Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the UK courier express parcel logistics industry generated approximately USD ~ billion in total service revenue according to datasets published by Ofcom and logistics industry statistics from the UK government and transport authorities. Market demand is primarily driven by expanding digital retail ecosystems, rising parcel volumes from online marketplaces, and increasing requirements for time-definite delivery services across commercial and residential logistics networks. Advanced parcel sorting infrastructure, automated distribution hubs, and integrated logistics platforms continue strengthening operational efficiency across national courier networks.

London, Birmingham, Manchester, and Leeds represent the most dominant logistics hubs within the UK courier express parcel market due to dense consumer populations, advanced transport connectivity, and large concentrations of e-commerce fulfillment centers. These cities host major parcel sorting hubs, air cargo gateways, and urban micro-distribution facilities that support rapid parcel movement across metropolitan areas. Strong motorway infrastructure and international cargo connectivity through Heathrow and East Midlands airports enable efficient domestic and cross-border parcel distribution throughout the national logistics network.

Market Segmentation

By Product Type

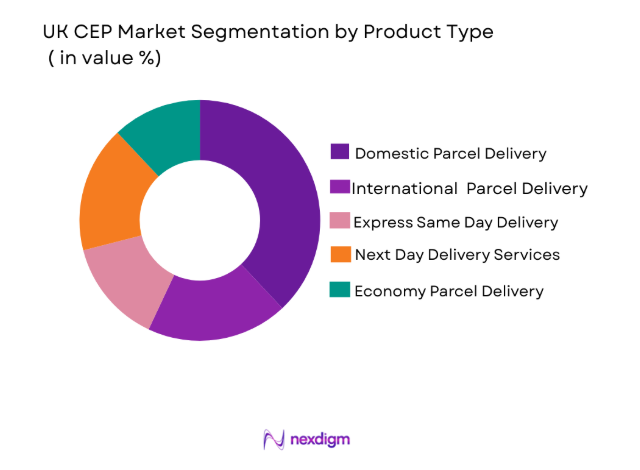

UK CEP market is segmented by product type into domestic parcel delivery, international parcel delivery, express same day delivery, next day delivery services, and economy parcel delivery. Recently, domestic parcel delivery has a dominant market share due to factors such as large national e-commerce shipment volumes, extensive courier distribution networks, and strong consumer reliance on home delivery services for retail goods. Domestic shipments generate the highest parcel flow as retailers and logistics operators maintain nationwide last-mile delivery infrastructure connecting fulfillment centers with residential neighborhoods and commercial districts.

By Platform Type

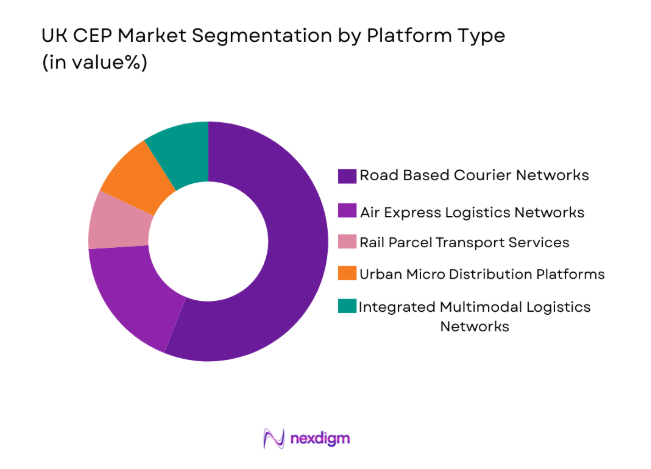

UK CEP market is segmented by platform type into road-based courier networks, air express logistics networks, rail parcel transport services, urban micro-distribution platforms, and integrated multimodal logistics networks. Recently, road-based courier networks have a dominant market share due to widespread national highway connectivity, dense urban delivery routes, and the operational flexibility required for last-mile parcel distribution. Courier companies rely heavily on road transportation fleets including vans, electric delivery vehicles, and motorcycle couriers to efficiently deliver parcels directly to consumers and businesses across metropolitan and regional locations.

Competitive Landscape

The UK CEP market is moderately consolidated with several international logistics providers and domestic courier companies dominating parcel delivery infrastructure across the country. Major companies operate large automated parcel sorting hubs, integrated transportation fleets, and digital logistics platforms that enable high-volume shipment processing. Competitive differentiation is driven by delivery speed, national coverage, technology integration, and last-mile logistics capabilities.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Delivery Network Size |

| Royal Mail Group | 1516 | London, UK | ~ | ~ | ~ | ~ | ~ |

| DPD UK | 1970 | Buckinghamshire, UK | ~ | ~ | ~ | ~ | ~ |

| DHL Parcel UK | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| UPS UK | 1907 | Atlanta, USA | ~ | ~ | ~ | ~ | ~ |

| Evri | 1974 | Leeds, UK | ~ | ~ | ~ | ~ | ~ |

UK CEP Market Analysis

Growth Drivers

Expansion of E Commerce Retail Logistics and Digital Marketplace Fulfillment

Rapid expansion of digital retail platforms and online marketplace ecosystems significantly strengthens parcel shipment volumes within the UK courier express parcel market. Online retail platforms generate extremely high order volumes requiring reliable logistics infrastructure connecting distribution centers with residential consumers. Logistics companies continuously expand automated parcel sorting hubs, regional fulfillment warehouses, and last mile delivery fleets to handle growing shipment volumes efficiently. Retail companies increasingly partner with third party logistics providers capable of managing complex nationwide distribution networks. Mobile commerce platforms and digital payment systems further simplify purchasing behavior, encouraging frequent online retail transactions across consumer segments. Logistics providers also deploy route optimization software and predictive analytics to improve delivery efficiency and fleet productivity across metropolitan delivery routes. As digital retail continues expanding across the UK economy, courier express parcel services remain essential logistics infrastructure supporting national e commerce supply chains and consumer delivery expectations.

Increasing Demand for Time Definite and Same Day Delivery Services

Consumer expectations for faster delivery times have become a major driver shaping operational strategies across the UK courier express parcel market. Online shoppers increasingly demand same day and next day parcel delivery services for retail products including electronics, clothing, groceries, and household goods. Logistics providers respond by investing heavily in urban micro distribution centers and automated sorting facilities designed to accelerate parcel processing speeds. Technology platforms supporting real time shipment tracking and route optimization allow courier companies to complete deliveries more efficiently across densely populated urban regions. Retail companies also integrate order management systems with logistics networks to ensure rapid parcel dispatch following customer purchases. Advanced warehouse robotics and automated packaging systems help reduce handling time within fulfillment centers. These technological and operational improvements allow logistics providers to maintain competitive delivery speeds while managing high parcel volumes generated by expanding online retail demand.

Market Challenges

Rising Transportation Costs and Fuel Price Volatility

Increasing transportation expenses represent one of the most significant operational challenges facing courier express parcel logistics providers operating across the UK. Delivery companies depend heavily on vehicle fleets for last mile distribution activities across urban and regional logistics networks. Rising fuel prices increase the operational cost of maintaining large delivery fleets and transportation infrastructure required to support parcel distribution. Logistics providers must therefore carefully manage route planning, fleet utilization, and fuel consumption to maintain cost efficiency across delivery operations. Urban traffic congestion also increases vehicle idle time and delivery route delays, further increasing transportation expenses across logistics networks. Courier companies continue investing in electric delivery vehicles and route optimization software designed to reduce fuel consumption and improve delivery productivity. However, the transition toward sustainable transportation infrastructure requires significant capital investment and operational adjustments within existing delivery networks.

Urban Congestion and Last Mile Delivery Infrastructure Limitations

Urban congestion across major UK metropolitan regions significantly complicates last mile delivery operations within the courier express parcel logistics market. High population density and limited urban road capacity create logistical challenges for delivery vehicles operating within city centers. Delivery companies often face restricted access zones, parking limitations, and traffic delays that reduce operational efficiency. Increasing parcel shipment volumes generated by e commerce further intensify pressure on urban logistics infrastructure. Courier companies therefore invest in micro fulfillment centers and parcel locker networks located within city districts to shorten delivery distances. Some logistics providers also deploy bicycle couriers and electric cargo vehicles capable of navigating congested urban environments more efficiently. Despite these innovations, last mile delivery operations remain one of the most complex and cost intensive aspects of courier logistics services.

Opportunities

Expansion of Automated Parcel Sorting Infrastructure and Robotics

Automation technologies represent a major opportunity for improving operational efficiency across the UK courier express parcel market. Logistics providers increasingly deploy automated parcel sorting systems, robotics assisted warehouse operations, and artificial intelligence driven logistics management platforms. Automated sorting hubs allow courier companies to process extremely high parcel volumes with greater accuracy and reduced labor requirements. Robotics systems assist with parcel handling, packaging, and order processing within large fulfillment warehouses. These technologies significantly improve operational productivity while reducing human error within parcel processing workflows. Logistics providers investing in automation infrastructure are able to accelerate parcel throughput and maintain competitive delivery speeds. As parcel shipment volumes continue expanding due to digital commerce growth, automated logistics infrastructure will become essential for managing high capacity parcel distribution networks.

Growth of Sustainable Logistics and Electric Delivery Vehicle Adoption

Environmental sustainability initiatives create significant opportunities for innovation within the UK courier express parcel logistics industry. Government policies promoting carbon emission reductions encourage logistics companies to adopt electric delivery vehicles and low emission transportation technologies. Electric van fleets reduce operational fuel costs while supporting sustainability goals across urban logistics networks. Courier companies also invest in green logistics initiatives including energy efficient distribution centers and optimized delivery routing systems designed to reduce carbon emissions. Sustainable logistics strategies also improve corporate environmental reputation among retail partners and consumers. As regulatory pressure and environmental awareness continue increasing, adoption of electric vehicle fleets and sustainable logistics infrastructure will play an increasingly important role in shaping the future of parcel delivery operations.

Future Outlook

The UK CEP market is expected to experience continued expansion as e-commerce retail logistics volumes increase and consumers demand faster parcel delivery services. Technology integration including automated warehouses, artificial intelligence route optimization, and electric vehicle logistics networks will significantly transform parcel distribution infrastructure. Government sustainability initiatives and urban logistics planning will further encourage adoption of low emission delivery systems. Growing cross border e-commerce and international parcel shipments are also expected to strengthen logistics demand across national courier networks.

Major Players

- Royal Mail Group

- DPD UK

- Evri

- DHL Parcel UK

- UPS UK

- FedEx Express UK

- Parcelforce Worldwide

- Yodel Delivery Network

- TNT Express UK

- CitySprint

- DX Group

- UK Mail

- APC Overnight

- Whistl

- Amazon Logistics

Key Target Audience

- E-commerce retailers

- Manufacturing and industrial companies

- Pharmaceutical and healthcare companies

- Logistics and parcel delivery companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Retail distribution companies

Research Methodology

Step 1: Identification of Key Variables

Researchers identified key market variables including parcel shipment volumes, logistics infrastructure capacity, transportation networks, and digital commerce demand indicators. Data sources included government trade statistics, logistics industry databases, and company financial disclosures.

Step 2: Market Analysis and Construction

Market sizing and structural analysis were conducted using multiple data triangulation techniques combining logistics sector revenue datasets, parcel shipment statistics, and supply chain infrastructure indicators.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from logistics companies, supply chain analysts, and transportation specialists validated research assumptions and operational trends shaping the courier express parcel industry.

Step 4: Research Synthesis and Final Output

All collected data and validated insights were synthesized into a comprehensive market report outlining structural dynamics, competitive positioning, technology trends, and long term growth opportunities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid Expansion of E Commerce Retail and Digital Marketplace Platforms

Increasing Demand for Same Day and Time Definite Parcel Delivery Services

Growth of Cross Border E Commerce and International Trade Shipments - Market Challenges

Rising Transportation Costs and Fuel Price Volatility

Urban Congestion and Last Mile Delivery Infrastructure Constraints

Labor Shortages in Logistics and Delivery Operations - Market Opportunities

Adoption of Electric Delivery Vehicles for Sustainable Urban Logistics

Expansion of Automated Parcel Sorting Hubs and Smart Locker Networks

Growth of Cross Border Parcel Services Supporting Online Retail Exports - Trends

Integration of Artificial Intelligence and Route Optimization Systems in Delivery Networks

Expansion of Automated Parcel Locker Infrastructure Across Urban Areas - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Domestic Parcel Delivery Services

International Parcel Delivery Services

Express Same Day Delivery Services

Economy Standard Delivery Services

Time Definite Delivery Services - By Platform Type (In Value%)

Road Based Courier Networks

Air Express Delivery Networks

Rail Integrated Parcel Transport

Urban Micro Distribution Platforms

Integrated Multimodal Logistics Platforms - By Fitment Type (In Value%)

Business to Business Delivery Services

Business to Consumer Delivery Services

Consumer to Consumer Parcel Services

Cross Border E Commerce Parcel Services - By End User Segment (In Value%)

E Commerce Retailers

Manufacturing and Industrial Shippers

Healthcare and Pharmaceutical Companies

- Market Share Analysis

- Cross Comparison Parameters (Delivery Speed, Network Coverage, Parcel Volume Capacity, Technology Integration, Pricing Structure, Customer Service Capabilities, Cross Border Logistics Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Royal Mail Group

DPD UK

Evri

UPS UK

FedEx Express UK

DHL Parcel UK

Parcelforce Worldwide

Yodel Delivery Network

TNT Express UK

DX Group

CitySprint

UK Mail

Hermes UK

APC Overnight

Whistl

- E Commerce Retailers Driving High Volume Parcel Shipments Across Urban Regions

- Manufacturing Companies Requiring Reliable Distribution Networks for Spare Parts and Components

- Healthcare Sector Increasing Demand for Secure Medical Parcel Transportation

- SME Businesses Expanding Online Retail Channels Requiring Logistics Support

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now