Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the UAE defense market reached approximately USD ~ billion in military expenditure, supported by sustained modernization programs and procurement initiatives, according to Global Data. Strategic investments across army, air force, and naval capabilities continue to reinforce national security priorities amid regional tensions involving Iran and Yemen. Rising geopolitical uncertainty and expanded defense planning have accelerated acquisition cycles, while increased per capita spending reflects strong fiscal commitment toward maintaining advanced operational readiness and deterrence capabilities.

Abu Dhabi dominates the defense ecosystem due to its concentration of military headquarters, procurement authorities, and domestic defense manufacturers, including large state-backed industrial groups that strengthen sovereign capability. Dubai also plays a significant role through logistics infrastructure, aerospace services, and international defense exhibitions that attract global contractors. The UAE’s strategic Middle East location supports multinational partnerships, while normalization initiatives with Israel have enabled technology cooperation, reinforcing the country’s positioning as a regional defense innovation hub.

Market Segmentation

By Product Type

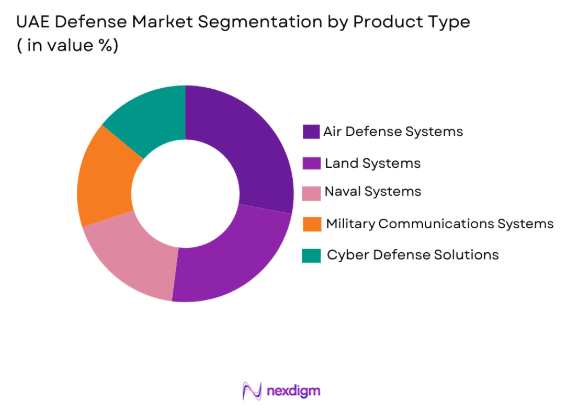

UAE Defense Market is segmented by product type into land systems, air defense systems, naval systems, cyber defense solutions, and military communications systems. Recently, air defense systems have a dominant market share due to factors such as escalating missile threats, regional instability, and the government’s focus on integrated protection infrastructure. Continuous investments in radar networks, interceptor technologies, and early warning platforms have strengthened demand. Advanced procurement strategies prioritize layered defense architectures capable of countering aerial and ballistic threats, while partnerships with global contractors enhance technological transfer. Additionally, modernization of legacy platforms and alignment with network-centric warfare doctrines have elevated adoption, ensuring operational resilience and faster threat response across critical national assets.

By Platform Type

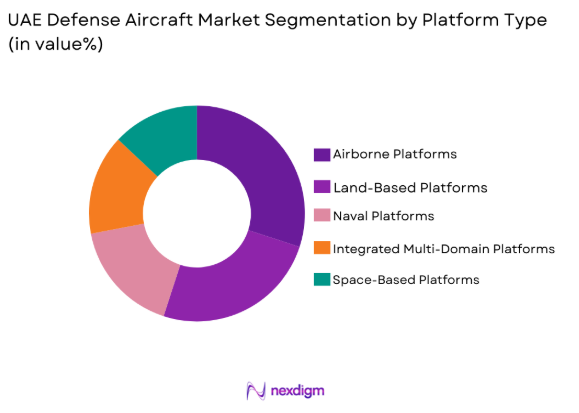

UAE Defense Market is segmented by platform type into land-based platforms, airborne platforms, naval platforms, space-based platforms, and integrated multi-domain platforms. Recently, airborne platforms have a dominant market share due to factors such as rapid response requirements, surveillance expansion, and emphasis on air superiority. Investments in fighter aircraft upgrades, unmanned aerial systems, and airborne intelligence platforms continue to drive procurement momentum. Enhanced border monitoring capabilities and expeditionary readiness further reinforce adoption. Collaborative defense agreements and training interoperability with allied nations have also increased reliance on advanced aviation assets, while modernization agendas prioritize precision engagement capabilities and extended operational range to address evolving security dynamics effectively.

Competitive Landscape

The UAE defense market demonstrates moderate consolidation, characterized by strong state-backed enterprises alongside global contractors supplying advanced systems. Strategic joint ventures and technology transfer agreements shape competition, while domestic industrialization policies support localized manufacturing. Major players maintain influence through integrated solutions spanning cyber, aerospace, and land systems, reinforcing long-term procurement partnerships with defense authorities.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Government Partnership Level |

| EDGE Group | 2019 | Abu Dhabi | ~ | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1995 | USA | ~ | ~ | ~ | ~ | ~ |

| Raytheon Technologies | 2020 | USA | ~ | ~ | ~ | ~ | ~ |

| BAE Systems | 1999 | UK | ~ | ~ | ~ | ~ | ~ |

| Thales Group | 2000 | France | ~ | ~ | ~ | ~ | ~ |

UAE Defense Market Analysis

Growth Drivers

Strategic Military Modernization Programs

The UAE’s sustained commitment to upgrading its armed forces has become a central catalyst driving defense market expansion, supported by military expenditure reaching approximately USD ~ billion according to GlobalData. Government planners continue to prioritize advanced weapons acquisition, next-generation command systems, and integrated battlefield technologies to ensure preparedness against evolving threats in the Middle East security environment. Procurement strategies increasingly emphasize interoperability across land, air, and naval domains, allowing the armed forces to operate within joint mission frameworks that enhance response efficiency during crises. Continuous capability development has encouraged long-term supplier relationships, prompting global contractors to deepen regional presence through partnerships, maintenance agreements, and localized production facilities aligned with national industrial strategies. Additionally, investment in precision-guided munitions, surveillance architectures, and electronic warfare capabilities reflects a doctrinal shift toward technologically superior deterrence rather than manpower-heavy deployments. Defense planners are also reinforcing layered defense networks capable of countering ballistic missiles, unmanned systems, and asymmetric attack vectors, strengthening infrastructure protection across energy corridors and urban centers. Institutional reforms that streamline procurement governance have improved acquisition timelines, enabling faster deployment of critical systems without compromising compliance requirements. Rising per capita defense expenditure further signals fiscal resilience and demonstrates that modernization remains embedded within broader national security planning despite fluctuating macroeconomic conditions. Meanwhile, collaboration with allied militaries has intensified training exchanges and operational benchmarking, indirectly accelerating technology adoption as forces align with international performance standards. Collectively, these modernization initiatives sustain procurement momentum, stimulate domestic manufacturing ambitions, and reinforce the UAE’s long-term objective of maintaining technologically advanced armed forces capable of navigating complex geopolitical realities.

Expansion of Domestic Defense Manufacturing Ecosystem

The emergence of indigenous defense production capabilities is reshaping procurement dynamics by reducing reliance on imports while strengthening supply chain sovereignty within the UAE security architecture. State-backed industrial groups have expanded portfolios across autonomous platforms, cyber technologies, precision weapons, and naval engineering, positioning the country as a regional production hub rather than solely a buyer of foreign equipment. This industrial evolution aligns with national diversification agendas that seek to transform defense spending into a catalyst for high-value manufacturing, research employment, and advanced engineering competencies. Government support mechanisms, including strategic funding channels and partnership frameworks, have encouraged joint ventures with global technology leaders, accelerating knowledge transfer and fostering localized innovation cycles. Domestic assembly lines and maintenance facilities also shorten lifecycle support timelines, ensuring operational readiness while minimizing logistical dependencies during periods of geopolitical disruption. The integration of artificial intelligence, robotics, and advanced materials within locally produced systems further enhances competitiveness, allowing manufacturers to address both national requirements and export opportunities. Increasing arms revenues among Middle Eastern producers, supported by demand linked to regional conflicts, demonstrate the commercial viability of expanding production footprints. Industrial clustering within Abu Dhabi has created an ecosystem where research institutes, defense contractors, and testing facilities collaborate on next-generation capabilities, reinforcing technological self-sufficiency. Workforce development initiatives are simultaneously cultivating specialized talent pools capable of sustaining long-term innovation trajectories across aerospace and cyber domains. As domestic manufacturing scales, the UAE strengthens negotiating leverage in international procurement discussions while building an export-oriented defense economy that supports sustained market growth.

Market Challenges

High Capital Intensity and Budgetary Allocation Constraints

Defense capability development requires substantial financial commitments, and although the UAE demonstrates strong fiscal capacity, the scale of investment necessary for advanced systems places persistent pressure on long-term budget optimization. Modern missile defense architectures, stealth aircraft integration, and digital battlefield networks involve multibillion-dollar lifecycle costs encompassing procurement, maintenance, upgrades, and personnel training. Such financial intensity necessitates careful prioritization across competing national spending areas including infrastructure, social programs, and economic diversification initiatives. Even with consistent expenditure growth, defense authorities must evaluate opportunity costs to ensure strategic balance without overstretching public finances during periods of global economic uncertainty. Complex procurement cycles also increase exposure to cost overruns, particularly when integrating cutting-edge technologies that demand customized engineering and extended testing phases. Currency fluctuations and inflation within global defense supply chains can further amplify acquisition expenses, complicating long-term contract planning. Additionally, maintaining readiness across multiple domains requires recurring investments that extend well beyond initial purchases, reinforcing the structural nature of defense spending obligations. Policymakers must therefore adopt rigorous evaluation frameworks to align capability ambitions with sustainable fiscal trajectories while preserving operational superiority. Budget transparency expectations and governance standards add another layer of scrutiny, compelling authorities to demonstrate value realization from large-scale programs. Consequently, while financial strength supports modernization, the capital-intensive nature of defense transformation remains a structural constraint influencing procurement pacing and portfolio selection.

Dependence on Foreign Technology and Supply Chains

Despite rapid progress in domestic manufacturing, the UAE continues to rely on external suppliers for several high-end technologies including advanced propulsion systems, specialized semiconductors, and certain missile components. This reliance exposes procurement strategies to geopolitical restrictions, export controls, and regulatory approvals that can delay program execution or limit technology access during periods of diplomatic tension. Supply chain disruptions observed across global defense industries have highlighted vulnerabilities associated with concentrated production hubs and scarce critical minerals required for electronics and weapons manufacturing. Integration challenges also arise when combining foreign-developed platforms with locally produced subsystems, often requiring complex interoperability testing that extends deployment timelines. Intellectual property constraints may restrict modification capabilities, reducing flexibility in customizing systems to specific operational doctrines. Furthermore, vendor lock-in risks can emerge when long-term maintenance contracts tie armed forces to particular suppliers, potentially constraining competitive pricing leverage. Efforts to diversify sourcing channels demand significant coordination and certification processes, adding administrative complexity to acquisition planning. Technology transfer agreements mitigate some exposure but frequently involve phased implementation that delays full autonomy. Cybersecurity considerations additionally require rigorous vetting of imported software-driven systems to prevent embedded vulnerabilities. As a result, while international partnerships remain essential for technological advancement, external dependency continues to represent a strategic challenge influencing resilience and procurement agility.

Opportunities

Integration of Artificial Intelligence and Autonomous Defense Systems

Rapid advances in artificial intelligence present transformative opportunities for the UAE defense market by enabling predictive threat detection, automated surveillance, and decision-support tools that enhance operational efficiency across multi-domain environments. Defense planners increasingly recognize that AI-driven architectures can compress response timelines while reducing cognitive burdens on personnel operating within high-pressure mission scenarios. Autonomous aerial and maritime platforms equipped with advanced analytics expand persistent monitoring capabilities, particularly across critical maritime routes and border regions requiring continuous oversight. Investments in machine learning algorithms also strengthen cyber defense frameworks by identifying anomalies before they escalate into operational disruptions. Collaborative initiatives between domestic manufacturers and international technology firms are accelerating experimentation cycles, allowing prototypes to transition more quickly into deployable systems. AI-enabled maintenance diagnostics further optimize asset availability by forecasting component failures and minimizing downtime within high-value fleets. Training ecosystems are simultaneously evolving through simulation platforms that replicate complex combat conditions without the risks associated with live exercises. As defense doctrines increasingly emphasize network-centric warfare, intelligent data fusion becomes essential for synthesizing inputs from satellites, sensors, and battlefield units into unified command views. Regulatory openness toward emerging technologies supports structured testing environments while maintaining oversight standards. Collectively, the integration of AI and autonomy positions the UAE to enhance deterrence credibility while cultivating a technologically differentiated defense posture.

Growing Defense Export Potential and Regional Industrial Leadership

The UAE is progressively transitioning from a predominantly import-oriented defense posture toward an export-capable industrial model, creating new revenue pathways that can reinforce long-term market sustainability. Rising arms revenues among Middle Eastern producers indicate expanding demand for regionally manufactured systems, particularly those optimized for desert operations and asymmetric threat environments. Export growth enhances economies of scale, enabling manufacturers to distribute development costs across broader customer bases while improving price competitiveness. Strategic participation in international defense exhibitions strengthens visibility and fosters procurement dialogues with emerging military buyers seeking diversified sourcing options. Government-backed financing structures and diplomatic engagement further support export negotiations by aligning defense trade with broader foreign policy objectives. Industrial partnerships are also facilitating co-production arrangements that allow overseas customers to participate in localized assembly, increasing attractiveness while deepening bilateral ties. As domestic research capabilities mature, intellectual property ownership expands, granting manufacturers greater control over product roadmaps and customization pathways. Workforce specialization in advanced engineering disciplines reinforces credibility among global procurement agencies evaluating supplier reliability. Additionally, export-driven growth can stimulate adjacent sectors such as aerospace services, cybersecurity, and advanced materials manufacturing. This evolution toward regional industrial leadership ultimately strengthens economic resilience while elevating the UAE’s influence within the global defense marketplace.

Future Outlook

The UAE defense market is expected to sustain steady expansion driven by modernization priorities, indigenous manufacturing growth, and adoption of advanced digital warfare technologies. Regulatory backing for domestic production and joint ventures is likely to strengthen industrial self-sufficiency while supporting export ambitions. Increasing emphasis on cybersecurity, autonomous systems, and integrated command networks will reshape capability development. Demand-side momentum should remain supported by regional security considerations and strategic deterrence planning, reinforcing long-term procurement pipelines.

Major Key Players

- Lockheed Martin

- Raytheon Technologies

- BAE Systems

- Thales Group • Northrop Grumman

- Leonardo S.p.A.

- Saab AB

- Boeing Defense

- Elbit Systems

- Rheinmetall AG

- L3Harris Technologies

- General Dynamics

- Dassault Aviation

- MBDA

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Defense manufacturers

- Aerospace system integrators

- Cybersecurity solution providers

- Military communications vendors

- Autonomous systems developers

- Defense logistics providers

Research Methodology

Step 1: Identification of Key Variables

Core variables including defense expenditure, procurement trends, geopolitical drivers, industrial participation, and technology adoption were identified through structured secondary research. Emphasis was placed on credible institutional datasets and defense publications to establish a reliable analytical baseline.

Step 2: Market Analysis and Construction

The market framework was constructed by synthesizing expenditure data, capability development patterns, and supplier activity. Segmentation logic was applied to map demand across product and platform categories while aligning findings with national defense strategies.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary insights were evaluated against defense policy developments and industry commentary to validate assumptions. Expert perspectives from aerospace and security domains supported refinement of competitive positioning and procurement dynamics.

Step 4: Research Synthesis and Final Output

Validated data points were integrated into a cohesive narrative supported by quantitative indicators. Analytical consistency checks ensured alignment between market drivers, challenges, and opportunity pathways before finalizing the report output.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising military expenditure supported by a defense budget of about USD ~ billion based on IMF data

Strategic geopolitical positioning encouraging continuous modernization of armed forces

Expansion of indigenous defense manufacturing capabilities through technology partnerships

Adoption of advanced unmanned and autonomous systems

Growing investment in cyber defense and electronic warfare infrastructure - Market Challenges

High dependency on foreign defense suppliers for advanced platforms

Complex regulatory approvals associated with arms procurement

Budget allocation pressures during economic diversification efforts

Integration challenges across multi-domain operational systems

Rising lifecycle and maintenance costs of advanced equipment - Market Opportunities

Localization initiatives promoting domestic defense production

Expansion of AI-driven battlefield and surveillance capabilities

Strengthening regional defense collaborations and joint ventures - Trends

Shift toward multi-domain warfare readiness

Increasing deployment of unmanned aerial and ground systems

Greater emphasis on cybersecurity resilience

Adoption of smart command-and-control architectures

Growing participation in international defense exhibitions and partnerships - Government Regulations & Defense Policy

National defense strategies prioritizing technological sovereignty

Export control frameworks governing arms transfers

Procurement policies supporting local industrial participation

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Air Defense Systems

Naval Combat Systems

Armored and Tactical Vehicles

Military Aircraft and UAV Systems

Cybersecurity and Electronic Warfare Systems - By Platform Type (In Value%)

Land-Based Platforms

Airborne Platforms

Naval Platforms

Space-Enabled Defense Platforms

Integrated Multi-Domain Platforms - By Fitment Type (In Value%)

Line-Fit Systems

Retrofit Upgrades

Modular Deployments

Network-Centric Installations

Mobile Rapid Deployment Systems - By End User Segment (In Value%)

Armed Forces

National Guard

Homeland Security Agencies

Special Operations Forces

Defense Research Organizations - By Procurement Channel (In Value%)

Government-to-Government Agreements

Direct Ministry Procurement

Strategic Defense Partnerships

International Competitive Tendering

Domestic Defense Contracts - By Material / Technology (in Value %)

Composite Armor Materials

AI-Enabled Defense Technologies

Hypersonic and Missile Technologies

Advanced Radar and Sensor Technologies

Secure Communication Networks

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Technology Capability, Platform Diversity, Contract Value, Localization Strategy, R&D Investment, Supply Chain Strength, Interoperability Standards, Lifecycle Support, Strategic Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

EDGE Group

Lockheed Martin

Raytheon Technologies

Northrop Grumman

Boeing Defense

BAE Systems

Thales Group

Leonardo

Rheinmetall AG

Saab AB

Elbit Systems

L3Harris Technologies

General Dynamics

Naval Group

Hanwha Aerospace

- Armed forces increasingly prioritize network-centric warfare capabilities

- Homeland security agencies invest in integrated surveillance infrastructure

- Special operations units demand lightweight and high-mobility platforms

- Defense research entities focus on next-generation weapons and AI integration

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now