Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UAE Truck Aggregator market reached approximately USD ~ billion based on a recent historical assessment, supported by rapid digitalization of freight brokerage, rising SME participation in logistics platforms, and strong non-oil trade flows exceeding USD ~ billion through national ports and free zones. Expansion of e-commerce distribution networks and construction supply chains has increased reliance on on-demand trucking marketplaces, while government smart logistics initiatives and high smartphone penetration have accelerated adoption of aggregator platforms among fleet owners and shippers.

Dubai and Abu Dhabi dominate the UAE Truck Aggregator market due to concentration of logistics infrastructure, industrial zones, and international trade gateways. Dubai’s Jebel Ali Port handled cargo volumes exceeding USD ~ billion in trade value, supporting dense freight movements and platform adoption among transport brokers and SMEs. Abu Dhabi’s Khalifa Industrial Zone and energy logistics corridors generate consistent bulk trucking demand. Strong road connectivity between emirates and cross-border GCC trade routes further reinforce these cities as aggregator activity hubs.

Market Segmentation

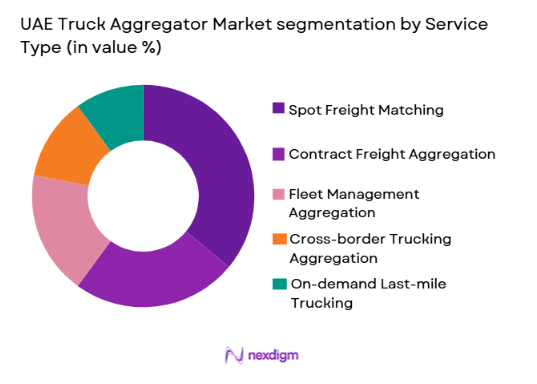

By Service Type

UAE Truck Aggregator market is segmented by service type into spot freight matching, contract freight aggregation, fleet management aggregation, cross-border trucking aggregation, and on-demand last-mile trucking. Recently, spot freight matching has a dominant market share due to factors such as volatile shipment demand, SME shipper preference for flexible pricing, and high prevalence of fragmented owner-operator fleets requiring real-time load access. Growth in e-commerce replenishment shipments and construction material transport has intensified short-term booking patterns. Aggregator platforms offering dynamic pricing and instant truck availability have captured majority transactional volumes, especially in urban logistics corridors and port-linked freight movements.

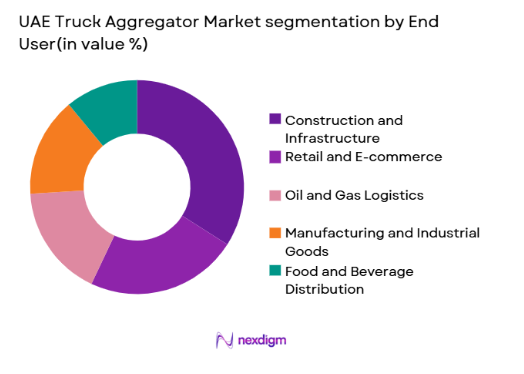

By End-User

UAE Truck Aggregator market is segmented by end-user into construction and infrastructure, retail and e-commerce, oil and gas logistics, manufacturing and industrial goods, and food and beverage distribution. Recently, construction and infrastructure has a dominant market share due to factors such as continuous project logistics demand, bulk material movement requirements, and geographically dispersed construction sites across emirates. Aggregator platforms enable contractors to secure flexible truck capacity for cement, steel, and aggregates transport without owning fleets. Large-scale urban development and industrial expansion have sustained heavy truck utilization, reinforcing construction sector dependence on digital freight aggregation solutions.

Competitive Landscape

The UAE Truck Aggregator market is moderately consolidated with a mix of regional digital freight platforms and logistics technology firms competing on fleet coverage, pricing algorithms, and cross-border capability. Leading Growth-stage aggregators dominate SME shipper acquisition and urban freight matching volumes, while integrated logistics players leverage existing transport networks and enterprise contracts. Technology differentiation through telematics integration, real-time tracking, and AI pricing engines is shaping competitive positioning, and consolidation is emerging through partnerships with ports, free zones, and logistics service providers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Integration Depth |

| Trukker | 2016 | UAE | ~ | ~ | ~ | ~ | ~ |

| Fetchr Logistics | 2012 | UAE | ~ | ~ | ~ | ~ | ~ |

| Shyft | 2017 | UAE | ~ | ~ | ~ | ~ | ~ |

| LoadMe | 2019 | UAE | ~ | ~ | ~ | ~ | ~ |

| Jeebly Logistics | 2016 | UAE | ~ | ~ | ~ | ~ | ~ |

UAE Truck Aggregator Market Analysis

Growth Drivers

Digitalization of SME Freight Procurement and Spot Logistics Adoption:

Digitalization of SME freight procurement and spot logistics adoption is accelerating UAE Truck Aggregator market expansion as small and medium shippers increasingly prefer on-demand trucking access rather than fixed fleet ownership. The UAE hosts over 557,000 SMEs generating major domestic trade flows, and many rely on aggregators to secure flexible transport capacity across emirates and free zones. Aggregator platforms reduce empty backhauls and transaction costs, improving fleet utilization and shipper efficiency simultaneously. Real-time price discovery and instant booking enable SMEs to manage shipment variability tied to retail cycles and project logistics. Government digital economy programs and widespread smartphone penetration exceeding 95% have lowered adoption barriers among drivers and brokers. Aggregators also provide digital documentation and payment settlement, replacing manual brokerage processes historically prevalent in fragmented trucking markets. Integration with warehouse management and e-commerce fulfillment systems has further embedded aggregators in SME supply chains. As logistics digitization continues across trade and distribution sectors, SME participation remains a structural demand driver for aggregator platforms.

Infrastructure Expansion and Cross-Emirate Trade Corridors:

Infrastructure expansion and cross-emirate trade corridors are strengthening UAE Truck Aggregator market growth by increasing freight movements requiring flexible trucking capacity. The UAE logistics sector handles trade flows exceeding USD 600 billion annually across ports, industrial zones, and free trade hubs, creating continuous road freight demand between emirates. Major infrastructure programs including industrial corridors, logistics parks, and construction megaprojects generate sustained bulk material transport needs. Aggregator platforms enable contractors and suppliers to access trucks rapidly across geographically dispersed project sites without maintaining fleets. Cross-emirate highways and GCC land trade routes support high truck utilization, favoring digital freight matching for return loads. Logistics hubs such as Jebel Ali and Khalifa Port create dense freight clustering that benefits aggregator marketplaces connecting multiple shippers and carriers. Government investment in smart logistics and transport digitization further encourages platform adoption. As infrastructure and trade connectivity expand, trucking demand variability increases, reinforcing aggregator usage for capacity balancing and route optimization.

Market Challenges

Fragmented Fleet Ownership and Driver Digital Adoption Barriers:

Fragmented fleet ownership and driver digital adoption barriers constrain UAE Truck Aggregator market efficiency because the majority of trucks are owned by small operators with limited technology familiarity. Many drivers lack digital literacy or incentives to consistently use aggregator applications, reducing platform liquidity and real-time capacity visibility. Traditional brokerage relationships remain entrenched in certain freight segments, limiting platform penetration. Device costs, data connectivity issues in remote routes, and language diversity among drivers also hinder adoption. Aggregators must invest heavily in onboarding, training, and support to build supply-side participation. Inconsistent digital usage results in unreliable truck availability data, affecting shipper trust and pricing accuracy. Cash-based transactions still persist in parts of the trucking ecosystem, complicating digital payment integration. Regulatory requirements for licensing and compliance vary across emirates, adding onboarding complexity. Until fleet digitization reaches critical mass, aggregators face structural friction in scaling network effects and matching efficiency.

Freight Price Volatility and Platform Margin Compression:

Freight price volatility and platform margin compression challenge UAE Truck Aggregator market profitability due to fluctuating trucking demand tied to construction cycles, trade flows, and fuel costs. Spot freight rates can vary significantly across seasons and routes, complicating pricing algorithm stability and revenue predictability for aggregators. Shippers frequently compare multiple platforms, intensifying price competition and reducing commission margins. Aggregators often subsidize pricing or incentives to acquire carriers and shippers, raising operating costs. Fuel price variability directly affects driver pricing expectations and platform rate consistency. Construction and infrastructure project cycles create demand spikes followed by slowdowns, producing uneven platform transaction volumes. Cross-border trucking regulations and delays also influence route pricing unpredictably. Competitive entry of new digital logistics startups further pressures commissions. Sustained margin compression limits aggregator investment capacity in technology, marketing, and fleet onboarding, slowing long-term market maturation.

Opportunities

Integration with Port, Free Zone, and Industrial Logistics Ecosystems:

Integration with port, free zone, and industrial logistics ecosystems presents significant opportunity for UAE Truck Aggregator market expansion by embedding platforms into high-volume freight nodes. The UAE hosts over 40 free zones and multiple mega ports generating dense trucking demand for container drayage and industrial shipments. Aggregators integrated with terminal booking systems and warehouse platforms can secure recurring freight flows and enterprise clients. Digital gate scheduling, yard management, and container tracking integration improves truck turnaround efficiency. Logistics park operators increasingly seek digital transport orchestration tools to manage tenant freight movements. Aggregators providing API connectivity to port and zone systems can become preferred capacity providers. Such integration also enhances regulatory compliance and documentation workflows. Concentrated freight demand in these ecosystems enables scale economics and route optimization. As ports and zones digitize operations, aggregator partnerships create long-term transactional stability and revenue growth.

AI-Driven Dynamic Pricing and Predictive Freight Matching:

AI-driven dynamic pricing and predictive freight matching offer transformative opportunity for UAE Truck Aggregator market by improving pricing accuracy, capacity utilization, and network efficiency. Freight demand in the UAE varies by corridor, project activity, and trade cycles, creating ideal conditions for predictive analytics. AI models can forecast shipment demand, recommend pricing, and optimize route allocation to minimize empty miles. Real-time telematics and GPS data enable continuous fleet visibility and algorithm learning. Dynamic pricing enhances shipper cost transparency while protecting carrier margins. Aggregators deploying advanced analytics can differentiate through superior matching speed and reliability. Predictive demand insights also support fleet planning and cross-border load balancing. As data volume grows with platform usage, algorithm performance compounds competitive advantage. AI-enabled optimization thus represents a major pathway for scaling profitability and service quality in digital trucking aggregation.

Future Outlook

The UAE Truck Aggregator market is expected to expand steadily over the next five years, supported by continued logistics digitization, infrastructure development, and growth in non-oil trade flows. Increasing integration with ports, free zones, and enterprise supply chains will stabilize platform demand. Advancements in AI-based pricing, telematics, and real-time freight visibility will enhance efficiency and adoption. Government smart mobility initiatives and cross-border GCC logistics harmonization will further accelerate digital trucking aggregation across the region.

Major Players

- Trukker

- Fetchr Logistics

- Shyft

- LoadMe

- Jeebly Logistics

- Cargoz

- Fleetroot

- Maqta Gateway Logistics Platforms

- Nowports MENA

- Bayan Logistics Technologies

- Transcorp Logistics Platforms

- EFS Facilities Logistics Solutions

- GWC Digital Logistics

- TruckIt

- Fretello Logistics

Key Target Audience

- Logistics platform investors

- Freight and trucking companies

- E-commerce fulfillment operators

- Construction logistics providers

- Port and free zone authorities

- Retail and distribution enterprises

- Supply chain technology vendors

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Demand indicators such as freight volumes, SME logistics adoption, and infrastructure activity were mapped. Supply variables including fleet size, aggregator penetration, and digital platform usage were identified across UAE logistics corridors.

Step 2: Market Analysis and Construction

Market size was constructed using trade flow values, trucking utilization metrics, and digital freight penetration rates across emirates. Segment shares were derived from transaction patterns across service types and end-user industries.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through interviews with logistics operators, platform providers, and fleet owners across UAE freight corridors. Assumptions on pricing, adoption, and demand drivers were refined using industry feedback.

Step 4: Research Synthesis and Final Output

Validated data was synthesized into market models and segment structures. Competitive mapping, growth drivers, and outlook trends were developed to produce final analytical insights and forecasts.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid e-commerce and retail distribution expansion

Infrastructure and construction freight demand growth

Digitalization initiatives in UAE logistics sector

SME adoption of on-demand transport platforms

Cross-border GCC trade facilitation policies - Market Challenges

Fragmented trucking fleet ownership structure

Driver and fleet digital adoption gaps

Pricing volatility in spot freight markets

Regulatory compliance across emirates

Platform competition and margin pressure - Market Opportunities

Integration with port and free zone logistics systems

AI-driven dynamic freight pricing adoption

Expansion into cross-border GCC aggregation - Trends

Shift toward real-time freight visibility platforms

Growth of asset-light digital logistics models

Telematics-driven fleet performance analytics

API integration with enterprise supply chains

Adoption of predictive demand matching - Government Regulations & Defense Policy

UAE digital transport and smart mobility policies

Freight licensing and fleet compliance frameworks

Cross-emirate and GCC logistics harmonization - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Digital Freight Matching Platforms

On-demand Truck Booking Apps

Fleet Aggregation Management Systems

Enterprise Freight Exchange Platforms

Cross-border Load Matching Systems - By Platform Type (In Value%)

Mobile-based Aggregation Platforms

Web-based Freight Marketplaces

API-integrated Logistics Platforms

Cloud-native Aggregator Platforms

Telematics-enabled Aggregation Platforms - By Fitment Type (In Value%)

Third-party Logistics Integrated

Standalone Aggregator Platforms

Embedded OEM Logistics Solutions

Marketplace-integrated Systems

Broker-assisted Aggregation Models - By EndUser Segment (In Value%)

SME Shippers and Traders

Large Enterprise Logistics Buyers

E-commerce and Retail Distributors

Construction and Industrial Firms

Freight Forwarders and 3PLs - By Procurement Channel (In Value%)

Direct Platform Subscription

Broker-mediated Onboarding

Enterprise Contract Procurement

Government Logistics Tenders

Partner Logistics Integrations - By Material / Technology (in Value %)

AI-based Load Optimization Algorithms

Telematics and IoT Tracking Modules

Cloud-native Microservices Architecture

Blockchain Freight Documentation

Predictive Pricing Engines

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Platform Scalability, Fleet Coverage, Pricing Model Flexibility, Real-time Tracking Capability, API Integration Depth, Cross-border Operations, AI Optimization Level, Customer Segment Focus, Telematics Integration, Regulatory Compliance Support)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Trukker

Fetchr Logistics

Shyft

LoadMe

TruckIt

Jeebly

Fretello Logistics

Nowports MENA

Maqta Gateway Logistics Platforms

Cargoz

Bayan Logistics Technologies

Fleetroot

Transcorp Logistics Platforms

EFS Facilities Logistics Solutions

GWC Digital Logistics

- SMEs leveraging aggregators to reduce empty miles and costs

- E-commerce firms prioritizing real-time truck availability

- Construction sector requiring flexible bulk transport capacity

- 3PLs integrating aggregators for capacity scaling

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now