Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UAE Printed Circuit Board market reached approximately USD ~ billion based on a recent historical assessment, supported by electronics manufacturing expansion, telecom infrastructure upgrades, and defense electronics localization initiatives. Demand is driven by rapid deployment of data centers, 5G network rollouts, automotive electronics integration, and industrial automation projects. Increasing local assembly of electronic systems and government-backed industrial diversification strategies have strengthened domestic PCB procurement across telecommunications, aerospace, and industrial electronics sectors.

Abu Dhabi and Dubai dominate the UAE Printed Circuit Board market due to concentration of defense manufacturing zones, aerospace programs, electronics assembly clusters, and advanced industrial infrastructure. Abu Dhabi benefits from defense procurement ecosystems and sovereign industrial initiatives, while Dubai leads through electronics trading hubs, contract manufacturing services, and telecom infrastructure projects. Strong logistics connectivity, free-zone manufacturing incentives, and proximity to regional export markets further reinforce these cities as PCB demand and integration centers across the Middle East electronics value chain.

Market Segmentation

By Product Type:

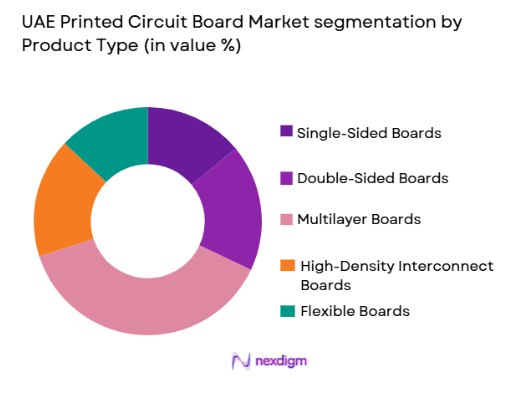

UAE Printed Circuit Board market is segmented by product type into single-sided boards, double-sided boards, multilayer boards, high-density interconnect boards, and flexible boards. Recently, multilayer boards have a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Multilayer PCBs dominate because telecom equipment, defense electronics, and industrial automation systems deployed across the UAE require complex circuitry and high component density. Expansion of 5G base stations, radar electronics, and data center servers has increased multilayer board consumption significantly. Local contract manufacturers prioritize multilayer assembly capability to serve aerospace and telecom clients requiring compact high-performance electronics. Growth in automotive electronics and smart infrastructure projects has also increased multilayer PCB usage for embedded control systems. Additionally, multilayer boards provide superior signal integrity and thermal performance needed in high-frequency communication equipment. These performance advantages and broad application compatibility sustain multilayer PCB leadership across UAE electronics manufacturing and integration sectors.

By End-Use Industry:

UAE Printed Circuit Board market is segmented by end-use industry into telecommunications, aerospace and defense, automotive electronics, industrial electronics, and consumer electronics. Recently, telecommunications has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Telecommunications dominates PCB demand because nationwide 5G deployment, fiber network expansion, and data center construction require high-frequency multilayer boards and HDI circuits. Telecom operators and infrastructure vendors procure large PCB volumes for routers, base stations, switching equipment, and optical transmission hardware. Continuous network upgrades and rising data consumption sustain replacement and expansion cycles of telecom electronics. UAE’s position as a regional digital connectivity hub has accelerated telecom infrastructure investment across mobile, enterprise, and cloud networks. Additionally, smart city and IoT infrastructure programs rely heavily on telecom electronics platforms incorporating advanced PCBs. These structural telecom investments maintain its leadership in PCB consumption across UAE electronics applications.

Competitive Landscape

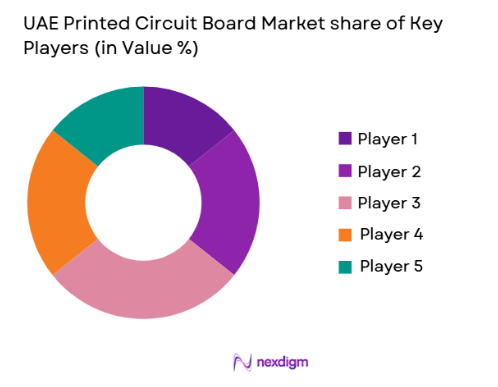

The UAE Printed Circuit Board market shows moderate consolidation, with procurement dominated by international PCB manufacturers supplying through regional distributors and contract manufacturers. Global multilayer and HDI PCB producers maintain strong influence due to advanced technology capabilities and aerospace-grade certifications. Local electronics assemblers depend on established Asian and European PCB suppliers for telecom and defense applications. Strategic partnerships with UAE defense and telecom integrators strengthen supplier positioning, while specialized high-reliability PCB providers hold competitive advantage in aerospace and mission-critical electronics segments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | UAE Market Presence |

| AT&S | 1987 | Austria | ~ | ~ | ~ | ~ | ~ |

| TTM Technologies | 1978 | USA | ~ | ~ | ~ | ~ | ~ |

| Unimicron Technology | 1990 | Taiwan | ~ | ~ | ~ | ~ | ~ |

| Ibiden | 1912 | Japan | ~ | ~ | ~ | ~ | ~ |

| Shennan Circuits | 1984 | China | ~ | ~ | ~ | ~ | ~ |

UAE Printed Circuit Board Market Analysis

Growth Drivers

Telecom Infrastructure Expansion and 5G Network Deployment:

Rapid nationwide deployment of 5G networks and data transmission infrastructure in the UAE is significantly increasing demand for advanced multilayer and high-frequency printed circuit boards across telecom hardware. Telecommunications operators are investing heavily in base stations, fiber backbone upgrades, and cloud data centers, all of which rely on high-performance PCB assemblies. High-speed communication equipment requires low-loss substrates and multilayer routing structures to maintain signal integrity, driving procurement of technologically advanced boards. The UAE’s strategy to become a regional digital connectivity hub has accelerated installation of telecom electronics across urban and industrial zones. Expansion of hyperscale data centers supporting cloud services and AI processing further increases server and switching hardware demand, boosting PCB consumption. Telecom equipment manufacturers and integrators operating in the UAE prioritize high-density and multilayer boards to support miniaturized and energy-efficient electronics. Continuous upgrades to network capacity and latency performance sustain recurring PCB replacement cycles across telecom infrastructure. Growth in IoT connectivity and smart infrastructure platforms also expands telecom electronics deployment requiring specialized PCBs. These structural telecom investments collectively reinforce long-term PCB demand growth across the UAE electronics ecosystem.

Defense Electronics Localization and Aerospace Manufacturing Programs:

The UAE’s strategic focus on domestic defense manufacturing and aerospace capability development is driving strong demand for high-reliability printed circuit boards used in radar, avionics, communication, and mission-critical electronic systems. National industrial programs promoting local defense production have encouraged integration of electronics assembly and PCB sourcing within the country. Aerospace platforms require multilayer and rigid-flex boards capable of operating under extreme temperature, vibration, and electromagnetic conditions, supporting specialized PCB procurement. Expansion of unmanned aerial systems, surveillance equipment, and electronic warfare technologies increases consumption of advanced boards across defense applications. Partnerships between international aerospace companies and UAE defense entities are transferring electronics manufacturing and assembly capability into local facilities. Certification requirements for military-grade electronics favor high-quality PCB suppliers with aerospace compliance, strengthening procurement volumes. Continued investment in space and satellite programs further raises demand for high-reliability PCB technology. Localization incentives and secure supply chain priorities also encourage regional PCB sourcing to reduce dependence on external defense electronics supply. These aerospace and defense manufacturing initiatives significantly reinforce UAE PCB market expansion.

Market Challenges

Dependence on Imported Advanced PCB Technologies and Materials:

The UAE Printed Circuit Board market faces structural challenges due to reliance on imported multilayer PCB fabrication technologies, substrates, and electronic materials from Asia and Europe. Domestic manufacturing capability for high-layer-count and HDI PCB production remains limited, restricting local value addition in electronics supply chains. Telecom and defense electronics integrators often procure advanced boards externally because of technology complexity and specialized fabrication requirements. Import dependence exposes the UAE market to global supply chain disruptions, logistics costs, and geopolitical trade uncertainties affecting electronic components and laminates. Fluctuations in semiconductor and electronics production cycles in supplier countries can delay PCB availability for UAE projects. Local contract manufacturers primarily perform assembly rather than fabrication, constraining domestic PCB industry development. Establishing advanced PCB manufacturing facilities requires high capital investment and technical expertise not yet fully localized. Aerospace and defense certification processes further raise barriers for new local PCB producers. This structural import dependence remains a key constraint on domestic PCB manufacturing growth in the UAE.

Cost Competitiveness Pressure from Established Asian PCB Manufacturing Hubs:

The UAE Printed Circuit Board market encounters strong cost competition from mature PCB manufacturing hubs in Taiwan, China, South Korea, and Southeast Asia, where economies of scale and integrated supply chains reduce production costs. Asian PCB manufacturers benefit from established raw material ecosystems, high-volume fabrication lines, and experienced workforce capabilities that enable competitive pricing. UAE electronics assemblers and telecom integrators often favor imported PCBs due to lower costs compared with potential local production. Limited domestic fabrication scale prevents cost optimization across UAE PCB manufacturing operations. High labor and facility costs within the UAE further challenge price competitiveness relative to Asian producers. Global PCB suppliers with large-scale manufacturing also offer diversified technology portfolios and rapid production turnaround, strengthening their procurement attractiveness. Defense and aerospace electronics demand high-quality boards that established international manufacturers can deliver with proven reliability. Without significant scale and ecosystem integration, UAE PCB fabrication remains economically constrained. Persistent international price competition continues to limit domestic PCB manufacturing expansion in the UAE.

Opportunities

Localization of High-Reliability PCB Manufacturing for Aerospace and Defense:

Expansion of domestic aerospace and defense manufacturing programs in the UAE creates a significant opportunity to localize production of high-reliability printed circuit boards required in mission-critical electronics systems. Defense procurement strategies increasingly prioritize secure regional supply chains and local industrial participation, encouraging investment in specialized PCB fabrication facilities. Aerospace electronics applications demand rigid-flex and multilayer boards capable of operating under harsh environmental conditions, creating demand for technologically advanced manufacturing capability. Establishing certified PCB production aligned with military and aerospace standards would reduce import dependence and strengthen national electronics sovereignty. Partnerships between global PCB manufacturers and UAE defense entities can transfer fabrication expertise and certification processes into local facilities. Growing satellite, unmanned aerial vehicle, and avionics programs further expand domestic demand for aerospace-grade boards. Localization initiatives also align with broader industrial diversification goals aimed at developing high-technology manufacturing sectors. High-reliability PCB production offers potential export opportunities across Middle Eastern defense markets. This strategic localization pathway represents a major growth opportunity for UAE PCB industry development.

Expansion of Electric Mobility and Smart Infrastructure Electronics:

Rapid adoption of electric mobility solutions and smart infrastructure technologies across the UAE presents a strong opportunity for printed circuit board demand growth in automotive electronics and intelligent systems. Electric vehicle charging networks, smart transportation platforms, and connected mobility infrastructure rely on control electronics incorporating multilayer and power PCBs. Automotive electrification increases onboard electronics content including battery management, power conversion, and sensor systems, all requiring advanced boards. Smart city initiatives integrating IoT sensors, traffic control electronics, and digital monitoring systems also expand PCB consumption across infrastructure projects. UAE investments in sustainable transport and urban digitalization are accelerating deployment of intelligent electronics platforms. Local integration of mobility electronics systems encourages PCB sourcing for regional assembly operations. Power electronics and thermal management boards required in EV infrastructure create demand for specialized PCB materials and designs. Growth in autonomous and connected mobility technologies further increases circuit complexity and board density requirements. These electric mobility and smart infrastructure developments create long-term PCB demand expansion opportunities in the UAE market.

Future Outlook

The UAE Printed Circuit Board market is expected to expand steadily over the next five years driven by telecom infrastructure modernization, defense electronics localization, and industrial automation adoption. Increasing investment in data centers, aerospace systems, and smart mobility platforms will sustain demand for advanced multilayer and high-reliability PCBs. Government industrial diversification policies and localization initiatives are likely to encourage regional electronics manufacturing and PCB sourcing. Technological shift toward high-density and thermal-management boards will further shape market evolution.

Major Players

- AT&S

- TTM Technologies

- Unimicron Technology

- Ibiden

- Shennan Circuits

- Zhen Ding Technology

- Tripod Technology

- Compeq Manufacturing

- Nippon Mektron

- Meiko Electronics

- Daeduck Electronics

- Flexium Interconnect

- Career Technology

- Kingboard PCB

- NCAB Group

Key Target Audience

- Telecommunications equipment manufacturers

- Aerospace anddefense contractors

- Automotive electronics manufacturers

- Industrial automation OEMs

- Electronics manufacturing services providers

- Government and regulatory bodies

- Investments and venture capitalist firms

- Data center infrastructure providers

Research Methodology

Step 1: Identification of Key Variables

Key variables such as PCB type demand, telecom infrastructure deployment, defense electronics procurement, and industrial automation adoption were identified. Market drivers, supply chain structure, and technology trends influencing UAE PCB consumption were mapped.

Step 2: Market Analysis and Construction

The UAE PCB market structure was constructed using electronics manufacturing output, telecom equipment deployment, and defense electronics production indicators. Segment shares were derived from application demand distribution and electronics integration patterns.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions were validated through consultation with electronics manufacturing specialists, telecom infrastructure experts, and defense electronics professionals. Technology adoption patterns and procurement trends were cross-verified.

Step 4: Research Synthesis and Final Output

All validated insights were synthesized into market size estimation, segmentation modeling, and trend analysis. Final conclusions were structured to reflect UAE electronics industry dynamics and PCB demand evolution.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of regional electronics manufacturing and assembly ecosystem

Rising telecom infrastructure upgrades and data center deployments

Growth in defense electronics localization initiatives in UAE

Increasing automotive electronics integration in mobility projects

Demand for industrial automation and IoT-enabled equipment - Market Challenges

Limited domestic raw material and laminate production capability

Dependence on imported advanced multilayer PCB technologies

High qualification standards for aerospace and defense applications

Volatility in semiconductor and electronic component supply chains

Cost competitiveness pressure from Asian PCB manufacturing hubs - Market Opportunities

Localization of high-reliability aerospace and defense PCB production

Growth in EV charging and smart mobility electronics infrastructure

Expansion of advanced packaging and HDI PCB manufacturing - Trends

Shift toward high-density interconnect and miniaturized boards

Adoption of lead-free and halogen-free PCB materials

Integration of flexible circuits in wearable and medical devices

Automation and digitalization in PCB fabrication processes

Rising demand for thermal management metal core boards - Government Regulations & Defense Policy

National industrial localization and in-country value programs

Defense electronics manufacturing incentives and partnerships

Environmental compliance and hazardous substance restrictions - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Single-Sided Printed Circuit Boards

Double-Sided Printed Circuit Boards

Multilayer Printed Circuit Boards

High-Density Interconnect Boards

Flexible and Rigid-Flex Boards - By Platform Type (In Value%)

Consumer Electronics Platforms

Industrial Automation Platforms

Automotive Electronics Platforms

Telecom Infrastructure Platforms

Aerospace and Defense Platforms - By Fitment Type (In Value%)

Surface Mount Technology Assemblies

Through-Hole Assemblies

Mixed Technology Assemblies

Embedded Component Boards

High-Reliability Military Grade Boards - By EndUser Segment (In Value%)

Electronics Manufacturing Services Providers

Telecommunications Equipment Manufacturers

Automotive Electronics Integrators

Aerospace and Defense Contractors

Industrial Equipment OEMs - By Procurement Channel (In Value%)

Direct OEM Procurement

Contract Manufacturing Procurement

Government and Defense Tenders

Authorized Electronics Distributors

Project-Based Engineering Procurement - By Material / Technology (in Value %)

FR-4 Epoxy Glass Laminates

Polyimide High-Temperature Substrates

Metal Core Printed Circuit Boards

Ceramic Substrate Boards

Halogen-Free Eco Laminates

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Manufacturing Capability, Technology Complexity, Application Focus, EndUse Industries, Production Scale, Quality Certifications, Localization Presence, R&D Investment, Supply Chain Integration, Cost Competitiveness)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

AT&S

TTM Technologies

Unimicron Technology

Zhen Ding Technology

Compeq Manufacturing

Tripod Technology

Ibiden

Nippon Mektron

Shennan Circuits

Kingboard PCB

Flexium Interconnect

Career Technology

Meiko Electronics

Daeduck Electronics

NCAB Group

- Telecom operators increasing demand for high-frequency multilayer boards

- Defense contractors prioritizing secure domestic PCB sourcing

- Industrial OEMs adopting embedded and high-reliability circuits

- Electronics assemblers expanding SMT-based PCB procurement

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now