Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UAE smart thermometers market is valued at US$ ~ million, up from US$ ~ million in the prior period, based on country-level thermometer revenue tracking. Demand is being pulled by higher outpatient throughput, stricter infection-control practices that favor non-contact measurement, and rising consumer adoption of app-enabled, quick-read devices sold through pharmacies and e-commerce. A fast shift toward mercury-free devices is also supported by clinical preferences and procurement policies.

Within the UAE, Dubai and Abu Dhabi dominate smart thermometer consumption because they concentrate the country’s largest hospital networks, private clinic density, and retail pharmacy footprints—accelerating both institutional procurement and consumer retail sales. Abu Dhabi’s resident base increased from ~ million to ~, while the UAE’s population moved from ~ to ~, expanding the addressable homecare base and chronic-care monitoring need in the most urbanized emirates. These hubs also lead digital-health adoption and medical tourism, which strengthens demand for fast triage tools, including contactless thermometry.

Market Segmentation

By Product Category

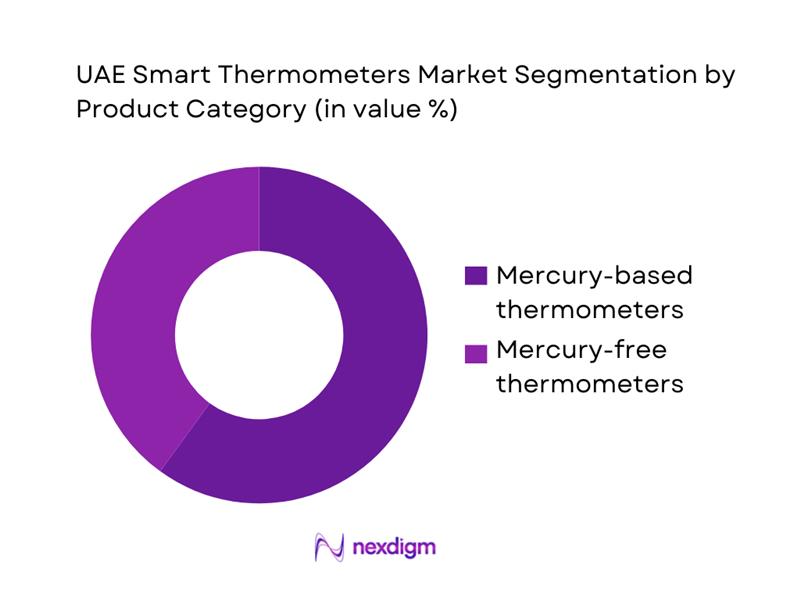

The UAE smart thermometers market is segmented into mercury-based thermometers and mercury-free thermometers. Recently, mercury-based thermometers hold the dominant share because legacy clinical and household usage remains high in price-sensitive channels, supported by habitual purchase behavior and widespread availability across small pharmacies and general trade. At the same time, mercury-free formats are the strategic growth engine as consumers and providers shift toward faster readings, non-contact scanning, and app-connected monitoring features used for family health tracking and remote consultations. This creates a “split market”: incumbency sustains mercury-based volumes, while hospitals, premium pharmacy chains, and e-commerce listings increasingly push mercury-free SKUs. Market momentum is therefore moving toward mercury-free adoption, but the installed base and replacement cycle continue to favor mercury-based products in the current mix.

By Connectivity & Usage Mode

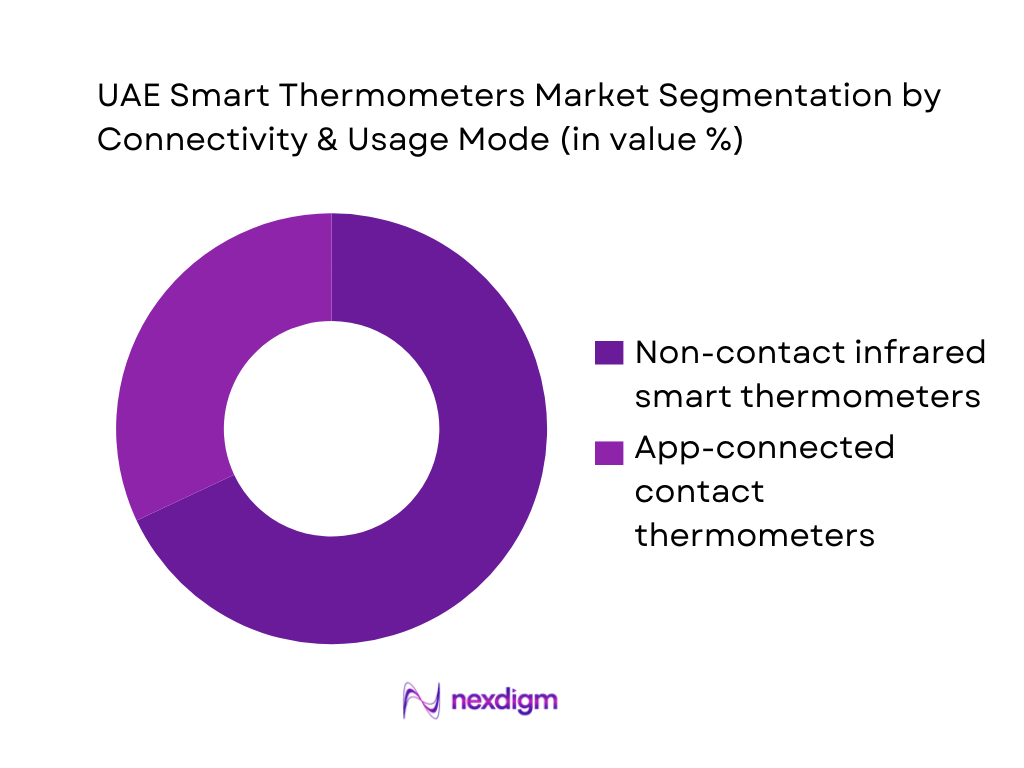

The market is segmented into infrared digital, in-ear, oral/axillary digital, and others. Recently, infrared digital thermometers dominate because they deliver rapid readings, reduce cross-infection risk through non-contact workflows, and fit high-traffic settings such as clinics, emergency triage, and household use during seasonal illness peaks. In UAE retail, consumer preference also leans toward convenience—one-button operation, backlit displays, memory functions, and in premium models, mobile-app logging for family health records. Hospitals and clinics favor IR devices for throughput and standardized screening, while households favor them for ease of use with children and elderly patients. As digital health adoption rises, infrared models also integrate better into remote care pathways where quick symptom checks and longitudinal tracking are preferred.

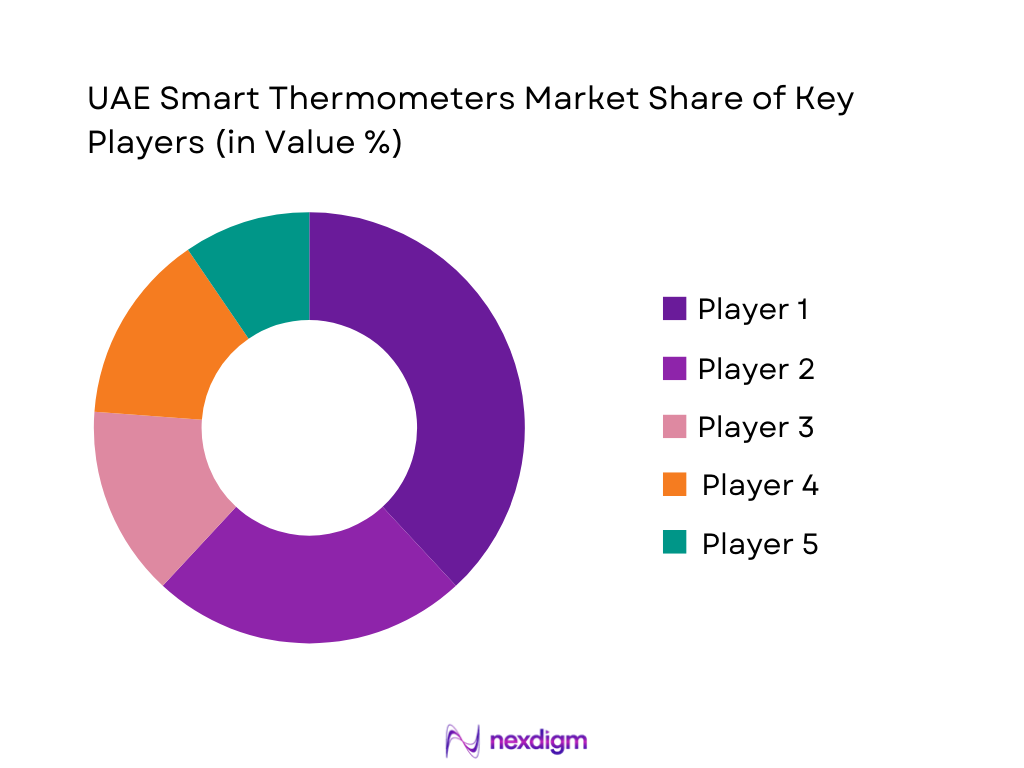

Competitive Landscape

The UAE smart thermometers market is led by a mix of global medical device brands and consumer health electronics players distributed through hospital tenders, local distributors, and pharmacy/e-commerce channels. Competitive advantage is shaped by clinical accuracy claims, speed of reading, non-contact performance, regulatory compliance, warranty/service support in UAE, and breadth of SKU coverage (homecare vs professional).

| Company | Established | Headquarters | Core Thermometer Portfolio | UAE Route-to-Market Strength | Clinical vs Consumer Focus | Smart/App Connectivity | Non-contact IR Range | Warranty/Service Model |

| OMRON | 1933 | Kyoto, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Microlife | 1981 | Taiwan (corporate base) | ~ | ~ | ~ | ~ | ~ | ~ |

| Exergen | 1980 | Watertown, MA, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Welch Allyn (Hillrom/Baxter) | 1915 | Skaneateles Falls, NY, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Braun (Kaz / Helen of Troy) | 1921 | Germany (brand origin) | ~ | ~ | ~ | ~ | ~ | ~ |

UAE Smart Thermometers Market Dynamics

Growth Drivers

Homecare expansion

Home-based monitoring is scaling in the UAE because the clinical ecosystem is large enough to shift routine fever/triage loads away from hospitals while still keeping formal pathways for escalation. The UAE recorded ~ healthcare facilities, ~ operating hospitals, and ~ hospital beds, supported by a human health workforce of ~—creating strong clinical back-up for homecare use-cases like pediatric fever and post-discharge monitoring. In Dubai alone, the regulator licensed ~ home healthcare centres in a single quarter, signalling continued capacity build-out. On the demand side, Dubai hospitals logged ~ patient attendances and ~ accident & emergency visits, which reinforces the operational value of safe home triage tools such as smart thermometers integrated into care protocols. Macroeconomically, the UAE’s GDP (current prices) is USD ~ billion and GDP per capita is USD ~, supporting household spending power and payer capacity for home diagnostics within insured/managed-care pathways.

E-pharmacy penetration

E-pharmacy growth in the UAE is anchored in two measurable enablers: a fast-expanding regulated pharmacy footprint, and high digital access capacity that supports repeat purchases and rapid fulfilment for home diagnostics. Abu Dhabi’s health regulator lists ~ pharmacies operating in the emirate, illustrating dense last-mile availability for device dispensing and after-sales handling. In Dubai, the health authority licensed ~ pharmacies in one quarter, reinforcing continued outlet addition and competitive fulfilment networks that support OTC-like diagnostic purchases. Digitally, the telecom regulator reported ~ internet subscriptions and ~ active mobile subscriptions, which expands the reachable base for app-linked thermometers, e-prescription journeys and delivery tracking. On the consumer-regulatory side, the Ministry of Economy & Tourism recorded ~ complaints received through its e-services platform in a single year—evidence that online commerce issues are being formally routed and resolved, which matters for trust in device purchases. Macroeconomic capacity remains supportive: the UAE’s GDP (current prices) at USD ~ billion sustains logistics investment, while high GDP per capita at USD ~ supports recurring e-pharmacy demand for connected home-monitoring tools.

Challenges

Price competition

Price-led competition is structurally intense in the UAE because distribution density is high, new licences keep expanding the retail footprint, and public-sector oversight is active—pushing brands to defend value through accuracy, connectivity and service rather than premium pricing alone. Abu Dhabi alone lists ~ pharmacies, creating heavy SKU competition and frequent substitution pressure for OTC-like devices. In Dubai, the health regulator licensed ~ pharmacies in a single quarter, and also licensed ~ outpatient clinics and ~ home healthcare centres, expanding the number of procurement points that can compare suppliers. Nationally, the ecosystem scale is large: ~ healthcare facilities and ~ health workforce increase the number of channels where competitive tenders, rebates (non-price elements), and private-label strategies can emerge. From a macro lens, the UAE’s GDP (current prices) at USD ~ billion supports a large consumer market, but it also attracts many importers and brands into a relatively concentrated geography—intensifying shelf competition. With GDP per capita at USD ~, consumers can pay for quality, but they also have the purchasing power to switch quickly across brands and channels, sustaining ongoing price pressure.

Counterfeit and grey imports

Counterfeit/grey imports are a practical risk for smart thermometers in the UAE because the country is a high-throughput trading hub and consumers increasingly purchase devices through multi-merchant online channels. Enforcement data shows the scale: Dubai Customs recorded ~ seizures involving ~ counterfeit items in one year, and separately reported ~ intellectual property seizures valued at AED ~ million, indicating sustained counterfeit interception activity across categories that include electronics and other fast-moving consumer goods. On the regulatory side, the UAE’s Federal Decree-Law No. ~ explicitly defines “Grey Market” circulation and extends inspection reach into ports/logistics centers, reflecting heightened controls over non-authorised channels. This matters for thermometers because counterfeit devices often fail accuracy expectations, undermine trust in connected readings, and increase returns. Macro context supports why this remains persistent: a GDP (current prices) of USD ~ billion aligns with high volumes of imported consumer and healthcare goods, while the UAE’s global aviation role amplifies cross-border flows that illicit traders try to exploit.

Opportunities

Hospital-to-home pathways

The strongest near-term opportunity for UAE smart thermometers is deeper integration into hospital-to-home pathways, because the country’s measured inpatient and outpatient volumes create a large “transition” pool where remote temperature logging reduces readmissions and unnecessary returns to emergency care. Nationally, hospitals recorded ~ admitted patients and ~ hospital days of stay, while government health centers recorded ~ visitors—a large base of patients moving between facility-led care and community follow-up. These volumes make structured discharge packs (including connected thermometers) operationally attractive, especially for post-infectious recovery, pediatric fever monitoring, and homecare nursing visits. Dubai’s regulator licensed ~ home healthcare centres in a single quarter, signalling expanding delivery capacity for at-home monitoring and escalation protocols. Macro capacity remains supportive: the UAE’s GDP (current prices) is USD ~ billion, enabling investment into digital discharge, care coordination and insurer-driven home monitoring programmes, while GDP per capita of USD ~ supports demand for reliable, clinician-aligned home diagnostics without needing future projections to justify adoption.

Bundled vitals kits

Bundling smart thermometers into “vitals kits” (temperature + BP + SpO₂ where clinically appropriate) is an opportunity in the UAE because the country has the digital access base and the pharmacy/service density to distribute kits at scale, while high utilisation volumes support repeat use in families and chronic-care households. The telecom regulator reports ~ active mobile subscriptions and ~ internet subscriptions, which supports app-based dashboards and caregiver sharing across multiple devices. The healthcare delivery base is also large: ~ healthcare facilities and ~ health workforce increase the number of touchpoints that can recommend bundled monitoring for home follow-up, especially after clinic visits or during seasonal infection peaks. Channel availability is strong: Abu Dhabi lists ~ pharmacies, creating broad shelf presence and fulfilment capacity for kits (including replacements and warranties). Macro indicators support consumer readiness for “bundle convenience”: GDP per capita at USD ~ aligns with higher adoption of integrated home-monitoring ecosystems, while a USD ~ billion economy sustains investment in connected-health platforms that make multi-parameter kits more useful than standalone devices.

Future Outlook

Over the next five to six years, the UAE smart thermometers market is expected to expand steadily as mercury-free adoption rises, non-contact screening becomes routine in more care pathways, and consumers increasingly buy connected home-health devices through e-commerce and organized pharmacy chains. The market’s ~ value is US$ ~ million and the forecast implies a ~ CAGR. Growth will also be supported by population expansion in major emirates, continued investment into digital health, and higher chronic-disease monitoring intensity that increases household readiness to adopt multi-parameter home monitoring bundles (BP + glucose + temperature).

Major Players

- OMRON

- Microlife

- Exergen

- Welch Allyn

- 3M

- Medtronic

- Terumo

- Medline Industries

- Briggs Healthcare

- Braun

- Withings

- iHealth

- Beurer

- Rossmax

Key Target Audience

- Procurement heads

- Procurement heads

- Category heads

- Heads of e-commerce marketplace health categories

- Medical device distributors and channel partners

- Health insurance provider network strategy teams

- Corporate wellness and occupational health program heads

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

We build a UAE ecosystem map covering manufacturers, importers, distributors, pharmacies, e-commerce channels, and provider procurement. Desk research consolidates regulatory pathways, product definitions (smart/digital/IR), pricing tiers, and key demand drivers to define variables influencing sales velocity and adoption.

Step 2: Market Analysis and Construction

We compile historical revenue datapoints, triangulating country-level thermometer market sizing with category-level splits (product type, use-case orientation, and channel structure). We assess UAE demand anchors (homecare vs clinical procurement) and validate consistency against supplier and channel signals.

Step 3: Hypothesis Validation and Expert Consultation

We validate hypotheses through structured expert interviews with distributors, pharmacy category managers, hospital procurement teams, and clinician users. Discussions focus on purchase criteria, tender dynamics, preferred device types, accuracy expectations, warranty/service frictions, and switching triggers.

Step 4: Research Synthesis and Final Output

We synthesize findings using a bottom-up view (SKU presence, channel economics, procurement patterns) and reconcile with top-down country sizing. Outputs are reviewed for internal consistency, with assumptions documented and sensitivities highlighted for “smart-only” splits.

- Executive Summary

- Research Methodology (Market definitions and scope boundaries, smart thermometer taxonomy, assumptions & exclusions, abbreviations, data triangulation framework, market sizing logic, bottom-up SKU/channel build, top-down healthcare spending linkage, primary interviews mix, validation checks, limitations)

- Definition and Scope

- Market Genesis and Adoption Curve

- Evolution of Use-Cases

- Business Cycle and Seasonality

- UAE Go-to-Market Structure

- Growth Drivers

Homecare expansion

E-pharmacy penetration

Pediatric demand

Rapid screening needs

Connected health adoption - Challenges

Price competition

Counterfeit and grey imports

Calibration and accuracy trust

Regulatory documentation burden

Returns and warranty costs - Opportunities

Hospital-to-home pathways

Bundled vitals kits

Maternity and baby ecosystems

Employer health programs

Travel retail partnerships - Trends

Contactless preference

Multi-user apps

Fever tracking analytics

Multilingual UX

Subscription add-ons - Regulatory & Policy Landscape

- SWOT Analysis

- Stakeholder & Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competitive Intensity & Ecosystem Mapping

- By Value, 2019–2024

- By Volume, 2019–2024

- By Average Selling Price, 2019–2024

- Installed Base and Replacement Cycle, 2019–2024

- By Technology Architecture (in Value %)

No-touch infrared

Contact digital

In-ear

Temporal artery/forehead

Smart wearables/patch thermometers - By Connectivity Type (in Value %)

Standalone

Bluetooth

Wi-Fi

App-enabled

Cloud-linked family profiles - By End-Use Industry (in Value %)

Households

Hospitals and clinics

Pharmacies

Schools and education

Corporates and industrial sites

Hospitality and aviation - By Distribution Channel (in Value %)

Retail pharmacy chains

Independent pharmacies

E-commerce marketplaces

Hospital procurement and tenders

Electronics retailers - By Region (in Value %)

Dubai

Abu Dhabi

Sharjah

Northern Emirates

Free Zones and institutional clusters - By Price Band (in Value %)

Entry

Mid

Premium

- Market Share of Major Players

Cross Comparison Parameters (Product portfolio breadth, Measurement accuracy and evidence, Connectivity and app ecosystem, Regulatory readiness and certifications, Pricing architecture in AED, Distribution reach and availability, After-sales and warranty service network, Partnerships and institutional penetration) - Competitive Positioning Matrix

- Pricing Analysis

- Strategic Moves and Recent Developments

- Detailed Profiles of Major Companies

Braun

Omron

Beurer

Withings

iHealth

Microlife

Exergen

Welch Allyn

Rossmax

Berrcom

B.Well

Geratherm

Trister

Accurete

- Household Buyer Journey

- Hospital and Clinic Procurement

- Pharmacy Channel

- Corporate and School Screening Use

- Decision-Making Unit Map

- By Value, 2025–2030

- By Volume, 2025–2030

- By Average Selling Price, 2025–2030

- Installed Base and Replacement Cycle, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now