Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UK cloud infrastructure market reflects sustained enterprise digitalization and hyperscale data center expansion across compute, storage, and networking platforms supporting public and private cloud deployment models. Based on a recent historical assessment, the market size is approximately USD ~ billion, driven by rapid cloud adoption across financial services, retail, healthcare, and government digital transformation programs. Hyperscale provider investments and colocation expansion further strengthen national cloud infrastructure capacity and service delivery ecosystems.

London dominates cloud infrastructure deployment due to financial sector demand, dense connectivity networks, and concentration of hyperscale data centers and cloud regions. Surrounding areas including Slough, Manchester, and Dublin-linked connectivity corridors support secondary infrastructure clusters due to land availability and power capacity. Strong subsea cable connectivity and proximity to European markets reinforce regional significance. Enterprise headquarters concentration and digital economy scale sustain long-term infrastructure utilization across the United Kingdom cloud ecosystem.

Market Segmentation

By Deployment Type

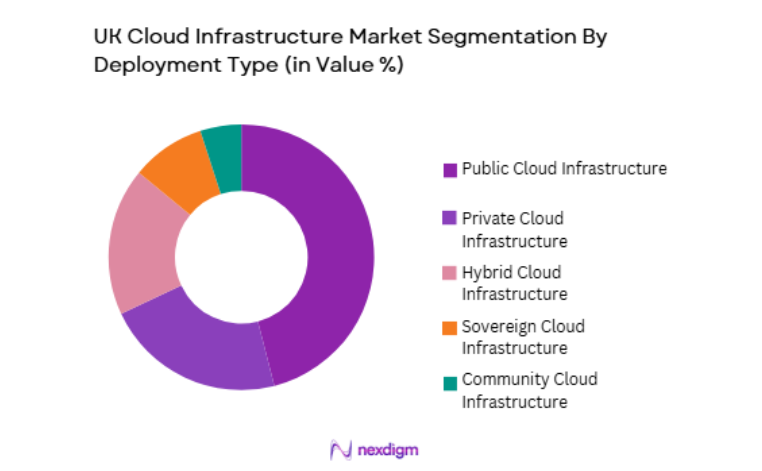

UK Cloud Infrastructure Market is segmented by deployment type into public cloud infrastructure, private cloud infrastructure, hybrid cloud infrastructure, community cloud infrastructure, and sovereign cloud infrastructure. Recently, public cloud infrastructure has a dominant market share due to large-scale enterprise migration, hyperscale provider presence, and scalable consumption-based service models aligned with UK digital transformation priorities. Major hyperscale firms operate multiple availability zones and regions across London and surrounding data center corridors, ensuring high reliability and latency optimization for enterprises. Public cloud platforms offer advanced analytics, AI, and platform services that reduce internal infrastructure requirements for organizations. Government cloud-first policies and regulated sector adoption further reinforce public cloud utilization.

By End-Use Industry

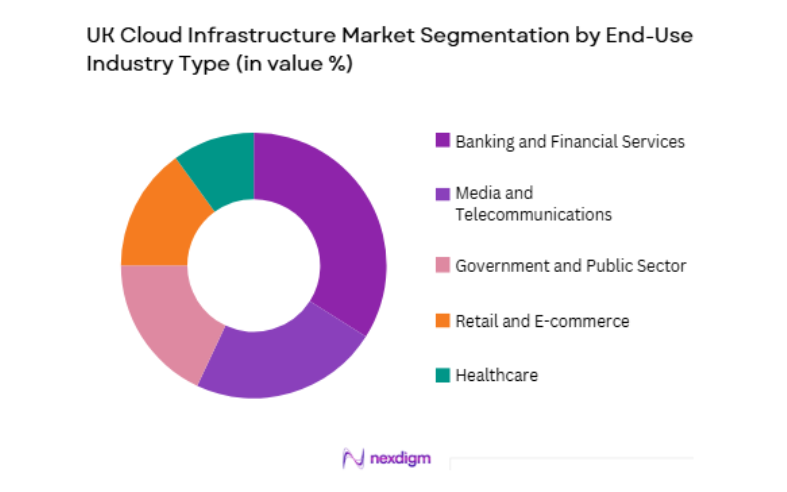

UK Cloud Infrastructure Market is segmented by end-use industry into banking and financial services, retail and e-commerce, healthcare, government and public sector, and media and telecommunications. Recently, banking and financial services has a dominant market share due to strong digital banking transformation, fintech ecosystem expansion, and regulatory-compliant cloud adoption across transaction processing, analytics, and cybersecurity workloads. London’s global financial hub status drives large-scale cloud infrastructure utilization for real-time payments, trading platforms, and customer data platforms. Financial institutions increasingly migrate legacy systems to cloud-native architectures requiring scalable compute and storage infrastructure. Regulatory frameworks encouraging operational resilience and disaster recovery further promote multi-region cloud deployment.

Competitive Landscape

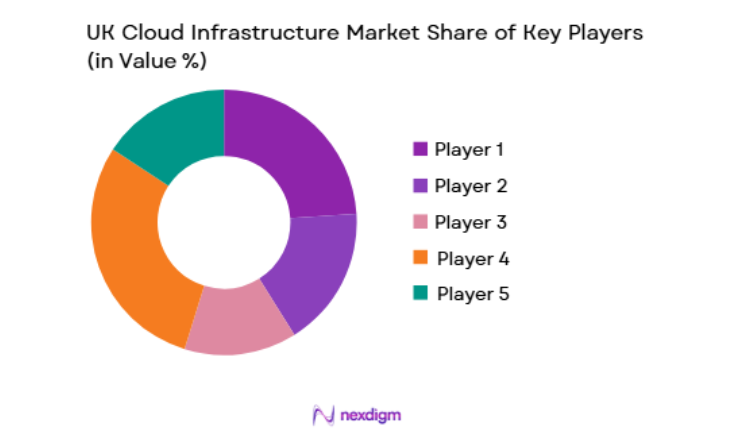

The UK cloud infrastructure market is highly concentrated, dominated by global hyperscale providers alongside major colocation and enterprise cloud vendors operating regional data centers and cloud regions. Hyperscale firms drive infrastructure investment and service innovation, while colocation providers supply interconnection-rich facilities supporting hybrid and enterprise deployments. Strong competition exists in enterprise cloud services, sovereign cloud solutions, and regulated industry hosting across the United Kingdom.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | UK Cloud Regions |

| Amazon Web Services | 2006 | Seattle, USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft Azure | 2010 | Redmond, USA | ~ | ~ | ~ | ~ | ~ |

| Google Cloud | 2008 | Mountain View, USA | ~ | ~ | ~ | ~ | ~ |

| Equinix | 1998 | California, USA | ~ | ~ | ~ | ~ | ~ |

| Digital Realty | 2004 | Texas, USA | ~ | ~ | ~ | ~ | ~ |

UK Cloud Infrastructure Market Analysis

Growth Drivers

Enterprise Digital Transformation and Cloud-Native Application Adoption

UK organizations across financial services, retail, healthcare, and public sector increasingly migrate legacy IT systems toward cloud-native architectures requiring scalable compute, storage, and networking infrastructure integrated with analytics and AI services delivered through hyperscale cloud platforms. Cloud adoption enables operational agility, faster service deployment, and cost optimization compared with on-premise infrastructure. Financial institutions modernize core banking and payments systems on cloud platforms. Retail and e-commerce firms adopt cloud for omnichannel commerce and data analytics. Healthcare providers deploy cloud-based patient data and diagnostics systems. Public sector digital services expand cloud hosting requirements. Start-ups rely on public cloud for rapid scaling and global reach. Hybrid architectures integrate enterprise private and public cloud resources. Continuous application modernization drives sustained infrastructure demand. These factors collectively accelerate UK cloud infrastructure expansion nationwide.

Hyperscale Data Center Expansion and Connectivity Ecosystem Growth

Global hyperscale cloud providers continuously expand UK data center regions and availability zones supported by dense fiber networks, subsea cable connectivity, and interconnection-rich colocation hubs enabling low-latency cloud services for enterprises and digital platforms across domestic and international markets. London and Slough corridors host major hyperscale facilities. Edge data centers expand regional cloud delivery capacity. Connectivity ecosystems enable multi-cloud and hybrid deployments. Colocation providers integrate hyperscale on-ramps. High-bandwidth networks support AI and analytics workloads. International connectivity strengthens global cloud service delivery. Energy-efficient data center technologies enable scalable infrastructure. Power availability planning supports expansion. These investments significantly strengthen UK cloud infrastructure capabilities.

Market Challenges

Data Sovereignty, Regulatory Compliance, and Security Assurance Requirements

UK cloud infrastructure deployment faces stringent regulatory requirements across financial services, healthcare, and government sectors mandating data residency, cybersecurity assurance, and operational resilience compliance influencing cloud architecture design, provider selection, and infrastructure localization strategies across the national market. Sensitive data handling rules limit cross-border cloud deployment. Sovereign cloud requirements increase infrastructure costs. Compliance certification timelines extend deployment cycles. Security audits and encryption standards raise operational complexity. Regulated sectors require multi-region redundancy. Vendor lock-in concerns affect provider choice. Data protection legislation shapes infrastructure location decisions. Government procurement frameworks impose compliance barriers. Security incident risks influence adoption pace. These constraints complicate cloud infrastructure scaling nationwide.

Power Availability, Sustainability Constraints, and Data Center Planning Approvals

UK cloud infrastructure expansion depends heavily on reliable power supply, renewable energy integration, and planning approvals for large-scale data centers, creating capacity constraints in key regions such as London and Slough where land, grid connectivity, and environmental regulations affect facility development timelines and investment feasibility. Data centers require high energy density infrastructure. Grid capacity limitations delay new facilities. Renewable energy procurement increases costs. Planning regulations restrict site expansion. Environmental sustainability standards raise compliance complexity. Cooling infrastructure requirements intensify land constraints. Urban density limits hyperscale campus development. Community opposition affects approvals. Power pricing volatility impacts operating costs. These factors restrict rapid cloud infrastructure growth.

Opportunities

Sovereign and Regulated Industry Cloud Infrastructure Expansion

Increasing demand for sovereign, compliant cloud environments across government, defense, healthcare, and financial services sectors creates significant opportunities for localized UK cloud infrastructure deployment with enhanced security, data residency, and operational control aligned with national digital sovereignty policies and regulated industry transformation requirements. Public sector digitalization requires sovereign hosting. Defense systems need secure cloud environments. Financial regulators encourage domestic data processing. Healthcare data protection drives local infrastructure. Hyperscale providers develop sovereign offerings. Partnerships with local data center operators expand capacity. Certification frameworks support compliance infrastructure. Domestic hosting strengthens national resilience. Enterprise demand for compliant cloud grows. These trends enable sovereign cloud infrastructure expansion.

Edge Computing and AI-Optimized Cloud Infrastructure Development

Growth in artificial intelligence, real-time analytics, and latency-sensitive applications across media, telecom, autonomous systems, and industrial automation creates opportunities for distributed edge cloud infrastructure deployment across UK regions complementing centralized hyperscale facilities and enabling advanced digital services and emerging technology ecosystems nationwide. AI workloads require specialized compute infrastructure. Edge nodes reduce latency for digital services. Telecom networks integrate edge cloud platforms. Smart city applications need local processing. Autonomous systems depend on distributed computing. Industrial IoT expands regional cloud demand. Media streaming requires edge delivery. Regional data centers support resilience. Hybrid cloud architectures integrate edge nodes. These drivers support edge cloud infrastructure growth.

Future Outlook

The UK cloud infrastructure market is expected to grow steadily over the next five years, driven by enterprise digital transformation, AI adoption, and hyperscale data center expansion. Sovereign cloud and regulated sector hosting will expand domestic infrastructure deployment. Edge computing and distributed cloud architectures will complement centralized hyperscale regions. Sustainability requirements and power infrastructure planning will shape data center development strategies nationwide.

Major Players

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- IBM Cloud

- Oracle Cloud

- Equinix

- Digital Realty

- NTT Global Data Centers

- CyrusOne

- OVHcloud

- Alibaba Cloud

- Colt Data Centre Services

- Telehouse

- Global Switch

- Rackspace

Key Target Audience

- Enterprises and large corporations

- Banking and financial institutions

- Telecommunications operators

- Media and digital platforms

- Healthcare providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- E-commerce companies

Research Methodology

Step 1: Identification of Key Variables

Key variables including data center capacity, hyperscale investments, cloud adoption rates, deployment models, and regional infrastructure distribution were identified from industry reports, company disclosures, and government digital policy documents. Sectoral demand across finance, telecom, retail, and public sector was mapped to infrastructure requirements. Technology trends in AI and edge computing were incorporated.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using secondary data from cloud provider financials, data center capacity announcements, regulatory filings, and digital economy statistics. Regional infrastructure clusters and deployment models were benchmarked. Segment shares were estimated based on workload distribution and sector adoption patterns across the United Kingdom.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with cloud architects, data center planners, and enterprise IT leaders across finance, telecom, and public sectors. Infrastructure growth assumptions and regulatory impacts were refined through expert feedback. Technology adoption trends and deployment preferences were cross-checked against practitioner insights.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative inputs were synthesized into a structured market model integrating infrastructure capacity, demand drivers, segmentation shares, and competitive dynamics. Regional and regulatory influences were incorporated into growth projections. Final outputs were reviewed for alignment with national digital strategy and cloud adoption trends.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Accelerating enterprise digital transformation and cloud migration across UK industries

Expansion of sovereign and regulated cloud demand in public and financial sectors

Rising AI and data intensive workloads driving scalable cloud infrastructure adoption - Market Challenges

Data sovereignty and compliance complexity across multi cloud environments

High energy costs and sustainability requirements for large scale data centers

Vendor lock in risks and interoperability limitations across cloud platforms - Market Opportunities

Growth of sovereign cloud and secure government cloud infrastructure programs

Expansion of edge cloud to support low latency industrial and AI applications

Modernization of legacy enterprise IT into hybrid and multi cloud architectures - Trends

Adoption of multi cloud and hybrid cloud operating models across enterprises

Integration of AI optimized cloud infrastructure and GPU cloud services

Shift toward sustainable and energy efficient cloud data center design - Government regulations

UK data protection and sovereignty regulations affecting cloud hosting models

National cybersecurity and critical infrastructure protection standards

Energy efficiency and carbon reporting requirements for data centers - SWOT analysis

- Porters Five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Public Cloud Infrastructure

Private Cloud Infrastructure

Hybrid Cloud Infrastructure

Multi Cloud Management Platforms

Cloud Native Infrastructure Stacks - By Platform Type (In Value%)

Hyperscale Cloud Data Centers

Enterprise On Premise Cloud

Colocation Cloud Platforms

Edge Cloud Infrastructure

Sovereign and Government Cloud - By Fitment Type (In Value%)

Greenfield Cloud Deployments

Brownfield Data Center Modernization

Containerized Cloud Modules

Software Defined Cloud Stacks

Managed Cloud Infrastructure - By End User Segment (In Value%)

Financial Services Institutions

Public Sector and Government Agencies

Telecom and Media Companies

- Market Share Analysis

- Cross Comparison Parameters (Service Portfolio Breadth, Data Center Footprint, Compliance Certifications, Deployment Model Flexibility, Pricing Model, Network Connectivity, Managed Services Depth, AI Infrastructure Integration, Sovereign Cloud Capability, Ecosystem Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Amazon Web Services

Microsoft

Google Cloud

IBM

Oracle

Alibaba Cloud

OVHcloud

Equinix

Digital Realty

NTT

Fujitsu

Atos

BT Group

Rackspace Technology

Capgemini

- Financial institutions adopting hybrid cloud for regulated workloads and analytics

- Government agencies deploying sovereign cloud for secure digital services

- Telecom operators integrating edge cloud for 5G and low latency applications

- Healthcare organizations migrating data platforms to compliant cloud environments

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now