Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the UAE Freight Aggregator market is expected to reach approximately USD ~ billion by the end of the year, driven by rapid growth in the logistics and e-commerce sectors. Factors such as government initiatives to enhance infrastructure and the increasing need for efficient transportation solutions contribute to the market’s expansion. The growing demand for faster and more cost-effective shipping solutions is one of the primary drivers of market growth. This market’s development is also supported by the increasing digitization and automation in freight operations.

Dominant cities in the UAE, such as Dubai and Abu Dhabi, lead the market due to their strategic locations as logistics hubs, and robust infrastructure investments by the government, making them ideal for shipping and warehousing operations. Dubai’s status as a key global trade center and its state-of-the-art facilities, including its ports and airports, attract international logistics companies, contributing to the city’s dominance. Furthermore, the UAE’s policies encouraging business expansion in the transportation and logistics sectors further solidify its competitive edge in the freight aggregation space.

Market Segmentation

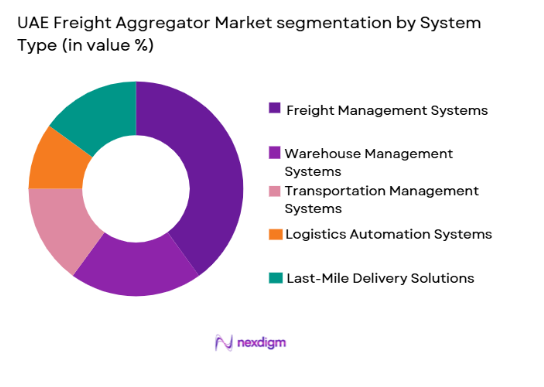

By System Type:

UAE Freight Aggregator market is segmented by system type into Freight Management Systems, Warehouse Management Systems, Transportation Management Systems, Logistics Automation Systems, and Last-Mile Delivery Solutions. Recently, Freight Management Systems has a dominant market share due to the increasing demand for streamlined operations, real-time tracking, and integration with other logistics services. Companies are increasingly adopting these systems to reduce inefficiencies and meet the growing consumer demand for speed and reliability in freight operations. With technological advancements and investments in digital platforms, Freight Management Systems are integral to optimizing the supply chain processes and improving overall logistics performance.

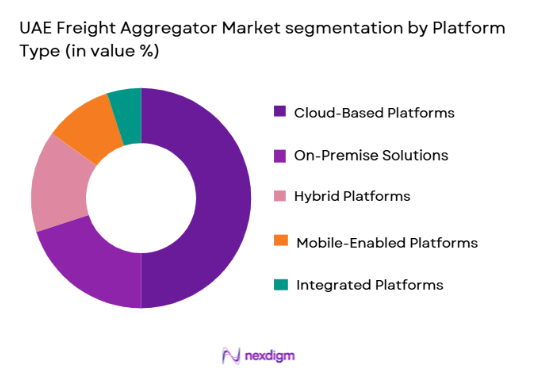

By Platform Type:

UAE Freight Aggregator market is segmented by platform type into Cloud-Based Platforms, On-Premise Solutions, Hybrid Platforms, Mobile-Enabled Platforms, and Integrated Platforms. Cloud-Based Platforms have gained a significant share due to their ability to provide flexibility, scalability, and real-time updates across the entire logistics network. The demand for cloud-based solutions has surged as businesses are increasingly looking to reduce overhead costs and improve operational efficiency. These platforms offer seamless integration, allowing users to manage and monitor their logistics processes from anywhere, making them an attractive choice for organizations operating in the fast-paced freight aggregation market.

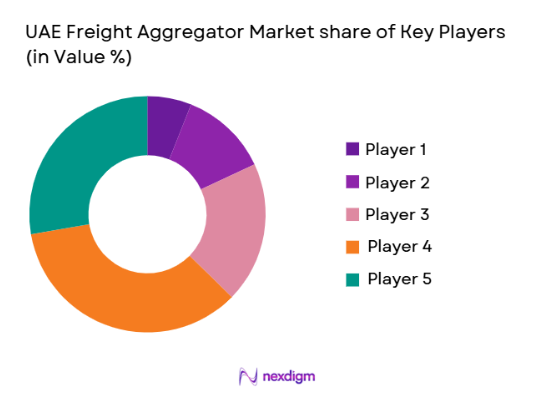

Competitive Landscape

The UAE Freight Aggregator market is highly competitive, with several major players involved in consolidating market share through partnerships, technological advancements, and geographic expansion. The influence of leading players in the logistics and transportation sector continues to drive market development, with established companies diversifying their portfolios to include innovative freight aggregation solutions. These firms leverage their extensive supply chain networks and deep pockets for R&D to stay ahead of the competition. Mergers and acquisitions within the sector also shape the market’s dynamics, creating opportunities for increased market penetration and service diversification.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Technology Integration |

| Aramex | 1982 | Dubai, UAE | ~ | ~ | ~ | ~ | ~ |

| DP World | 2005 | Dubai, UAE | ~ | ~ | ~ | ~ | ~ |

| DHL Supply Chain | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| DB Schenker | 1872 | Essen, Germany | ~ | ~ | ~ | ~ | ~ |

UAE Freight Aggregator Market Analysis

Growth Drivers

Government Support for Infrastructure Development:

Government initiatives focused on infrastructure development, including port upgrades and the construction of logistics parks, play a significant role in driving the growth of the UAE Freight Aggregator market. As part of its strategic Vision 2030, the UAE has made substantial investments in enhancing its transportation and logistics infrastructure. These initiatives create a conducive environment for the growth of the freight aggregation market by reducing transportation bottlenecks and enabling faster shipping solutions. Additionally, the introduction of tax incentives and public-private partnerships further accelerates the development of modern logistics hubs and facilitates trade within and outside the UAE. These government efforts ensure that the country remains competitive in the global logistics market.

E-commerce Growth and Demand for Faster Shipping:

The boom in the e-commerce industry, particularly in the UAE and the wider Middle East region, has significantly contributed to the demand for efficient freight aggregation services. Consumers are increasingly expecting faster delivery times, putting pressure on logistics providers to adopt smarter and more agile systems. The rise of online retail platforms has led to a surge in demand for last-mile delivery and real-time tracking solutions, making freight management systems and logistics automation crucial to meeting consumer expectations. The growing trend of on-demand services has also prompted businesses to optimize their supply chains to handle higher volumes of goods in shorter timeframes, further boosting the need for advanced freight aggregation systems.

Market Challenges

High Operational Costs:

One of the key challenges facing the UAE Freight Aggregator market is the high operational costs associated with transportation, warehousing, and technology integration. While infrastructure improvements and technological advancements have helped to streamline logistics processes, the cost of maintaining these systems remains a burden for many players in the market. The high costs of fuel, labor, and logistics equipment, as well as rising regulatory compliance expenses, continue to impact profitability. As the demand for faster and more efficient services grows, so does the pressure to balance cost-effectiveness with service quality. Companies must find innovative ways to reduce operational costs while maintaining competitive service levels, posing a significant challenge to profitability in this market.

Integration of Emerging Technologies:

While the integration of cutting-edge technologies such as AI, IoT, and automation has the potential to greatly enhance operational efficiency, many companies in the UAE Freight Aggregator market face challenges in adopting these solutions. The high initial investment required for upgrading legacy systems to accommodate new technologies can be a barrier to entry for smaller logistics firms. Furthermore, the complexity of integrating multiple technologies across the entire supply chain can lead to operational disruptions if not managed properly. As a result, many companies struggle to stay ahead of the curve in terms of technological adoption, which hampers their ability to scale and meet the growing demands of the market.

Opportunities

Demand for Sustainable Freight Solutions:

There is a growing emphasis on sustainability in the logistics sector, driven by both government policies and consumer preferences for eco-friendly services. The UAE Freight Aggregator market stands to benefit from the rising demand for sustainable freight solutions, such as electric vehicles (EVs) for last-mile delivery, and optimized routes that reduce fuel consumption. Additionally, the development of green logistics infrastructure, such as energy-efficient warehouses and the use of renewable energy sources, presents a lucrative opportunity for market players. As companies increasingly focus on reducing their carbon footprint and aligning with global sustainability goals, this trend is expected to lead to new growth opportunities in the market.

Expansion into Emerging Markets:

The growing demand for freight aggregation services across emerging markets in the Middle East and North Africa (MENA) presents a significant growth opportunity for companies operating in the UAE. As trade volumes increase in these regions, there is an increasing need for efficient logistics solutions to support the movement of goods. By expanding into these high-growth markets, companies can capitalize on the rising demand for advanced freight aggregation systems. Furthermore, regional trade agreements and economic collaborations between the UAE and other MENA countries are expected to boost cross-border trade, further driving the need for reliable and scalable logistics solutions in these areas.

Future Outlook

The future outlook of the UAE Freight Aggregator market appears positive, with continued growth expected over the next five years. Technological advancements, such as AI-powered systems, automation, and IoT solutions, will drive operational efficiency and optimize logistics operations. Government support for infrastructure development, alongside the increasing demand for sustainable and efficient freight services, will further fuel the market’s growth. As consumer demand for faster and more reliable delivery services rises, logistics companies in the UAE will continue to innovate, presenting opportunities for both local and global players to expand their presence in the region.

Major Players

- Aramex

- DP World

- DHL Supply Chain

- Kuehne + Nagel

- DB Schenker

- XPO Logistics

- CEVA Logistics

- TNT Express

- UPS

- FedEx

- Kerry Logistics

- Logitech

- Transcom

- Meydan Freight Services

- Agility Logistics

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Logistics companies

- Retail and e-commerce platforms

- Manufacturers

• Third-party logistics (3PL) providers

• Shipping and freight service providers

• Technology providers for logistics solutions

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying the critical market variables that influence the market landscape, including economic, technological, and regulatory factors.

Step 2: Market Analysis and Construction

Market trends, customer needs, and competitor dynamics are analyzed and constructed into a comprehensive market model, providing a foundation for projections and forecasts.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through consultations with industry experts, ensuring that the findings are relevant and actionable for decision-makers.

Step 4: Research Synthesis and Final Output

The research findings are synthesized into a final market report, providing actionable insights and strategic recommendations for market participants.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rise in E-commerce Demand

Increasing Focus on Logistics Efficiency

Government Initiatives to Boost Infrastructure

Adoption of Advanced Technologies in Freight

Growing Cross-Border Trade - Market Challenges

High Operational Costs

Regulatory Compliance Issues

Integration of New Technologies

Security Concerns in Freight Systems

Dependency on Infrastructure Development - Market Opportunities

Emerging Demand for Green Logistics

Expansion of Smart Cities and IoT Applications

Adoption of Autonomous Delivery Systems - Trends

Shift to Cloud-Based Freight Solutions

Focus on Last-Mile Delivery Innovation

Increased Investment in Digital Platforms

Integration of AI and Robotics

Growth in Cross-Border E-commerce Logistics - Government Regulations & Defense Policy

Regulations on Data Privacy in Freight

Government Funding for Transportation Infrastructure

Policies on Sustainable Logistics Solutions - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Freight Management Systems

Warehouse Management Systems

Transportation Management Systems

Logistics Automation Systems

Last-Mile Delivery Solutions - By Platform Type (In Value%)

Cloud-Based Platforms

On-Premise Solutions

Hybrid Platforms

Mobile-Enabled Platforms

Integrated Platforms - By Fitment Type (In Value%)

On-Demand Solutions

Fixed Installations

Custom Solutions

Scalable Solutions

Fully Automated Solutions - By EndUser Segment (In Value%)

Retail Industry

Logistics Providers

E-commerce Platforms

Manufacturers

Third-Party Logistics (3PL) Providers - By Procurement Channel (In Value%)

Direct Procurement

Bidding Platforms

Third-Party Distributors

Online Marketplaces

Private Sector Procurement - By Material / Technology (in Value%)

AI-Powered Systems

Internet of Things (IoT) Solutions

Blockchain Technology

Robotics and Automation

Data Analytics Solutions

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Material/Technology, Key Partnerships, Geographic Presence, Innovation Capacity, Market Reach)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Aramex

DP World

DB Schenker

Maersk

Kuehne + Nagel

DHL Supply Chain

XPO Logistics

CEVA Logistics

TNT Express

UPS

FedEx

Kerry Logistics

Logitech

Transcom

Meydan Freight Services

- Increased Demand from E-commerce Platforms

- Challenges Faced by 3PL Providers

- Adoption of Automation in Retail Logistics

- Technological Advancements in Freight Management

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now