Download PDF

Download PDFMarket Overview

The UAE Energy Drink Market is valued at USD ~ million, based on latest country-level market assessment, and the market is expected to grow at 5.71% CAGR across the long-term forecast window. Demand is driven by quick energy needs, sports and fitness participation, expanding retail networks, low-sugar reformulation, premium imported brands and active urban lifestyles. A later benchmark places the market at USD 246.4 million, confirming continued category expansion. The UAE Energy Drink Market is led by Dubai, Abu Dhabi and Sharjah because these emirates combine tourism, airports, nightlife, hypermarkets, petrol stations, gyms, offices, universities and expatriate worker demand. Abu Dhabi’s population reached 4.14 million, while the Abu Dhabi Region alone had 2,823,340 residents and Al Ain had 986,910, supporting petrol-station, office, industrial and modern-retail beverage demand. Dubai dominates premium retail, duty-free, hotel, nightlife and quick-commerce energy drink occasions.

Market Segmentation

By Product Type

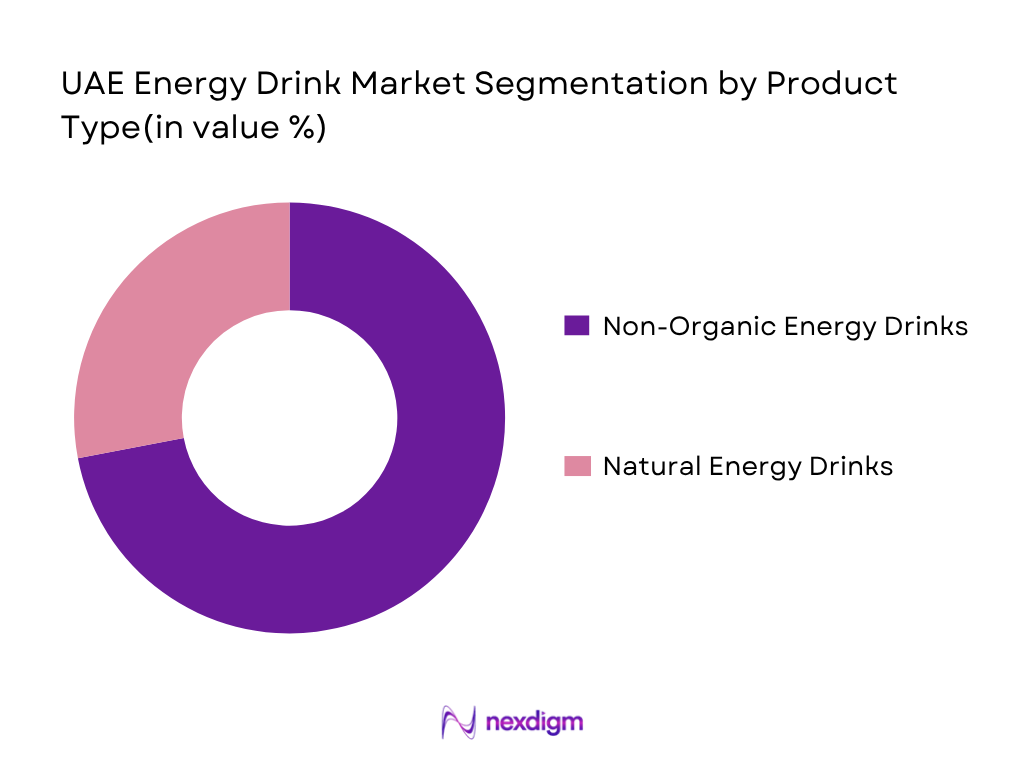

UAE Energy Drink Market is segmented by product type into non-organic energy drinks, natural energy drinks and organic energy drinks. Recently, non-organic energy drinks have a dominant market share in UAE under product type segmentation due to their deep consumer familiarity, extensive imported brand availability, wider flavor variety and stronger visibility across supermarkets, petrol stations, convenience stores, duty-free outlets, hotels and nightlife venues. Brands such as Red Bull, Monster, Rockstar, Power Horse, Hell, Carabao and Boom Boom have created strong recall around quick energy, alertness, driving, work productivity and late-night consumption. Natural and organic energy drinks are expanding in premium urban channels because of health-conscious consumers, but they remain smaller due to higher price positioning, limited mainstream shelf space and narrower product availability.

By Distribution Channel

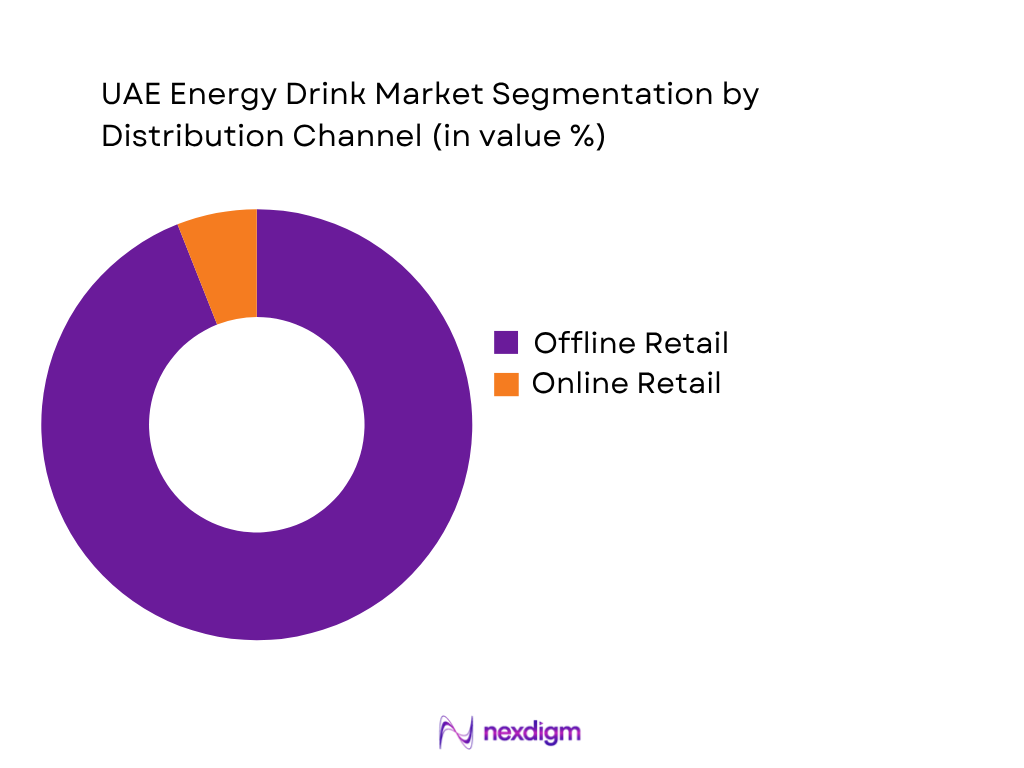

UAE Energy Drink Market is segmented by distribution channel into offline retail and online retail. Recently, offline retail has a dominant market share in UAE under distribution channel segmentation because energy drinks are highly impulse-led and frequently consumed chilled immediately after purchase. Hypermarkets, supermarkets, convenience stores, baqalas, petrol stations, duty-free outlets, hotels, gyms, beach venues, bars and clubs remain the strongest selling points. Offline retail also benefits from high visual merchandising, cold-shelf placement, checkout visibility, multipack promotions and tourist footfall. Petrol stations operated by ADNOC, ENOC, EPPCO and Emarat are especially important for drivers, commuters and delivery riders. Online retail is expanding through Amazon, Noon, Talabat, Careem and InstaShop, but chilled availability and immediate consumption still keep offline channels dominant.

Competitive Landscape

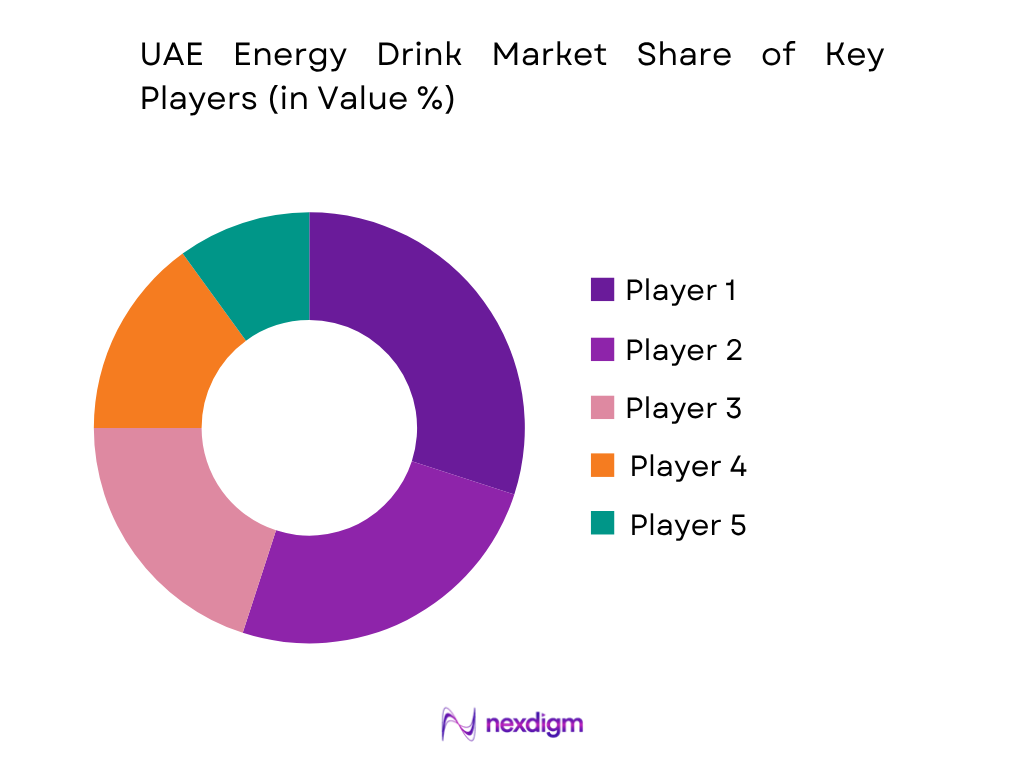

The UAE Energy Drink Market is led by global premium brands, GCC-recognized energy brands, European value-premium brands and UAE-based beverage distributors. Red Bull and Monster maintain strong visibility through premium positioning, sports sponsorships, convenience-store presence and HoReCa relevance. Power Horse, Hell, Carabao and Boom Boom compete through broader affordability, imported-style cans and supermarket availability. The market is moderately fragmented because imported SKUs, local distributors, e-commerce sellers and fitness-linked products continue to enter the category, while the 100% excise tax limits aggressive volume growth and pushes brands toward premiumization, zero-sugar variants and stronger retail execution.

| Company | Establishment Year | Headquarters | Core Energy Portfolio | UAE Positioning | Packaging Focus | Distribution Strength | Product Innovation Focus | Market-Specific Edge |

| Red Bull GmbH | 1984 | Fuschl am See, Austria | ~ | ~ | ~ | ~ | ~ | ~ |

| Monster Beverage Corporation | 1935 | Corona, California, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| PepsiCo | 1965 | Purchase, New York, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Power Horse Energy Drinks | 1994 | Linz, Austria | ~ | ~ | ~ | ~ | ~ | ~ |

| HELL Energy | 2006 | Szikszó, Hungary | ~ | ~ | ~ | ~ | ~ | ~ |

UAE Energy Drink Market Analysis

Growth Drivers

Tourism, Airports and Hotel-Led Energy Drink Consumption

UAE Energy Drink Market is supported by tourism-led beverage occasions across airports, hotels, malls, beaches, events, nightlife and duty-free retail. The UAE Ministry of Economy reported 15.3 million hotel guests across the seven emirates in the first half of 2024, with hotel rooms reaching 213,741 and hotel nights exceeding 53 million. UAE airports handled 71.75 million passengers in the same period, while airport capacity was estimated at more than 160 million passengers. These travel and hospitality flows directly support chilled cans, multipacks, premium imports, hotel minibar sales, airport retail and late-night energy drink demand.

High-Income Urban Economy and Premium Functional Beverage Demand

UAE Energy Drink Market benefits from a high-income, urban and retail-dense economy where consumers can access premium cans, zero-sugar variants, imported flavours and functional beverage formats. The World Bank reported UAE GDP at USD 552.32 billion and GDP per capita at USD 50,273.5 in 2024, supporting strong purchasing capacity for branded FMCG products. Dubai’s population reached 4,248,200 residents at the end of 2024, while active individuals during peak hours reached 5,937,800, reflecting heavy daily movement across workplaces, malls, hotels, retail zones and transit corridors. This supports impulse energy drink consumption through supermarkets, baqalas, forecourts and quick-commerce platforms.

Market Challenges

Excise-Tax Exposure and Reformulation Pressure

UAE Energy Drink Market faces a structural challenge from excise taxation and sugar-linked policy changes. The Federal Tax Authority clarified that energy drinks will continue to be subject to the existing 100% excise tax on the excise price and will not shift into the new tiered volumetric model for sweetened drinks. The same clarification defines high-sugar drinks as those containing 8 g or more of total sugar per 100 ml, moderate-sugar drinks as 5 g to less than 8 g, and low-sugar drinks as less than 5 g. This directly raises compliance pressure for importers, distributors and full-sugar energy drink brands.

Import, Labelling and Multi-Channel Compliance Complexity

UAE Energy Drink Market is highly exposed to imported SKUs, Arabic labelling, product registration, excise compliance and multi-emirate retail execution. The World Bank reported UAE GDP at USD 552.32 billion, showing the scale of the country’s formal trading economy, while Dubai alone recorded 4,248,200 usual residents and 5,937,800 active individuals during peak hours at the end of 2024. Large daily movement increases opportunity but also makes execution more complex across baqalas, hypermarkets, petrol stations, duty-free outlets, hotels, gyms and delivery platforms. Energy drink brands must maintain compliant labels, correct tax declarations, chilled availability and consistent distributor service across fragmented retail touchpoints.

Market Opportunities

Zero-Sugar and Low-Sugar Energy Drink Expansion

UAE Energy Drink Market has future growth opportunity in zero-sugar, low-sugar and reduced-calorie energy drinks because tax and health policies are making sugar content commercially important. The Federal Tax Authority states that drinks containing only artificial sweeteners are subject to 0% excise tax under the new sweetened-drink tiered volumetric model, while high-sugar beverages are classified at 8 g or more of total sugar per 100 ml. Although energy drinks remain under the existing energy-drink excise category, these official thresholds influence retailer, importer and consumer attention toward sugar content. Brands can use current policy signals to expand zero-sugar cans, fitness-positioned SKUs and premium functional variants.

Dubai-Centric Forecourt, Quick-Commerce and Daytime Mobility Demand

UAE Energy Drink Market has future growth opportunity in Dubai’s commuter, delivery, office and visitor economy because energy drinks are consumed during driving, long workdays, shift work, gym routines and late-night activities. Dubai recorded 4,248,200 usual residents, plus 1,689,600 workers residing outside Dubai and temporary residents during peak hours, taking active individuals to 5,937,800 at the end of 2024. Dubai Statistics also identified 205,079 residents in Jabal Ali Industrial First and 160,831 in Muhaisanah Second, both relevant to worker-focused beverage demand. These current mobility clusters support petrol-station chillers, baqalas, workplace vending, delivery apps and value-to-premium pack segmentation.

Future Outlook

The UAE Energy Drink Market is expected to grow steadily, supported by tourism, modern retail, premium imported beverages, active lifestyles, sports participation, quick-commerce and the continued shift toward low-sugar and zero-sugar energy drinks. The long-term forecast benchmark indicates 5.71% CAGR, with the market expected to reach USD 412.5 million by the end of the available forecast horizon.

Over the next several years, the UAE market will remain heavily shaped by Dubai and Abu Dhabi. Dubai will continue to support premium cans, duty-free sales, nightlife mixers, hotel consumption, delivery-platform visibility and tourist-led impulse demand. Abu Dhabi will support demand through offices, government-sector employment, industrial zones, petrol stations, fitness venues and major sports events. Sharjah, Ajman and the Northern Emirates will remain more value-led, with baqalas, supermarkets and commuter retail supporting broader availability.

The strongest growth spaces are zero-sugar energy drinks, reduced-sugar variants, natural-caffeine products, sports energy drinks, amino-acid and electrolyte-fortified formulations, and imported flavor extensions. Excise taxation will remain a restraint, particularly for full-sugar products, but it also creates opportunity for premium positioning and better-for-you reformulation. E-commerce and quick-commerce will increase trial for multipacks, limited editions and international SKUs, while petrol stations and convenience stores will remain central to immediate chilled consumption.

Major Players

- Red Bull UAE

- Monster Energy UAE

- PepsiCo UAE

- The Coca-Cola Company UAE

- Power Horse Energy Drinks

- HELL Energy UAE

- Carabao Energy Drink UAE

- Star Drinks UAE

- BCS Globals

- Boom Boom Energy Drink

- Eurostar Beverages

- Aujan Group Holding

- Masafi

- Prime Hydration UAE

- G Fuel UAE

Key Target Audience

- Energy drink manufacturers and brand owners

- Functional beverage companies

- Carbonated soft drink and packaged beverage companies

- Hypermarket, supermarket and convenience retail chains

- Petrol station, duty-free and travel retail operators

- HoReCa, gym and sports nutrition channel operators

- Investments and venture capitalist firms

- Government and regulatory bodies (Federal Tax Authority, Ministry of Industry and Advanced Technology, Ministry of Health and Prevention, Dubai Municipality, Abu Dhabi Agriculture and Food Safety Authority, UAE Competition Regulation Committee)

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map for the UAE Energy Drink Market, covering brand owners, importers, distributors, hypermarkets, supermarkets, petrol stations, baqalas, duty-free operators, HoReCa outlets, gyms, e-commerce platforms and regulators. The objective is to identify variables such as pack type, sugar profile, caffeine positioning, excise exposure, retail channel, consumer occasion and emirate-level demand.

Step 2: Market Analysis and Construction

In this phase, historical data for the UAE Energy Drink Market is compiled through country-level market benchmarks, company portfolios, SKU listings, retail shelf checks, e-commerce availability and channel mapping. The assessment reviews how cans, multipacks, zero-sugar products, imported SKUs, convenience stores, petrol stations and hospitality outlets contribute to category revenue and product visibility.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through computer-assisted telephone interviews with beverage distributors, supermarket buyers, petrol-station retail managers, hotel and nightlife suppliers, gym retailers, e-commerce sellers and importers. These consultations provide insights into SKU velocity, chilled shelf placement, brand switching, excise-tax impact, flavor demand, promotional activity and channel-specific acceptance.

Step 4: Research Synthesis and Final Output

The final phase triangulates top-down market benchmarks with bottom-up brand, SKU, pack and channel evidence. Direct engagement with beverage manufacturers, distributors and retail stakeholders helps verify product segmentation, competitive positioning, emirate-wise demand, retail execution, regulatory exposure and future opportunity areas in the UAE Energy Drink Market.

- Executive Summary

- Research Methodology [market definitions and assumptions, RTD energy drink classification, stimulant beverage scope, GCC energy drink standards mapping, UAE excise-tax adjustment, top-down sizing, bottom-up sizing, retail audit checks, distributor interviews, SKU-level price-pack benchmarking]

- Definition and Scope

- Overview Genesis

- Timeline of Major Players

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers (tourism, expatriate base, fitness culture, petrol-station retail, nightlife, high disposable income, modern grocery, delivery economy)

- Market Challenges (excise tax, sugar scrutiny, caffeine limits, imported SKU dependency, shelf competition, regulatory labelling)

- Market Opportunities (zero sugar, natural caffeine, date-based energy, sports energy, duty-free, tourism, forecourt, quick commerce)

- Market Trends (zero sugar, premium cans, natural caffeine, imported flavors, gaming energy, fitness energy, multipacks, sugar-tax response)

- SWOT Analysis

- Porter’s Five Forces

- By Value (2020-2025)

- By Volume (2020-2025)

- By Unit Sales (2020-2025)

- By Product Type (In Value %)

Carbonated RTD Energy Drinks

Non-Carbonated Energy Drinks

Sugar-Free Energy Drinks

Sports Energy Drinks - By Packaging Type (In Value %)

Aluminum Cans

PET Bottles

Glass Bottles

Multipacks

Slim Cans

Large Cans - By Distribution Channel (In Value %)

Hypermarkets and Supermarkets

Convenience Stores and Forecourt Retail

Petrol Stations

Traditional Groceries and Baqalas

Duty-Free and Travel Retail - By Emirate (In Value %)

Dubai

Abu Dhabi

Sharjah

Ajman

Ras Al Khaimah

- Market Share of Major Players on the Basis of Value and Volume

- Cross Comparison Parameters (caffeine mg per litre, sugar grams per 100 ml, zero-sugar SKU mix, excise-tax exposure, Arabic-label compliance, hypermarket and forecourt distribution depth, HoReCa and duty-free presence, sports and nightlife activation intensity)

- SWOT Analysis of Major Players [brand equity, importer strength, channel access, reformulation capability, price exposure, regulatory compliance]

- Detailed Profiles of Major Companies

Red Bull UAE

Monster Energy UAE

PepsiCo UAE

The Coca-Cola Company UAE

Power Horse Energy Drinks

HELL Energy UAE

Carabao Energy Drink UAE

Star Drinks UAE

BCS Globals

Boom Boom Energy Drink

Eurostar Beverages

Aujan Group Holding

Masafi

Prime Hydration UAE

G Fuel UAE

- Market Demand and Utilization

- Purchasing Power and Budget Allocation

- Regulatory and Compliance Requirements

- Needs, Desires and Pain Point Analysis

- Decision-Making Process

- By Value (2026-2035)

- By Volume (2026-2035)

- By Unit Sales (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now