Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UAE Used Tractor market current size stands at around USD ~ million, reflecting steady transactional activity across refurbishment yards, dealer-certified resale programs, and owner-to-owner transfers. Demand is sustained by equipment replacement cycles in commercial farming and contracting, while inbound flows of pre-owned units support fleet availability. Pricing dispersion remains wide due to condition variance, hours of use, and retrofit status. After-sales services, parts availability, and refurbishment standards increasingly shape buyer preferences and transaction velocity across resale channels.

Demand concentration is highest in Abu Dhabi and Al Ain due to large-scale farms and contracting clusters, while Sharjah and Ras Al Khaimah host dense reseller yards and logistics access. Dubai acts as a trading and financing hub supporting cross-emirate transactions. Ecosystem maturity is reinforced by port connectivity, warehousing, inspection facilities, and service workshops. Policy emphasis on food security, municipal landscaping, and infrastructure maintenance supports sustained utilization across emirates without concentrating transactions in a single geography.

Market Segmentation

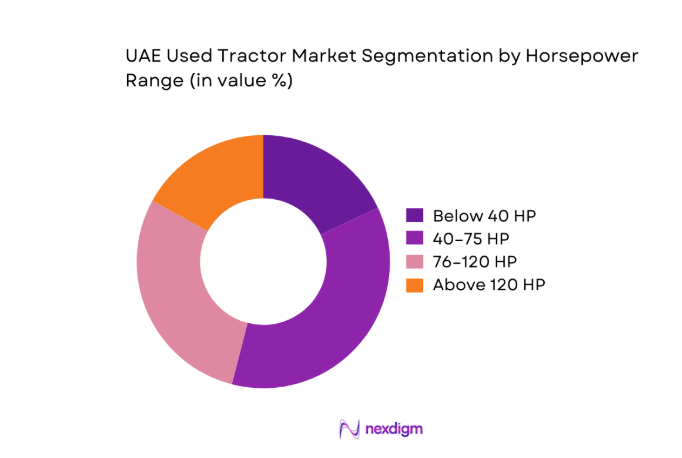

By Horsepower Range

Demand skews toward mid-to-high horsepower units due to mixed-use requirements across farms, municipal landscaping, and contracting tasks. Tractors in the 40–75 HP and 76–120 HP ranges dominate resale liquidity because they balance fuel efficiency with implement compatibility for tillage, hauling, and maintenance. Below 40 HP units attract hobby farms and greenhouse operators but face limited supply consistency. Above 120 HP units circulate within commercial operations with higher utilization intensity, leading to structured fleet refresh cycles. Buyers prioritize drivetrain condition, transmission reliability, and hydraulic performance, making mid-range horsepower segments the most resilient in turnover and refurbishment activity across emirates.

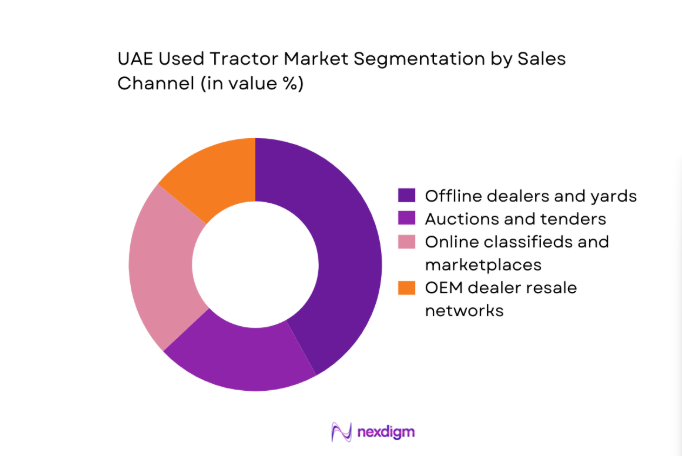

By Sales Channel

Offline dealers and yards remain dominant due to inspection needs, financing facilitation, and immediate service access. Auctions contribute to fleet liquidation flows from contractors and rental operators, supporting periodic supply surges. Online classifieds and marketplaces improve price discovery and reach smaller buyers, but conversion rates depend on verified inspections and logistics support. OEM dealer resale networks are growing through certified pre-owned programs that bundle refurbishment, warranties, and parts assurance. Channel choice is shaped by risk tolerance, urgency of deployment, and access to after-sales support, with multi-channel buyers increasingly triangulating prices before closing transactions.

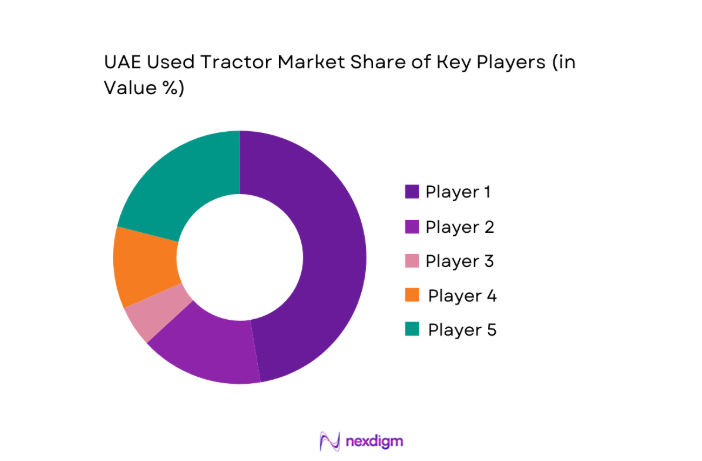

Competitive Landscape

The competitive environment is fragmented, with value creation concentrated in refurbishment depth, inspection credibility, service coverage, and channel orchestration. Operators differentiate through inventory breadth, logistics speed, and post-sale support rather than exclusive access to supply. Consolidation remains limited, favoring agile multi-channel strategies.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Al-Futtaim Auto & Machinery Company | 1955 | Dubai | ~ | ~ | ~ | ~ | ~ | ~ |

| Al-Bahar | 1953 | Dubai | ~ | ~ | ~ | ~ | ~ | ~ |

| United Gulf Equipment | 2006 | Dubai | ~ | ~ | ~ | ~ | ~ | ~ |

| Galadari Engineering Works | 1978 | Dubai | ~ | ~ | ~ | ~ | ~ | ~ |

| Al Marwan Group | 1978 | Sharjah | ~ | ~ | ~ | ~ | ~ | ~ |

UAE Used Tractor Market Analysis

Growth Drivers

Rising farm mechanization in desert and controlled-environment agriculture

Mechanization intensity rose alongside controlled-environment farming expansion, with greenhouse acreage registrations increasing by 184 in 2024 and 167 in 2025 across multiple emirates. Irrigated plot counts recorded 312 new installations in 2024, supporting equipment utilization density. Water-efficient irrigation permits reached 2,941 in 2025, reinforcing mechanized operations for soil preparation and logistics. Farm labor permits declined by 1,284 in 2024, raising reliance on machinery for productivity continuity. Port clearance volumes for used agricultural machinery consignments reached 6,214 units in 2025, improving fleet availability. Extension programs conducted 94 mechanization workshops in 2024, accelerating adoption and refurbishment demand across resale channels.

Cost advantage over new tractors amid budget constraints of small farms

Smallholder farm registrations increased by 1,126 in 2024 and 1,041 in 2025, expanding demand for affordable mechanization. Agricultural credit approvals numbered 3,218 cases in 2024, with average loan tenures extending to 48 months in 2025, favoring pre-owned equipment uptake. Import inspection clearances for used tractors reached 5,403 in 2024, improving availability. Equipment downtime reports fell by 213 incidents in 2025 following refurbishment standards enforcement. Repair workshop certifications rose to 176 facilities in 2024, strengthening maintenance ecosystems. Cooperative procurement groups registered 62 new entities in 2025, aggregating purchasing power for used equipment acquisition.

Challenges

Limited transparency on machine history and usage hours

Verification gaps persist as odometer tampering cases documented 417 incidents in 2024 and 389 in 2025 by inspection authorities. Digital service records coverage reached only 1,284 machines in 2024, constraining provenance checks. Pre-import inspection rejections totaled 612 consignments in 2025, delaying deployment cycles. Title transfer discrepancies affected 2,073 transactions in 2024, increasing legal processing time. Workshop diagnostics adoption reached 96 certified scanners in 2025, insufficient for market-wide coverage. Dispute mediation cases filed with commercial departments numbered 241 in 2024, reflecting trust deficits that slow turnover and elevate buyer due diligence burdens.

High maintenance costs for older imported units

Failure rates for transmissions on tractors exceeding 12 years reached 1,184 incidents in 2024, increasing workshop queues. Spare parts backorders averaged 19 days in 2025 due to discontinued model components. Warranty claim approvals declined by 327 cases in 2024 for grey-import units lacking service histories. Workshop labor certifications expanded by 142 technicians in 2025, yet capacity gaps persist during peak seasons. Preventive maintenance compliance audits recorded 2,016 non-compliance notices in 2024, elevating downtime risks. Equipment inspection intervals shortened to 90 days in 2025, raising operational burdens for older fleets and constraining reliable utilization.

Opportunities

Growth of certified pre-owned programs by OEM dealers

Certified programs expanded inspection throughput to 1,734 units in 2024 and 1,962 in 2025, raising buyer confidence and accelerating turnover. Warranty-backed refurbishment protocols covered 47 standardized checkpoints by 2025, improving reliability outcomes. Service appointment lead times fell from 14 days to 7 days in 2024, enhancing deployment readiness. Dealer yard capacity increased by 23 locations in 2025, improving geographic coverage. Training completions reached 618 technicians in 2024, standardizing diagnostics. Compliance audits recorded 1,103 passes in 2025, strengthening trust signals that reduce transaction friction and enable structured fleet renewal cycles.

Digital marketplaces improving price discovery and reach

Verified listings increased to 4,812 in 2024 and 5,376 in 2025, broadening buyer reach across emirates. Escrow-enabled transactions processed 1,946 orders in 2025, reducing settlement risks. Logistics integrations covered 27 hubs by 2024, shortening delivery cycles. Remote inspection bookings reached 2,391 sessions in 2025, improving pre-purchase confidence. Fraud reports declined by 318 cases in 2024 following ID verification rollouts. Data dashboards tracked 14 condition metrics per listing in 2025, enhancing transparency and supporting faster decision cycles for multi-channel buyers seeking reliable used equipment access.

Future Outlook

The market is expected to remain anchored in refurbishment quality, inspection credibility, and multi-channel reach through 2035. Policy emphasis on food security, municipal maintenance, and sustainable operations will sustain utilization. Digital verification and certified resale programs should compress transaction cycles and improve trust. Cross-emirate logistics integration and service network expansion will continue to shape competitive advantage.

Major Players

- Al-Futtaim Auto & Machinery Company

- Al-Bahar

- United Gulf Equipment

- Galadari Engineering Works

- Al Marwan Group

- Masaood Power Division

- Juma Al Majid Equipment

- Al Shirawi Equipment Company

- Tractors & Farm Equipment FZE

- Hako Middle East FZE

- SMH Equipment FZE

- Arabian Jerusalem Equipment Trading

- Al Saqr Industries

- Al Hutaib Machinery

- Emirates Auction

Key Target Audience

- Commercial farming enterprises and agribusiness operators

- Greenhouse and controlled-environment agriculture operators

- Landscaping and municipal maintenance departments

- Construction and contracting firms

- Equipment dealers and refurbishment workshops

- Fleet rental and leasing operators

- Investments and venture capital firms

- Government and regulatory bodies with agency names

Research Methodology

Step 1: Identification of Key Variables

Core variables were defined across equipment age bands, hours of use, refurbishment depth, inspection pass rates, channel mix, service coverage, and logistics readiness. Regulatory compliance indicators and port clearance workflows were mapped to assess supply reliability. Demand-side variables included farm registrations, municipal maintenance workloads, and contracting utilization intensity.

Step 2: Market Analysis and Construction

Primary operational indicators were constructed from port inspections, workshop certifications, yard capacities, and logistics hub coverage. Secondary institutional indicators captured mechanization programs, irrigation permits, and service workforce accreditations. Channel performance was modeled using listing verification rates, escrow adoption, and delivery lead times.

Step 3: Hypothesis Validation and Expert Consultation

Operational hypotheses were validated through structured consultations with refurbishment managers, inspection engineers, logistics coordinators, and financing officers. Field audits tested consistency of diagnostics protocols and service SLAs. Cross-emirate comparisons refined assumptions on channel effectiveness and service density impacts on turnover velocity.

Step 4: Research Synthesis and Final Output

Findings were synthesized into a coherent market narrative integrating demand drivers, constraints, and opportunity pathways. Indicator triangulation ensured internal consistency across channels and service ecosystems. The final output emphasized operational readiness, policy alignment, and channel orchestration as determinants of competitive advantage.

- Executive Summary

- Research Methodology (Market Definitions and grading of used tractors by age and condition, Dealer and auction house primary interviews across UAE emirates, Import-export records and customs data triangulation, Fleet audits at large farms and contracting firms, Price tracking across classifieds and resale platforms, OEM dealer buyback and trade-in program analysis)

- Definition and Scope

- Market evolution

- Usage patterns across agriculture and contracting

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising farm mechanization in desert and controlled-environment agriculture

Cost advantage over new tractors amid budget constraints of small farms

Expansion of landscaping and municipal maintenance projects

Inflow of used tractors from Japan and Europe

Replacement cycles of large agribusiness and contracting fleets

Availability of dealer refurbishment and warranty programs - Challenges

Limited transparency on machine history and usage hours

High maintenance costs for older imported units

Spare parts availability for discontinued models

Financing constraints for smallholder farmers

Regulatory and inspection inconsistencies for used machinery

Seasonal demand volatility linked to farming cycles - Opportunities

Growth of certified pre-owned programs by OEM dealers

Digital marketplaces improving price discovery and reach

Rising demand from greenhouse and hydroponic farms

Refurbishment and retrofitting services for emissions and safety compliance

Cross-border sourcing from surplus markets

Service contracts and extended warranty offerings - Trends

Shift toward higher horsepower used tractors for commercial farms

Increased preference for 4WD units for sandy terrain

Use of telematics retrofits for fleet monitoring

Bundled sales of implements with used tractors

Growth of auction-based liquidation of rental fleets

Price sensitivity driving demand for Japanese-origin tractors - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Active Fleet, 2020–2025

- By Average Selling Price, 2020–2025

- By Horsepower Range (in Value %)

Below 40 HP

40–75 HP

76–120 HP

Above 120 HP - By Application (in Value %)

Crop farming

Horticulture and greenhouse operations

Livestock and dairy farms

Landscaping and municipal services

Construction and earthmoving support - By Tractor Type (in Value %)

Two-wheel drive tractors

Four-wheel drive tractors

Compact tractors

Utility tractors

Row-crop tractors - By Source of Supply (in Value %)

Dealer-certified used

Independent resellers

Farm fleet replacement

Rental and leasing fleet disposals

Direct owner-to-owner sales - By Sales Channel (in Value %)

Offline dealers and yards

Auctions and tenders

Online classifieds and marketplaces

OEM dealer resale networks - By Emirate (in Value %)

Abu Dhabi

Dubai

Sharjah

Ajman

Ras Al Khaimah

Fujairah

Umm Al Quwain

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (tractor age and hours, refurbishment standards, warranty terms, pricing and financing options, parts availability, service network coverage, inventory breadth, delivery lead times)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Al-Futtaim Auto & Machinery Company

Al-Bahar (Mohamed Abdulrahman Al-Bahar LLC)

United Gulf Equipment

Galadari Engineering Works

Tractors & Farm Equipment FZE

Al Shirawi Equipment Company

Al Marwan Group

Arabian Jerusalem Equipment Trading

Masaood Power Division

Juma Al Majid Equipment

Al Saqr Industries

Hako Middle East FZE

SMH Equipment FZE

Al Hutaib Machinery

Emirates Auction

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2026–2035

- By Volume, 2026–2035

- By Active Fleet, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now