Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UAE home finance market demonstrates strong institutional depth with outstanding residential mortgage balances estimated at approximately USD ~ billion based on a recent historical assessment by central banking disclosures and financial statements of leading lenders. Market expansion is driven by sustained expatriate homeownership demand, developer-backed financing schemes, and competitive Islamic and conventional mortgage offerings from major banks, supported by stable property transaction volumes and regulatory clarity in lending frameworks.

Dubai and Abu Dhabi dominate the UAE home finance market due to concentrated population density, premium residential supply, and mature property registration ecosystems enabling efficient mortgage processing and collateral enforcement. Dubai leads through international buyer participation and large-scale master-planned developments, while Abu Dhabi benefits from government-linked housing initiatives and higher income stability among nationals. Both emirates host the majority of bank headquarters and developer financing partnerships, reinforcing financing availability and borrower access.

Market Segmentation

By Product Type

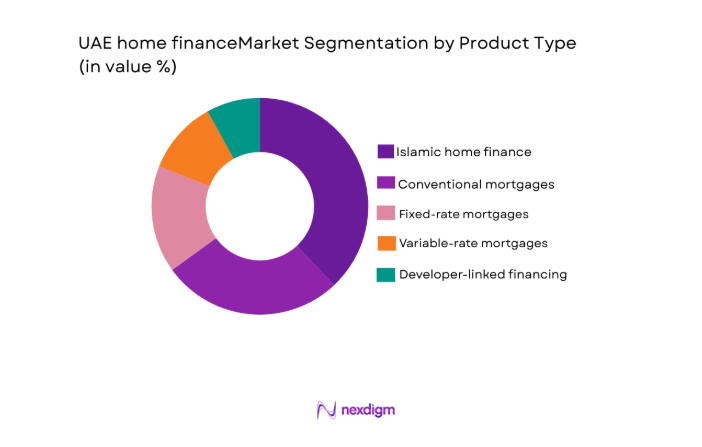

UAE home finance market is segmented by product type into conventional mortgages, Islamic home finance, fixed-rate mortgages, variable-rate mortgages, and developer-linked financing. Recently, Islamic home finance has a dominant market share due to strong consumer preference for Sharia-compliant structures, extensive product availability from Islamic banks, and government support for Islamic finance leadership. The segment benefits from cost-plus Murabaha and Ijara structures aligning with regional cultural expectations and risk-sharing principles. Major lenders actively promote Islamic offerings through competitive profit rates and bundled property packages, attracting both nationals and expatriates seeking ethical finance alternatives. Regulatory endorsement of Islamic banking frameworks and tax neutrality between Islamic and conventional products further sustains its market leadership.

By Platform Type

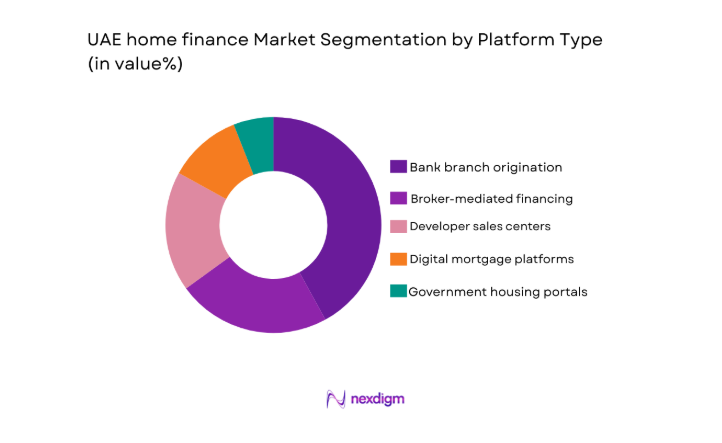

UAE home finance market is segmented by platform type into bank branch origination, digital mortgage platforms, broker-mediated financing, developer sales centers, and government housing portals. Recently, bank branch origination has a dominant market share due to borrower trust in established banking relationships, regulatory documentation requirements, and preference for in-person advisory during high-value property transactions. Large lenders maintain specialized mortgage desks and relationship managers offering tailored eligibility assessments and cross-selling of insurance and accounts, reinforcing branch relevance. Complex expatriate documentation, valuation coordination, and title registration processes often necessitate physical verification, sustaining branch-led origination dominance despite gradual digitalization. Strategic co-location of bank desks within developer projects also channels applicants through branch-linked processing pipelines.

Competitive Landscape

The UAE home finance market is moderately consolidated, with large universal and Islamic banks controlling most mortgage portfolios through extensive funding bases and developer alliances. Competition centers on pricing spreads, loan-to-value flexibility, and expatriate eligibility criteria, while digital onboarding and pre-approval speed increasingly differentiate lenders. Strategic partnerships with major developers and government housing programs reinforce incumbent dominance and create high entry barriers for smaller institutions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Loan-to-Value Range |

| Emirates NBD | 1963 | Dubai | ~ | ~ | ~ | ~ | ~ |

| First Abu Dhabi Bank | 2017 | Abu Dhabi | ~ | ~ | ~ | ~ | ~ |

| Abu Dhabi Commercial Bank | 1985 | Abu Dhabi | ~ | ~ | ~ | ~ | ~ |

| Dubai Islamic Bank | 1975 | Dubai | ~ | ~ | ~ | ~ | ~ |

| Mashreq Bank | 1967 | Dubai | ~ | ~ | ~ | ~ | ~ |

UAE Home Finance Market Analysis

Growth Drivers

Rising expatriate property ownership and residency-linked real estate demand

The UAE residential financing landscape is structurally supported by a large expatriate population seeking long-term housing stability in response to evolving residency regulations and property-linked visa frameworks that encourage ownership rather than rental tenure. Expanded residency pathways, including long-duration investor and professional visas, have strengthened expatriate willingness to commit capital into real estate assets financed through mortgages, directly enlarging the eligible borrower base for home finance institutions. Property developers actively align with this demand by structuring payment plans that transition buyers into bank mortgages upon project completion, creating a pipeline of financed transactions and predictable mortgage origination volumes. Mortgage lenders respond through specialized expatriate underwriting models that account for employment contracts, income remittance patterns, and sectoral risk segmentation, enabling broader credit access without materially elevating default risk. International workforce inflows into finance, technology, and professional services sectors concentrated in Dubai and Abu Dhabi sustain consistent demand for mid-to-premium residential units typically financed through bank loans rather than cash purchases. Home finance growth is further reinforced by competitive interest and profit rate cycles linked to global benchmarks that periodically reduce borrowing costs and stimulate refinancing activity among existing homeowners. Banking institutions leverage cross-selling strategies tying mortgages with salary transfer accounts, insurance, and wealth products, increasing customer lifetime value and incentivizing aggressive mortgage acquisition campaigns. Stable legal enforceability of property rights and mortgage collateral under UAE land department systems enhances lender confidence and encourages balance sheet allocation toward housing finance portfolios. Consequently, expatriate ownership expansion functions as a foundational demand engine sustaining mortgage market depth and long-term growth trajectory.

Developer-bank financing partnerships and structured property sales ecosystems

The UAE home finance market benefits from a uniquely integrated developer-bank collaboration model in which major real estate developers pre-arrange mortgage facilities with partner banks to streamline buyer financing at the point of sale. Large master developers embed bank representatives within project sales centers, enabling instant eligibility assessment, pre-approval issuance, and documentation capture during property reservation stages, significantly reducing friction in mortgage acquisition. This arrangement increases conversion rates from off-plan sales to financed purchases, particularly among expatriate buyers who rely on financing to complete property transfers upon handover. Developers further incentivize mortgage uptake through subsidized profit rates, fee waivers, and post-handover payment plans that bridge the transition from construction installments to bank mortgages, sustaining origination pipelines for lenders. Banks benefit from predictable borrower inflows linked to large project launches and phased community developments, allowing targeted capital allocation and portfolio growth planning aligned with construction cycles. Regulatory clarity on escrow accounts, project registration, and completion assurance reduces financing risk perception and encourages banks to participate in developer-linked mortgage programs at scale. Mortgage securitization potential and stable collateral valuation within planned communities further enhance lender appetite for such structured partnerships. The ecosystem also supports digital integration of property registries, valuation services, and mortgage processing, improving approval speed and customer experience while reducing operational costs. As a result, developer-bank alignment acts as a systemic growth driver anchoring mortgage market expansion across residential development cycles.

Market Challenges

Interest rate sensitivity and borrower affordability constraints in variable benchmark environments

The UAE home finance market is inherently exposed to global monetary policy transmission through its currency peg and banking sector linkage to international benchmark rates, causing mortgage profit and interest rates to fluctuate in tandem with external tightening cycles. Rising borrowing costs elevate monthly repayment obligations for variable-rate borrowers and reduce eligibility thresholds under debt-burden ratio regulations, shrinking the pool of qualified applicants and slowing new mortgage origination volumes. Prospective homeowners often delay purchases during high-rate periods, shifting toward rental accommodation or smaller property segments, which alters financing mix and compresses average loan sizes for lenders. Existing borrowers also face refinancing risk as fixed-rate periods expire and loans reset to higher floating rates, potentially increasing delinquency probability among leveraged households. Banks must strengthen credit assessment buffers and provisioning frameworks during such cycles, increasing capital allocation costs and reducing net profitability from mortgage portfolios. Developer sales momentum can weaken when financing affordability declines, indirectly reducing mortgage demand and exposing lenders to pipeline volatility linked to real estate transaction cycles. Government housing programs and developer subsidies partially offset affordability pressure but are insufficient to neutralize macro-rate effects across the broader expatriate market segment. Mortgage lenders consequently confront cyclical origination instability and heightened credit risk management burdens during tightening phases. Sustained rate volatility therefore represents a structural constraint affecting long-term financing accessibility and market expansion stability.

Concentration risk in prime urban property markets and limited geographic diversification

The UAE home finance market is heavily concentrated in Dubai and Abu Dhabi residential sectors, exposing lenders to correlated real estate price cycles and localized economic conditions rather than diversified national housing demand. Mortgage collateral values are closely tied to urban property performance within these emirates, making portfolios sensitive to supply surges in specific communities or cyclical corrections in luxury and expatriate-focused housing segments. Secondary emirates possess smaller and less liquid property markets with limited transaction depth, discouraging lenders from expanding mortgage exposure beyond primary urban centers and reinforcing concentration risk. Geographic concentration also aligns borrower employment exposure with similar economic sectors such as government, oil-linked industries, and service sectors located in major cities, increasing systemic credit correlation within portfolios. During downturns affecting prime urban real estate, lenders face simultaneous collateral value adjustments and borrower repayment stress, amplifying loss severity compared to geographically diversified housing markets. Regulatory loan-to-value caps mitigate leverage risk but do not eliminate exposure to regional price volatility within concentrated metropolitan housing ecosystems. Expansion into affordable housing and emerging emirate markets remains constrained by lower property liquidity and valuation transparency challenges. Mortgage lenders therefore maintain portfolios skewed toward high-value urban properties, limiting diversification and increasing cyclical sensitivity. Concentration in dominant emirates consequently represents a structural vulnerability affecting resilience and risk distribution in the UAE home finance market.

Opportunities

Digital mortgage origination and automated credit assessment transformation

The UAE home finance market presents substantial growth potential through end-to-end digital mortgage platforms that automate borrower onboarding, credit evaluation, property valuation coordination, and approval workflows, significantly reducing processing time and operational costs for lenders. Integration of national digital identity systems and electronic property registries enables remote documentation verification and secure transaction processing without physical branch interaction, improving accessibility for expatriate borrowers with complex employment documentation. Artificial intelligence-based credit scoring models incorporating income stability analytics, remittance behavior, and sectoral employment risk can expand eligibility for underserved borrower segments while maintaining prudent risk thresholds. Digital pre-approval systems embedded within developer portals and real estate platforms allow buyers to obtain financing eligibility instantly during property search, increasing conversion from interest to purchase. Mortgage lenders can leverage data analytics to personalize pricing, optimize loan-to-value ratios, and predict refinancing opportunities, enhancing portfolio profitability and customer retention. Automated valuation models reduce dependency on manual appraisals and accelerate loan disbursement cycles, improving borrower experience and competitive positioning. Fintech partnerships and open banking frameworks enable seamless integration of salary data, account histories, and payment patterns into underwriting processes. Digital transformation also lowers origination costs, allowing lenders to serve mid-income segments profitably and expand mortgage penetration. Consequently, digitalization represents a high-impact opportunity to scale accessibility, efficiency, and market reach within the UAE home finance ecosystem.

Expansion of affordable housing finance and government-supported ownership programs

The UAE home finance market has significant opportunity to broaden mortgage penetration through affordable housing initiatives and government-backed ownership schemes targeting mid-income expatriates and nationals currently underserved by traditional mortgage structures. Public-private partnerships enabling subsidized land allocation and developer incentives can reduce property acquisition costs, making financed ownership feasible for a larger demographic segment previously constrained to rental markets. Mortgage lenders can design lower loan-size products with flexible repayment tenors and structured down-payment support aligned with government housing objectives, expanding portfolio diversification and volume growth. Specialized financing frameworks for first-time buyers and long-term residents strengthen social stability goals while generating sustained mortgage demand. Integration of housing funds and guarantee programs can reduce credit risk exposure for lenders entering affordable segments, encouraging participation across banks and Islamic institutions. Affordable housing communities also create new collateral pools with standardized valuation and liquidity characteristics, enhancing financing scalability. Growth in workforce housing linked to economic diversification sectors such as manufacturing, logistics, and services further expands borrower bases beyond prime urban professionals. Mortgage institutions leveraging this segment can achieve stable long-duration portfolios with lower volatility compared to luxury property cycles. Therefore, affordable housing finance expansion offers a structurally resilient growth avenue for the UAE home finance market.

Future Outlook

The UAE home finance market is expected to expand steadily as digital lending infrastructure matures and residency-linked property ownership incentives continue attracting expatriate buyers. Technological integration across registries, valuation, and underwriting will shorten approval timelines and broaden borrower access. Regulatory stability and developer-bank partnerships will sustain origination pipelines, while affordable housing initiatives may diversify demand segments. Interest rate normalization cycles could further improve affordability and refinancing activity.

Major Players

- Emirates NBD

- First Abu Dhabi Bank

- Abu Dhabi Commercial Bank

- Dubai Islamic Bank

- Mashreq Bank

- HSBC UAE

- Standard Chartered UAE

- Commercial Bank of Dubai

- Sharjah Islamic Bank

- Ajman Bank

- National Bank of Fujairah

- United Arab Bank

- RAKBANK

- Al Hilal Bank

- ADIB

Key Target Audience

- Banks and mortgage lender

- Real estate developers

- Property investment firms

- Investments and venture capitalist firms

- Government and regulatory bodies

- Housing finance institutions

- Islamic finance providers

- Property brokerage networks

Research Methodology

Step 1: Identification of Key Variables

Core variables including mortgage outstanding volumes, property transaction values, lending rates, borrower demographics, and emirate-level housing supply were mapped. Regulatory frameworks, bank financial disclosures, and housing policy indicators were incorporated to define market boundaries and structural drivers.

Step 2: Market Analysis and Construction

Segmental modeling by product type and origination platform was developed using bank portfolio data and property transaction distribution. Urban concentration factors, developer financing ecosystems, and borrower eligibility parameters were synthesized to construct market structure and competitive dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on demand drivers, digital adoption, and affordability trends were validated through review of central banking publications, lender reports, and housing authority disclosures. Cross-verification ensured consistency across institutional, geographic, and borrower-segment dimensions.

Step 4: Research Synthesis and Final Output

Quantitative estimates and qualitative insights were integrated into a unified framework describing growth drivers, risks, and opportunities. Segmentation shares, competitive positioning, and outlook assessments were finalized to produce an actionable UAE home finance market outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expatriate Residency-Linked Property Ownership Demand

Developer-Bank Integrated Financing Ecosystems

Competitive Islamic Finance Penetration

Urban Population Concentration in Dubai and Abu Dhabi

Digital Mortgage Processing and Approval Systems - Market Challenges

Interest Rate Sensitivity to Global Benchmark Cycles

High Property Price Concentration in Prime Emirates

Stringent Debt Burden Ratio Regulations

Expatriate Employment Volatility Risk

Limited Affordable Housing Supply - Market Opportunities

Expansion of Affordable Housing Finance Programs

Digital Mortgage and Remote Onboarding Adoption

Green and Sustainable Housing Finance Products - Trends

Increasing Adoption of Islamic Home Finance

Growth of Digital Mortgage Origination Channels

Rising Off-Plan Property Financing Demand

Integration of AI in Credit Assessment

Developer-Subsidized Mortgage Rate Programs - Government Regulations & Defense Policy

UAE Central Bank Mortgage Lending Caps and LTV Rules

Islamic Finance Regulatory Framework Alignment

Residency Visa Policies Linked to Property Ownership - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Islamic Home Finance

Conventional Mortgage Loans

Fixed-Rate Mortgage Products

Variable-Rate Mortgage Products

Developer-Linked Mortgage Schemes - By Platform Type (In Value%)

Bank Branch Origination

Digital Mortgage Platforms

Broker-Mediated Financing

Developer Sales Center Financing

Government Housing Portals - By Fitment Type (In Value%)

Ready Property Financing

Off-Plan Property Financing

Refinancing and Balance Transfer

Equity Release Financing

Construction-Linked Financing - By End User Segment (In Value%)

Expatriate Salaried Buyers

UAE National Homebuyers

Property Investors

First-Time Homebuyers

High-Net-Worth Individuals

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Mortgage Portfolio Size, Islamic Finance Capability, Digital Origination Level, LTV Range, Expatriate Eligibility Policy, Developer Partnerships, Processing Time, Interest/Profit Rate Competitiveness)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Emirates NBD

First Abu Dhabi Bank

Abu Dhabi Commercial Bank

Dubai Islamic Bank

Abu Dhabi Islamic Bank

Mashreq Bank

Commercial Bank of Dubai

HSBC Middle East

Standard Chartered UAE

RAKBANK

Sharjah Islamic Bank

Ajman Bank

United Arab Bank

National Bank of Fujairah

Al Hilal Bank

- Expatriate professionals represent the largest financed buyer base due to residency-linked ownership incentives

- UAE nationals benefit from government housing programs and subsidized financing structures

- Property investors drive demand for refinancing and equity release products

- High-net-worth individuals sustain premium mortgage demand in luxury developments

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now