Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UAE edge computing market reached approximately USD ~ million based on a recent historical assessment, driven by accelerated 5G standalone deployments, national AI infrastructure investments, and sovereign data localization mandates that require low-latency processing within national borders. Telecom operators and cloud hyperscalers expanded multi-access edge computing nodes across major urban clusters, while oil and gas, transport, and public safety sectors adopted localized analytics systems, as reported by the UAE Telecommunications and Digital Government Regulatory Authority and IDC regional infrastructure trackers.

Abu Dhabi and Dubai dominate the UAE edge computing market due to concentrated hyperscale data center ecosystems, government-backed smart city platforms, and early 5G standalone network rollout enabling distributed compute nodes across dense urban infrastructure. Abu Dhabi’s sovereign cloud and industrial digitalization programs in energy and utilities accelerate edge deployments, while Dubai’s smart mobility, surveillance, and tourism digitalization initiatives create sustained demand for real-time edge analytics infrastructure, according to Smart Dubai and UAE Digital Economy Strategy publications.

By Product Type

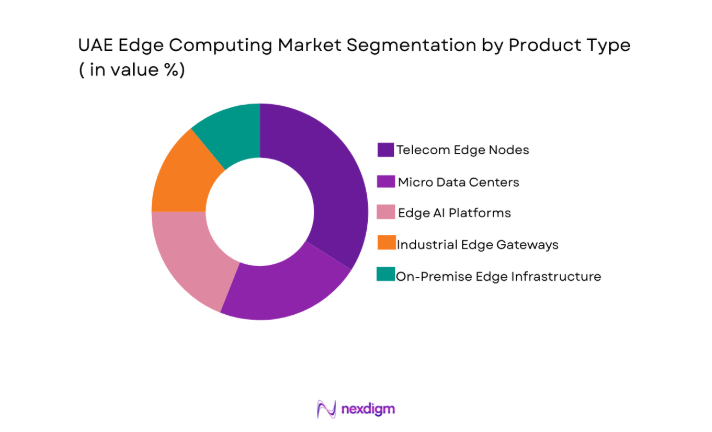

UAE Edge Computing market is segmented by product type into telecom edge nodes, micro data centers, edge AI platforms, industrial edge gateways, and on-premise edge infrastructure. Recently, telecom edge nodes has a dominant market share due to nationwide 5G standalone deployment, telecom operator ownership of network edge sites, and hyperscaler partnerships extending cloud services to radio and aggregation layers. Enterprise and government workloads prefer telecom-hosted edge for secure connectivity, regulatory compliance, and latency assurance, while operators monetize MEC platforms through private networks, IoT, and smart city services.

By Platform Type

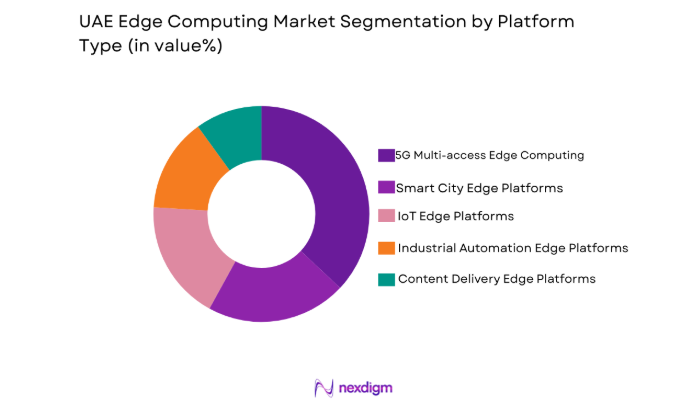

UAE Edge Computing market is segmented by product type into 5G multi-access edge computing platforms, IoT edge platforms, smart city edge platforms, industrial automation edge platforms, and content delivery edge platforms. Recently, 5G multi-access edge computing platforms has a dominant market share due to telecom integration within national 5G networks, enterprise demand for ultra-low latency applications, and hyperscaler cloud extension strategies at telecom edge locations. Government digital services, mobility analytics, and industrial private networks rely on MEC platforms for localized processing and orchestration across distributed infrastructure environments.

Competitive Landscape

The UAE edge computing market shows moderate consolidation, with global infrastructure vendors, telecom equipment providers, and hyperscale cloud firms dominating large-scale deployments through partnerships with national telecom operators and government digital programs. Major players leverage integrated hardware-software stacks, sovereign cloud compliance, and industry-specific edge solutions to secure contracts, while regional system integrators participate in deployment and integration layers.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | UAE Telecom Partnerships |

| Huawei Technologies | 1987 | Shenzhen, China | ~ | ~ | ~ | ~ | ~ |

| Nokia Corporation | 1865 | Espoo, Finland | ~ | ~ | ~ | ~ | ~ |

| Ericsson | 1876 | Stockholm, Sweden | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | Texas, USA | ~ | ~ | ~ | ~ | ~ |

| Hewlett Packard Enterprise | 2015 | Texas, USA | ~ | ~ | ~ | ~ | ~ |

UAE Edge Computing Market Analysis

Growth Drivers

5G Standalone Network Expansion Enabling Distributed Edge Infrastructure

The UAE’s nationwide rollout of 5G standalone architecture provides a foundational distributed network fabric that supports low-latency compute at radio access sites and aggregation nodes, fundamentally accelerating telecom-integrated edge computing adoption across enterprise and public sector applications. Telecom operators deploy MEC nodes within base stations and central offices to deliver localized processing for industrial automation, video analytics, smart mobility, and mission-critical communications workloads that require millisecond latency and high bandwidth reliability across dense urban corridors. Government digital transformation programs mandate real-time analytics across surveillance, transport management, and public safety systems, creating sustained demand for telecom-hosted edge infrastructure embedded within national communication networks. Hyperscale cloud providers partner with UAE telecom firms to extend cloud services to the edge, enabling hybrid architectures where enterprise workloads operate near data sources while integrating with centralized cloud environments for orchestration and storage. Industrial sectors including oil and gas, utilities, and logistics adopt private 5G networks combined with edge nodes to enable autonomous operations, predictive maintenance, and remote asset monitoring across geographically distributed infrastructure. The telecom duopoly market structure accelerates coordinated infrastructure rollout, ensuring nationwide coverage and standardized edge platforms that enterprises can adopt without fragmentation risks. National data sovereignty policies also encourage in-country data processing, making telecom-embedded edge infrastructure a compliant solution for regulated sectors requiring secure local analytics. These combined network, regulatory, and industrial forces position 5G standalone deployment as the primary catalyst transforming edge computing from niche infrastructure to a core national digital platform layer.

Government Smart City and Sovereign AI Infrastructure Investments

The UAE government’s strategic prioritization of AI-driven smart cities and sovereign digital infrastructure programs creates sustained structural demand for edge computing systems that enable localized, secure, and real-time data processing across urban and national services ecosystems. Smart mobility, surveillance analytics, intelligent transport systems, and urban environmental monitoring require distributed compute nodes positioned close to sensors and cameras to process high-volume data streams without latency constraints or bandwidth bottlenecks associated with centralized cloud processing. National AI strategies emphasize sovereign control over sensitive datasets in public safety, healthcare, and government services, reinforcing deployment of localized edge infrastructure within national boundaries to ensure compliance with cybersecurity and data residency frameworks. Government-backed mega-projects in Abu Dhabi and Dubai integrate edge computing within digital twin platforms, autonomous transport networks, and energy optimization systems, creating long-term infrastructure procurement pipelines for edge hardware and platforms. Public sector demand also catalyzes private sector adoption, as industrial firms align with national digital ecosystems and interoperability standards defined by government programs. Sovereign cloud initiatives deploy distributed data centers and micro edge facilities across emirates to support e-government, defense, and critical infrastructure analytics workloads requiring resilient localized processing. Public funding and regulatory support reduce investment risk for telecom operators and vendors expanding edge networks, accelerating nationwide deployment scale. This alignment of policy, urban digitalization, and sovereign AI infrastructure strategy establishes government investment as a structural demand engine sustaining long-term edge computing market growth in the UAE.

Market Challenges

High Capital and Operational Costs of Distributed Edge Infrastructure Deployment

Deploying edge computing infrastructure across geographically distributed sites in telecom networks, industrial facilities, and urban environments requires substantial upfront capital investment in ruggedized hardware, micro data centers, power systems, and connectivity integration, creating financial barriers for widespread adoption beyond large telecom and government projects. Edge nodes must operate reliably in harsh environmental conditions including heat, dust, and remote locations common in energy and infrastructure sectors, necessitating specialized cooling, enclosure, and maintenance solutions that increase equipment and lifecycle costs compared to centralized data centers. Operational complexity also rises significantly as enterprises and operators must manage thousands of distributed compute sites, requiring advanced orchestration platforms, remote monitoring systems, and skilled technical personnel capable of maintaining edge hardware and software stacks across dispersed locations. Power availability and cooling constraints in remote industrial or roadside deployments further increase infrastructure engineering requirements and ongoing operational expenditure. Telecom operators and government agencies absorb these costs at scale, but smaller enterprises face economic challenges justifying localized edge deployment compared to centralized cloud alternatives. Integration with legacy IT and operational technology environments also adds cost through customization and interoperability engineering. Procurement cycles in regulated sectors can extend deployment timelines, increasing total cost of ownership and slowing adoption momentum. These combined capital intensity and operational complexity factors represent a structural constraint limiting edge computing diffusion across smaller enterprises and non-critical applications in the UAE.

Cybersecurity and Interoperability Risks Across Distributed Multi-Vendor Edge Ecosystems

Edge computing environments inherently expand the attack surface of digital infrastructure by distributing compute nodes across numerous physical locations and networks, creating significant cybersecurity management challenges in securing data, applications, and connectivity across heterogeneous deployments involving multiple vendors and platforms. Industrial and government edge workloads often process sensitive operational or public safety data, requiring robust encryption, identity management, and intrusion detection capabilities at each distributed node, which increases system complexity and security management overhead. Multi-vendor architectures combining telecom equipment, IT servers, AI accelerators, and software platforms can introduce interoperability gaps that complicate integration, updates, and lifecycle management across edge environments. Lack of standardized edge orchestration and management frameworks across vendors creates operational silos and potential vulnerabilities where inconsistent patching or configuration occurs. Remote or unattended edge sites are also exposed to physical tampering or environmental disruption risks, necessitating additional security and resilience design. Enterprises adopting edge must integrate cybersecurity monitoring across both IT and operational technology domains, which traditionally operate separately, increasing organizational complexity. Regulatory compliance requirements for data protection and critical infrastructure security further increase implementation and auditing costs. These security and interoperability risks represent a key barrier requiring advanced governance, standards adoption, and integrated platforms to ensure scalable and secure edge deployment across the UAE.

Opportunities

AI-Enabled Industrial and Energy Sector Edge Analytics Platforms

The UAE’s energy, utilities, and industrial sectors operate geographically dispersed assets including oilfields, pipelines, power plants, and logistics infrastructure that generate high-volume sensor and video data streams requiring real-time analysis near source locations, creating a substantial opportunity for specialized edge analytics platforms tailored to industrial operations. Edge-deployed AI inference systems enable predictive maintenance, anomaly detection, autonomous inspection, and safety monitoring without reliance on centralized connectivity, improving operational reliability and reducing downtime across critical infrastructure. National industrial digitalization programs and energy transition initiatives emphasize automation and remote operations, further accelerating demand for ruggedized edge AI hardware and software integrated with industrial control systems. Vendors can develop vertical-specific edge solutions for upstream energy, utilities grid monitoring, and smart manufacturing that combine domain algorithms with localized compute platforms. Integration with private 5G networks enhances deterministic connectivity and latency control, enabling advanced robotics and autonomous operations supported by edge intelligence. Industrial firms prioritize cybersecurity and data sovereignty, favoring localized processing architectures aligned with national regulations. Partnerships between industrial operators, telecom providers, and technology vendors can create ecosystem platforms delivering managed edge analytics services. This convergence of industrial digitalization, AI adoption, and connectivity infrastructure positions industrial edge analytics as a high-value growth segment within the UAE edge computing market.

Smart City Mobility, Surveillance, and Urban Digital Twin Edge Infrastructure

The UAE’s globally recognized smart city initiatives create a major opportunity for edge computing infrastructure supporting real-time urban mobility management, surveillance analytics, environmental monitoring, and digital twin platforms that require distributed processing across city infrastructure layers. Autonomous transport corridors, intelligent traffic systems, and connected public transit generate continuous sensor and video data streams that must be processed locally to enable immediate decision-making and control actions without network latency constraints. Edge computing enables urban digital twins by synchronizing real-world data with simulation platforms in near real time, improving planning, safety, and infrastructure optimization across cities. Surveillance and public safety systems rely on edge AI for facial recognition, incident detection, and crowd analytics while maintaining compliance with data residency policies. Environmental and energy monitoring across buildings and utilities networks also benefits from localized analytics reducing bandwidth and cloud processing costs. Government funding and regulatory frameworks support deployment of distributed compute nodes across urban assets such as street infrastructure, transport hubs, and public facilities. Integration with telecom 5G networks ensures connectivity scalability and resilience. Vendors offering modular, city-integrated edge platforms can capitalize on long-term smart city infrastructure expansion programs across the UAE.

Future Outlook

The UAE edge computing market is expected to expand steadily over the next five years driven by nationwide 5G standalone densification, sovereign AI infrastructure programs, and industrial digitalization initiatives across energy and manufacturing sectors. Government smart city platforms and urban digital twin deployments will accelerate distributed compute demand. Telecom hyperscaler partnerships and private 5G adoption will further expand enterprise edge use cases. Regulatory emphasis on data localization and cybersecurity will continue to favor in-country edge processing architectures.

Major Players

- Huawei Technologies

- Nokia Corporation

- Ericsson

- Dell Technologies

- Hewlett Packard Enterprise

- Cisco Systems

- Amazon Web Services

- Microsoft Corporation

- Google Cloud

- Schneider Electric

- Vertiv Group

- Lenovo Group

- ZTE Corporation

- Intel Corporation

- IBM Corporation

Key Target Audience

- Telecommunications operators

- Oil and gas companies

- Smart city authorities

- Government and regulatory bodies

- Industrial automation firms

- Cloud service providers

- Infrastructure investment funds

- Investments and venture capitalist firms

Research Methodology

Step 1: Identification of Key Variables

Key market variables including telecom edge deployment scale, government digital infrastructure investments, industrial automation adoption, and hyperscaler partnerships were identified through analysis of regulatory publications, telecom infrastructure reports, and enterprise digitalization data sources across the UAE technology ecosystem.

Step 2: Market Analysis and Construction

Market structure and segmentation were constructed using deployment patterns across telecom, industrial, and government sectors, supported by infrastructure vendor data, national digital economy strategies, and regional ICT spending benchmarks to estimate segment distribution and competitive positioning.

Step 3: Hypothesis Validation and Expert Consultation

Findings and assumptions were validated through consultation of telecom technology whitepapers, UAE digital government frameworks, and industry deployment case studies to confirm demand drivers, adoption constraints, and technology trends shaping the edge computing landscape.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into a structured market framework covering segmentation, competitive dynamics, growth drivers, challenges, and opportunities, ensuring alignment with UAE digital infrastructure policies, telecom rollout data, and enterprise adoption patterns across sectors.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of national 5G standalone networks enabling distributed compute nodes

Smart city and digital government initiatives requiring real-time localized processing

Industrial digitalization in energy and manufacturing sectors increasing edge demand

Data sovereignty and latency requirements driving in-country processing adoption

Growth of AI and IoT workloads necessitating near-source analytics infrastructure - Market Challenges

High deployment and operational costs for distributed edge infrastructure

Interoperability gaps across multi-vendor edge ecosystems

Limited skilled workforce for edge and AI infrastructure management

Security vulnerabilities across distributed compute environments

Power and cooling constraints in remote or harsh deployment locations - Market Opportunities

Edge-enabled AI services for smart mobility and autonomous systems ecosystems

Localized data processing solutions for regulated sectors and sovereign workloads

Partnerships between telecom operators and hyperscalers for edge cloud expansion - Trends

Convergence of 5G and edge computing architectures in telecom networks

Adoption of micro modular data centers across urban clusters

Integration of AI inference at the edge for video and sensor analytics

Growth of industry-specific edge platforms for oil and gas and utilities

Shift toward software-defined and virtualized edge infrastructure models - Government Regulations & Defense Policy

National data residency and cybersecurity compliance frameworks

Telecom regulatory support for MEC and distributed infrastructure

Smart city and AI national strategies promoting localized compute adoption - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

On-premise Edge Infrastructure

Micro Data Center Solutions

Edge AI Compute Platforms

Industrial Edge Gateways

Telecom Edge Nodes - By Platform Type (In Value%)

5G Multi-access Edge Computing Platforms

IoT Edge Platforms

Autonomous Systems Edge Platforms

Smart City Edge Platforms

Content Delivery Edge Platforms - By Fitment Type (In Value%)

Standalone Edge Deployments

Integrated Telco Edge Installations

Cloud-connected Edge Systems

Ruggedized Industrial Edge Units

Modular Containerized Edge Facilities - By EndUser Segment (In Value%)

Telecommunications Operators

Government and Smart City Authorities

Oil and Gas and Energy Operators

Manufacturing and Industrial Enterprises

Healthcare and Life Sciences Providers - By Procurement Channel (In Value%)

Direct OEM Procurement

Telecom Operator Partnerships

System Integrator Contracts

Cloud Service Provider Channels

Government Digital Infrastructure Tenders - By Material / Technology (in Value %)

AI Accelerator and GPU-based Edge Systems

ARM-based Low-power Edge Architectures

Ruggedized Industrial Hardware Platforms

Liquid-cooled Edge Infrastructure

Software-defined Edge Virtualization Stacks

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Edge compute performance, Latency optimization capability, AI acceleration integration, Deployment scalability, Industry vertical solutions, Interoperability standards support, Security architecture robustness, Energy efficiency, Service and support ecosystem)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Huawei Technologies

Nokia Corporation

Ericsson

Dell Technologies

Hewlett Packard Enterprise

Cisco Systems

Amazon Web Services

Microsoft Corporation

Google Cloud

Schneider Electric

Vertiv Group

Lenovo Group

ZTE Corporation

Intel Corporation

IBM Corporation

- Telecom operators expanding MEC deployments to monetize 5G enterprise services

- Government agencies adopting sovereign edge infrastructure for secure data processing

- Energy and industrial firms deploying rugged edge systems for remote operations analytics

- Healthcare providers leveraging edge AI for imaging and real-time patient monitoring

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now