Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UAE online insurance market recorded approximately USD ~ billion in digitally distributed gross written premiums based on a recent historical assessment, reflecting the expanding role of direct web platforms, aggregators, and mobile insurance applications in policy issuance. Growth has been driven by high internet penetration exceeding 99 percent of the population and mandatory insurance categories such as motor and health that increasingly migrate to online channels. Insurers and aggregators have accelerated digital onboarding and instant policy issuance systems, expanding the addressable online customer base.

Dubai and Abu Dhabi dominate the UAE online insurance ecosystem due to concentration of insurers, brokers, and insurtech firms alongside advanced digital infrastructure and regulatory sandboxes supporting electronic policy issuance. Dubai’s status as a regional financial and fintech hub has attracted major aggregators and multinational insurers to establish digital distribution centers, while Abu Dhabi’s government-backed health insurance programs and smart services initiatives have accelerated online policy adoption among residents and employers seeking compliant coverage solutions.

Market Segmentation

By Product Type

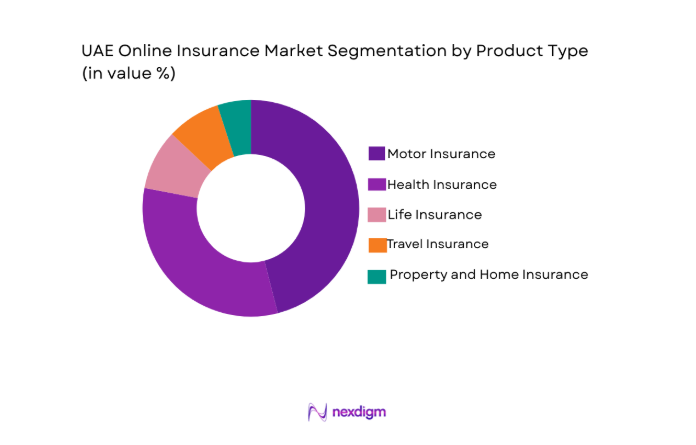

UAE online insurance market is segmented by product type into motor insurance, health insurance, life insurance, travel insurance, and property and home insurance. Recently, motor insurance has a dominant market share due to factors such as mandatory purchase regulations, standardized product structures, strong aggregator comparison capability, and high digital renewal frequency among vehicle owners in urban emirates where online price comparison and instant issuance provide significant convenience and cost transparency advantages.

By Platform Type

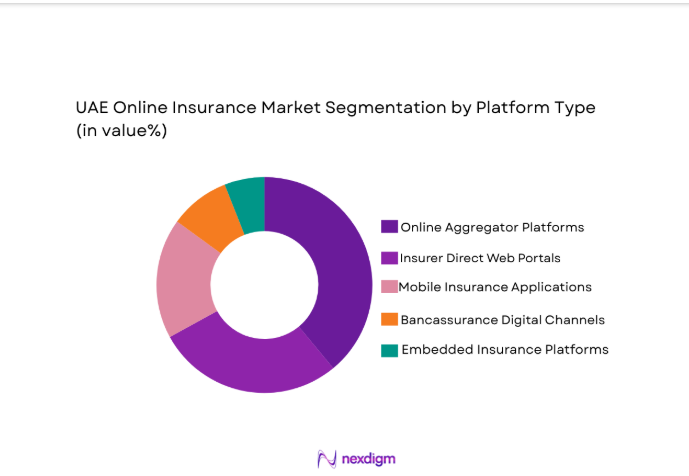

UAE online insurance market is segmented by platform type into insurer direct web portals, mobile insurance applications, online aggregator platforms, bancassurance digital channels, and embedded insurance platforms. Recently, online aggregator platforms have a dominant market share due to factors such as multi-insurer comparison capability, pricing transparency, strong digital marketing reach, and consumer preference for evaluating multiple policy options instantly within a single interface before purchase.

Competitive Landscape

The UAE online insurance market shows moderate consolidation with a mix of regional insurers, digital brokers, and aggregator platforms competing through pricing transparency and digital experience. Aggregators exert strong influence over customer acquisition, while insurers increasingly invest in proprietary digital portals and partnerships with fintech ecosystems to retain margin control. Cross-border insurers and insurtech entrants intensify competition by introducing AI underwriting and instant claims capabilities.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Distribution Model |

| Policybazaar.ae | 2018 | Dubai | ~ | ~ | ~ | ~ | ~ |

| Yallacompare | 2014 | Dubai | ~ | ~ | ~ | ~ | ~ |

| Shory | 2021 | Abu Dhabi | ~ | ~ | ~ | ~ | ~ |

| Sukoon Insurance | 1975 | Dubai | ~ | ~ | ~ | ~ | ~ |

| GIG Gulf | 1962 | Dubai | ~ | ~ | ~ | ~ | ~ |

UAE Online Insurance Market Analysis

Growth Drivers

Mandatory Motor and Health Insurance Digitization Policies

The UAE insurance ecosystem has experienced structural digital acceleration due to regulatory mandates requiring residents and vehicle owners to maintain valid motor and health coverage, which naturally channels high-volume policy categories into online distribution environments where compliance verification and issuance can be automated at scale across insurers and intermediaries. Digital policy issuance frameworks authorized by national regulators have enabled insurers and aggregators to provide legally valid electronic policies, eliminating physical documentation barriers and enabling instant purchase, renewal, and verification through integrated government databases and traffic or health compliance systems used by employers and authorities. The standardized nature of motor and basic health insurance products has allowed aggregators to develop algorithmic comparison engines capable of real-time premium quotation across multiple insurers, improving price transparency and reducing information asymmetry that historically favored intermediaries and offline brokers. Consumers increasingly prefer online renewal channels for mandatory insurance because digital platforms retain prior policy and vehicle or employee data, allowing rapid transaction completion with minimal input, thereby lowering friction and reinforcing repeat usage behavior that sustains channel migration. Employers responsible for workforce health coverage compliance also benefit from digital enrollment and certificate issuance portals that streamline onboarding for expatriate employees, a demographic representing a large share of insured lives in the country and requiring efficient digital processing. Insurers have recognized cost efficiencies in online channels where acquisition expenses and administrative processing are lower than traditional broker commissions and paper-based underwriting, encouraging strategic prioritization of digital distribution for mandatory insurance lines. Government smart services initiatives promoting paperless transactions across public and private sectors have further legitimized digital insurance purchasing behavior and increased consumer trust in electronic documentation and payment mechanisms integrated with national digital identity frameworks. As vehicle ownership and expatriate employment remain structurally embedded in the UAE economic model, the mandatory nature of these insurance classes ensures sustained transaction volumes that continuously reinforce online adoption dynamics.

High Smartphone Penetration and Fintech-Integrated Insurance Distribution

The UAE exhibits one of the world’s highest smartphone penetration rates alongside advanced mobile broadband infrastructure, creating an environment in which financial services consumption, including insurance, naturally transitions toward mobile-first interfaces that enable anytime policy purchase, renewal, and claims initiation across consumer segments accustomed to app-based transactions. Digital banks, payment wallets, ride-hailing platforms, and travel booking ecosystems have begun embedding insurance offerings directly into transaction journeys such as vehicle registration, travel booking, or loan issuance, transforming insurance from a standalone purchase decision into a contextual add-on facilitated through application programming interfaces connecting insurers with fintech platforms. Aggregators and digital brokers leverage targeted digital advertising and search-driven customer acquisition strategies that direct consumers to comparison portals optimized for mobile devices, enabling immediate premium evaluation and purchase without agent interaction, thereby reshaping distribution economics toward performance marketing and data analytics-driven engagement. Younger expatriate professionals and digitally literate residents show strong preference for mobile policy management, including digital storage of insurance certificates, renewal reminders, and instant customer support via chat interfaces, reinforcing habitual reliance on online channels over branch visits or phone-based brokerage. Insurers have invested in cloud-based policy administration systems and eKYC onboarding integrated with national identity verification databases, allowing customers to complete insurance purchase journeys entirely through smartphones without physical documentation submission or in-person verification requirements. The convergence of payments infrastructure with insurance distribution has enabled seamless premium collection via digital wallets and card tokenization, reducing transaction abandonment and supporting recurring policy renewals through automated billing cycles that stabilize online retention rates. Partnerships between insurers and super-apps or e-commerce ecosystems expand insurance visibility within daily digital activities such as mobility or travel planning, increasing exposure frequency and cross-selling potential across previously underpenetrated insurance categories. As digital financial ecosystems deepen across the UAE, insurance increasingly behaves as an embedded financial microservice rather than a standalone product, structurally reinforcing sustained growth in online distribution volumes.

Market Challenges

Consumer Trust Deficit in Fully Digital Insurance Transactions

Despite high digital adoption across financial services in the UAE, insurance purchasing still involves perceived long-term risk transfer and claims reliability considerations that create hesitation among segments unfamiliar with fully online insurers or aggregators, particularly when policy terms are complex or require interpretation beyond price comparison. Many consumers remain uncertain about the credibility of purely digital brokers or newer insurtech platforms relative to established insurers with physical branches, leading to reliance on known brands or offline intermediaries for reassurance regarding claims settlement integrity and regulatory protection. The intangible nature of insurance products intensifies trust sensitivity because customers cannot evaluate product performance until a claim event occurs, making reputation and perceived stability critical factors that digital-only entrants must overcome through branding and partnerships. Aggregator platforms emphasize premium price comparison but may not always communicate nuanced coverage differences clearly, which can lead to post-purchase dissatisfaction or perception gaps when claims outcomes differ from expectations, indirectly affecting confidence in online purchase channels. Language diversity among expatriate populations also creates comprehension challenges when policy wording or digital interfaces are not localized sufficiently, increasing reliance on human assistance rather than self-service digital journeys. Instances of fraudulent online entities or phishing attempts in broader financial services ecosystems further reinforce caution among users when sharing personal or payment information online, even though legitimate insurers operate secure systems. Complex claims processes requiring documentation and assessment sometimes revert customers to offline interaction despite online purchase, creating inconsistency in experience that weakens perception of end-to-end digital reliability. Insurers and regulators continue to address trust gaps through licensing transparency, secure payment frameworks, and consumer awareness campaigns, yet behavioral inertia and risk perception still moderate the pace of migration toward entirely digital insurance engagement.

Fragmented Legacy Systems and Integration Complexity Across Insurers

Many insurers operating in the UAE have historically relied on legacy core systems designed for agent-led distribution and manual underwriting workflows, creating technical constraints when attempting to integrate real-time quotation, policy issuance, and claims functionality with modern aggregator platforms or mobile applications. Differences in data standards, underwriting rules, and product configurations across insurers complicate aggregator integration because comparison engines require standardized digital interfaces to deliver accurate multi-insurer premium results instantly to customers. Insurers must invest significantly in middleware, API development, and cloud migration initiatives to enable seamless digital distribution while maintaining compliance with regulatory reporting and actuarial controls embedded in existing systems. Integration complexity increases operational risk during digital transformation because errors in pricing algorithms or policy issuance workflows can directly affect regulatory compliance or financial exposure, making insurers cautious in accelerating full online automation. Smaller insurers with limited technology budgets may struggle to match the digital capabilities of larger competitors or insurtech entrants, potentially reducing their visibility on aggregator platforms that prioritize insurers capable of real-time integration and instant issuance. Claims management systems often remain partially manual or document-based, limiting insurers’ ability to deliver fully digital post-purchase experiences that customers expect after seamless online acquisition. Data security and privacy requirements under UAE regulatory frameworks add additional layers of technical architecture and audit requirements during system modernization, extending implementation timelines and costs. As a result, uneven digital maturity across insurers constrains uniform online market development and creates variability in customer experience across platforms and providers.

Opportunities

Embedded Insurance Integration Within Digital Commerce and Mobility Platforms

The rapid expansion of digital commerce, travel booking, mobility services, and fintech applications in the UAE creates a structural opportunity to integrate insurance offerings directly into transaction ecosystems where customers already make purchase decisions, transforming insurance from a separate consideration into a contextual add-on seamlessly offered during related financial or consumption activities. Ride-hailing, vehicle leasing, airline booking, and e-commerce platforms can incorporate micro-insurance or mandatory coverage options through API-based connections with insurers, enabling instant policy issuance aligned with the underlying service transaction and reducing customer effort in sourcing coverage independently. Consumers increasingly accept bundled financial services experiences within digital platforms, which lowers psychological barriers to insurance purchase and increases conversion rates relative to standalone insurance portals requiring separate decision processes. Insurers benefit from embedded distribution through reduced customer acquisition costs and access to high-volume transaction flows generated by partner platforms, particularly in segments such as travel, device protection, and mobility-related insurance categories with natural contextual relevance. Data generated within digital platforms also enhances underwriting precision because insurers can access behavioral or transactional insights that improve risk assessment and personalized pricing models compared with traditional demographic-based underwriting approaches. Regulatory openness in the UAE toward fintech partnerships and digital ecosystems supports experimentation with embedded insurance models under controlled frameworks, accelerating market readiness for platform-based distribution architectures. As super-app ecosystems mature in the region, insurance is likely to become a background financial utility integrated across multiple daily activities, significantly expanding online insurance penetration beyond current mandatory categories.

AI-Driven Personalization and Usage-Based Insurance Product Innovation

Advances in artificial intelligence, telematics, and behavioral analytics enable insurers in the UAE to design personalized insurance products priced according to individual risk characteristics or real-time usage patterns, creating differentiated value propositions that align strongly with digital distribution channels capable of capturing and processing customer data efficiently. Motor insurance can incorporate telematics-based driving behavior monitoring through smartphone or vehicle-embedded sensors, allowing dynamic premium adjustment based on actual driving patterns rather than static demographic proxies, which appeals to digitally engaged customers seeking fairness and transparency. Health insurance can leverage wearable device data and digital health engagement metrics to offer wellness-linked incentives or personalized coverage tiers delivered through mobile applications, strengthening customer engagement and retention within online ecosystems. Personalized product configuration tools embedded in digital platforms allow customers to adjust deductibles, coverage modules, and add-ons interactively, improving perceived control and satisfaction compared with standardized offline policies. AI-driven recommendation engines within aggregator or insurer portals can analyze user profiles and prior behavior to suggest optimal insurance bundles, increasing cross-sell success across multiple insurance categories within a single digital journey. Data-centric underwriting models also enable insurers to serve previously underinsured segments such as gig-economy workers or short-term expatriates whose risk profiles do not align with traditional insurance structures but can be assessed dynamically through digital data sources. As customers become accustomed to personalized digital financial products across banking and commerce, expectation for similarly tailored insurance offerings will rise, positioning AI-enabled personalization as a key opportunity driver in the UAE online insurance market.

Future Outlook

The UAE online insurance market is expected to expand steadily as digital financial ecosystems deepen and mandatory insurance categories continue migrating toward fully electronic issuance and renewal. Embedded insurance within mobility, travel, and fintech platforms will broaden distribution reach beyond traditional channels. Advances in AI underwriting and telematics-based pricing will enhance personalization and customer engagement. Regulatory support for e-policies and digital identity will further strengthen consumer trust and operational efficiency across insurers and aggregators.

Major Players

- Policybazaar.ae

- Yallacompare

- Souqalmal

- Shory

- Bayzat

- InsuranceMarket.ae

- Sukoon Insurance

- GIG Gulf

- Daman

- Salama

- Tokio Marine UAE

- Orient Insurance

- Union Insurance

- Noor Takaful

- MetLife Gulf

Key Target Audience

- Insurance companies

- Digital insurance aggregators

- Insurtech platform providers

- Fintech and digital banking firms

- Automotive and mobility platforms

- Healthcare providers and hospital networks

- Investment and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables including digital insurance penetration, mandatory insurance volumes, online distribution share, and platform adoption rates were identified through regulatory data, insurer disclosures, and digital financial ecosystem metrics to define market boundaries and measurement indicators.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed by triangulating insurer premium data, aggregator transaction volumes, and digital policy issuance statistics across product categories and platforms to estimate online distribution contributions within the national insurance sector.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding digital adoption drivers, platform dominance, and consumer behavior were validated through industry expert interviews, insurer technology leaders, and insurtech platform operators to ensure alignment with operational realities and regulatory frameworks.

Step 4: Research Synthesis and Final Output

Validated data and insights were synthesized into structured market estimates, segmentation shares, and competitive mapping, ensuring consistency across sources and alignment with UAE insurance regulatory definitions and digital distribution classifications.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising digital adoption and mobile penetration in financial services

Regulatory encouragement for e-insurance and paperless policies

Growing expatriate demand for convenient insurance purchase

Expansion of insurtech partnerships and aggregators

Cost efficiency benefits for insurers through online distribution - Market Challenges

Consumer trust gaps in fully digital insurance transactions

Complex regulatory compliance across emirates and products

Limited awareness of online insurance options among SMEs

Integration challenges with legacy insurer systems

Price competition compressing digital channel margins - Market Opportunities

Expansion of embedded insurance in e-commerce and fintech ecosystems

AI-based personalized insurance product offerings

Digital health and motor telematics-linked insurance models - Trends

Shift toward aggregator-led policy comparison and purchase

Growth of mobile-first insurance buying behavior

Integration of instant claims submission via apps

Adoption of usage-based and on-demand insurance products

Partnerships between insurers and digital banks or super-apps - Government Regulations & Defense Policy

UAE Insurance Authority digital policy and e-signature regulations

Data protection and cybersecurity compliance mandates

Electronic payment and digital identity regulatory frameworks - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Motor Insurance

Health Insurance

Life Insurance

Travel Insurance

Property and Home Insurance - By Platform Type (In Value%)

Insurer Direct Web Portals

Mobile Insurance Applications

Online Aggregator Platforms

Bancassurance Digital Channels

Embedded Insurance Platforms - By Fitment Type (In Value%)

Fully Online Self-Service Purchase

Assisted Digital Purchase

API-Integrated Embedded Sales

White-Label Partner Integration

Chatbot-Led Sales Interfaces - By End User Segment (In Value%)

Individual Retail Customers

Small and Medium Enterprises

Corporate and Group Clients

Expatriate Population

High-Net-Worth Individuals - By Procurement Channel (In Value%)

Direct Insurer Websites

Insurance Comparison Aggregators

Digital Broker Platforms

Banking and Fintech Apps

Corporate Benefits Portals

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Product Breadth, Pricing Transparency, Claims Turnaround Time, Digital User Experience, Mobile Functionality, Partner Ecosystem Strength, Underwriting Automation Level, Customer Support Channels, Regulatory Compliance Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Policybazaar.ae

Yallacompare

Souqalmal

Shory

Bayzat

InsuranceMarket.ae

Sukoon Insurance

GIG Gulf

Daman

Salama

Tokio Marine UAE

Orient Insurance

Union Insurance

Noor Takaful

MetLife Gulf

- Retail customers prioritize price transparency and instant issuance

- SMEs demand bundled and customizable digital coverage

- Corporates require integrated employee insurance platforms

- Expatriates prefer multilingual and mobile-accessible services

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now