Download PDF

Download PDFMarket Overview

The UAE Food Traceability Market was valued at USD ~ Million in 2024 and is anticipated to expand at a CAGR of ~% during 2026–2035. The market is primarily driven by the UAE’s National Food Security Strategy 2051, government-led blockchain traceability initiatives, and the country’s halal certification framework governing food imports and domestic production. Launched in November 2018, the National Food Security Strategy 2051 aims to make the UAE the world’s best-ranked country in the Global Food Security Index by 2051, supported by 38 short- and long-term initiatives across 5 strategic goals, including diversifying supply sources to cover 3 to 5 alternative origins for each of the 18 main categories in the national food basket. The UAE Cabinet established the Emirates Food Security Council to coordinate implementation across federal and local entities. Silal, Abu Dhabi’s leading agri-tech food company established in September 2020 as part of ADQ, launched a blockchain-powered food tracing system in September 2023, enabling consumers to scan a QR code through the Silal App to trace the farm-to-fork journey of Silal Fresh produce. Meanwhile, the Emirates Authority for Standardization & Metrology (ESMA) and the Ministry of Industry and Advanced Technology (MoIAT) continue to develop blockchain-enabled halal certification frameworks, reflecting the strategic importance of traceability infrastructure across the UAE’s import-dependent food supply chain.

Market Segmentation

By Technology Type

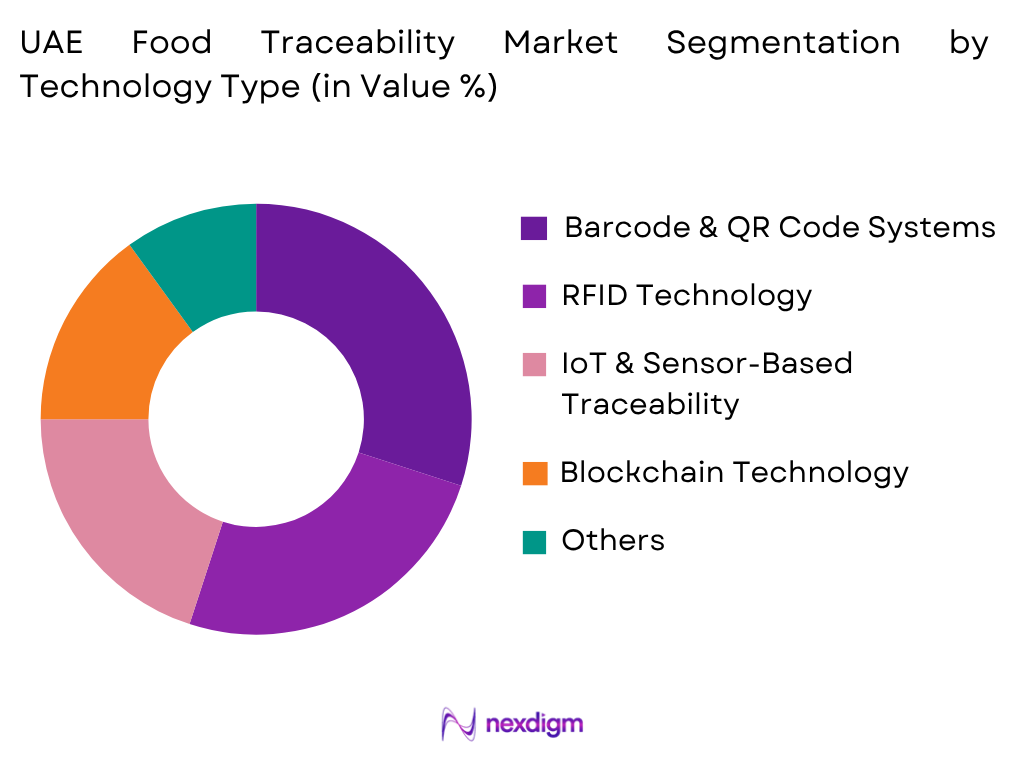

The UAE Food Traceability Market is segmented by technology type into barcode & QR code systems, RFID technology, IoT & sensor-based traceability, blockchain technology, GPS & location tracking systems, and other traceability technologies. Barcode & QR code systems hold the dominant market share due to their widespread compatibility with food labeling, product registration, warehouse identification, and retail scanning infrastructure. The technology is particularly suitable for the UAE’s import-intensive food supply chain, where large volumes of food products pass through registration, inspection, distribution, and retail processes. Dubai Municipality reported more than 1.5 million registered food products and food shipment inspections exceeding 7.3 million tons, illustrating the scale of product identification and compliance requirements across the food ecosystem. Barcode and QR-based systems also provide relatively simple integration with standardized traceability frameworks such as those supported by GS1 UAE. RFID and IoT technologies are increasingly relevant for warehouse visibility and cold-chain monitoring, while blockchain is emerging for provenance, authenticity, and multi-party supply-chain data sharing.

By Application

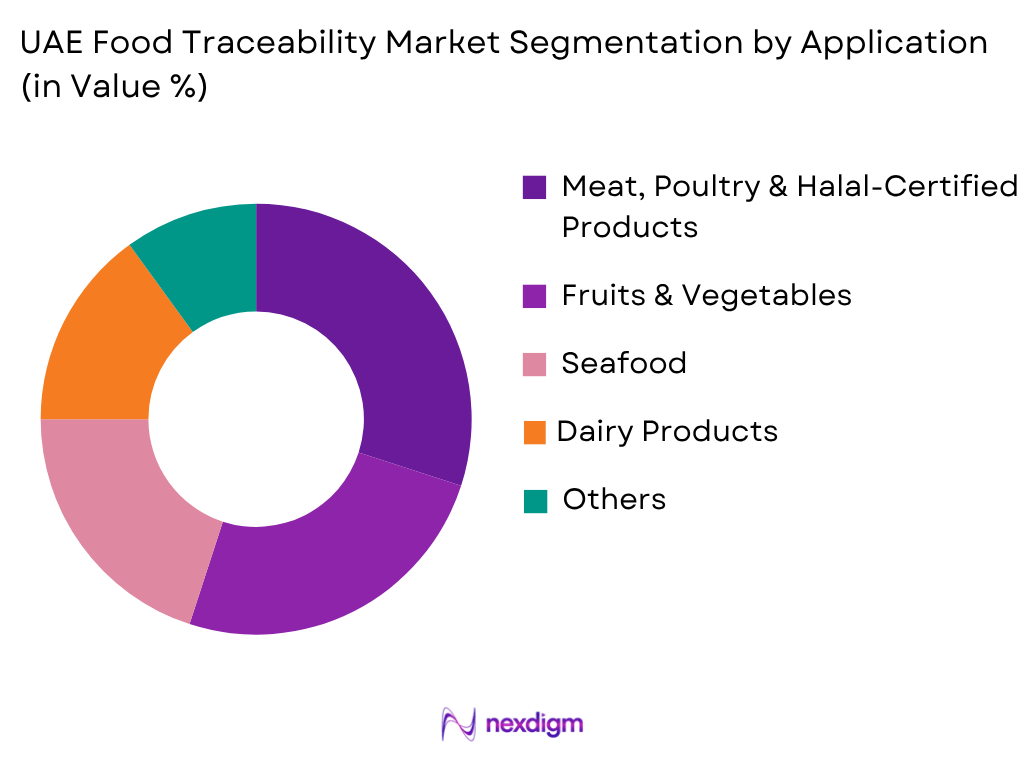

The Meat, Poultry & Halal-Certified Products segment holds a significant share of the UAE Food Traceability Market, reflecting the critical importance of halal certification verification for the country’s substantial food import base. The halal certification process, supervised by MoIAT with regulatory standards set by ESMA, requires accredited Conformity Assessment Bodies to conduct product testing, factory inspections, and audit reporting, creating strong demand for digital traceability systems capable of managing certificate issuance, renewal, and revocation processes. The Fruits & Vegetables segment also represents a significant application area, exemplified by Silal’s blockchain-powered tracing system for fresh produce, which allows consumers to verify the credibility of crop journey data directly through a mobile application. This segment benefits from the UAE’s National Food Security Strategy 2051 emphasis on diversifying fresh produce sourcing and increasing locally grown output through desert farming technology.

Competitive Landscape

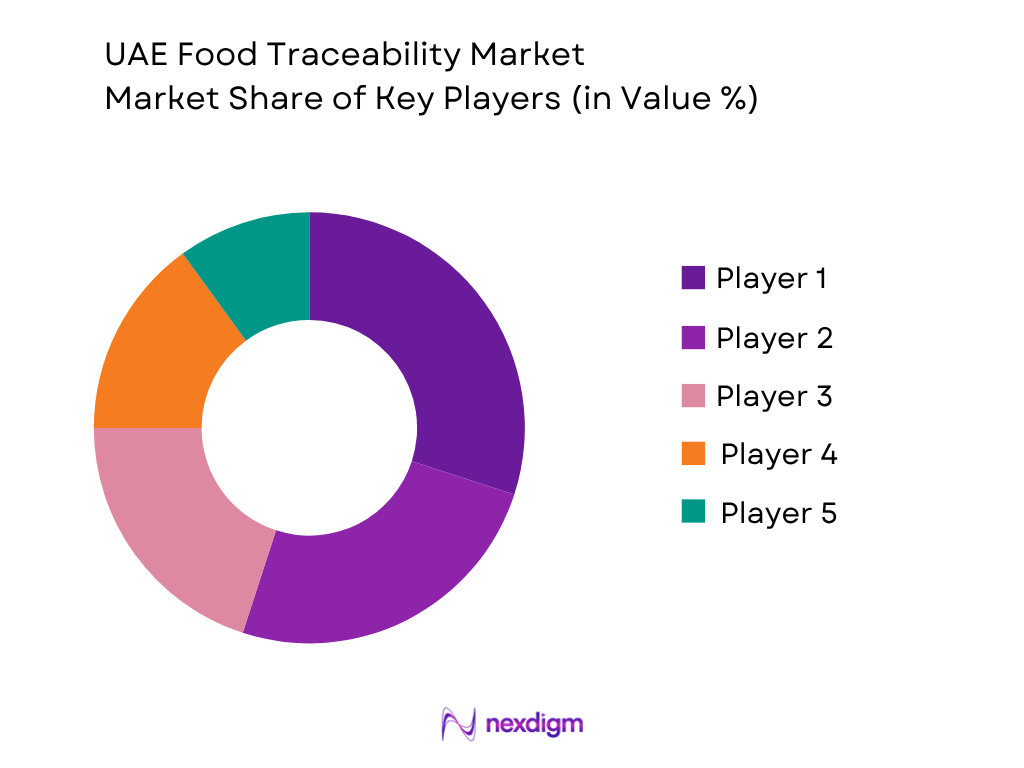

The UAE Food Traceability Market is moderately fragmented, with a government-backed domestic agri-tech company operating alongside established multinational enterprise technology providers and specialized traceability solution vendors. Competition is primarily based on platform interoperability, blockchain integration capability, regulatory compliance support for ESMA and MoIAT halal certification standards, ease of supplier onboarding across the UAE’s multi-source import network, and the ability to serve government-led food security initiatives. Silal, established in September 2020 as part of ADQ, one of the region’s largest holding companies with total assets of approximately USD 225 billion as of mid-2024, has expanded its market position through strategic acquisitions including a majority stake in SAFCO, a leading UAE-based food and beverage distributor, and Al Bakrawe Holding, a major regional importer and distributor of fresh produce. This positions Silal as a uniquely well-capitalized domestic player competing alongside global technology providers such as IBM Food Trust, SAP, Zebra Technologies, and Honeywell International, which supply hardware, software, and enterprise integration solutions to UAE food manufacturers and retailers.

| Company | Establishment Year | Headquarters | Primary Product Portfolio | Traceability Solution Portfolio

|

Deployment Presence | Major End-Use Industries | Key Strategic Focus | Certifications & Compliance |

| Silal | 2020 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| IBM | 1911 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| SAP | 1972 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Honeywell International | 1906 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Zebra Technologies Corporation | 1969 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

UAE Food Traceability Market Analysis

Growth Drivers

National Food Security Strategy 2051 Implementation

The UAE Food Traceability Market is experiencing sustained growth due to the government’s National Food Security Strategy 2051, which aims to position the UAE as the world’s best-ranked country in the Global Food Security Index by 2051. The strategy defines 18 main categories within the national food basket and mandates the identification of 3 to 5 alternative supply sources for each major food category, creating substantial demand for traceability systems capable of verifying and monitoring multiple international supply origins simultaneously. The UAE Cabinet’s establishment of the Emirates Food Security Council to coordinate implementation across federal and local entities further reinforces institutional commitment to traceability infrastructure. Silal’s September 2023 launch of a blockchain-powered food tracing system, enabling consumers to verify the farm-to-fork journey of fresh produce via QR code, exemplifies how government-backed entities are operationalizing the strategy’s technology-enabled sustainable food production objectives.

Halal Certification and Supply Chain Verification

The UAE’s halal certification framework, supervised by the Ministry of Industry and Advanced Technology (MoIAT) with regulatory standards set by the Emirates Authority for Standardization & Metrology (ESMA), continues to drive demand for digital traceability and certification management systems. Researchers have developed blockchain-enabled halal certification frameworks that allow accredited Conformity Assessment Bodies to conduct automated ingredient list scanning against ESMA-defined standards, alongside physical factory inspections, with the resulting certification decisions recorded through chaincode for secure issuance, renewal, or revocation. Given the UAE’s substantial reliance on food imports and its position as a regional trade and re-export hub, robust halal certification traceability systems are essential for maintaining consumer trust and supporting the credibility of the UAE’s food supply chain both domestically and for onward regional distribution.

Market Challenges

Heavy Import Dependency and Multi-Source Verification Complexity

The UAE Food Traceability Market faces significant challenges arising from the country’s heavy reliance on food imports, necessitated by limited arable land and challenging desert growing conditions. The National Food Security Strategy 2051’s own objective of securing 3 to 5 alternative supply sources for each of the 18 main food basket categories, while enhancing resilience, simultaneously creates substantial complexity for traceability systems that must verify and reconcile data across numerous international suppliers with varying levels of digital infrastructure and regulatory standards. Coordinating consistent, auditable traceability data across this diverse and geographically dispersed supplier base remains a significant operational challenge for UAE food importers, distributors, and government agencies.

Fragmented Regulatory Coordination Across Emirates

The UAE Food Traceability Market must navigate a regulatory landscape involving multiple federal and emirate-level bodies, including ESMA, MoIAT, and emirate-specific food safety authorities, each with distinct roles in setting standards, certification, and enforcement. While the Emirates Food Security Council was established to coordinate implementation of the National Food Security Strategy 2051 across federal and local entities, ensuring consistent traceability data standards and certification recognition across Abu Dhabi, Dubai, Sharjah, and the Northern Emirates continues to require ongoing coordination. This fragmentation can create administrative complexity for food companies operating across multiple emirates, each potentially subject to distinct inspection and documentation requirements.

Market Opportunities

Blockchain-Enabled Halal Certification Expansion

Continued development of blockchain-enabled halal certification frameworks, building on research partnerships involving MoIAT and ESMA, presents significant opportunities for traceability technology providers in the UAE. Automated ingredient list scanning, secure chaincode-based certificate management, and digital certificate sharing represent a scalable model that could be extended across the broader Gulf Cooperation Council region, given the UAE’s position as a regional hub for halal food trade and certification. Technology providers that can demonstrate compliance with ESMA standards while streamlining the certification workflow for manufacturers stand to capture significant value as halal food demand continues to grow both regionally and globally.

Regional Hub for Agri-Blockchain Innovation

The UAE, particularly Dubai, is increasingly positioning itself as a regional hub for agri-blockchain innovation, with platforms such as the Agriota E-Marketplace connecting international farmers directly with UAE food companies via blockchain to ensure transparent sourcing and fair pricing. The Middle East blockchain in agriculture and food supply chain market is capturing a growing share of the global market, which is projected to expand from approximately USD 0.6 billion in 2025 to USD 12.1 billion by 2035, at a CAGR of approximately 36%, driven by strategic government investments, food import diversification strategies, and smart farming initiatives. This positions UAE-based traceability providers and government entities such as Silal to develop scalable regional solutions serving both domestic food security objectives and broader Gulf Cooperation Council market needs.

Future Outlook

The UAE Food Traceability Market is expected to witness sustained expansion over the forecast period, supported by continued implementation of the National Food Security Strategy 2051, expanding blockchain-enabled halal certification frameworks, and growing government investment in agri-tech traceability infrastructure. Continued expansion of Silal’s blockchain tracing capabilities and strategic acquisitions across the UAE food distribution value chain are expected to strengthen domestic traceability infrastructure. The market is also likely to benefit from the UAE’s growing position as a regional hub for agri-blockchain innovation, supporting long-term growth across meat, halal-certified products, fresh produce, dairy, and processed food supply chain applications.

Major Players

- Silal

- IBM (Food Trust)

- SAP

- Zebra Technologies

- Honeywell International

- Oracle

- TE-FOOD International

- Antares Vision

- SGS SA

- Trustwell (FoodLogiQ)

- Wholechain

- Agthia Group

- Al Dahra Holding

- Optel Group

- Sensitech (Carrier)

Key Target Audience

- Food Traceability Software and Platform Providers

- Food & Beverage Manufacturers and Importers

- Food Retailers and Grocery Chains

- Foodservice Operators and Distributors

- Cold Chain Logistics and Hardware Providers

- Halal Certification Bodies and Conformity Assessment Bodies

- Investment and Sovereign Wealth Entities

- Government and Regulatory Bodies (Emirates Authority for Standardization & Metrology (ESMA), Ministry of Industry and Advanced Technology (MoIAT), Ministry of Climate Change and Environment (MOCCAE), Emirates Food Security Council)

- Technology Integrators and Compliance Consulting Firms

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying the complete ecosystem of the UAE Food Traceability Market, including software and platform providers, hardware manufacturers, system integrators, food and beverage processors, retailers, and regulatory authorities. Extensive secondary research is conducted using company annual reports, government publications, trade associations, customs statistics, industry journals, and proprietary databases to determine the variables influencing market demand, pricing, deployment, adoption, and technological developments.

Step 2: Market Analysis and Construction

Historical market information is collected and analyzed to estimate market size, deployment volumes, technology adoption trends, application-wise demand, and pricing trends. A combination of top-down and bottom-up approaches is used to estimate market revenues and validate segment-level performance. Adoption patterns across meat, halal-certified products, fresh produce, dairy, and processed foods are evaluated to establish an accurate representation of the industry.

Step 3: Hypothesis Validation and Expert Consultation

The preliminary findings are validated through Computer-Assisted Telephone Interviews (CATIs) and structured discussions with traceability software providers, procurement managers, distributors, food technologists, regulatory experts, and senior executives operating within the UAE food industry. These interviews help verify market assumptions, competitive developments, technology adoption trends, pricing dynamics, and future investment opportunities while refining the overall market estimates.

Step 4: Research Synthesis and Final Output

The final stage integrates insights obtained from primary interviews with quantitative information collected through secondary sources. Data triangulation techniques are applied to reconcile differences between supply-side and demand-side estimates, ensuring robust market forecasting. The report is then reviewed through multiple quality assurance checkpoints to deliver a comprehensive analysis covering market size, segmentation, competitive landscape, future outlook, and strategic recommendations for industry stakeholders.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Primary Industry Interviews, Secondary Research Validation, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Food Traceability Industry Value Chain Analysis

- Supply Chain Analysis

- Growth Drivers (National Food Security Strategy 2051 Implementation, Halal Certification and Supply Chain Verification, Government-Led Blockchain Traceability Initiatives, Heavy Food Import Diversification Requirements, Growth in Modern Retail and E-Commerce Grocery, Rising Consumer Demand for Transparency)

- Market Challenges (Heavy Import Dependency and Multi-Source Verification Complexity, Fragmented Regulatory Coordination Across Emirates, High Implementation Costs, Data Interoperability Complexity, Standardization Gaps Across Multiple Jurisdictions)

- Market Opportunities (Blockchain-Enabled Halal Certification Expansion, Regional Hub for Agri-Blockchain Innovation, AI-Enhanced Traceability and Predictive Analytics, Smart Labeling and Packaging, Cross-Border Trade Facilitation Platforms)

- Market Trends (Blockchain and AI Convergence, QR Code Consumer Transparency Adoption, Desert Agri-Tech and Local Production Traceability, Cross-Border Sourcing Platforms, Multi-Tier Supply Chain Interoperability)

- Government Regulations (ESMA Food Standards and Assessment Protocols, MoIAT Halal Certification Framework, National Food Security Strategy 2051, Import Compliance and Rules of Origin, Labeling Requirements)

- Import and Export Analysis (Trade Volume, Major Import Sources, Export Destinations, HS Code Analysis, Trade Balance)

- Technology Landscape (Blockchain Platforms, RFID and Barcode Systems, IoT Cold Chain Sensors, AI and Predictive Analytics, Cloud-Based Traceability Platforms)

- Sustainability Assessment (Food Waste Reduction, Recall Efficiency, Supply Chain Transparency, Ethical Sourcing Verification, Desert Farming Resource Efficiency)

- PESTLE Analysis

- SWOT Analysis

- Porter’s Five Forces Analysis

- Stakeholder Ecosystem

- Competition Ecosystem

- By Market Value (2020-2025)

- By Volume of Deployments (2020-2025)

- By Average Selling Price (2020-2025)

- By Technology (In Value %)

Blockchain

RFID

Barcode & QR Code

GPS/GIS

IoT Sensors & Others - By Deployment Mode (In Value %)

Cloud-Based

On-Premise

Hybrid - By Application (In Value %)

Meat, Poultry & Halal-Certified Products

Fruits & Vegetables

Seafood

Dairy Products

Bakery & Confectionery

Beverages

Processed Foods - By End User (In Value %)

Food Manufacturers

Food Retailers & Grocery Chains

Foodservice Operators

Distributors & Logistics Providers

Government & Regulatory Agencies - By Region (In Value %)

Abu Dhabi

Dubai

Sharjah & Northern Emirates

- Market Share of Major Players (By Value, Component, Technology, Application Industry, Deployment Mode)

- Cross Comparison Parameters (Platform Portfolio Breadth, Blockchain Integration Capability, Application Technical Support Capability, Deployment Capacity, Regulatory Compliance & Certifications, Food & Beverage Customer Base, Innovation & New Product Launch Frequency)

- SWOT Analysis of Major Players

- Pricing Analysis by Solution Category and Tier

- Deployment Capacity Analysis

- Manufacturing and Platform Footprint Analysis

- Distribution Network Analysis

- Innovation Benchmarking

- Detailed Profiles of Major Companies

Silal

IBM (Food Trust)

SAP

Zebra Technologies

Honeywell International

Oracle

TE-FOOD International

Antares Vision

SGS SA

Trustwell (FoodLogiQ)

Wholechain

Agthia Group

Al Dahra Holding

Optel Group

Sensitech (Carrier)

- Consumption Pattern Analysis (Deployment Scale, Integration Complexity, Product Category Penetration, Seasonal Demand, Reformulation Activity)

- Purchasing Criteria (Regulatory Compliance, Cost Efficiency, Interoperability, Scalability, Data Security, Supplier Onboarding Ease)

- Procurement and Supplier Selection Analysis

- Clean Label and Transparency Adoption Assessment

- Premium vs Conventional Solution Demand

- Product Attribute Preference Analysis (Data Accuracy, Real-Time Visibility, Ease of Integration, Scalability, Regulatory Alignment, User Friendliness)

- Consumer Health & Wellness Influence on Product Development

- Pain Point Analysis

- Decision-Making Process

- By Market Value (2026-2035)

- By Volume of Deployments (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now