Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UK AI Infrastructure Market is valued at approximately USD ~ billion based on recent historical assessments derived from national digital infrastructure investment data, hyperscale provider regional revenue disclosures, and enterprise AI infrastructure spending benchmarks. Growth is driven by rapid enterprise AI adoption, government digitalization programs, and expansion of high-performance computing capacity across industries including finance, healthcare, research, and public services. Accelerated deployment of GPU clusters, AI-optimized data centers, and advanced networking platforms is strengthening national AI computing capability.

Dominant regions include London, Slough, Cambridge, Manchester, and Edinburgh due to dense data center ecosystems, proximity to financial and research institutions, advanced fiber connectivity, and strong technology talent availability. London and Slough form the core hyperscale and colocation hub supporting enterprise AI workloads and cloud platforms. Cambridge leads in AI research computing infrastructure, while northern cities attract new AI data center campuses due to power availability, land access, and regional digital investment initiatives.

Market Segmentation

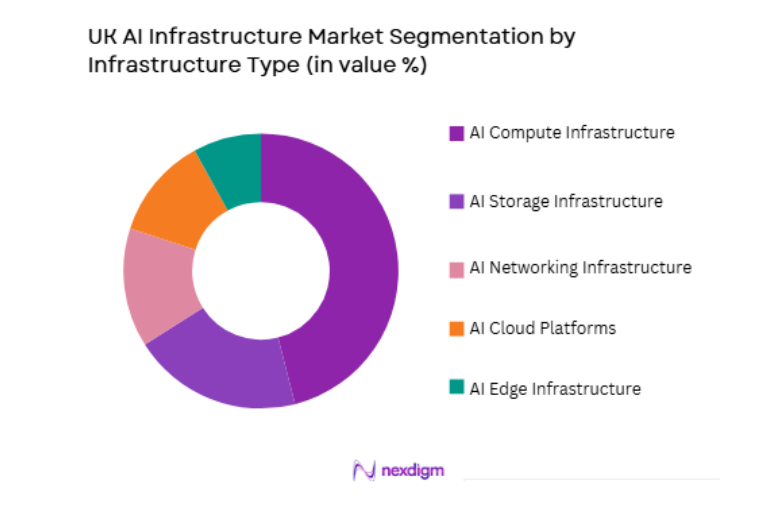

By Infrastructure Type

UK AI Infrastructure Market is segmented by infrastructure type into AI compute infrastructure, AI storage infrastructure, AI networking infrastructure, AI cloud platforms, and AI edge infrastructure. Recently, AI compute infrastructure has a dominant market share due to factors such as accelerated enterprise AI model training, research computing demand, hyperscale GPU cluster expansion, and widespread adoption of generative AI workloads across industries. Organizations require high-performance processors, AI accelerators, and scalable parallel computing architectures to support model development and inference deployment. National research institutions and financial services firms are investing heavily in AI supercomputing capacity to maintain competitiveness.

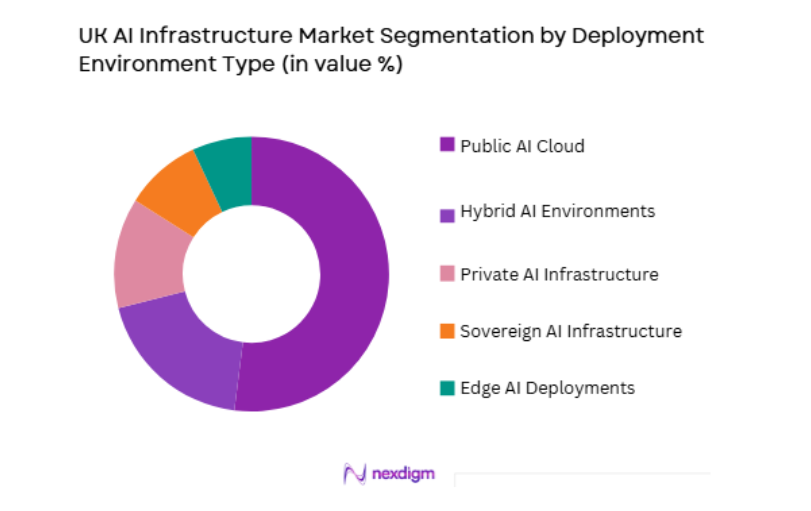

By Deployment Environment

UK AI Infrastructure Market is segmented by deployment environment into public AI cloud, private AI infrastructure, hybrid AI environments, sovereign AI infrastructure, and edge AI deployments. Recently, public AI cloud has a dominant market share due to factors such as rapid access to GPU resources, scalable AI platforms, managed machine learning services, and reduced capital investment requirements for enterprises adopting artificial intelligence capabilities. Organizations prefer consumption-based AI infrastructure rather than building dedicated hardware environments due to cost efficiency and faster deployment. Public AI cloud platforms also provide integrated development frameworks, data services, and security features that simplify enterprise AI implementation.

Competitive Landscape

The UK AI Infrastructure Market is moderately consolidated, shaped by hyperscale cloud providers, semiconductor firms, and specialized AI infrastructure vendors establishing regional compute capacity and AI cloud platforms. Competitive differentiation centers on GPU availability, sovereign cloud compliance, AI software ecosystems, and high-performance networking architecture. Domestic data center operators and European AI infrastructure initiatives are also strengthening presence to support national AI strategy goals and localized data processing requirements.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | UK AI Data Center Presence |

| Amazon Web Services | 2006 | Seattle, USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | Redmond, USA | ~ | ~ | ~ | ~ | ~ |

| Google Cloud | 2008 | Mountain View, USA | ~ | ~ | ~ | ~ | ~ |

| NVIDIA | 1993 | Santa Clara, USA | ~ | ~ | ~ | ~ | ~ |

| IBM | 1911 | Armonk, USA |

UK AI Infrastructure Market Analysis

Growth Drivers

National AI Strategy and Public-Private AI Infrastructure Investment Programs

The United Kingdom’s national artificial intelligence strategy and coordinated public-private investment initiatives are significantly accelerating development of advanced AI computing infrastructure across research institutions, enterprise sectors, and cloud platforms nationwide. Government funding programs are supporting establishment of national AI supercomputing facilities, academic research clusters, and sovereign cloud environments designed to strengthen domestic AI capability and data sovereignty. Collaborative partnerships between technology firms, universities, and public agencies are enabling shared AI infrastructure platforms accessible to startups and enterprises lacking capital for dedicated systems. Financial incentives and innovation grants are encouraging deployment of GPU-accelerated computing and specialized AI data centers across regions beyond London. Public sector digital transformation programs are integrating AI analytics and automation platforms into healthcare, transportation, and public administration systems, increasing infrastructure demand. National policies promoting responsible AI and secure data environments also stimulate localized infrastructure expansion to meet regulatory requirements. Strategic emphasis on AI competitiveness with global economies drives sustained investment in computing capacity and high-speed networking.

Enterprise Adoption of Generative AI and Advanced Analytics Platforms

Rapid adoption of generative artificial intelligence, machine learning analytics, and automated decision systems by UK enterprises is creating substantial demand for scalable AI computing, storage, and cloud infrastructure across financial services, healthcare, retail, and industrial sectors. Organizations are deploying large language models, predictive analytics engines, and intelligent automation platforms that require high-performance GPU clusters and distributed data processing environments. Financial institutions are investing in AI infrastructure for fraud detection, algorithmic trading, and customer intelligence systems requiring real-time processing capabilities. Healthcare providers are adopting AI diagnostics and imaging analysis platforms that depend on specialized computing architectures. Retail and digital commerce firms deploy personalization and recommendation engines that increase data processing intensity. Enterprises prefer cloud-based AI infrastructure to accelerate deployment and reduce hardware ownership complexity. Software vendors increasingly design applications optimized for AI cloud execution, reinforcing infrastructure consumption patterns.

Market Challenges

Limited Power Capacity and Grid Constraints for AI Data Centers

Expansion of AI infrastructure in the United Kingdom is constrained by limited electrical grid capacity, high energy costs, and planning restrictions affecting deployment of large-scale AI data centers and high-performance computing facilities across major regions. AI compute clusters consume significantly more electricity than conventional IT infrastructure due to GPU-dense architectures and cooling requirements. Urban regions with strong connectivity and enterprise demand face power availability limitations that delay new data center approvals. Grid reinforcement and renewable energy integration projects require long development timelines, slowing infrastructure scaling. High national electricity prices increase operating costs for AI computing compared to competing global regions. Environmental regulations and community concerns regarding land use and emissions further complicate site development. Infrastructure providers must invest in energy-efficient cooling and power optimization technologies to maintain sustainability targets.

Shortage of Specialized AI Infrastructure Skills and Integration Expertise

The UK AI Infrastructure Market faces significant challenges due to limited availability of professionals skilled in AI hardware deployment, high-performance computing architecture, and large-scale AI cloud integration across enterprises and public institutions. Designing and operating GPU clusters, distributed AI platforms, and high-speed networking environments requires specialized engineering expertise not widely available in traditional IT workforces. Enterprises adopting AI often lack internal capability to integrate models with scalable infrastructure environments efficiently. Research institutions also compete for limited HPC and AI engineering talent. Skills shortages increase deployment timelines, project costs, and operational risk in AI infrastructure initiatives. Training programs and academic curricula have not yet scaled to meet industry demand for AI systems engineers and infrastructure architects. Dependence on external specialists increases cost and slows adoption among smaller organizations.

Opportunities

Sovereign and Regulated AI Cloud Infrastructure Development

Growing regulatory emphasis on data sovereignty, privacy protection, and secure AI processing environments is creating strong opportunities for sovereign AI cloud infrastructure tailored to government, defense, healthcare, and financial services sectors within the United Kingdom. Organizations handling sensitive data require domestically hosted AI platforms compliant with national regulations and sector-specific governance frameworks. Sovereign AI cloud environments ensure data residency, security certification, and operational transparency aligned with public policy requirements. Government agencies and regulated industries increasingly prioritize trusted domestic infrastructure providers over global platforms for critical workloads. Investments in national AI clouds and secure data centers are therefore expanding to support sensitive AI applications. Collaboration between domestic infrastructure firms and global technology vendors enables compliant deployment architectures. These sovereign AI platforms also support national innovation ecosystems and research programs requiring secure computing environments.

Edge AI Infrastructure for Smart Cities and Industrial Automation

Deployment of edge AI infrastructure across smart city systems, transportation networks, manufacturing environments, and connected public services is creating significant growth opportunities for distributed AI computing platforms throughout the United Kingdom. Real-time analytics for traffic management, energy optimization, public safety, and urban monitoring requires localized AI processing near data sources rather than centralized cloud regions. Industrial automation and robotics systems depend on low-latency AI inference capabilities integrated with operational technology environments. Telecom operators and infrastructure providers are deploying edge computing nodes integrated with 5G networks to support distributed AI applications. Public infrastructure modernization programs and smart city initiatives stimulate demand for localized AI processing platforms. Edge AI also enables privacy-preserving data processing by keeping sensitive information within local jurisdictions. Standardized edge orchestration technologies simplify deployment and management of distributed AI nodes.

Future Outlook

The UK AI Infrastructure Market is expected to expand steadily as national AI strategy implementation, enterprise generative AI adoption, and sovereign cloud initiatives accelerate infrastructure deployment. Hyperscale providers and domestic operators will expand GPU data centers and AI cloud platforms across regions. Edge AI and 5G integration will support distributed intelligent systems. Government investment and regulatory alignment will strengthen domestic AI computing capability.

Major Players

- Amazon Web Services

- Microsoft

- Google Cloud

- NVIDIA

- IBM

- Oracle

- Intel

- Equinix

- Digital Realty

- Arm

- Graphcore

- Hewlett Packard Enterprise

- Dell Technologies

- Cisco Systems

- Atos

Key Target Audience

- AI infrastructure providers

- Cloud service providers

- Telecom operators

- Data center developers

- Enterprise AI adopters

- Semiconductor and hardware manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables including AI infrastructure spending, GPU deployment capacity, AI cloud adoption, enterprise AI workload intensity, and regional data center expansion were defined. Supply indicators such as provider revenue, AI hardware shipments, and data center footprint were mapped. Demand indicators across industries and research sectors were incorporated to ensure comprehensive market representation.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed through triangulation of provider financial data, UK digital infrastructure investment statistics, enterprise AI adoption benchmarks, and data center capacity datasets. Segment shares were estimated based on infrastructure deployment patterns and AI workload distribution.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with AI infrastructure architects, cloud engineers, data center strategists, and enterprise AI adoption specialists. Technology adoption patterns, infrastructure requirements, and regulatory impacts were cross-checked against real implementation experience. Expert insights refined assumptions on segment dominance and growth drivers.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative insights were synthesized into structured market intelligence covering size, segmentation, competitive dynamics, and strategic outlook. Consistency checks ensured alignment between AI adoption trends, infrastructure expansion, and policy frameworks. The final output integrates analytical modeling with strategic interpretation for decision-grade market understanding.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

National AI strategy and public funding initiatives

Enterprise adoption of generative AI and analytics

Expansion of sovereign and secure AI compute capacity - Market Challenges

Limited power and data center capacity in key regions

High cost of advanced AI accelerators and systems

Data governance and privacy compliance complexity - Market Opportunities

Development of sovereign AI cloud platforms

AI infrastructure for regulated industry workloads

Expansion of regional AI compute clusters - Trends

Rapid growth of GPU dense AI data centers

Shift toward liquid cooling and high density racks

Integration of AI infrastructure with edge networks - Government regulations

UK AI governance and safety frameworks

Data protection and residency regulations

Energy and sustainability standards for data centers - SWOT analysis

- Porters Five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AI Training Compute Infrastructure

AI Inference and Edge Infrastructure

AI Storage and Data Pipeline Infrastructure

AI Networking and Interconnect Infrastructure

AI Software Stack and Orchestration Infrastructure - By Platform Type (In Value%)

Hyperscale AI Cloud Platforms

Enterprise Private AI Clusters

Colocation AI Ready Data Centers

Edge AI and 5G Integrated Platforms

Government and Sovereign AI Platforms - By Fitment Type (In Value%)

Greenfield AI Data Center Deployments

Retrofit of Existing Data Centers for AI

On Premise AI Cluster Installations

Modular and Containerized AI Infrastructure

Hybrid AI Cloud Integration - By End User Segment (In Value%)

Financial Services and Fintech Firms

Healthcare and Life Sciences Organizations

Public Sector and Defense Agencies

Telecom and Digital Service Providers

- Market Share Analysis

- Cross Comparison Parameters (AI Compute Density and Performance, Accelerator Portfolio and Architecture Support, Data Center Power and Cooling Capacity, High Speed Interconnect and Networking Capability, AI Software and Framework Ecosystem, Sovereign and Regulatory Compliance Readiness)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

NVIDIA

AMD

Intel

Arm

Graphcore

Google Cloud

Microsoft Azure

Amazon Web Services

Oracle

IBM

Equinix

Digital Realty

Schneider Electric

Hewlett Packard Enterprise

Dell Technologies

- Financial sector deploying AI for risk and analytics workloads

- Healthcare institutions scaling AI diagnostics infrastructure

- Public sector investing in sovereign AI capabilities

- Telecom operators integrating AI with 5G and edge networks

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now