Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UK Advanced Materials market is expected to reach USD ~ billion in 2024, driven by increasing demand across industries such as automotive, aerospace, electronics, and energy. The need for high-performance, durable, and sustainable materials is spurring the adoption of advanced composites, polymers, and nanomaterials. Additionally, innovations in material science, including developments in 3D printing and lightweight materials, are further fueling market growth, making advanced materials integral to achieving higher efficiency and sustainability across various industries.

The regions of London, Birmingham, and Cambridge play a key role in driving the growth of the UK Advanced Materials market. London is a major hub for technology and innovation, with a growing number of startups and academic institutions focused on material science research. Birmingham is at the center of the UK’s automotive industry, where advanced materials are increasingly used to manufacture lightweight, high-strength components for vehicles. Cambridge is home to world-leading research in nanotechnology and advanced materials, fostering collaborations between academic and industrial sectors to accelerate the development and commercialization of new materials.

Market Segmentation

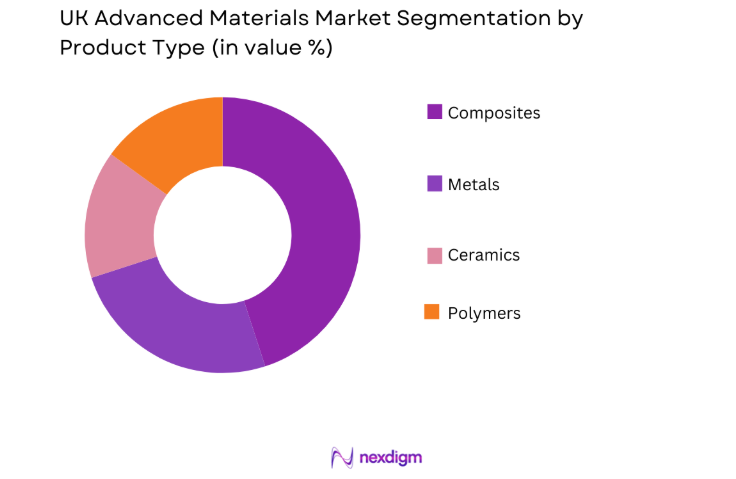

By Product Type

The UK Advanced Materials market is segmented by product type into composites, metals, ceramics, and polymers. Recently, composites have captured a dominant market share due to their use in high-performance applications in industries such as aerospace, automotive, and energy. Composites, particularly carbon fiber and fiber-reinforced polymers, offer superior strength-to-weight ratios, making them ideal for lightweight structures that require high durability. The growing focus on reducing vehicle weight for fuel efficiency, as well as the adoption of lightweight materials in aerospace and renewable energy sectors, has further driven the demand for composites. As manufacturing technologies evolve and costs decrease, composites are expected to see continued dominance in the market.

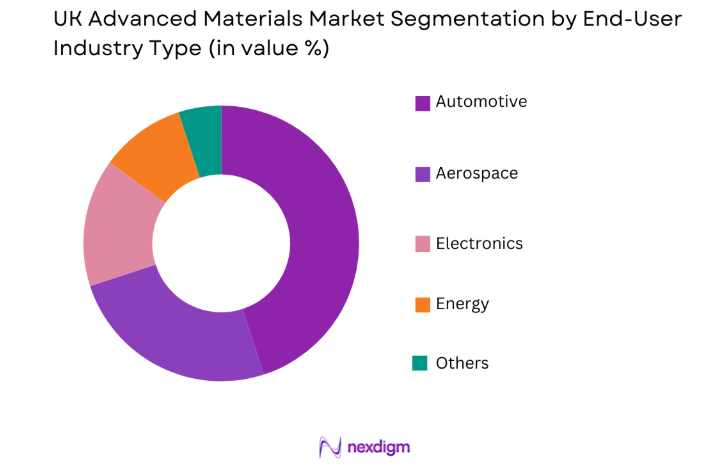

By End-User Industry

The UK Advanced Materials market is segmented by end-user industry into automotive, aerospace, electronics, energy, and others. The automotive industry holds a dominant market share due to the increasing use of advanced materials in vehicle manufacturing. As automakers aim to enhance fuel efficiency, reduce emissions, and improve vehicle safety, the demand for lightweight and high-strength materials has surged. Advanced composites, such as carbon fiber, are being increasingly incorporated into vehicle designs, including body panels, interiors, and structural components. Additionally, advancements in electric vehicle (EV) technologies, which require high-performance materials for batteries and powertrains, are further driving the demand for advanced materials in the automotive sector. The growing emphasis on sustainability in transportation fuels the adoption of advanced materials to meet environmental and regulatory standards.

Competitive Landscape

The UK Advanced Materials market is highly competitive, with both established global players and innovative local companies driving the development and commercialization of new materials. Major players are focusing on innovations in lightweight materials, nanomaterials, and sustainable composites to meet the evolving demands of industries such as automotive, aerospace, and energy. There is a significant focus on research and development (R&D), and companies are increasingly partnering with universities and research institutions to accelerate material innovation. Additionally, government incentives for green technologies and advanced manufacturing are fostering competition and encouraging companies to invest in sustainable solutions. As the demand for high-performance and sustainable materials continues to grow, the market is likely to experience further consolidation, with large companies acquiring smaller startups to expand their product offerings.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| 3M | 1902 | St. Paul, USA | ~ | ~ | ~ | ~ | ~ |

| Dow Inc. | 1897 | Midland, USA | ~ | ~ | ~ | ~ | ~ |

| Hexcel | 1948 | Stamford, USA | ~ | ~ | ~ | ~ | ~ |

| Covestro | 2015 | Leverkusen, Germany | ~ | ~ | ~ | ~ | ~ |

| Carpenter Technology | 1889 | Wyomissing, USA | ~ | ~ | ~ | ~ | ~ |

UK Advanced Materials Market Analysis

Growth Drivers

Technological Advancements in Material Science

Technological advancements in material science are a significant growth driver for the UK Advanced Materials market. The development of advanced materials such as high-strength composites, lightweight alloys, and nanomaterials has enabled industries to produce products that are stronger, lighter, and more energy-efficient. These innovations have transformed sectors like aerospace, automotive, and energy, where material performance is critical. For instance, carbon fiber composites have revolutionized the automotive and aerospace industries by providing high-strength yet lightweight alternatives to traditional materials. Furthermore, the growing research in nanotechnology is enabling the development of materials with unique properties, such as enhanced thermal and electrical conductivity, which are crucial for applications in electronics, energy, and healthcare. As material science continues to evolve, the demand for advanced materials will increase, driving further growth in the market. The ongoing innovation in manufacturing processes, such as 3D printing and additive manufacturing, will also play a pivotal role in driving demand for advanced materials that can be customized for specific applications.

Sustainability and Environmental Regulations

The increasing focus on sustainability and environmental regulations is a key driver of the UK Advanced Materials market. As industries face growing pressure to reduce carbon footprints, enhance energy efficiency, and meet stringent environmental standards, the demand for sustainable materials is rising. Advanced materials, particularly composites, polymers, and recyclable materials, offer solutions to help businesses meet these sustainability goals. In the automotive industry, for example, the use of lightweight materials is essential to improving fuel efficiency and reducing emissions, aligning with the UK’s goals for reducing carbon emissions. In addition, the UK government’s policies supporting green manufacturing, recycling, and sustainable infrastructure development further incentivize the use of advanced materials in various sectors. As industries increasingly prioritize eco-friendly solutions, the demand for advanced materials that offer both high performance and sustainability will continue to drive market growth.

Market Challenges

High Production Costs and Limited Accessibility

One of the main challenges facing the UK Advanced Materials market is the high production costs associated with manufacturing advanced materials. Materials such as carbon fiber, graphene, and titanium alloys require complex and costly production processes that limit their accessibility, particularly for smaller businesses or startups. The expense involved in the research, development, and manufacturing of these materials can be a barrier for companies looking to adopt them in their production processes. Additionally, the limited scalability of some advanced material production techniques means that mass production is not always cost-effective, preventing many industries from fully integrating these materials into their supply chains. The high costs associated with advanced materials also impact their use in cost-sensitive industries such as construction and consumer goods, limiting their widespread adoption despite their performance advantages. Overcoming these cost barriers through improved manufacturing techniques, economies of scale, and government incentives for sustainable production will be essential for the market’s growth.

Integration with Existing Infrastructure

The integration of advanced materials with existing infrastructure presents a significant challenge in the UK market. Many industries, especially in traditional manufacturing and construction sectors, continue to rely on legacy materials that are not compatible with advanced alternatives. For example, incorporating new advanced composites or alloys into existing production lines, machines, and construction materials can require extensive modifications or entire system overhauls. This can be particularly challenging for companies that cannot afford to make the necessary capital investments. The need to upgrade or replace infrastructure to accommodate advanced materials may also cause production delays and increase downtime, impacting overall efficiency. Additionally, the lack of standardization in advanced material specifications and applications makes it difficult for industries to implement these materials seamlessly into their existing systems. Addressing these integration challenges will require coordinated efforts between material manufacturers, engineers, and industry stakeholders to develop compatible systems and solutions.

Opportunities

Growth of Electric Vehicles (EVs) and Lightweight Materials

The growth of the electric vehicle (EV) market presents a significant opportunity for the UK Advanced Materials market. As the automotive industry shifts toward electric vehicles, there is an increasing demand for lightweight, high-performance materials that can improve energy efficiency and vehicle performance. Advanced materials such as carbon fiber composites and lightweight alloys are ideal for reducing the weight of EVs, allowing for longer battery life and improved energy consumption. The push for sustainable and energy-efficient transportation solutions further drives the adoption of advanced materials in EV manufacturing. Additionally, the rise of autonomous vehicles, which require advanced sensors, lightweight materials, and high-performance components, provides further opportunities for advanced materials to play a pivotal role in the automotive sector. As the UK government continues to support the transition to electric and low-emission vehicles, the demand for advanced materials will grow, creating opportunities for manufacturers to expand their product offerings in the automotive industry.

Increasing Use of Nanomaterials in Electronics and Energy

The increasing use of nanomaterials in electronics and energy applications presents a significant opportunity for the UK Advanced Materials market. Nanomaterials offer unique properties, such as enhanced conductivity, strength, and flexibility, making them ideal for use in electronic devices, batteries, and energy storage systems. As demand for smaller, more powerful, and energy-efficient electronic devices continues to rise, the need for advanced nanomaterials is growing. In the energy sector, nanomaterials are being explored for use in next-generation batteries, solar cells, and energy storage solutions, offering improved performance and lower costs. The UK’s strong focus on digital technologies, smart grids, and renewable energy further drives the demand for nanomaterials that can enhance the efficiency and sustainability of energy systems. The development of new nanomaterial-based solutions presents exciting growth prospects for the UK Advanced Materials market, particularly in the fields of electronics, energy, and environmental applications.

Future Outlook

The UK Advanced Materials market is expected to experience continued growth over the next five years, driven by advancements in material science and increasing demand across industries such as automotive, aerospace, electronics, and energy. The continued development of sustainable materials, nanotechnology, and composites will open new opportunities for companies to innovate and meet the evolving needs of various sectors. Government policies supporting green manufacturing and research in advanced materials will further accelerate market growth, creating a favorable environment for innovation. The increasing demand for lightweight, high-performance, and energy-efficient materials will drive the adoption of advanced materials, particularly in industries focused on sustainability and digital transformation.

Major Players

- 3M

- Dow Inc.

- Hexcel

- Covestro

- Carpenter Technology

- BASF

- Huntsman Corporation

- DuPont

- Arkema

- Mitsubishi Chemical

- Toray Industries

- Solvay

- Owens Corning

- PPG Industries

- SGL Carbon

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Aerospace manufacturers

- Automotive manufacturers

- Energy and utility companies

- Construction industry leaders

- Industrial design and development companies

Research Methodology

Step 1: Identification of Key Variables

Key market drivers, challenges, and trends are identified, focusing on factors such as technological advancements, market demand, and regulatory policies.

Step 2: Market Analysis and Construction

An in-depth analysis of market trends, segmentation, and competition is conducted to construct an accurate market model.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts and key stakeholders provide feedback to validate assumptions and refine the research findings based on real-world insights.

Step 4: Research Synthesis and Final Output

The findings from analysis and consultations are synthesized into a final report, providing actionable insights, strategic recommendations, and a clear market outlook for stakeholders in the UK Advanced Materials market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Increase in Demand for Lightweight and Durable Materials

Rising Application in Aerospace and Automotive Sectors

Advancements in Nano and Smart Materials - Market Challenges

High Production Costs for Advanced Materials

Challenges in Standardization and Quality Control

Environmental Impact and Recycling Issues - Market Opportunities

Expansion in Smart Manufacturing Technologies

Growth in Renewable Energy Applications

Rising Investment in High-Tech Construction Materials - Trends

Emerging Use of 3D Printing in Advanced Materials

Integration of AI and Robotics in Material Development - Government Regulations

Regulations on Sustainable Material Sourcing

Compliance with Safety Standards in Aerospace and Automotive Sectors

Environmental Regulations for Advanced Material Recycling - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Advanced Composites

Nanomaterials

Smart Materials

Conductive Polymers

High-Performance Alloys - By Platform Type (In Value%)

Thermal Conductivity Platforms

High-Strength Platforms

Lightweight Platforms

Corrosion-Resistant Platforms - By Fitment Type (In Value%)

On-Premise Solutions

Cloud-Based Solutions

Modular Systems

Integrated Manufacturing Solutions - By End User Segment (In Value%)

Automotive

Aerospace

Construction

- Market Share Analysis

- Cross Comparison Parameters (Material Performance, Cost, Durability, Environmental Impact, Manufacturing Complexity, Technological Integration, End User Adoption)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

BASF SE

Dow Chemical Company

3M Company

DuPont

Covestro AG

SABIC

Hexcel Corporation

Toray Industries

Sumitomo Chemical

Huntsman Corporation

ArcelorMittal

Mitsubishi Chemical Corporation

Solvay Group

DSM

LANXESS AG

- Increasing Adoption of High-Performance Alloys in Automotive

- Growing Demand for Composites in Aerospace

- Shift Towards Smart Materials in Construction

- Rising Investment in Nano-Materials for Electronics

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now