Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UAE last-mile delivery market is valued at approximately USD ~ billion based on a recent historical assessment, supported by strong expansion in e-commerce retailing, food delivery platforms, and rapid urban logistics development. Growth is driven by rising parcel volumes from online marketplaces such as Amazon and Noon, alongside increasing demand for same-day and on-demand deliveries. Investments in smart logistics infrastructure, digital fleet management systems, and automated fulfillment centers are also strengthening delivery efficiency, accelerating adoption of advanced last-mile logistics services across the country’s retail and logistics sectors.

Dubai and Abu Dhabi dominate the UAE last-mile delivery market due to high population density, extensive retail infrastructure, and strong e-commerce penetration. Dubai functions as the country’s primary logistics hub supported by Dubai Logistics City, Jebel Ali Port, and advanced urban transport networks that facilitate efficient parcel distribution. Abu Dhabi benefits from growing digital commerce adoption and government-backed logistics modernization programs. Other cities including Sharjah and Al Ain are emerging logistics nodes as retail expansion, food delivery demand, and residential development increase parcel delivery volumes across the broader UAE urban ecosystem.

Market Segmentation

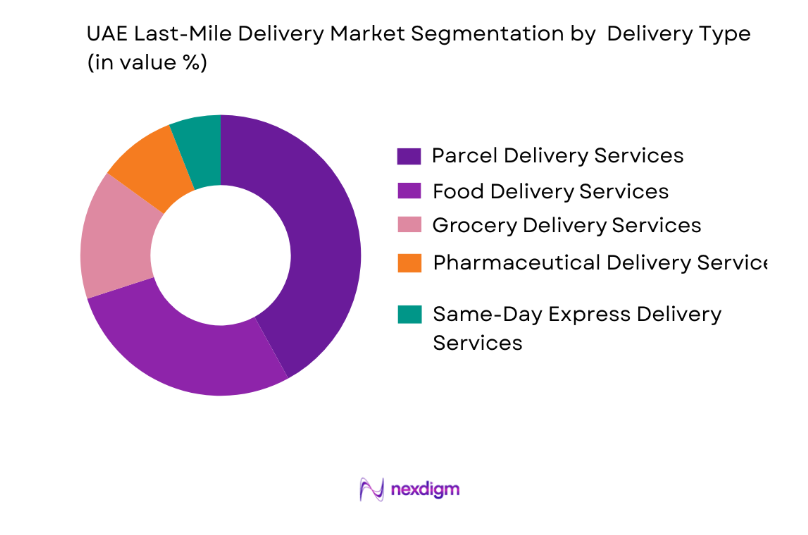

By Delivery Type

UAE Last-Mile Delivery market is segmented by delivery type into parcel delivery services, food delivery services, grocery delivery services, pharmaceutical delivery services, and same-day express delivery services. Recently, parcel delivery services has a dominant market share due to factors such as strong e-commerce expansion, rising online retail transactions, and the presence of major international logistics providers operating large-scale parcel distribution networks. Major e-commerce platforms including Amazon, Noon, and regional online retailers generate large volumes of parcels that require efficient final-mile distribution across urban areas. Parcel delivery providers increasingly deploy automated sorting centers, digital tracking platforms, and route optimization software to manage high shipment volumes efficiently. Retailers and logistics firms also invest in micro fulfillment centers and urban distribution hubs located close to residential areas to improve delivery speed. The growth of cross-border e-commerce imports further increases parcel delivery demand, particularly through Dubai’s logistics hubs connected to global trade networks.

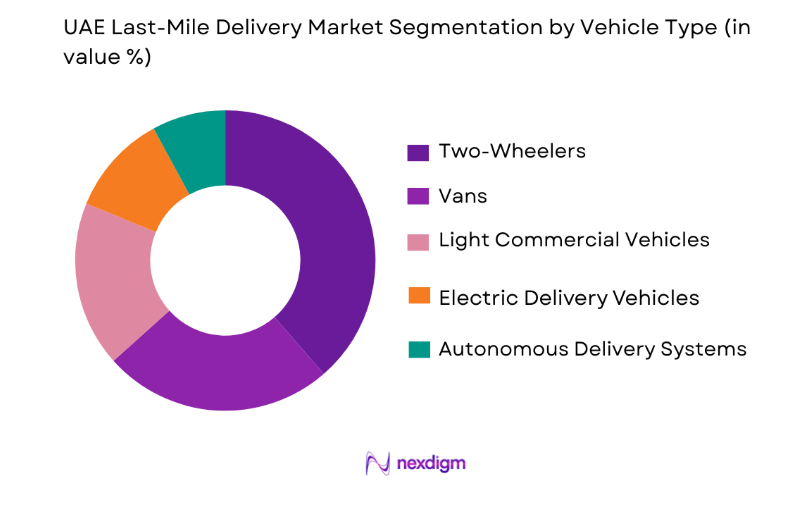

By Vehicle Type

UAE Last-Mile Delivery market is segmented by Vechicle type into two-wheelers, vans, light commercial vehicles, electric delivery vehicles, and autonomous delivery systems. Recently, two-wheelers has a dominant market share due to factors such as faster navigation through congested urban areas, lower operating costs, and strong adoption by food delivery and quick commerce platforms. Motorbikes enable delivery riders to complete multiple short-distance deliveries within dense urban environments where parking limitations and traffic congestion affect larger vehicles. Food delivery platforms including Talabat, Deliveroo, and Careem heavily rely on motorbike fleets to ensure rapid order fulfillment. Logistics companies also prefer two-wheelers because they require lower fuel consumption and reduced maintenance costs compared to larger delivery vehicles. Rapid growth in quick commerce services delivering groceries and convenience products within short time windows further strengthens demand for motorbike-based delivery networks across major UAE cities.

Competitive Landscape

The UAE last-mile delivery market features a moderately consolidated competitive structure where large international logistics providers operate alongside regional courier companies and technology-driven delivery platforms. Major firms maintain strong delivery networks supported by automated fulfillment centers, advanced route optimization technologies, and integrated digital logistics platforms. Competitive advantage is largely determined by delivery speed, fleet capacity, technological integration, and geographic network coverage. Strategic partnerships with e-commerce platforms and retailers play a key role in strengthening market positioning among logistics providers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Size |

| Aramex | 1982 | Dubai, UAE | ~ | ~ | ~ | ~ | ~ |

| DHL Express | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| FedEx | 1971 | Memphis, USA | ~ | ~ | ~ | ~ | ~ |

| UPS | 1907 | Atlanta, USA | ~ | ~ | ~ | ~ | ~ |

| Emirates Post Group | 1909 | Abu Dhabi, UAE | ~ | ~ | ~ | ~ | ~ |

UAE Last-Mile Delivery Market Analysis

Growth Drivers

Rapid Expansion of E-Commerce Platforms and Online Retail Marketplaces

explanation continues in the same sentence. The rapid expansion of e-commerce platforms across the United Arab Emirates significantly accelerates demand for last-mile delivery services as online retail transactions generate large volumes of parcel shipments requiring fast and reliable distribution networks. Major e-commerce marketplaces including Amazon UAE, Noon, and Namshi process millions of online orders each month, creating sustained demand for logistics providers capable of handling high-frequency deliveries across urban residential areas. Consumers increasingly prefer digital shopping platforms because they provide convenience, competitive pricing, and wider product selection compared to physical retail stores, which further increases parcel delivery volumes across the country’s logistics networks. Retailers invest heavily in digital storefronts, mobile commerce platforms, and integrated payment gateways that encourage consumers to complete purchases through online channels rather than traditional shopping malls. Logistics companies therefore expand distribution infrastructure including micro fulfillment centers, automated sorting facilities, and urban parcel hubs designed to accelerate delivery speed and manage growing order volumes efficiently. Technology integration plays a central role in supporting this growth because route optimization software, artificial intelligence based demand forecasting, and automated fleet management systems help logistics companies improve delivery efficiency while reducing operational costs. E-commerce platforms also implement same-day and next-day delivery service standards that increase pressure on logistics providers to expand delivery capacity and strengthen last-mile infrastructure across major cities. The increasing popularity of cross-border e-commerce imports further contributes to parcel delivery demand because international retailers ship products to UAE consumers through logistics hubs located in Dubai and Abu Dhabi. As online shopping continues to reshape retail consumption patterns across the country, last-mile logistics services become an essential component of the national e-commerce ecosystem.

Growth of Food Delivery and Quick Commerce Platforms

The rapid growth of food delivery and quick commerce platforms significantly drives expansion of the UAE last-mile delivery market as consumers increasingly rely on digital applications to order meals, groceries, and household essentials for immediate home delivery. Major platforms such as Talabat, Deliveroo, Careem, and Noon Food operate large networks of delivery riders capable of fulfilling thousands of orders each day across urban areas including Dubai, Abu Dhabi, and Sharjah. Changing consumer lifestyles characterized by busy work schedules and growing demand for convenience encourage residents to rely on digital food ordering platforms instead of traditional dining or grocery shopping. Restaurants and grocery retailers partner with these platforms to expand their customer reach and increase sales through online ordering channels that provide real-time order tracking and mobile payment systems. Logistics technology including GPS-enabled fleet tracking, AI-driven route optimization, and automated dispatching platforms allows delivery companies to manage high volumes of orders efficiently while ensuring timely deliveries to customers. The quick commerce model further accelerates demand for last-mile logistics because companies promise ultra-fast delivery of groceries and convenience products within short time windows that require dense delivery networks and strategically located micro-warehouses. Retailers invest in dark stores and urban fulfillment hubs designed specifically to support rapid order processing and dispatch operations within densely populated neighborhoods. Delivery service providers also expand fleets of motorbikes and small delivery vehicles that allow riders to navigate urban traffic conditions quickly while maintaining high delivery frequency. As food delivery and quick commerce services continue to expand across the UAE’s urban population centers, the demand for efficient last-mile logistics infrastructure increases significantly.

Market Challenges

High Operational Costs and Urban Delivery Logistics Complexity

The high operational costs associated with maintaining urban delivery networks represent a significant challenge for companies operating in the UAE last-mile delivery market because logistics providers must manage complex delivery operations across densely populated metropolitan environments. Delivery companies incur substantial expenses related to vehicle fleets, fuel consumption, labor wages, warehouse infrastructure, and advanced logistics technologies required to maintain efficient operations. Urban traffic congestion in major cities such as Dubai and Abu Dhabi can significantly increase delivery times and reduce the number of deliveries that drivers can complete within a single shift. Logistics firms must therefore invest in route optimization technologies, real-time traffic monitoring systems, and advanced fleet management software designed to minimize delays and improve delivery efficiency. Labor costs also represent a major operational expense because delivery companies rely on large workforces of drivers and warehouse personnel to manage high parcel volumes. Companies must further allocate resources toward maintaining vehicle fleets, implementing safety standards, and complying with local transportation regulations that govern commercial delivery operations. Rising fuel costs and vehicle maintenance expenses increase the financial burden on logistics companies, particularly those operating large motorbike and van fleets used for urban deliveries. In addition, last-mile delivery companies must invest in secure parcel lockers, micro-fulfillment centers, and urban distribution hubs located close to residential areas in order to maintain rapid delivery service standards demanded by consumers. These infrastructure investments require substantial capital expenditure that may reduce profitability margins for logistics service providers operating within competitive pricing environments.

Regulatory Compliance and Urban Transport Restrictions

explanation continues in the same sentence. Regulatory compliance requirements and urban transportation restrictions create operational challenges for companies involved in last-mile delivery services across the United Arab Emirates because logistics providers must follow strict rules governing commercial vehicle operations, driver licensing, and road safety standards. Government authorities implement transport regulations designed to manage traffic congestion and improve road safety in rapidly growing urban environments. Delivery companies must therefore ensure that their vehicle fleets meet regulatory requirements including vehicle registration standards, emissions compliance rules, and commercial transport licensing conditions. Urban planning authorities in certain districts impose restrictions on commercial delivery vehicles operating within residential areas during peak traffic hours in order to reduce congestion and noise levels. These restrictions may limit the flexibility of logistics providers attempting to complete deliveries within tight time windows demanded by e-commerce retailers and consumers. Companies must also comply with labor regulations governing working hours, employee safety standards, and driver welfare requirements that affect operational scheduling and workforce management strategies. Technology investments are required to maintain compliance with digital documentation systems, vehicle monitoring platforms, and regulatory reporting requirements enforced by transportation authorities. Logistics providers therefore face administrative complexity in addition to operational challenges as they navigate evolving regulatory frameworks that govern commercial delivery operations. Maintaining compliance with these regulations increases operational costs while requiring companies to allocate resources toward legal oversight, compliance monitoring, and driver training programs.

Opportunities

Adoption of Autonomous Delivery Technologies and Drone Logistics Systems

explanation continues in the same sentence. The adoption of autonomous delivery technologies including ground delivery robots and drone logistics systems represents a major opportunity for companies operating in the UAE last-mile delivery market as technological innovation begins to transform urban logistics operations. Technology companies and logistics providers increasingly experiment with autonomous delivery vehicles designed to transport parcels across short distances within residential neighborhoods and commercial districts. Autonomous delivery robots equipped with artificial intelligence navigation systems can travel along sidewalks and pedestrian paths while safely avoiding obstacles and interacting with customers through mobile notification systems. Drone delivery technology also attracts interest from logistics companies because unmanned aerial vehicles can transport small parcels quickly across congested urban environments where road traffic slows traditional delivery vehicles. Government authorities in the United Arab Emirates actively support experimentation with autonomous mobility technologies through regulatory sandboxes and pilot programs that allow companies to test innovative delivery solutions under controlled conditions. Logistics providers invest in research partnerships with robotics developers and aviation technology companies to explore the practical applications of these emerging delivery technologies. Autonomous delivery solutions may significantly reduce labor costs while increasing delivery speed for short-distance shipments within densely populated areas. These technologies also support sustainability objectives because electric-powered robots and drones produce fewer emissions compared to traditional combustion engine delivery vehicles. As technological capabilities continue to advance, autonomous logistics systems could become a transformative component of the UAE’s future last-mile delivery infrastructure.

Expansion of Electric Delivery Vehicle Fleets and Sustainable Logistics Initiatives

explanation continues in the same sentence. The expansion of electric delivery vehicle fleets represents a significant opportunity for logistics providers in the UAE last-mile delivery market as companies increasingly adopt environmentally sustainable transportation solutions that reduce carbon emissions associated with urban logistics operations. Government sustainability strategies encourage the transition toward electric mobility technologies through incentives and infrastructure development programs that support the deployment of electric vehicles across commercial transportation sectors. Logistics companies invest in electric vans, electric motorbikes, and battery-powered delivery vehicles designed specifically for urban logistics operations where short-distance travel and frequent stops characterize delivery routes. Electric delivery vehicles offer lower operating costs compared to traditional fuel-powered vehicles because electricity prices remain more stable than fuel prices and electric drivetrains require less mechanical maintenance. Charging infrastructure expansion across major cities including Dubai and Abu Dhabi supports this transition by allowing logistics providers to recharge fleets at strategically located charging stations throughout the urban transportation network. Retailers and e-commerce platforms increasingly partner with logistics companies that operate environmentally sustainable delivery fleets in order to strengthen corporate sustainability commitments and meet environmental reporting requirements. Electric delivery fleets also contribute to improved air quality within densely populated urban areas where large volumes of delivery vehicles operate daily. As government sustainability policies continue to encourage electric mobility adoption, logistics providers that invest early in electric delivery fleets may gain competitive advantages in the evolving last-mile delivery market.

Future Outlook

The UAE last-mile delivery market is expected to experience strong growth over the next five years driven by continued expansion in e-commerce retailing, quick commerce platforms, and digital logistics technologies. Investments in automated fulfillment centers, AI-driven logistics software, and electric delivery fleets are expected to improve delivery efficiency and sustainability. Government initiatives promoting smart city infrastructure and autonomous mobility technologies will further support logistics innovation. Rising demand for faster delivery services and digital retail transactions will continue to strengthen long-term growth prospects for last-mile delivery providers across the UAE.

Major Players

- Aramex

- DHL Express

- FedEx

- UPS

- Emirates Post Group

- Fetchr

- Jeebly

- Quiqup

- ShipaDelivery

- ZajelCourier Services

- Amazon Logistics

- Careem

- Talabat

- Noon Express

- DTDC Express

Key Target Audience

- Logistics and supply chain companies

- E-commerce retailers

- Food delivery platform operators

- Retail and distribution companies

- Transportation infrastructure developers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Technology andlogisticsplatform providers

Research Methodology

Step 1: Identification of Key Variables

Key variables influencing the UAE last-mile delivery market were identified including e-commerce transaction volumes, parcel delivery demand, logistics infrastructure capacity, delivery fleet expansion, and digital logistics technology adoption across urban retail and logistics networks.

Step 2: Market Analysis and Construction

The market structure was analyzed using secondary data sources, logistics industry reports, government publications, and company disclosures to construct a comprehensive understanding of demand drivers, operational frameworks, and competitive dynamics within the last-mile logistics sector.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, logistics professionals, and supply chain analysts were consulted to validate research assumptions, confirm market trends, and evaluate technological developments influencing delivery networks and urban logistics infrastructure.

Step 4: Research Synthesis and Final Output

Collected data was synthesized using analytical models to produce a structured market assessment including market segmentation, competitive analysis, growth drivers, operational challenges, and future opportunities across the UAE last-mile delivery industry.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid Expansion of E-commerce and Online Retail Platforms

Increasing Consumer Demand for Same Day and On Demand Deliveries

Rising Investments in Urban Logistics Infrastructure and Smart Delivery Technologies

Market Challenges

High Operational Costs for Urban Delivery Networks

Traffic Congestion and Urban Infrastructure Limitations

Complex Logistics Coordination for High Volume Parcel Deliveries - Market Opportunities

Adoption of Autonomous Delivery Vehicles and Drone Logistics

Expansion of Micro Fulfillment Centers in Urban Areas

Growth of Green Logistics and Electric Delivery Fleets - Trends

Integration of AI Driven Route Optimization Technologies

Expansion of Dark Stores and Urban Micro Warehousing

Rising Adoption of Contactless Delivery and Digital Payment Systems - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Parcel Delivery Services

Grocery and Food Delivery Services

Same Day Express Delivery Services

On Demand Courier Delivery Services

Scheduled Delivery Services - By Platform Type (In Value%)

E-commerce Marketplace Platforms

Retail Store Fulfillment Platforms

Food Delivery Aggregator Platforms

Direct Brand Delivery Platforms

Logistics Service Provider Platforms - By Fitment Type (In Value%)

In House Delivery Fleet Operations

Third Party Logistics Delivery Services

Hybrid Fulfillment Delivery Networks

Crowdsourced Delivery Networks

Micro Fulfillment Center Based Delivery - By EndUser Segment (In Value%)

E-commerce Retailers

Food and Grocery Retailers

Healthcare and Pharmaceutical Companies

- Market Share Analysis

- CrossComparison Parameters (Delivery Network Coverage, Fleet Size and Vehicle Mix, Technology Integration, Delivery Speed Capability, Service Pricing Models)

- SWOT Analysis of Key Competitors

Pricing & Procurement Analysis

Porter’s Five Forces

Key Players

Aramex

Emirates Post Group

Fetchr

Careem Now

Talabat

Noon Express

Amazon Logistics

DHL Express

FedEx Express

UPS

JeeblyQuiqup

Shipa Delivery

Zajel Courier Services

DTDC Express

- E-commerce Retailers Driving High Parcel Delivery Volumes

- Food Delivery Platforms Requiring Rapid On Demand Logistics

- Healthcare Providers Demanding Temperature Controlled Medical Deliveries

- Retail Chains Expanding Omnichannel Fulfillment and Home Delivery

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now