Download PDF

Download PDF Download PDF

Download PDFMarket Overview

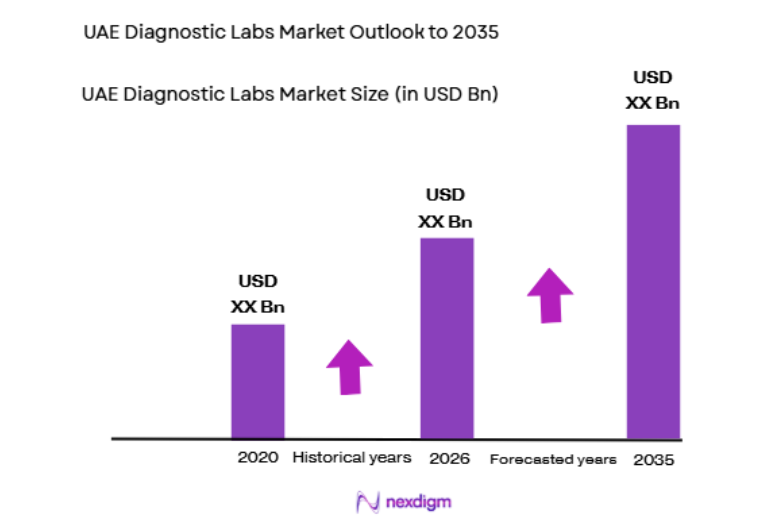

The UAE diagnostic labs market has grown steadily as healthcare providers increasingly rely on laboratory testing to support clinical decision making and preventive healthcare programs. Based on a recent historical assessment, the UAE diagnostic labs market size is valued at approximately USD ~ billion, supported by expanding healthcare infrastructure and rising diagnostic testing demand across hospitals and standalone laboratories. Government investments in advanced medical laboratories, increasing chronic disease screening programs, and expanding private healthcare networks continue to drive demand for diagnostic testing services across the country.

Dubai and Abu Dhabi dominate the UAE diagnostic laboratory ecosystem due to advanced healthcare infrastructure, strong regulatory oversight, and the presence of large hospital networks and international diagnostic service providers. Dubai’s healthcare free zones and medical tourism initiatives attract global laboratory service companies and advanced testing facilities. Abu Dhabi also plays a key role through large hospital systems and government supported healthcare modernization programs. These cities host numerous accredited diagnostic laboratories that offer advanced pathology and molecular testing services.

Market Segmentation

Market Segmentation

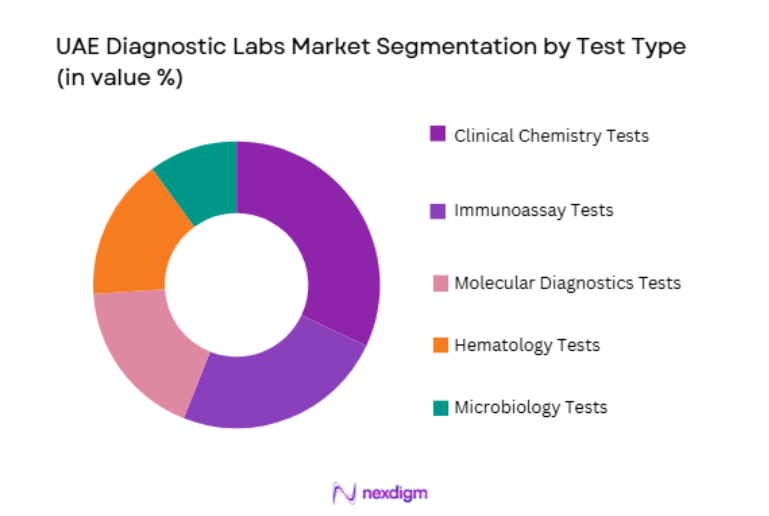

By Test Type

UAE Diagnostic Labs market is segmented by test type into clinical chemistry tests, immunoassay tests, molecular diagnostics tests, hematology tests, and microbiology tests. Recently, clinical chemistry tests has a dominant market share due to increasing demand for routine diagnostic screening across hospitals, clinics, and preventive healthcare programs. Clinical chemistry testing is widely used to monitor metabolic conditions, kidney function, liver health, and cardiovascular risk indicators, which makes it one of the most frequently ordered diagnostic procedures in healthcare systems. Hospitals and diagnostic laboratories rely on automated clinical chemistry analyzers to process large volumes of blood samples efficiently while maintaining high testing accuracy. Government health screening initiatives and employer sponsored health checkup programs further increase the demand for routine biochemical testing services.

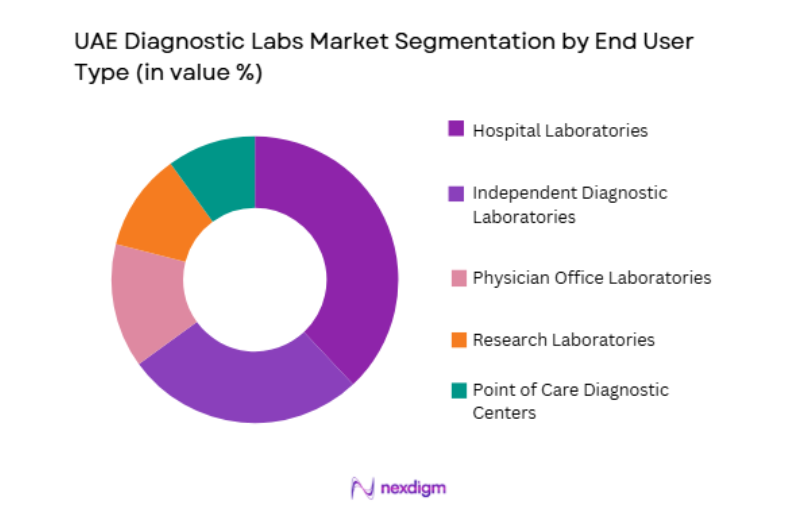

By End User

By End User

UAE Diagnostic Labs market is segmented by end user into hospital laboratories, independent diagnostic laboratories, physician office laboratories, research laboratories, and point of care diagnostic centers. Recently, hospital laboratories has a dominant market share due to the large number of diagnostic tests performed within hospital networks and integrated healthcare systems. Hospitals operate centralized diagnostic laboratories capable of conducting a wide range of medical tests including pathology, clinical chemistry, microbiology, and molecular diagnostics. Hospital laboratories benefit from strong patient inflow and integrated clinical workflows that enable physicians to order laboratory tests and receive results rapidly during patient treatment.

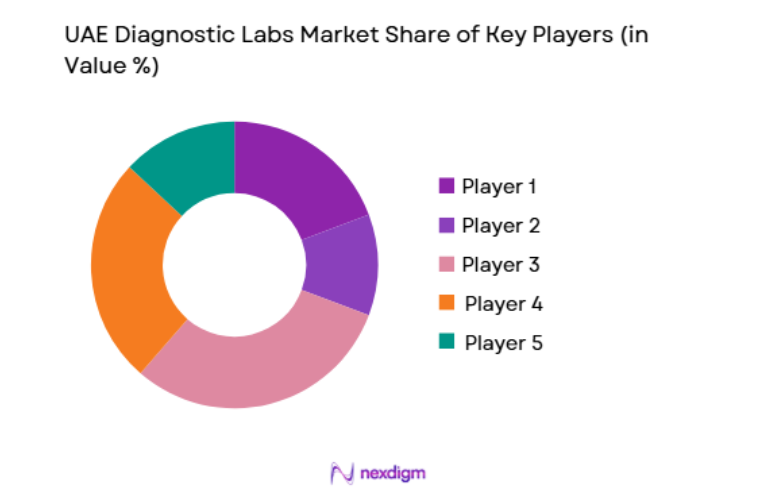

Competitive Landscape

Competitive Landscape

The UAE diagnostic labs market features a competitive environment where international laboratory service providers, regional diagnostic companies, and hospital owned laboratories compete to expand diagnostic testing capabilities. Large diagnostic networks continue to strengthen market presence through laboratory acquisitions, strategic partnerships with hospitals, and expansion of specialized testing services such as molecular diagnostics and genetic testing. Market consolidation is gradually increasing as larger laboratory chains expand regional laboratory networks.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Laboratory Network Coverage |

| Pure Health | 2006 | UAE | ~ | ~ | ~ | ~ | ~ |

| NMC Healthcare | 1975 | UAE | ~ | ~ | ~ | ~ | ~ |

| Aster DM Healthcare | 1987 | UAE | ~ | ~ | ~ | ~ | ~ |

| Unilabs | 1987 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Eurofins Scientific | 1987 | Luxembourg | ~ | ~ | ~ | ~ | ~ |

UAE Diagnostic Labs Market Analysis

UAE Diagnostic Labs Market Analysis

Growth Drivers

Expansion of Preventive Healthcare and Routine Diagnostic Screening Programs

Preventive healthcare initiatives are becoming a central component of healthcare strategies across the UAE, which significantly increases demand for diagnostic laboratory testing services across hospitals, clinics, and independent diagnostic laboratories. Healthcare authorities actively promote early disease detection through routine health screening programs that include blood testing, metabolic panels, and infectious disease diagnostics, which drive continuous demand for laboratory testing services across healthcare facilities. Employers across the UAE also conduct corporate health screening programs for employees that require regular diagnostic testing, further strengthening the demand for clinical laboratory services. Hospitals increasingly rely on laboratory diagnostics to support clinical decision making because accurate laboratory results enable physicians to diagnose diseases at early stages and implement appropriate treatment strategies. Rising awareness among patients regarding preventive health checkups also contributes to increasing utilization of laboratory testing services. Diagnostic laboratories deploy automated testing technologies capable of processing large volumes of samples efficiently while maintaining high accuracy and turnaround times. Healthcare insurers encourage preventive health screening because early detection of diseases reduces long term treatment costs and improves patient outcomes. Government healthcare programs continue investing in laboratory infrastructure and advanced diagnostic technologies to support population health management initiatives.

Rising Prevalence of Chronic Diseases and Increasing Demand for Advanced Diagnostics

The increasing prevalence of chronic diseases such as diabetes, cardiovascular diseases, and respiratory disorders across the UAE significantly drives demand for laboratory diagnostic services because these conditions require continuous monitoring and regular laboratory testing. Physicians rely heavily on laboratory tests to evaluate disease progression, monitor treatment effectiveness, and identify potential complications associated with chronic illnesses. Diagnostic laboratories perform biochemical tests, hormone analysis, and molecular diagnostics that provide critical clinical information for managing long term health conditions. Healthcare providers also conduct specialized laboratory tests for early detection of genetic disorders and cancer biomarkers that support personalized medicine approaches. The growing adoption of advanced diagnostic technologies including molecular diagnostics and genetic testing further expands laboratory testing capabilities across the UAE healthcare sector. Hospitals and diagnostic laboratories invest heavily in automated laboratory equipment and high throughput analyzers capable of processing large volumes of test samples with improved accuracy and efficiency. Rising lifestyle related risk factors such as obesity and sedentary lifestyles also contribute to increasing chronic disease prevalence, which leads to greater demand for laboratory testing services.

Market Challenges

High Operational Costs and Capital Intensive Laboratory Infrastructure

Diagnostic laboratories require significant financial investment in laboratory infrastructure, specialized testing equipment, and highly trained medical laboratory professionals, which creates operational challenges for diagnostic service providers operating within the UAE healthcare market. Advanced diagnostic technologies including molecular diagnostics platforms, automated analyzers, and genetic testing equipment require substantial capital expenditure and continuous maintenance to ensure reliable laboratory performance. Laboratories must also maintain strict quality control standards and accreditation requirements that involve ongoing investments in laboratory quality management systems and regulatory compliance programs. Highly skilled laboratory technicians and pathologists are essential for performing specialized diagnostic procedures and interpreting complex laboratory test results, which increases operational costs for laboratory service providers. Diagnostic laboratories also invest in laboratory information management systems that manage large volumes of diagnostic data and ensure efficient communication between healthcare providers and laboratory facilities. Rising operational costs can create financial pressure for smaller independent laboratories attempting to compete with larger diagnostic networks that benefit from economies of scale. Additionally, maintaining rapid turnaround times for laboratory test results requires efficient laboratory workflow management and continuous equipment maintenance. Healthcare providers often negotiate laboratory service pricing with diagnostic laboratories, which may limit profit margins for laboratory service providers.

Regulatory Compliance and Quality Accreditation Requirements

Diagnostic laboratories operating within the UAE healthcare system must comply with strict regulatory frameworks and quality accreditation standards designed to ensure accuracy and reliability of laboratory testing services. Healthcare regulatory authorities such as the Ministry of Health and Prevention, Dubai Health Authority, and Department of Health Abu Dhabi enforce laboratory licensing requirements and quality assurance protocols that diagnostic laboratories must follow before offering testing services. Laboratories must undergo regular inspections and accreditation processes to ensure compliance with international laboratory quality standards such as ISO medical laboratory accreditation frameworks. Compliance with these regulatory standards requires laboratories to implement rigorous quality control procedures, staff training programs, and laboratory process documentation systems that ensure diagnostic accuracy. Diagnostic laboratories also invest in advanced laboratory information systems capable of tracking test samples and maintaining secure patient data records in accordance with healthcare data protection regulations. Meeting regulatory requirements may increase operational complexity for laboratories because compliance procedures require continuous monitoring and documentation of laboratory operations. Smaller diagnostic laboratories may face challenges meeting regulatory compliance standards due to limited financial resources and technical expertise.

Opportunities

Growth of Molecular Diagnostics and Genetic Testing Services

Advances in molecular diagnostics and genetic testing technologies create strong opportunities for diagnostic laboratories operating within the UAE healthcare market because healthcare providers increasingly rely on advanced laboratory testing methods for disease detection and personalized medicine. Molecular diagnostic techniques enable laboratories to detect genetic mutations, infectious pathogens, and cancer biomarkers with high precision, which significantly improves clinical diagnosis and treatment planning. Healthcare institutions invest heavily in molecular diagnostic platforms capable of performing polymerase chain reaction testing and next generation sequencing technologies that support advanced disease detection. Physicians utilize genetic testing services to identify hereditary disease risks and develop personalized treatment strategies tailored to individual patient genetic profiles. Rising demand for cancer diagnostics and infectious disease testing further strengthens opportunities for laboratories specializing in molecular diagnostics. Government healthcare authorities also promote research initiatives supporting genomic medicine and precision healthcare programs that encourage adoption of advanced genetic testing technologies. Diagnostic laboratories collaborate with research institutions and biotechnology companies to expand testing capabilities and develop innovative diagnostic solutions. The increasing use of personalized medicine approaches within healthcare systems further strengthens demand for specialized laboratory testing services.

Expansion of Medical Tourism and International Healthcare Services

The UAE has emerged as a major destination for medical tourism in the Middle East due to advanced healthcare infrastructure and internationally accredited healthcare facilities, which creates significant opportunities for diagnostic laboratory service providers. International patients visiting the UAE for specialized medical treatments often require comprehensive diagnostic testing before undergoing surgical procedures or complex medical treatments. Hospitals serving medical tourists rely heavily on diagnostic laboratories capable of performing specialized pathology tests, imaging related laboratory diagnostics, and genetic screening services that support treatment planning. Healthcare free zones and international hospital partnerships further strengthen the country’s reputation as a global healthcare destination. Diagnostic laboratories located within major healthcare clusters benefit from increased patient volumes associated with international medical tourism. Advanced laboratory technologies and internationally accredited laboratory services also attract patients seeking reliable diagnostic testing services during their treatment journey. Healthcare providers collaborate with diagnostic laboratories to offer integrated healthcare services that include pre treatment diagnostic evaluations and post treatment monitoring. Government initiatives promoting healthcare tourism further support investment in advanced laboratory infrastructure across the country.

Future Outlook

The UAE diagnostic labs market is expected to experience sustained expansion as healthcare providers continue investing in advanced laboratory technologies and automated diagnostic systems. Increasing adoption of molecular diagnostics, genetic testing, and personalized medicine approaches will strengthen laboratory testing capabilities. Government healthcare modernization initiatives and expanding medical tourism will further support demand for diagnostic services.

Major Players

- Pure Health

- NMC Healthcare

- Aster DM Healthcare

- Eurofins Scientific

- Unilabs

- Synlab International

- Sonic Healthcare

- Quest Diagnostics

- Abbott Diagnostics

- Roche Diagnostics

- BioReference Laboratories

- Cerba Healthcare

- ARUP Laboratories

- Mayo Clinic Laboratories

- Al Borg Diagnostics

Key Target Audience

- Hospital networks and healthcare providers

- Independent diagnostic laboratory chains

- Pharmaceutical and biotechnology companies

- Medical device manufacturers

- Health insurance providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

Key variables affecting the UAE diagnostic labs market were identified through analysis of healthcare infrastructure expansion, laboratory testing demand, chronic disease prevalence, and regulatory frameworks governing diagnostic services across the country.

Step 2: Market Analysis and Construction

Market size estimation and segmentation were constructed using healthcare expenditure data, laboratory testing volumes, hospital diagnostic service utilization, and analysis of diagnostic laboratory infrastructure across public and private healthcare providers.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including laboratory specialists, healthcare administrators, and diagnostic equipment providers were consulted to validate laboratory testing trends and technological developments influencing diagnostic laboratory services.

Step 4: Research Synthesis and Final Output

All research findings were consolidated through structured analytical models to generate validated insights regarding market segmentation, competitive landscape, regulatory developments, and future growth opportunities within the UAE diagnostic labs market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising demand for preventive healthcare and routine diagnostics

Government support for advanced diagnostic infrastructure

Expansion of organized diagnostic laboratory networks across urban centers - Market Challenges

High capital investment for advanced diagnostic equipment

Shortage of skilled laboratory personnel

Regulatory compliance and accreditation requirements for laboratories - Market Opportunities

Expansion of home sample collection and digital reporting services

Adoption of AI based diagnostic and analytical tools

Growth in molecular and precision diagnostics services - Trends

Integration of laboratory information management systems (LIMS)

Rising demand for genomic and personalized diagnostic testing - Government Regulations

Laboratory accreditation standards under the DHA and MOHAP

Licensing and quality compliance for diagnostic facilities

Health data management and patient privacy regulations - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Pathology and Laboratory Testing Services

Radiology and Imaging Diagnostics

Molecular and Genomic Diagnostics

Point of Care Diagnostic Testing

Preventive Health Screening Services - By Platform Type (In Value%)

Standalone Diagnostic Laboratories

Hospital Based Diagnostic Laboratories

Chain Diagnostic Laboratory Networks

Home Sample Collection Diagnostic Platforms

Digital Diagnostic Reporting Platforms - By Fitment Type (In Value%)

Central Reference Laboratories

Regional Processing Laboratories

Collection and Sample Processing Centers

Mobile Diagnostic Testing Units - By End User Segment (In Value%)

Hospitals and Healthcare Providers

Individual Patients and Preventive Health Users

Corporate Health Screening Programs

- Market Share Analysis

- Cross Comparison Parameters (Testing Portfolio Range, Diagnostic Technology Integration, Turnaround Time for Test Results, Laboratory Network Coverage, Digital Reporting Capability, Home Sample Collection Services)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Al Borg Laboratories

NMC Diagnostics

Mediclinic Middle East Labs

Thumbay Laboratories

Aster DM Healthcare Labs

Saudi German Diagnostics UAE

Vivo Diagnostics

Emirates Diagnostic Center

Dr. Sulaiman Al Habib Medical Group Labs

HealthBay Diagnostics

LifeCare Medical Labs

Nova Medical Center Labs

Medcare Laboratories

Al Zahra Hospital Labs

Universal Diagnostic Center

- Hospitals leveraging advanced diagnostic labs for clinical decision support

- Patients increasingly adopting preventive and early disease detection testing

- Corporate organizations implementing employee health screening programs

- Insurance providers integrating diagnostic testing in preventive care programs

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now