Download PDF

Download PDFMarket Overview

The UAE Food Acidulants Market was valued at approximately USD ~ million in 2024 and is projected to grow at a CAGR of approximately 7.0% through 2031, consistent with the LAMEA food acidulants growth trajectory identified across regional market research. The UAE represents one of the most dynamic food acidulant markets in the Middle East and Africa region, underpinned by a food and beverage manufacturing sector that hosts over 2,000 food and beverage companies generating USD 7.63 billion in annual revenue, according to the USDA Foreign Agricultural Service. The global food acidulants market was valued at USD 6.39 billion in 2023 and is expected to grow at a CAGR of 6.3% through 2032, with the global market projected to reach USD 8.6 billion by 2031, reflecting the strong underlying demand environment for pH control, flavor enhancement, and preservation ingredients across the food and beverage industry. The UAE’s food acidulants market is shaped by the country’s strategic role as a GCC food trade and re-export hub, with Jebel Ali Port facilitating efficient movement of food ingredients across the broader Middle East, North Africa, and South Asian markets. Market demand is further driven by excise tax-induced beverage reformulation, expanding HoReCa infrastructure catering to over 17 million annual tourists, rising halal food manufacturing activity, and growing consumer preference for natural and clean-label food ingredient systems aligned with the UAE’s National Food Security Strategy 2051.

Market Segmentation

By Acidulant Type

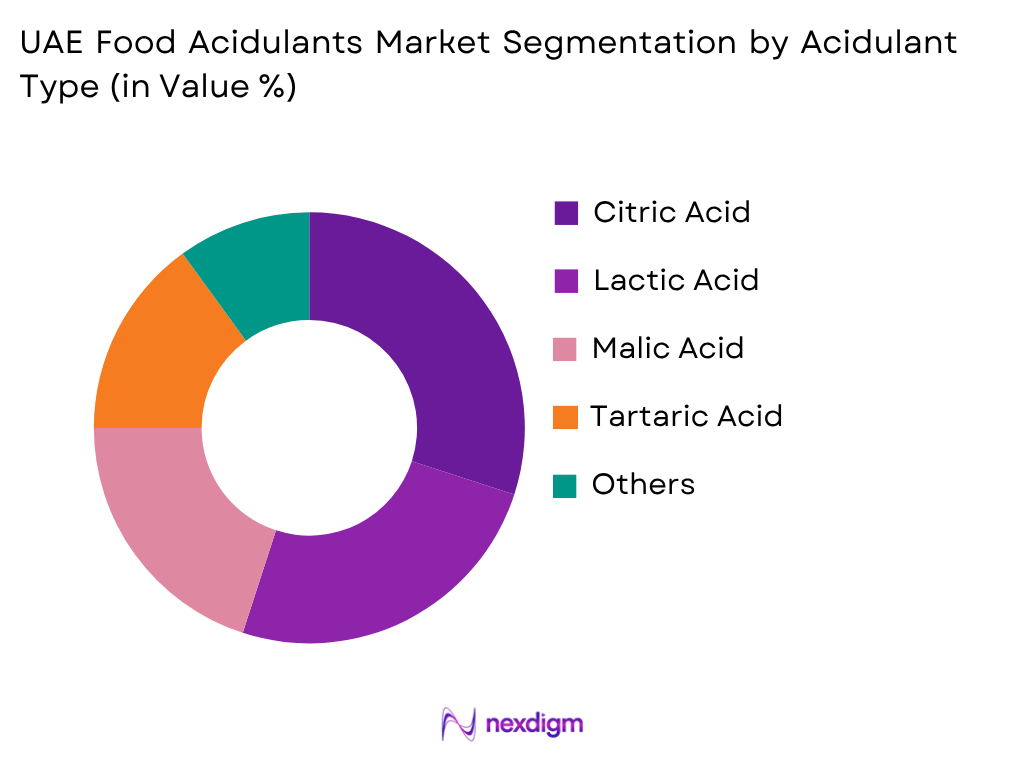

Citric acid dominates the UAE food acidulants market, consistent with its global leadership position where it accounts for approximately 60% of carbohydrate-based food additive volume, owing to its multifunctional capabilities as a pH buffer, flavor enhancer, natural preservative, chelating agent, and emulsification support ingredient across the widest range of food and beverage applications. The global citric acid market was valued at USD 3.7 billion in 2024, growing at a CAGR of 4.30% through 2031, with food and beverage applications accounting for 65.4% of total volume. In the UAE, citric acid is extensively utilized across carbonated and flavored beverages, fruit juices, functional drinks, bakery products, confectionery, dairy items, and sauces, making it the single most important acidulant ingredient for the country’s food and beverage manufacturing sector. The UAE’s excise tax framework, which applies a 50% levy on carbonated drinks and a 100% levy on energy drinks, has accelerated the reformulation of beverage products toward natural citric acid and malic acid-based acidulant systems that enable reduced-sugar and clean-label beverage positioning. Lactic acid represents the fastest-growing acidulant segment in the UAE, driven by rising demand from dairy processors, plant-based food manufacturers, and meat processing companies that utilize its antimicrobial and pH control properties to extend shelf life and improve food safety in temperature-sensitive product categories. Malic acid and tartaric acid are gaining traction in premium beverage, confectionery, and functional food applications where their distinctive flavor profiles offer formulation differentiation advantages.

By Application

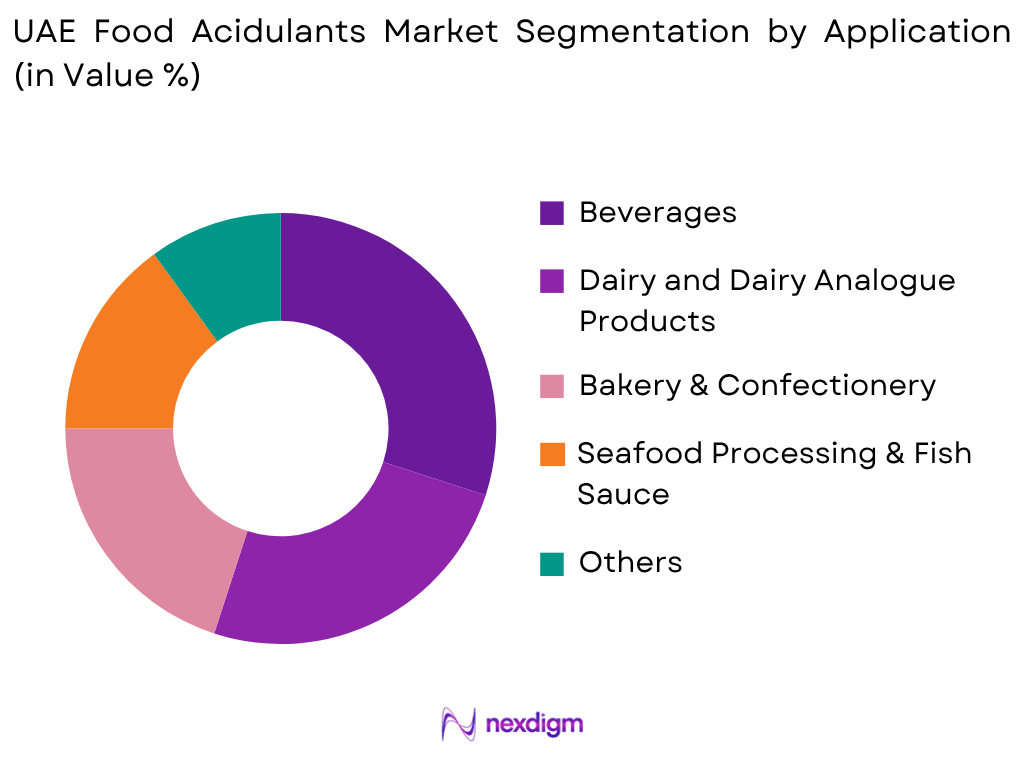

The beverages segment accounts for the largest share of food acidulant demand in the UAE, reflecting the country’s high per-capita consumption of carbonated soft drinks, energy drinks, flavored waters, fruit juices, and functional beverages across its diverse expatriate and tourist population. According to market research, beverages accounted for approximately 50.1% of global food acidulants market share in 2023, and this dominance is replicated in the UAE where the large HoReCa sector, high tourism footfall, and the warm climate collectively drive substantial demand for acidulated beverage products throughout the year. The UAE’s excise tax on carbonated and energy drinks has simultaneously created pressure for manufacturers to reformulate beverages with reduced sugar content while maintaining the acidic flavor profile that consumers associate with carbonated drinks, driving demand for citric acid, malic acid, and tartaric acid as reformulation tools. The bakery and confectionery segment represents the second-largest application area, consistent with the global market where bakery and confectionery accounted for approximately 26% of food acidulant revenue in 2023. UAE bakery manufacturers utilize citric acid and lactic acid extensively for dough conditioning, pH control, mold inhibition, and flavor enhancement in bread, pastries, biscuits, and confectionery products. The dairy segment also contributes significantly to acidulant demand, driven by the UAE’s growing yogurt, flavored milk, processed cheese, and dairy beverage manufacturing base. The processed meat and ready meal segments are expanding as domestic food manufacturers increase production of halal-certified processed meat products and convenience meal solutions for the UAE’s large and diverse urban consumer population.

Competitive Landscape

The UAE Food Acidulants Market is served by a combination of global specialty chemical and ingredient companies operating through regional distribution networks, free zone trading operations, and direct commercial relationships with major food manufacturers in Dubai, Abu Dhabi, and Sharjah. Leading international acidulant producers including Jungbunzlauer, Cargill, Tate & Lyle, Corbion, and ADM supply citric acid, lactic acid, malic acid, and other organic acids to the UAE market through established distribution agreements with regional ingredient trading houses and specialty food ingredient distributors. The UAE’s Jebel Ali Free Zone provides strategic advantages for ingredient importers, enabling duty-free storage, trans-shipment logistics, and efficient re-export operations across the GCC and broader MENA region. Competition centers on supply chain reliability, pricing competitiveness relative to Chinese fermentation-based citric acid producers, halal certification documentation, technical application support for food manufacturers, and the breadth of natural and clean-label acidulant product portfolios.

| Company | Establishment Year | Headquarters | Primary Acidulant Portfolio | Key Application Industries

|

Manufacturing Presence | R&D Capability | Distribution Network | Clean Label Solutions |

| Jungbunzlauer Suisse AG | 1867 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Tate & Lyle PLC | 1859 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Cargill Incorporated | 1865 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Archer Daniels Midland (ADM) | 1902 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Corbion N.V. | 1919 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

UAE Food Acidulants Market Analysis

Growth Drivers

Expanding Food & Beverage Processing Sector and UAE National Food Security Strategy 2051

The UAE’s food and beverage processing sector represents the most fundamental structural growth driver for the food acidulants market. The UAE hosts over 2,000 food and beverage companies generating USD 7.63 billion in annual revenue, according to the USDA Foreign Agricultural Service, with 568 predominantly small and medium-sized food and beverage processors concentrated primarily across Dubai’s 315 food factories, and the remainder distributed across Abu Dhabi, Sharjah, Ras Al Khaimah, and other emirates. The UAE packaged food market reached USD 7.6 billion in 2024 and is forecast to reach USD 10.4 billion by 2029, reflecting accelerating growth in packaged and processed food demand that directly underpins acidulant ingredient procurement. The UAE’s National Food Security Strategy 2051 has established an ambitious goal to achieve global leadership on the Food Security Index by 2051 through investments in domestic food production, food technology innovation, and supply chain resilience, including the development of the Food Tech Valley initiative to triple domestic food production by 2030. According to the IMF, the UAE GDP per capita reached USD 49,377.6 in 2024 and GDP growth was projected at 4.0% for the year, providing a strong macroeconomic environment for continued food industry investment and consumer spending. The UAE’s strategic location as the world’s second-largest food commodity trading hub, combined with world-class port infrastructure at Jebel Ali, provides unmatched ingredient import logistics efficiency that enables food manufacturers to maintain reliable access to internationally sourced acidulant ingredients including citric acid, lactic acid, and malic acid throughout the year.

Tourism-Driven HoReCa Expansion and Excise Tax-Induced Beverage Reformulation

The UAE’s position as one of the world’s most prominent tourism destinations generates substantial and continuously growing demand for food and beverage products that require acidulant ingredients for flavor, preservation, and pH management. The UAE foodservice market was valued at USD 8.5 billion in 2024 and is projected to reach USD 14.2 billion by 2032 at a CAGR of 6.25%, driven by an influx of more than 17 million annual international visitors and a domestic population with high per-capita spending on food and dining. Dubai’s achievement of three Michelin Green stars in 2024 reflects the sophistication of the UAE’s culinary sector, while the broader expansion of quick-service restaurant chains, cloud kitchens, and institutional catering operations creates sustained demand for acidulant ingredients across beverages, sauces, condiments, and prepared food categories supplied to hospitality operators. The UAE’s excise tax framework, imposing a 50% tax on carbonated beverages and a 100% tax on energy drinks, has created a structural reformulation incentive for beverage manufacturers to develop natural, lower-sugar, and clean-label beverage alternatives that maintain the desired tartness and flavor profiles through the precise use of citric acid, malic acid, and tartaric acid acidulant systems. Consumer foodservice through leisure grew 17% to USD 762 million in 2023, and consumer foodservice through standalone outlets grew 10% to USD 4 billion, reflecting the sustained growth of the out-of-home consumption market that supplies a significant share of acidulant ingredient demand across the UAE’s food processing supply chain.

Market Challenges

Near-Total Import Dependency and Citric Acid Price Volatility

The UAE food acidulants market faces a fundamental structural challenge in its near-total dependence on imported acidulant ingredients, given the country’s negligible domestic production capacity for fermentation-based organic acids including citric acid, lactic acid, and malic acid. According to USDA FAS, approximately 80 to 90% of the UAE’s food and agricultural products are imported, and this dependency extends fully to specialty food ingredients including acidulants. Citric acid, the dominant acidulant consumed in the UAE, is primarily produced through large-scale fermentation operations in China and Eastern Europe, exposing UAE importers and food manufacturers to global fermentation input cost volatility, shipping cost fluctuations, and supply chain disruptions that can affect availability and pricing of this critical ingredient. China’s dominance in global citric acid production creates both cost advantages for buyers and concentration risk, as any disruption to Chinese fermentation output, export regulations, or logistics can rapidly affect citric acid pricing and availability across the GCC market. The global food acidulants market’s susceptibility to raw material input cost volatility, driven by fluctuations in agricultural commodity prices for corn, molasses, and other fermentation substrates used in organic acid production, creates price risk for UAE food manufacturers that cannot easily substitute acidulant types without reformulation investment. Ensuring a reliable supply of halal-certified acidulant documentation from international suppliers represents an additional procurement requirement that can extend sourcing timelines and add complexity to ingredient qualification processes for UAE manufacturers serving the halal food sector.

ESMA and Regulatory Compliance Costs and Counterfeit Ingredient Risks

Food manufacturers and ingredient suppliers operating in the UAE must navigate a comprehensive regulatory framework administered by the Emirates Authority for Standardization and Metrology (ESMA), the Dubai Municipality Food Control Department, and the Abu Dhabi Agriculture and Food Safety Authority (ADAFSA), each of which enforces specific food additive permitted lists, import documentation requirements, and food safety compliance standards that apply to acidulant ingredients. All food imports into the UAE must comply with the GSO 9:2013 labeling standard, which mandates specific labeling disclosures for food additives including acidulants, and food manufacturers must maintain comprehensive documentation demonstrating that acidulant ingredients meet UAE food additive permitted concentrations across each specific food product category in which they are used. The presence of counterfeit or substandard food ingredients in regional trading markets presents a quality risk for food manufacturers that source acidulants through informal trading channels rather than established certified ingredient suppliers, potentially creating food safety compliance risks and product recall exposure. Compliance costs associated with ESMA ingredient approvals, halal certification renewals, import documentation management, and Dubai Municipality food factory licensing collectively represent a recurring operational cost burden for food manufacturers seeking to maintain compliant acidulant procurement practices in the UAE’s strictly regulated food industry environment.

Market Opportunities

Natural and Clean-Label Acidulant Growth and GCC Re-Export Hub Development

The accelerating global shift toward natural, organic, and clean-label food ingredients is creating significant commercial opportunities for suppliers of naturally derived acidulants in the UAE market. Health-conscious consumers in the UAE, particularly among the growing Western and health-focused expatriate community, are increasingly checking food labels and preferring products with recognizable, natural ingredient lists, driving demand for naturally derived citric acid from citrus fermentation, malic acid from apple and other fruit sources, and lactic acid from fermentation processes that can be positioned as natural and clean-label alternatives to synthetic acid regulators. The clean-label trend is reinforcing demand for naturally sourced acidulants in premium packaged food categories including flavored yogurts, premium beverages, artisanal bakery products, and gourmet sauces and dressings sold through the UAE’s extensive modern retail and specialty food retail channels. The UAE’s strategic position as the GCC’s primary food trade and re-export hub, leveraging Jebel Ali’s world-class port and free zone infrastructure, creates a complementary commercial opportunity for acidulant importers and distributors to develop UAE-based ingredient warehousing and distribution operations that supply not only the domestic market but also the broader GCC region including Saudi Arabia, Kuwait, Bahrain, Qatar, and Oman. The UAE Food Tech Valley initiative and sustained government investment in food processing infrastructure across free zones including KIZAD in Abu Dhabi and Dubai Industrial City are expected to attract new food manufacturing facilities that will generate additional acidulant ingredient demand and expand the addressable market for specialty ingredient suppliers.

Lactic Acid Expansion in Dairy, Plant-Based, and Meat Applications

Lactic acid represents one of the highest-growth opportunity segments within the UAE food acidulants market, driven by its expanding applications across dairy, plant-based food, and processed meat categories that are each experiencing strong demand growth from the UAE’s diverse and health-conscious consumer population. In dairy applications, lactic acid is increasingly used as a natural acidulant and pH control agent in yogurt, fermented dairy beverages, and fresh cheese manufacturing, where its antimicrobial properties simultaneously improve product safety and extend shelf life without relying on synthetic preservatives. The UAE’s dairy sector is supported by growing domestic consumer demand for natural and functional dairy products that align with health-conscious purchasing patterns increasingly prevalent among both Emirati and expatriate consumer segments. In processed meat applications, lactic acid’s key functional properties including antimicrobial action, pathogenic bacteria control, flavor protection, improved water binding capacity, and sodium reduction support are becoming increasingly relevant to UAE halal meat processors seeking to improve product quality and safety while meeting evolving consumer preferences for cleaner and more nutritious processed meat products. The rapid growth of plant-based and alternative protein food products in the UAE, reflecting global food technology trends and the city-state’s progressive attitude toward novel food categories, is also creating new demand for lactic acid as a natural acidulant in plant-based meat products, dairy alternative beverages, and fermented plant-based food applications. The global processed meat market is expected to surpass USD 3.6 trillion by 2032, providing a strong commercial backdrop for continued lactic acid demand growth across both conventional and plant-based protein food manufacturing in the UAE.

Future Outlook

The UAE Food Acidulants Market is expected to maintain strong growth through the 2035 forecast period, supported by continued expansion of the food and beverage processing sector, sustained tourism-driven HoReCa demand, and the progressive adoption of natural and clean-label acidulant systems aligned with evolving consumer health preferences. Excise tax-driven beverage reformulation will continue to incentivize citric acid, malic acid, and tartaric acid adoption as manufacturers develop lower-sugar, naturally acidified beverage alternatives. Lactic acid demand is expected to accelerate across dairy, plant-based, and halal meat processing applications, while the UAE’s role as a GCC ingredient re-export hub will generate additional distribution and warehousing investment in Jebel Ali and free zone-based acidulant supply chain infrastructure. Continued government investment under the National Food Security Strategy 2051 and the Food Tech Valley initiative will progressively expand domestic food manufacturing capacity and reinforce long-term acidulant ingredient demand across the Kingdom’s growing processed food and beverage industry.

Major Players

- Jungbunzlauer Suisse AG

- Cargill Incorporated

- Tate & Lyle PLC

- Corbion N.V.

- Archer Daniels Midland Company (ADM)

- Bartek Ingredients Inc.

- Brenntag SE

- Univar Solutions (Univar Food Ingredients)

- IMCD Group

- Hawkins Watts Limited

- Sigma-Aldrich (Merck KGaA)

- Weifang Ensign Industry Co. Ltd.

- TTCA Co. Ltd.

- Gadot Biochemical Industries

- Prinova Group LLC

Key Target Audience

- Food & Beverage Manufacturers and Ingredient Procurement Teams

- Beverage Producers and Bottlers

- Bakery, Dairy, and Processed Food Producers

- Specialty Food Ingredient Distributors and Trading Companies

- Foodservice Operators, HoReCa Chains, and Catering Companies

- Free Zone-Based Ingredient Import and Re-Export Companies

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies (Emirates Authority for Standardization and Metrology (ESMA), Dubai Municipality Food Control Department, Abu Dhabi Agriculture and Food Safety Authority (ADAFSA), Ministry of Climate Change and Environment, GCC Standardization Organization (GSO))

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying the major stakeholders across the UAE food acidulants value chain, including international acidulant manufacturers, regional distributors and ingredient trading companies, food and beverage processing companies, regulatory agencies, and end-user sectors across beverages, bakery, dairy, meat, and convenience foods. Extensive secondary research is conducted using ESMA regulatory publications, USDA Foreign Agricultural Service UAE Food Processing Ingredients reports, Dubai Municipality guidelines, company annual reports, GCC trade statistics, and proprietary ingredient market databases to establish the key variables influencing market demand, pricing, and competitive dynamics.

Step 2: Market Analysis and Construction

Historical market information is compiled and analyzed to estimate the overall food acidulants market size by type, function, form, application, and end user. Ingredient import statistics, food processing sector revenue data, excise tax impact analysis on beverage reformulation, HoReCa sector growth metrics, and consumer health trend research are integrated using both bottom-up and top-down market sizing approaches to ensure comprehensive coverage of all demand-generating segments within the UAE market.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market estimates are validated through Computer Assisted Telephone Interviews (CATIs) and structured discussions with ingredient procurement managers, food technologists, regulatory affairs specialists, distributor executives, and food industry associations operating within the UAE and across the GCC. These consultations provide critical commercial insights into acidulant adoption trends, halal certification requirements, ESMA compliance dynamics, pricing benchmarks, and the competitive dynamics among international and regional ingredient suppliers serving the UAE food manufacturing ecosystem.

Step 4: Research Synthesis and Final Output

The final stage integrates primary research findings with secondary data to develop a comprehensive market assessment covering market size, segmentation, regulatory landscape, competitive positioning, end-user demand analysis, and future growth opportunities. Multiple validation techniques including data triangulation and cross-verification against ESMA, USDA FAS, Dubai Municipality, and GCC trade statistics are employed to ensure the accuracy and credibility of the final market report.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Taxonomy, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Primary Industry Interviews, Secondary Research Validation, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Industry Value Chain Analysis

- Supply Chain Analysis

- Growth Drivers (Expanding Food & Beverage Processing Sector, Rising Packaged Food and Beverage Consumption, Growing HoReCa and Tourism-Driven Food Demand, UAE National Food Security Strategy 2051, Clean-Label and Natural Acidulant Demand, Excise Tax-Driven Beverage Reformulation, Halal Food Manufacturing Growth, Rising Demand for Convenience and Ready-to-Eat Foods)

- Market Challenges (Near-Total Import Dependency for Acidulant Raw Materials and Finished Ingredients, Price Volatility of Citric Acid and Fermentation-Based Inputs, Currency and Trade Flow Risks, ESMA and Dubai Municipality Regulatory Compliance Costs, Counterfeit and Substandard Ingredient Risks, Competition from GCC Re-Export Markets)

- Market Opportunities (Natural and Organic Acidulant Growth, Lactic Acid Expansion in Dairy and Meat Applications, Beverage Sector Reformulation Driven by Excise Tax, GCC Re-Export Hub Opportunity, Functional Food Acidulant Innovation, Clean-Label Citric Acid and Malic Acid Premiumization, Free Zone Ingredient Distribution Hub Development, Jebel Ali Port-Enabled Supply Chain Efficiency)

- Market Trends (Natural Fermentation-Derived Acidulants, Clean-Label Acidulant Sourcing, Citric Acid Demand in Energy and Functional Beverages, Lactic Acid Use in Plant-Based and Dairy Products, Malic Acid in Low-Calorie and Sports Beverages, Organic Acid Innovation, Digital B2B Ingredient Procurement, Sustainable Acidulant Sourcing Programs)

- Government Regulations & Policy Framework (Emirates Authority for Standardization and Metrology (ESMA) Food Additive Standards, Dubai Municipality Food Safety Standards, Abu Dhabi Agriculture and Food Safety Authority (ADAFSA) Regulations, UAE Food Safety Law Federal Decree No. 10 of 2015, GCC Standardization Organization (GSO) Food Additive Standards, Halal Certification Requirements, Excise Tax on Carbonated and Energy Drinks, Import Licensing and Customs Procedures)

- ESMA and UAE Regulatory Framework Analysis (Permitted Food Additives List under UAE Food Safety Law, GSO 9:2013 Labeling Compliance, GCC Unified Food Law Alignment, Halal Compliance Requirements for Imported Acidulants, Import Documentation and Certification Requirements, Dubai Municipality Food Control Department Inspection Standards)

- UAE Excise Tax Impact Analysis (50% Tax on Carbonated Drinks, 100% Tax on Energy Drinks, Reformulation Incentives, Beverage Manufacturer Response, Natural and Low-Sugar Acidulant Demand Acceleration)

- UAE as GCC Re-Export Hub Analysis (Jebel Ali Free Zone Ingredient Trade Flows, Re-Export Volumes to Saudi Arabia, Kuwait, Bahrain, Oman, Qatar, Regional Distribution Infrastructure)

- Food Processing Industry Assessment (Beverages, Bakery, Dairy, Meat Processing, Sauces and Condiments, Convenience Foods, Snack Foods)

- Ingredient Import Analysis (Import Volumes by Acidulant Type, Key Sourcing Countries, Import Price Trends, Logistics and Customs Considerations, Free Zone Advantages)

- HoReCa and Tourism Demand Analysis (Hotel Sector F&B Requirements, Tourism Growth Impact, Foodservice Chain Expansion, Michelin-Starred Restaurant Sector)

- SWOT Analysis

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Stakeholder Ecosystem

- Competition Ecosystem

- By Market Value (2020-2025)

- By Volume Consumption (2020-2025)

- By Average Selling Price (2020-2025)

- By Acidulant Type (In Value %)

Citric Acid

Lactic Acid

Acetic Acid

Phosphoric Acid

Malic Acid

Tartaric Acid

Fumaric Acid

Other Acidulants (Adipic Acid, Glucono-delta-lactone, Succinic Acid) - By Function (In Value %)

pH Control & Buffering

Flavor Enhancement

Microbial Control & Preservation

Leavening Agent

Chelating & Sequestrant Agent

Emulsification Support - By Application (In Value %)

Beverages

Bakery & Confectionery

Dairy & Frozen Desserts

Processed Meat & Poultry

Sauces, Dressings & Condiments

Convenience Foods & Ready Meals

Snack Foods

Other Food Applications - By Distribution Channel (In Value %)

Direct Sales to Food Manufacturers

Ingredient Distributors & Specialty Traders

Wholesale & Cash and Carry

Online B2B Platforms - By Emirate (In Value %)

Dubai

Abu Dhabi

Sharjah

Ras Al Khaimah

Other Emirates

- Market Share Analysis (By Value, Volume, Acidulant Type, Application, Distribution Channel)

- Cross Comparison Parameters (Citric Acid Portfolio, Lactic Acid Portfolio, Malic Acid Portfolio, Phosphoric Acid Capability, Natural Acidulant Range, Halal Certification Portfolio, UAE Distribution Network, GCC Re-Export Capability, Technical Application Support, Clean-Label Solutions)

- SWOT Analysis of Major Players

- Pricing Analysis (By Acidulant Type, By Form, By Application, Import vs Local Distribution Pricing)

- Detailed Profiles of Major Companies

Jungbunzlauer Suisse AG

Cargill Incorporated

Tate & Lyle PLC

Corbion N.V.

Archer Daniels Midland Company (ADM)

Bartek Ingredients Inc.

Brenntag SE

Univar Solutions (Univar Food Ingredients)

IMCD Group

Hawkins Watts Limited

Sigma-Aldrich (Merck KGaA)

Weifang Ensign Industry Co. Ltd.

TTCA Co. Ltd.

Gadot Biochemical Industries

Prinova Group LLC

- Food Manufacturer Demand Analysis (Beverages, Dairy, Bakery, Meat, Sauces, Convenience Foods)

- Acidulant Type Adoption Rate by Food Category

- Natural vs Synthetic Acidulant Preference Analysis

- Halal Ingredient Compliance Analysis

- Import Price Sensitivity Analysis by End User Segment

- By Market Value (2026-2035)

- By Volume Consumption (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now