAE. Refrigeration engineers, pharmaceutical logistics specialists, and temperature monitoring system operators require specialized training and certification programs that are not widely available in the logistics workforce. Companies must therefore invest heavily in workforce training programs to ensure staff members understand the operational requirements associated with temperature controlled logistics systems. Logistics companies also rely on international technical experts to support advanced cold chain infrastructure development and operational management. Workforce shortages can increase operational risks because improper handling of temperature sensitive products can compromise pharmaceutical safety and food quality. Logistics operators therefore implement strict training programs and certification standards to maintain high operational standards across cold chain logistics networks. As cold chain logistics infrastructure continues expanding across the UAE, the demand for skilled technicians and logistics professionals capable of managing advanced refrigeration systems continues to increase significantly.

Opportunities

Expansion of Biopharmaceutical Manufacturing and Regional Vaccine Distribution Networks

Explanation continues in the same sentence. The global pharmaceutical industry increasingly develops biologic medicines, vaccines, and advanced therapies that require highly controlled temperature conditions during storage and transportation throughout the supply chain. The UAE has positioned itself as a regional pharmaceutical distribution hub capable of supporting these complex logistics requirements through advanced cold chain infrastructure and international trade connectivity. Pharmaceutical manufacturers continue expanding distribution networks that rely on specialized cold storage facilities, validated temperature monitoring systems, and compliant logistics procedures designed to protect temperature sensitive medicines. Regional healthcare demand for biologic drugs, vaccines, and specialized therapies continues increasing due to expanding healthcare infrastructure and growing patient populations across the Middle East and Africa. Logistics providers therefore have significant opportunities to expand pharmaceutical logistics services that support vaccine distribution programs and advanced medical treatments. Investments in pharmaceutical-grade warehouses, temperature controlled air cargo containers, and digital monitoring platforms enable logistics companies to handle highly sensitive medical products safely and efficiently. International pharmaceutical companies increasingly partner with logistics providers capable of maintaining strict temperature control throughout global supply chains. These developments create opportunities for logistics operators to develop specialized healthcare logistics divisions that support pharmaceutical distribution networks across regional healthcare markets. As biologic drug development continues expanding globally, demand for highly reliable pharmaceutical cold chain logistics infrastructure continues to grow significantly.

Adoption of Smart Cold Chain Monitoring and Automation Technologies

Explanation continues in the same sentence. Advances in digital logistics technologies are transforming the cold chain logistics industry by enabling real time monitoring of temperature conditions, shipment locations, and storage environments throughout the supply chain. Internet of Things sensors, cloud based logistics platforms, and automated warehouse management systems provide logistics operators with detailed visibility into cold chain operations across transportation networks and storage facilities. These technologies enable early detection of temperature deviations that could compromise product safety, allowing logistics providers to respond quickly and prevent product spoilage or pharmaceutical degradation. Automation technologies also improve warehouse efficiency by optimizing storage conditions, inventory management, and refrigeration energy consumption. Logistics providers increasingly deploy robotics and automated handling systems inside refrigerated warehouses to improve operational efficiency while reducing manual handling risks. Digital monitoring technologies also enable pharmaceutical manufacturers and food distributors to track product conditions throughout transportation and storage processes. Governments and regulatory agencies encourage the adoption of advanced monitoring technologies that improve transparency and compliance across pharmaceutical and food supply chains. As digital logistics technologies continue advancing, companies that invest in smart cold chain monitoring platforms and automated refrigeration systems gain significant operational advantages in maintaining product integrity and supply chain efficiency.

Future Outlook

The UAE Cold Chain Logistics market is expected to experience strong expansion driven by rising pharmaceutical distribution volumes, increasing demand for temperature-controlled food logistics, and growing e-commerce grocery delivery networks. Logistics companies are investing in automated cold storage facilities, smart temperature monitoring technologies, and integrated multimodal logistics infrastructure. Government initiatives supporting food security and pharmaceutical supply chains will further strengthen demand for advanced cold chain logistics systems. Increasing regional trade connectivity and healthcare distribution networks will continue supporting long-term market development.

Major Players

- DHL Supply Chain

- Kuehne + Nagel

- CEVA Logistics

- Agility Logistics

- Aramex

- Gulf Agency Company

- DB Schenker

- FedEx Logistics

- UPS Healthcare Logistics

- Hellmann Worldwide Logistics

- Milaha Logistics

- Al-Futtaim Logistics

- Emirates SkyCargo

- RSA Global

- Tristar Group

Key Target Audience

- Pharmaceutical and biotechnology companies

- Food and beverage manufacturers

- Retail and supermarket chains

- E-commerce grocery platforms

- Healthcare and hospital networks

- Logistics infrastructure developers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables including refrigerated storage capacity, transportation fleet size, pharmaceutical distribution demand, and food logistics infrastructure are identified to evaluate the UAE Cold Chain Logistics market structure and performance indicators. Industry reports, government publications, and logistics infrastructure data provide the initial dataset for market analysis.

Step 2: Market Analysis and Construction

The market framework is constructed by mapping cold chain logistics infrastructure, analyzing supply chain networks, and evaluating operational capabilities of logistics service providers. Demand patterns across pharmaceutical distribution, food imports, and retail supply chains are incorporated to determine market segmentation.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics executives, pharmaceutical supply chain specialists, and refrigeration technology providers are consulted to validate market assumptions and operational insights. Feedback from these stakeholders strengthens the reliability of market drivers, constraints, and infrastructure trends identified in the analysis.

Step 4: Research Synthesis and Final Output

Quantitative data and qualitative insights are integrated to generate a comprehensive assessment of the UAE Cold Chain Logistics market. The research process synthesizes supply chain infrastructure data, competitive landscape analysis, and regulatory frameworks to produce the final market intelligence report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of Pharmaceutical Distribution and Vaccine Logistics Infrastructure

Rapid Growth of Online Grocery and Food Delivery Platforms

Government Investments in Food Security and Cold Storage Infrastructure - Market Challenges

High Capital Investment Required for Temperature Controlled Infrastructure

Energy Intensive Operations and High Operational Costs

Complex Compliance with Pharmaceutical and Food Safety Standards - Market Opportunities

Expansion of Biopharmaceutical Manufacturing and Distribution Networks

Growth of Export Oriented Food Processing and Seafood Trade

Adoption of Smart Cold Chain Monitoring and Automation Technologies - Trends

Integration of IoT Enabled Temperature and Fleet Monitoring Systems

Development of Automated Cold Storage Warehouses and Robotics

Growth of Urban Micro Fulfillment Refrigerated Distribution Centers - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Refrigerated Warehousing

Temperature Controlled Transportation

Cold Storage Distribution Centers

Blast Freezing and Quick Freezing Systems

Pharmaceutical Grade Cold Chain Systems - By Platform Type (In Value%)

Road Transport Cold Chain

Air Cargo Cold Chain

Sea Freight Cold Chain

Integrated Multimodal Cold Chain

Urban Last Mile Refrigerated Delivery - By Fitment Type (In Value%)

Standalone Refrigerated Facilities

Integrated Warehouse and Transport Systems

Modular Cold Storage Units

Mobile Refrigerated Containers

IoT Enabled Temperature Monitoring Systems - By EndUser Segment (In Value%)

Pharmaceutical and Biotechnology Companies

Food and Beverage Manufacturers

Retail and Supermarket Chains

- Market Share Analysis

- CrossComparison Parameters (Cold Storage Capacity, Fleet Size, Temperature Compliance Standards, Service Coverage Network, Technology Integration)

- SWOT Analysis of Key Competitors

Pricing & Procurement Analysis

Porter’s Five Forces

Key Players

Agility Logistics

Gulf Agency Company (GAC)

Aramex

Emirates SkyCargo

Tristar Group

RSA Global

Kuehne + Nagel

DHL Supply Chain

DB Schenker

FedEx Logistics

UPS Healthcare Logistics

Milaha Logistics

Hellmann Worldwide Logistics

CEVA Logistics

Al-Futtaim Logistics

- Pharmaceutical Manufacturers Requiring Strict Temperature Controlled Distribution

- Food Retail Chains Expanding Refrigerated Supply Chain Networks

- Healthcare Providers Managing Vaccine and Biologic Storage Requirements

- E-commerce Grocery Platforms Driving Demand for Urban Cold Chain Logistics

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now