Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UAE Oral Care Market is valued at USD ~ million, based on Nexdigm Research’s country outlook, and is expected to expand with a forecast CAGR of 6.74% for the forecast period, benchmarked against long-range oral care industry growth outlooks. Demand is driven by daily-use toothpaste, premium toothbrushes, alcohol-free mouthwash, whitening products, and dental accessories. The market also benefits from the UAE pharmacy market’s USD ~ million size and strong OTC retail expansion.

Dubai, Abu Dhabi, and Sharjah dominate the UAE Oral Care Market because they concentrate premium retail, pharmacy chains, expatriate households, dental clinics, and e-commerce fulfillment. Abu Dhabi’s population reached 4.14 million, while Dubai added 170,000 residents and reached 3.825 million residents by year-end, supporting frequent replenishment categories such as toothpaste, toothbrushes, mouthwash, floss, and whitening products. Abu Dhabi also leads due to large healthcare spending and institutional dental-care procurement.

Market Segmentation

By Product Type

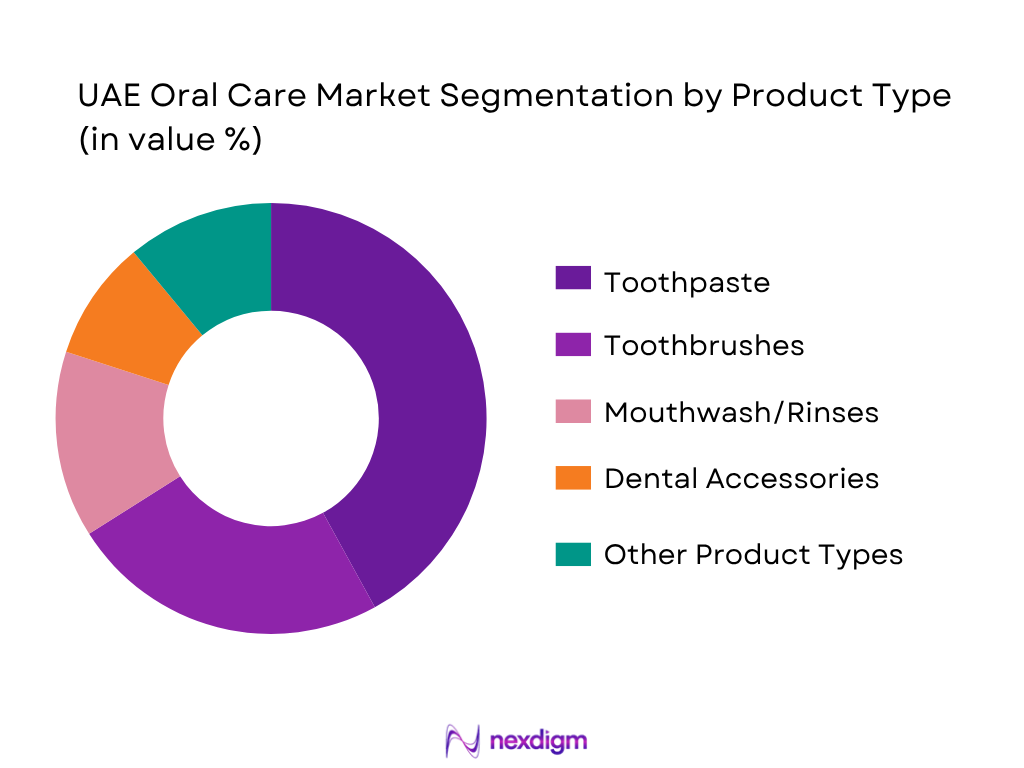

UAE Oral Care Market is segmented by product type into toothpaste, toothbrushes, mouthwash/rinses, dental accessories, whitening products, denture products, and electric oral care devices. Toothpaste holds the dominant market share due to its daily-replenishment nature, broad household penetration, and high SKU depth across sensitivity, whitening, herbal, fluoride, gum-care, and kids variants. The UAE market is highly brand-led, with consumers often trading up from regular toothpaste to sensitivity, enamel-repair, and whitening claims. Pharmacy chains and modern grocery retailers also give toothpaste strong shelf visibility, frequent promotions, and multipack-led value purchasing. Grand View Research identifies toothpaste as the largest revenue-generating UAE oral-care product, while toothbrushes are positioned as a high-growth category due to electric and premium formats.

By Distribution Channel

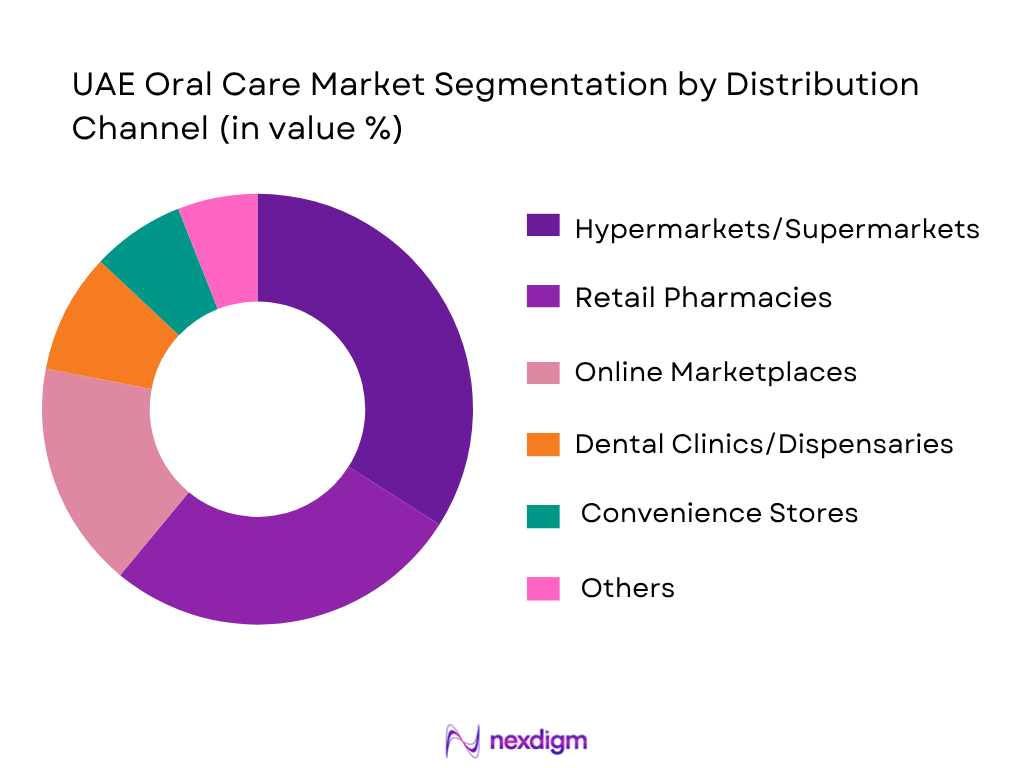

UAE Oral Care Market is segmented by distribution channel into hypermarkets/supermarkets, retail pharmacies, online marketplaces, dental clinics/dispensaries, convenience stores, brand websites, and specialty beauty and personal care stores. Hypermarkets and supermarkets dominate because oral care is purchased as part of recurring household grocery baskets, especially toothpaste, manual toothbrushes, mouthwash, and family packs. Carrefour, Lulu, Spinneys, and Union Coop provide high shelf visibility, price promotions, and multipack availability. Pharmacies remain strategically important for sensitivity toothpaste, medicated mouthwash, interdental products, and dentist-recommended brands. E-commerce is growing rapidly as UAE consumers increasingly buy replenishment healthcare and wellness products online, supported by the country’s fast-growing e-pharmacy channel.

Competitive Landscape

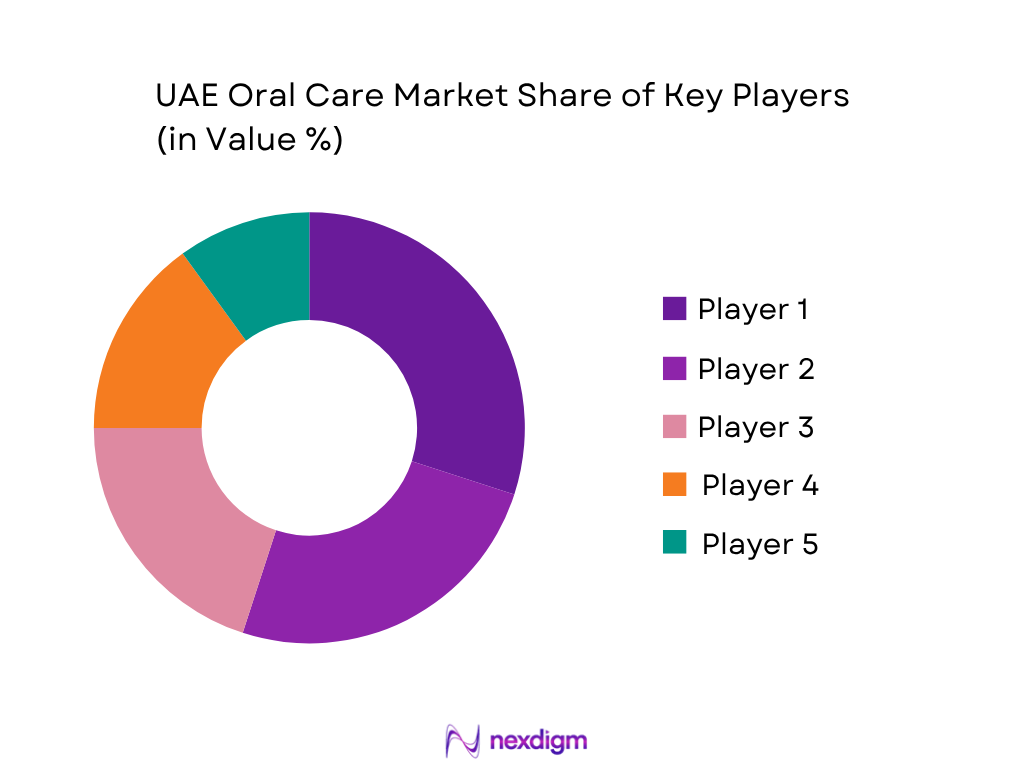

The UAE Oral Care Market is moderately consolidated, with multinational consumer-health and personal-care companies controlling mass and premium categories. Colgate-Palmolive, Procter & Gamble, Haleon, Unilever, Philips, Dabur, Himalaya, and Waterpik compete through pharmacy visibility, modern-trade shelf share, dental-professional recommendations, whitening claims, sensitivity positioning, and online promotional intensity.

| Player | Establishment Year | Headquarters | Core UAE Oral Care Portfolio | Key Positioning | Strongest Channel | Market-Specific Strength | Key Consumer Need Served | UAE Competitive Focus |

| Colgate-Palmolive | 1806 | New York, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Procter & Gamble / Oral-B | 1837 | Cincinnati, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Haleon / Sensodyne | 2022 | Weybridge, UK | ~ | ~ | ~ | ~ | ~ | ~ |

| Unilever | 1929 | London, UK | ~ | ~ | ~ | ~ | ~ | ~ |

| Philips Sonicare | 1891 | Amsterdam, Netherlands | ~ | ~ | ~ | ~ | ~ | ~ |

UAE Oral Care Market Analysis

Growth Drivers

Premiumization

Premiumization in the UAE Oral Care Market is supported by high disposable-income capacity, dense urban consumption, and a strong healthcare-retail environment. The World Bank records UAE population at 11 million and GDP per capita at USD 50,273.51, indicating a consumer base capable of moving beyond basic toothpaste into sensitivity care, whitening toothpaste, alcohol-free mouthwash, interdental brushes, and electric oral care devices. Dubai’s resident population reached 4,248,200, creating a large recurring demand pool for daily oral hygiene products across pharmacies, hypermarkets, and online platforms. The IMF noted UAE real GDP growth at 3.7 and non-hydrocarbon growth at 4.9, reflecting consumer-sector resilience that supports premium personal-care categories. Dubai healthcare expenditure reached AED 24.55 billion, showing broader household and institutional engagement with preventive health, which benefits premium oral care.

Dental Aesthetics

Dental aesthetics is a major growth driver for the UAE Oral Care Market because Dubai and Abu Dhabi combine premium consumers, cosmetic clinics, medical tourism, and a beauty-led retail culture. Dubai welcomed 18.72 million international overnight visitors, above 17.15 million in the previous comparable period, strengthening demand for whitening toothpaste, mouthwash, travel oral-care kits, breath fresheners, electric brushes, and clinic-recommended products. Dubai Health Authority’s investment guide positions Dubai as a healthcare investment hub with advanced infrastructure, while the UAE had 196 internationally accredited healthcare facilities, supporting trust in clinical and cosmetic dental services. Dubai’s healthcare expenditure of AED 24.55 billion further indicates strong healthcare utilization, enabling oral-care brands to align with dentist recommendation, whitening claims, enamel-safe claims, and preventive-care messaging. For oral care, aesthetics-driven demand is especially relevant for whitening, stain removal, gum appearance, fresh breath, and post-treatment maintenance after veneers, aligners, implants, and orthodontics.

Market Challenges

High Import Dependence

High import dependence remains a structural challenge for the UAE Oral Care Market because the country operates as a trade-led consumer market where global brands, imported finished goods, and distributor-led supply chains dominate many FMCG categories. The UAE’s non-oil imports reached AED 1.701 trillion, while total foreign trade reached AED 5.23 trillion, showing the scale of external supply dependence across consumer and industrial goods. WAM reported exports of AED 2.8619 trillion against imports of AED 2.3696 trillion across the broader trade base, confirming the country’s role as both an import and re-export hub. For oral care, this affects toothpaste, electric toothbrushes, replacement heads, mouthwash, dental floss, water flossers, whitening products, and professional clinic-dispensed SKUs. Import dependence increases exposure to shipment lead times, registration requirements, multilingual labelling, distributor availability, and brand-principal decisions. It also makes category planning more dependent on external manufacturing locations rather than domestic production flexibility.

Price Competition

Price competition in the UAE Oral Care Market is intensified by a large organized-retail base, high import availability, and value-conscious replenishment behavior. The macro environment supports strong consumer activity, but it also creates pressure on brands to compete for grocery baskets and pharmacy shelves. UAE inflation was recorded by the World Bank at 1.66337, while the Central Bank of the UAE reported average headline CPI inflation of 2.3 in Q2 and revised its inflation forecast to 1.8, reflecting a controlled but visible consumer-price environment. Dubai’s population base of 4,248,200 and the UAE’s 11 million population create scale, but frequent-purchase categories such as toothpaste and toothbrushes face direct comparison across hypermarkets, pharmacies, and online marketplaces. Imported supply breadth also increases SKU-level substitution between global brands, regional herbal brands, private-label options, and promotional multipacks. For oral-care suppliers, this limits pricing power in mass toothpaste, manual toothbrushes, and standard mouthwash while shifting margin protection toward sensitivity, whitening, dentist-recommended, and electric-device formats.

Market Opportunities

Sensitivity Toothpaste

Sensitivity toothpaste represents a strong future opportunity in the UAE Oral Care Market because it connects daily oral hygiene with preventive healthcare, dentist recommendation, and premium pharmacy purchasing. The UAE’s population of 11 million and GDP per capita of USD 50,273.51 support a consumer base able to pay for condition-specific oral-care products rather than only basic cavity protection. Dubai’s healthcare expenditure reached AED 24.55 billion, and private financing sources including insurance and household payments accounted for AED 15.29 billion, indicating active consumer participation in healthcare spending. This environment supports oral-care brands that position sensitivity toothpaste around enamel protection, gum health, post-whitening care, post-scaling care, and dentist-recommended use. Sensitivity toothpaste also fits pharmacy-led retail because consumers often seek trusted products for pain, discomfort, cold sensitivity, and gum-related concerns. As Dubai and Abu Dhabi continue to expand healthcare access and premium retail formats, sensitivity products can grow through dentist sampling, clinic tie-ups, pharmacy education, and multipack conversion.

Electric Toothbrushes

Electric toothbrushes are a future opportunity in the UAE Oral Care Market because they align with premiumization, preventive care, digital health adoption, and e-commerce-led device purchasing. UAE GDP per capita of USD 50,273.51 supports consumer willingness to adopt rechargeable brushes, sonic brushes, replacement heads, and app-linked oral-care devices. Dubai’s population reached 4,248,200, creating a concentrated urban base for premium devices sold through pharmacies, electronics retailers, online marketplaces, and dental clinics. Dubai welcomed 18.72 million international overnight visitors, increasing exposure to premium grooming and travel-friendly personal-care formats. The UAE’s non-oil economy is supported by IMF-reported growth of 3.7 and non-hydrocarbon growth of 4.9, while Dubai’s healthcare expenditure of AED 24.55 billion shows a strong preventive-health ecosystem. Electric toothbrush adoption is also supported by dentist-led recommendations for plaque control, orthodontic cleaning, gum care, and children’s brushing compliance. The strongest opportunity lies in bundles combining handles, brush heads, toothpaste, floss, and mouthwash through pharmacy and online subscription models.

Future Outlook

The UAE Oral Care Market is expected to maintain steady growth as consumers shift from basic oral hygiene toward preventive, cosmetic, and device-led oral care. Demand will be supported by premium toothpaste, sensitivity products, alcohol-free mouthwash, whitening solutions, electric toothbrushes, and water flossers. Pharmacy-led recommendations, online replenishment, and dental-clinic influence will continue shaping purchase behavior. Dubai and Abu Dhabi will remain the most important commercial hubs because they concentrate premium consumers, dental services, healthcare infrastructure, and organized retail. Growth will also be supported by broader Middle East oral-care momentum, where preventive dental-care awareness and oral-hygiene education are expanding. The Middle East oral care market is projected to grow at 7.61% CAGR, while long-range global oral care forecasts indicate 6.74% CAGR, supporting a favorable benchmark for UAE growth assumptions.

Major Players

- Colgate-Palmolive UAE

- Procter & Gamble UAE

- Haleon / Sensodyne UAE

- Unilever UAE

- Oral-B

- Philips Sonicare

- 3M Medical UAE

- Dabur International

- Himalaya Wellness

- Biofresh Healthcare Products

- Ansar Harford FZC

- Church & Dwight

- Lion Corporation

- Waterpik

- Curaprox

Key Target Audience

- Oral care product manufacturers

- Consumer healthcare companies

- FMCG distributors and importers

- Pharmacy chains and healthcare retailers

- Hypermarket and supermarket chains

- Dental clinic chains and cosmetic dental centers

- Investments and venture capitalist firms

- Government and regulatory bodies (MoHAP, Dubai Municipality, Abu Dhabi Department of Health, Emirates Authority for Standardization and Metrology)

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping the UAE Oral Care Market ecosystem, including manufacturers, importers, distributors, pharmacy chains, hypermarkets, online marketplaces, dental clinics, and regulatory agencies. Variables include product category, SKU pricing, consumer need state, channel penetration, brand availability, and emirate-level demand concentration.

Step 2: Market Analysis and Construction

Historical market data is compiled through secondary sources, retail audits, SKU benchmarking, pharmacy listings, distributor checks, and category-level sales indicators. The market is constructed using both top-down and bottom-up approaches, including product-level pricing, replenishment frequency, channel margins, and oral-care category penetration.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions are validated through interviews with oral-care distributors, retail category managers, pharmacy procurement teams, dentists, and e-commerce sellers. These discussions help refine segment splits, channel contribution, pricing behavior, promotional intensity, and dentist-driven brand preference.

Step 4: Research Synthesis and Final Output

The final phase integrates secondary research, expert inputs, channel checks, and competitive benchmarking. The output is validated against published market-size references, category growth indicators, and UAE-specific retail and healthcare dynamics to produce a structured market report.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Oral Care Category Taxonomy, Abbreviations, Top-Down Market Sizing, Bottom-Up SKU-Level Estimation, Retail Audit Approach, Dental-Clinic Channel Mapping, Primary Interviews with Distributors/Dentists/Retail Buyers, Price Benchmarking, Limitations and Forecast Assumptions)

- Definition and Scope

- Market Genesis

- Evolution of Oral Hygiene Adoption

- Business Cycle

- Supply Chain and Value Chain Analysis

- Demand Ecosystem

- Regulatory Landscape (MoHAP Registration, Emirates Quality Mark, Halal Claims, Fluoride Limits, Cosmetics and Personal Care Labelling, Municipality Approvals)

- Growth Drivers (Premiumization, Dental Aesthetics, Expatriate Population, Oral Hygiene Awareness, Pharmacy Retail Expansion, E-Commerce Penetration, Pediatric Dental Awareness, Dental Tourism)

- Market Challenges (High Import Dependence, Price Competition, Counterfeit Risk, SKU Fragmentation, Regulatory Registration Timelines, Low Flossing Adoption, Private Label Pressure)

- Market Opportunities (Sensitivity Toothpaste, Whitening Kits, Electric Toothbrushes, Water Flossers, Halal/Natural Toothpaste, Kids Oral Care, Subscription Oral Care, Dentist-Recommended Retail Bundles)

- Market Trends (Miswak and Herbal Positioning, Alcohol-Free Mouthwash, Charcoal and Whitening Claims, Sustainable Toothbrushes, Smart Oral Care Devices, Influencer-Led Dental Aesthetics, Pharmacy-Led Premiumization)

- Government and Compliance Analysis(Product Registration, Import Documentation, Labelling in Arabic/English, Halal Certification, Cosmetic Claims Regulation, Dental Clinic Procurement Compliance)

- SWOT Analysis(Product Innovation, Brand Loyalty, Import Reliance, Premium White Space)

- Stakeholder Ecosystem(Brand Principals, Importers, Distributors, Retail Chains, Pharmacies, Dental Clinics, E-Commerce Platforms, Regulatory Bodies)

- Porter’s Five Forces(Brand Intensity, Retail Buyer Power, Substitute Products, New Entrant Threat, Supplier Concentration)

- Pricing and Margin Structure(Importer Margin, Distributor Margin, Retailer Margin, Promotional Discounts, Online Price Undercutting, Clinic Dispensing Margin)

- Route-to-Market Analysis(Principal-to-Distributor, Direct Modern Trade, Pharmacy Chain Distribution, Marketplace Seller Model, Dental Clinic Channel)

- By Value(2020-2025)

- By Volume (2020-2025)

- By Average Selling Price (2020-2025)

- By Per Capita Oral Care Spend (2020-2025)

- By Retail vs Professional Channel Contribution (2020-2025)

- By Product Type (In Value%)

Toothpaste

Toothbrush

Mouthwash/Rinses

Dental Accessories

Denture Products - By Price Positioning (In Value%)

Mass

Mid-Premium

Premium

Professional/Dentist-Recommended

Luxury Cosmetic Oral Care - By Consumer Need State (In Value%)

Cavity Protection

Sensitivity Relief

Whitening/Aesthetics

Fresh Breath

Gum Health

Kids Oral Care

Orthodontic Care

Implant/Denture Care

Natural/Herbal Care - By Age Group (In Value%)

Infants and Toddlers

Children

Teenagers

Adults

Elderly Population - By End User (In Value%)

Homecare Consumers

Dental Hospitals and Clinics

Cosmetic Dental Centers

Pharmacies and Dental Dispensaries

Hospitality and Travel Kits - By Distribution Channel (In Value%)

Hypermarkets/Supermarkets

Retail Pharmacies

Online Marketplaces

Brand Websites

Dental Clinics/Dispensaries

Convenience Stores

Specialty Beauty and Personal Care Stores - By Region/Emirate (In Value%)

Dubai

Abu Dhabi

Sharjah

Ajman

Ras Al Khaimah

Fujairah

Umm Al Quwain - By Ingredient/Claim (In Value%)

Fluoride-Based

SLS-Free

Alcohol-Free

Halal-Certified

Organic/Natural

Vegan

Charcoal-Based

Miswak/Herbal

Enamel-Safe

Dentist-Recommended - By Packaging Format (In Value%)

Tubes

Pumps

Sachets

Bottles

Refills

Blister Packs

Family Packs

Travel Packs

Multipacks

- Market Share of Major Players (By Value, Volume, Product Category, Channel, Price Tier)

- Cross Comparison Parameters(Company Overview, Oral Care Portfolio, Hero SKUs, UAE Distribution Reach, Pharmacy Chain Presence, Hypermarket Shelf Share, E-Commerce Visibility, Dentist Recommendation Strength, Halal/Natural Claims, Whitening/Sensitivity Positioning, Price per Gram/ml, Promotional Intensity, Importer/Distributor Network, Recent Launches, Strengths, Weaknesses)

- SWOT Analysis of Major Players

(Brand Equity, Portfolio Depth, Channel Control, Premiumization Capability, Local Relevance) - Pricing Analysis by SKU (Toothpaste 75ml/100ml/125ml, Toothbrush Single/Multipack, Mouthwash 250ml/500ml, Electric Toothbrush, Water Flosser, Whitening Kit)

- Detailed Profiles of Major Companies

Colgate-Palmolive UAE

Procter & Gamble UAE

Haleon / Sensodyne UAE

Unilever UAE

Oral-B

Philips Sonicare

3M Medical UAE

Dabur International

Himalaya Wellness

Biofresh Healthcare Products

Ansar Harford FZC

Church & Dwight

Lion Corporation

Waterpik

Curaprox

- Demand and Utilization(Brushing Frequency, Mouthwash Usage, Sensitivity Incidence, Whitening Product Adoption, Pediatric Usage)

- Purchasing Power and Basket Analysis(Monthly Oral Care Basket, Premium Toothpaste Spend, Family Multipack Purchase, Online Replenishment)

- Consumer Pain Points(Sensitivity, Gum Bleeding, Bad Breath, Staining, Enamel Erosion, Orthodontic Cleaning, Denture Maintenance)

- Purchase Decision Process(Dentist Recommendation, Retail Promotion, Brand Trust, Halal/Natural Claims, Online Reviews, Price Per Gram/ml)

- Channel Preference Analysis (Pharmacy Trust, Hypermarket Basket Purchase, Noon/Amazon Convenience, Clinic Dispensing, Subscription Models)

- By Value (2026-2035)

- By Volume (2026-2035)

- By Average Selling Price (2026-2035)

- By Premium Product Contribution (2026-2035)

- By Online Channel Contribution (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now