Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UAE wealth management market demonstrates substantial scale, with assets under management in the domestic private banking and wealth advisory sector estimated at approximately USD ~ trillion based on recent historical assessments from central bank and financial center disclosures. Market expansion is primarily driven by high net worth migration inflows, sovereign capital recycling into private portfolios, and increasing participation of regional family businesses seeking structured investment and estate solutions through regulated wealth platforms.

Dubai and Abu Dhabi dominate the UAE wealth management market due to their status as global financial hubs hosting international private banks, asset managers, and family offices within established financial centers such as DIFC and ADGM. Their dominance is reinforced by regulatory clarity, cross-border investment connectivity, concentration of ultra-high-net-worth residents, and proximity to sovereign wealth institutions and regional corporate headquarters that anchor advisory demand and capital allocation activity.

Market Segmentation

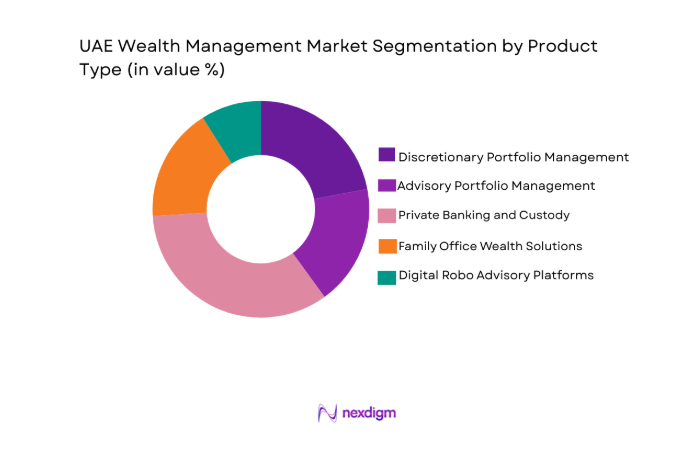

By Product Type

UAE wealth management market is segmented by product type into discretionary portfolio management, advisory portfolio management, private banking services, family office wealth solutions, and digital robo advisory platforms. Recently, private banking services has a dominant market share due to factors such as strong relationship-driven advisory culture, concentration of ultra-high-net-worth individuals requiring bespoke structuring, brand presence of global banks, and advanced custody and lending infrastructure within UAE financial centers.

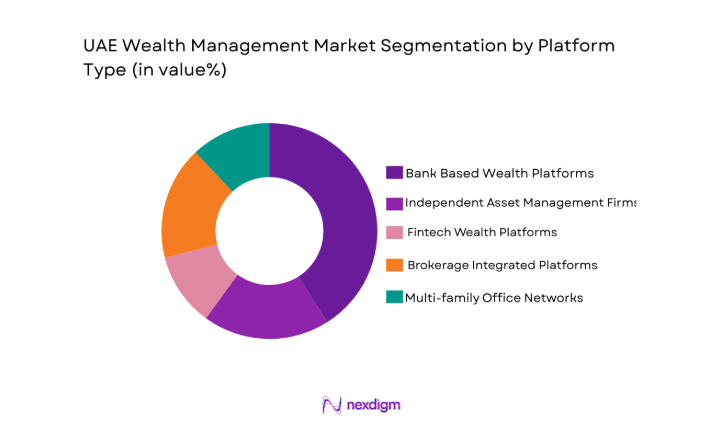

By Platform Type

UAE wealth management market is segmented by platform type into bank based wealth platforms, independent asset management firms, fintech wealth platforms, brokerage integrated platforms, and multi family office platforms. Recently, bank based wealth platforms has a dominant market share due to factors such as extensive client trust, integrated lending and custody capabilities, cross-border booking infrastructure, and long-established presence of international private banking institutions across Dubai and Abu Dhabi financial centers.

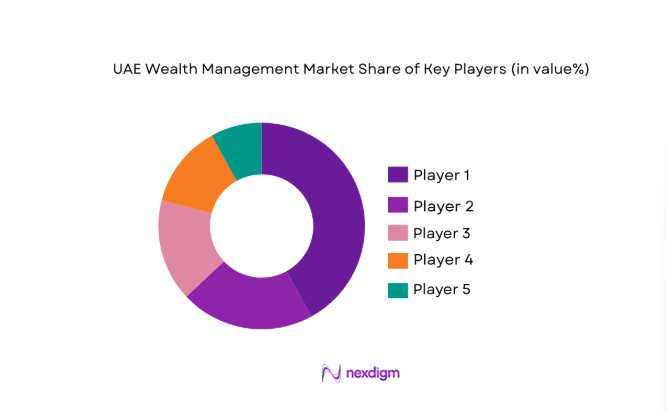

Competitive Landscape

The UAE wealth management market is moderately consolidated, led by international private banks and large domestic banking groups that command strong client trust and cross-border advisory capabilities. Global firms leverage brand reputation and global investment platforms, while regional banks maintain deep local relationships and regulatory familiarity. Independent asset managers and family offices are expanding but remain smaller, resulting in a competitive environment shaped by scale, global reach, and integrated banking-wealth ecosystems.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Client Segment Focus |

| Emirates NBD | 1963 | Dubai | ~ | ~ | ~ | ~ | ~ |

| First Abu Dhabi Bank | 2017 | Abu Dhabi | ~ | ~ | ~ | ~ | ~ |

| HSBC Private Bank | 1865 | London | ~ | ~ | ~ | ~ | ~ |

| UBS Wealth Management | 1862 | Zurich | ~ | ~ | ~ | ~ | ~ |

| Julius Baer | 1890 | Zurich | ~ | ~ | ~ | ~ | ~ |

UAE Wealth Management Market Analysis

Growth Drivers

High Net Worth Migration and Capital Inflows into UAE Financial Centers

The UAE wealth management market is fundamentally propelled by sustained inflows of high net worth and ultra-high-net-worth individuals relocating assets and residency to Dubai and Abu Dhabi due to political stability, favorable taxation, and lifestyle attractiveness compared with traditional offshore wealth hubs. This relocation trend has materially expanded the addressable client base for private banks, family offices, and advisory platforms, as entrepreneurs and global investors increasingly choose the UAE as a primary booking center for their international wealth holdings rather than secondary offshore jurisdictions. Regulatory residency initiatives such as long-term visas and investor residency frameworks have institutionalized wealth migration by offering durable settlement options tied to investment commitments and business presence, thereby anchoring client portfolios within domestic wealth platforms. The concentration of sovereign wealth institutions and regional corporate headquarters further amplifies inflows, as executives and stakeholders associated with these entities often consolidate personal assets locally under trusted advisory structures. Financial center infrastructure in DIFC and ADGM provides globally recognized regulatory regimes, legal certainty, and dispute resolution systems aligned with international standards, which reassures migrating investors regarding asset protection and governance continuity. Private banks have responded by expanding booking capabilities, multi-currency custody, and global investment access from UAE hubs, enabling clients to manage diversified portfolios without relocating assets to Europe or Asia. The interaction of migration, residency policy, and institutional financial ecosystems therefore creates a reinforcing cycle in which new entrants attract additional wealth services investment, strengthening the domestic advisory landscape. Over time this structural shift is transforming the UAE from a transactional offshore conduit into a primary wealth domicile, sustaining long-term growth in managed assets and advisory revenues.

Expansion of Regional Family Businesses and Intergenerational Wealth Structuring Demand

The UAE wealth management market is strongly driven by the evolution of regional family-owned conglomerates whose accumulated capital now requires formal governance, succession planning, and diversified portfolio management across generations. Many GCC family enterprises that historically retained wealth within operating businesses are transitioning toward structured investment holding entities, foundations, and trusts to manage liquidity events, generational transfer, and global diversification strategies. This transition significantly increases demand for professional wealth advisory, fiduciary structuring, estate planning, and discretionary investment management services delivered through private banks and family office platforms. UAE regulatory reforms enabling foundations, family business laws, and wealth structuring vehicles have provided credible legal frameworks for intergenerational transfer within domestic jurisdictions, reducing reliance on traditional offshore centers while retaining assets locally. As founders approach succession phases, heirs often seek institutional portfolio diversification beyond legacy operating sectors, expanding allocations into global equities, private markets, and alternatives managed by wealth advisors. Family offices are also professionalizing governance and reporting practices, requiring sophisticated risk analytics, consolidated portfolio oversight, and strategic asset allocation advisory that wealth managers are uniquely positioned to provide. Domestic financial centers have positioned themselves as neutral and stable jurisdictions for cross-border family ownership structures spanning multiple GCC and international assets, further anchoring advisory mandates. The scale of intergenerational capital transfer across regional conglomerates therefore represents a structural and multi-decade growth engine for wealth management services in the UAE. As these families institutionalize wealth oversight and succession frameworks, demand for integrated advisory and portfolio management capabilities continues to expand in depth and sophistication.

Market Challenges

Intense Global Competition from Established Offshore Wealth Hubs

The UAE wealth management market faces persistent competitive pressure from long-established global wealth centers such as Switzerland, Singapore, and London that possess decades of reputation in asset protection, advisory depth, and international booking experience. High net worth individuals often maintain diversified custody across multiple jurisdictions to mitigate geopolitical and regulatory risk, limiting the share of assets consolidated within UAE platforms despite residency relocation. These traditional hubs offer extensive product breadth, mature private market access, and highly specialized advisory expertise accumulated over long operational histories, creating switching inertia among global investors accustomed to those ecosystems. Although UAE financial centers have advanced significantly, perceptions of relative institutional maturity and global legacy still influence booking decisions among conservative wealth holders and multigenerational family offices. Cross-border regulatory equivalence and passporting arrangements also remain more extensive among established centers, enabling seamless investment distribution across continents that UAE platforms continue to expand but have not fully matched. Competitive tax neutrality and confidentiality traditions in historic offshore jurisdictions further reinforce their attractiveness for certain client segments prioritizing asset privacy and legacy continuity. As a result, UAE institutions must invest heavily in advisory talent, product innovation, and global partnerships to attract and retain a larger proportion of resident wealth portfolios. This ongoing rivalry constrains pricing power and necessitates continual capability upgrades across custody, structuring, and investment access domains. The competitive dynamic therefore represents a structural challenge requiring sustained differentiation rather than a temporary market condition.

Regulatory Complexity and Cross Border Compliance Burden

The UAE wealth management market operates within a complex matrix of domestic financial regulations, international transparency standards, and cross-jurisdictional tax reporting obligations that significantly increase operational and advisory burdens for institutions and clients. Wealth structures frequently span multiple legal domiciles, asset classes, and residency statuses, requiring precise compliance with anti-money-laundering, beneficial ownership, and tax disclosure frameworks enforced across global financial networks. Continuous evolution of international standards such as automatic information exchange regimes compels wealth managers to maintain advanced compliance infrastructure, documentation rigor, and client due diligence processes that elevate cost structures and onboarding timelines. Clients relocating to the UAE often retain financial ties to previous jurisdictions, necessitating dual or multi-jurisdictional reporting coordination that complicates advisory delivery and structuring recommendations. Regulatory fragmentation between onshore UAE rules and financial free zone regimes further adds complexity, as institutions must navigate differing licensing, client classification, and product distribution requirements across territories. For wealth managers, sustaining expertise across international tax, trust, and fiduciary laws becomes essential yet resource intensive, especially given talent scarcity in specialized cross-border structuring disciplines. Compliance scrutiny also heightens reputational risk exposure, compelling conservative risk policies that may limit product flexibility or client onboarding in sensitive jurisdictions. The cumulative effect of these factors raises operational costs and slows client acquisition cycles relative to simpler regulatory environments. Consequently, regulatory and compliance complexity constitutes a persistent structural challenge affecting scalability and efficiency in UAE wealth management operations.

Opportunities

Rise of Regional Family Office Ecosystems and Institutionalization of Private Wealth

The UAE wealth management market has a significant opportunity to become the primary domicile for regional family offices as Gulf wealth transitions from entrepreneurial ownership to institutional investment governance structures. Increasing liquidity events, generational transitions, and cross-border asset holdings are prompting families to establish formalized offices requiring portfolio management, risk oversight, fiduciary administration, and consolidated reporting capabilities. UAE financial centers provide neutral jurisdictional positioning, advanced legal vehicles, and proximity to family business headquarters, making them attractive hubs for these entities. Wealth managers can expand into multi-family office services, governance advisory, and institutional investment access tailored to regional cultural and succession preferences. As family offices scale assets and professionalize investment strategies, demand rises for private markets sourcing, co-investment opportunities, and strategic asset allocation frameworks that local platforms can provide. The clustering of multiple family offices within UAE hubs also creates network effects, fostering specialized service providers, talent pools, and investment collaboration ecosystems. Over time this concentration could position the UAE alongside Switzerland and Singapore as a global family office center. Capturing this opportunity requires sustained regulatory support, talent development, and product sophistication but offers substantial long-term asset growth potential. Institutionalization of private wealth therefore represents a structural opportunity to deepen and anchor regional capital within domestic advisory platforms.

Integration of Digital Assets and Alternative Investments into Wealth Portfolios

The UAE wealth management market is uniquely positioned to capitalize on the integration of digital assets, tokenized securities, and alternative investment vehicles into diversified client portfolios due to progressive regulatory initiatives and fintech adoption within financial centers. Investors globally are increasing allocations to private equity, venture capital, infrastructure, and digital asset classes seeking diversification and higher return potential, yet require regulated advisory channels to access these opportunities safely. UAE authorities have established virtual asset regulatory frameworks and innovation sandboxes that legitimize digital investment channels under supervised conditions, enabling wealth managers to incorporate these assets within advisory mandates. This regulatory clarity differentiates the UAE from many jurisdictions where digital asset oversight remains uncertain, attracting technologically oriented investors and entrepreneurial wealth segments. Wealth platforms can therefore expand product suites into tokenized funds, digital custody, and alternative co-investment structures aligned with emerging client demand. Integration of these assets also enhances portfolio diversification and engagement among younger generations of wealth holders transitioning into advisory relationships. As global capital markets evolve toward digitization and private market expansion, early adoption by UAE wealth institutions can strengthen competitive positioning and asset growth. The convergence of fintech innovation, regulatory openness, and client appetite thus creates a durable opportunity for product and revenue expansion in the wealth sector. Successfully harnessing this trend requires risk management sophistication and investor education but offers transformative growth potential.

Future Outlook

The UAE wealth management market is expected to sustain strong expansion driven by continued high-net-worth migration, institutionalization of regional family wealth, and regulatory innovation across financial centers. Digital advisory platforms and alternative investment integration will reshape service delivery models and client engagement. Supportive residency and business policies will reinforce asset inflows, while family office ecosystems deepen domestic capital management capabilities. Over the coming years, the UAE is positioned to strengthen its role as a primary global wealth hub.

Major Players

- Emirates NBD Asset Management

- First Abu Dhabi Bank Wealth Management

- HSBC Global Private Banking UAE

- Julius Baer Middle East

- UBS Wealth Management UAE

- Credit Suisse Middle East

- EFG Hermes Private Wealth

- ADCB Private Banking

- Standard Chartered Private Bank UAE

- Sarasin Alpen Middle East

- Lombard Odier Middle East

- Pictet Wealth Management UAE

- Barclays Private Bank Middle East

- Mashreq Private Banking

- Abu Dhabi Commercial Bank Wealth

Key Target Audience

- Private banks and wealth management institutions

- Family offices and ultra-high-net-worth investors

- Asset management companies

- Sovereign wealth related entities

- Financial technology wealth platforms

- Investments and venture capitalist firms

- Government and regulatory bodies

- Brokerage and investment advisory firms

Research Methodology

Step 1: Identification of Key Variables

Core market variables such as assets under management, client segments, platform structures, and regulatory frameworks were identified through financial disclosures and institutional reports. Demand drivers including migration flows and family wealth transitions were mapped to define market boundaries and analytical scope.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using banking sector asset data, wealth population statistics, and financial center activity metrics. Platform and product shares were modeled by triangulating institutional presence, service offerings, and client distribution patterns across UAE financial hubs.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultation with wealth advisors, financial analysts, and regional banking specialists. Regulatory interpretations and structural assumptions were cross-checked against official financial center publications and central bank communications to ensure consistency and accuracy.

Step 4: Research Synthesis and Final Output

All validated data and qualitative insights were synthesized into a structured market framework covering segmentation, competition, and growth dynamics. The final analysis integrates quantitative estimates with institutional context to present a coherent outlook for UAE wealth management evolution.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising concentration of high-net-worth expatriates and global entrepreneurs relocating to UAE

Expansion of sovereign wealth ecosystem and regional capital markets depth

Government residency and golden visa programs attracting global wealth inflows

Increasing intergenerational wealth transfer within GCC family businesses

Rapid adoption of digital wealth platforms and advisory automation - Market Challenges

Intensifying global competition from established offshore wealth centers

Regulatory compliance complexity across cross border investment structures

Talent scarcity in advanced wealth advisory and family office expertise

Market volatility affecting discretionary portfolio performance expectations

Client trust sensitivity linked to fiduciary transparency and governance - Market Opportunities

Growth of regional family office structuring and succession planning services

Expansion of Islamic compliant wealth and estate planning solutions

Integration of digital assets and alternative investments into portfolios - Trends

Shift toward holistic family office and legacy planning mandates

Rise of discretionary mandates over transactional brokerage relationships

Digital client experience platforms with real time portfolio visibility

Increasing allocation to private markets and alternatives

Consolidation among independent wealth and asset management firms - Government Regulations & Defense Policy

Strengthening of UAE securities and financial advisory licensing frameworks

Introduction of family business and foundation legal structures

Anti money laundering and beneficial ownership transparency reforms - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Discretionary Portfolio Management

Advisory Portfolio Management

Private Banking Services

Family Office Wealth Solutions

Digital Robo Advisory Platforms - By Platform Type (In Value%)

Bank Based Wealth Platforms

Independent Asset Management Firms

Fintech Wealth Platforms

Brokerage Integrated Platforms

Multi Family Office Platforms - By Fitment Type (In Value%)

Onshore UAE Wealth Structures

Offshore Investment Structures

Hybrid Cross Border Structures

Islamic Wealth Structures

Trust and Foundation Structures - By End User Segment (In Value%)

Ultra High Net Worth Individuals

High Net Worth Individuals

Mass Affluent Investors

Family Offices

Institutional Private Clients

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Client Segment Focus, Advisory Model, Asset Class Coverage, Geographic Reach, Digital Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Emirates NBD Asset Management

First Abu Dhabi Bank Wealth Management

HSBC Global Private Banking UAE

Julius Baer Middle East

UBS Wealth Management UAE

Credit Suisse Middle East

EFG Hermes Private Wealth

ADCB Private Banking

Standard Chartered Private Bank UAE

Sarasin Alpen Middle East

Lombard Odier Middle East

Pictet Wealth Management UAE

Barclays Private Bank Middle East

Mashreq Private Banking

Abu Dhabi Commercial Bank Wealth

- Ultra high net worth families demand integrated succession, governance, and global asset diversification advisory

- High net worth expatriates prioritize cross border structuring and tax efficient wealth preservation

- Mass affluent segment shows increasing adoption of digital advisory and managed portfolios

- Family offices seek institutional grade investment access and private market opportunities

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now