Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the UK Cold Chain Logistics Market generated approximately USD ~ billion in revenue supported by rising demand for temperature controlled logistics across pharmaceutical distribution, frozen food transportation, and perishable retail supply chains. Expanding biologics shipments, vaccine transportation networks, and frozen food consumption continue strengthening demand for refrigerated transportation fleets and temperature controlled warehousing infrastructure across national logistics networks. Increased investment in pharmaceutical manufacturing, online grocery retail distribution, and cold storage infrastructure further contributes to steady logistics demand.

Major logistics hubs including London, Birmingham, Manchester, and Liverpool dominate cold chain logistics activities due to their extensive transportation connectivity, large pharmaceutical distribution networks, and proximity to major retail distribution centers. These metropolitan regions host advanced refrigerated warehouses, pharmaceutical distribution facilities, and international cargo gateways that support temperature controlled imports and exports. Port cities such as Felixstowe and Southampton also strengthen cold chain logistics operations by facilitating large volumes of refrigerated container shipments entering national food and pharmaceutical supply chains.

Market Segmentation

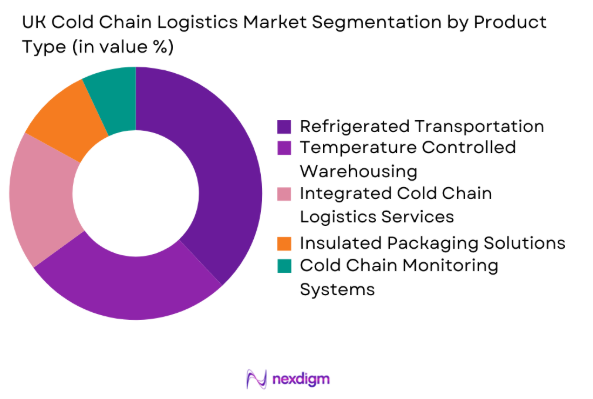

By Product Type

UK Cold Chain Logistics market is segmented by product type into refrigerated transportation, temperature controlled warehousing, cold chain monitoring systems, insulated packaging solutions, and integrated cold chain logistics services. Recently, refrigerated transportation has a dominant market share due to factors such as increasing distribution of frozen foods, rising pharmaceutical deliveries requiring strict temperature control, and expanding grocery retail supply chains across the United Kingdom. Retail supermarket networks and pharmaceutical distributors rely heavily on refrigerated truck fleets capable of maintaining controlled temperatures during nationwide distribution operations. Growing demand for home grocery delivery and pharmaceutical logistics further increases reliance on refrigerated vehicles. In addition, expansion of food exports and vaccine distribution programs strengthens the operational importance of refrigerated transportation infrastructure within the broader cold chain logistics ecosystem.

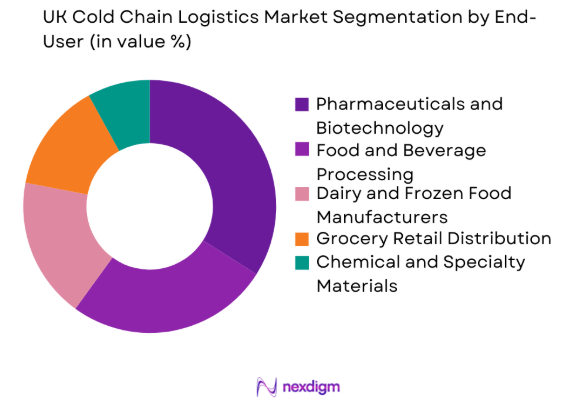

By End User Industry

UK Cold Chain Logistics market is segmented by end user industry into pharmaceuticals and biotechnology, food and beverage processing, dairy and frozen food manufacturers, chemical and specialty materials companies, and grocery retail distribution networks. Recently, pharmaceuticals and biotechnology have a dominant market share due to factors such as stringent regulatory requirements for temperature sensitive medicines, rising biologics manufacturing, and expanding vaccine distribution networks across healthcare systems. Pharmaceutical companies depend on validated temperature controlled transportation and storage systems capable of preserving drug efficacy during distribution. The rapid expansion of biopharmaceutical research and clinical supply chains also increases logistics demand for ultra low temperature transport and storage. As pharmaceutical innovation expands, logistics providers increasingly invest in specialized pharmaceutical warehouses and digital temperature monitoring platforms.

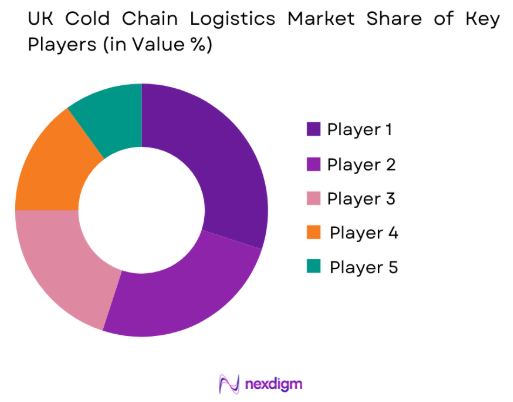

Competitive Landscape

The UK Cold Chain Logistics market demonstrates moderate consolidation with several global logistics companies operating alongside specialized refrigerated logistics providers. Major companies maintain competitive advantages through large refrigerated fleets, extensive temperature controlled warehousing capacity, and advanced digital monitoring technologies that ensure regulatory compliance for pharmaceutical and food shipments. Strategic investments in automated cold storage infrastructure, integrated distribution networks, and pharmaceutical logistics certification strengthen competitive positioning across the national cold chain ecosystem.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Refrigerated Fleet Capacity |

| DHL Supply Chain | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| Kuehne+Nagel | 1890 | Schindellegi, Switzerland | ~ | ~ | ~ | ~ | ~ |

| Lineage Logistics | 2012 | Michigan, USA | ~ | ~ | ~ | ~ | ~ |

| Americold Logistics | 1903 | Georgia, USA | ~ | ~ | ~ | ~ | ~ |

| GXO Logistics | 2021 | Connecticut, USA | ~ | ~ | ~ | ~ | ~ |

UK Cold Chain Logistics Market Analysis

Growth Drivers

Expansion of Pharmaceutical Biologics Distribution and Vaccine Supply Chains

The United Kingdom pharmaceutical sector increasingly depends on advanced temperature controlled logistics infrastructure to transport biologic medicines, vaccines, and specialty pharmaceutical products across national distribution networks. Biologic drugs such as monoclonal antibodies and gene therapies require strict temperature management to maintain stability and therapeutic effectiveness. Pharmaceutical manufacturers rely on certified cold chain logistics providers to maintain validated temperature ranges during distribution to hospitals, pharmacies, and research institutions. Vaccine distribution programs and biotechnology research clusters in Cambridge, Oxford, and London further increase logistics demand. Logistics providers invest in temperature monitoring technologies, digital tracking systems, and specialized pharmaceutical warehouses to ensure regulatory compliance and reliable transportation.

Rapid Growth of Online Grocery Retail and Fresh Food Distribution Networks

Consumer purchasing behavior in the United Kingdom is increasingly shifting toward online grocery platforms and home delivery services, strengthening demand for refrigerated logistics networks capable of transporting perishable food products. Supermarket chains invest in refrigerated truck fleets, automated cold storage warehouses, and digital logistics systems to manage complex distribution networks. Fresh produce, frozen foods, dairy products, and ready meals require strict temperature control to maintain quality during transportation and storage. Logistics providers expand regional cold storage facilities near urban populations to support rapid grocery deliveries. Growing digital grocery platforms and rising frozen food consumption further increase demand for advanced refrigerated logistics infrastructure across national food distribution networks.

Market Challenges

High Capital Investment Requirements for Refrigerated Warehousing and Transportation Infrastructure

Cold chain logistics infrastructure requires substantial capital investment due to the high costs associated with refrigerated transportation fleets, specialized cold storage warehouses, and advanced temperature monitoring technologies. Logistics providers must invest in insulated facilities, industrial refrigeration systems, automated cold storage equipment, and energy intensive cooling technologies to maintain precise temperature conditions for pharmaceutical and food shipments. Additional costs include backup power systems, digital monitoring platforms, and regulatory compliance requirements. Refrigerated transportation fleets also involve higher acquisition and maintenance expenses. Cold storage facilities consume significant electricity, increasing operational costs. Smaller logistics companies often face financial barriers, making expansion of refrigerated logistics infrastructure challenging despite rising demand.

Complex Regulatory Compliance Requirements for Pharmaceutical and Food Logistics

Cold chain logistics providers in the United Kingdom must comply with strict regulatory frameworks governing pharmaceutical distribution, food safety, and temperature controlled transportation. Pharmaceutical logistics requires adherence to Good Distribution Practice guidelines that mandate validated transport conditions, continuous monitoring systems, and detailed shipment documentation. Food supply chains are regulated through strict safety standards requiring precise temperature control for frozen foods, dairy products, and fresh produce during storage and transportation. Compliance involves implementing quality management systems, staff training, and specialized handling procedures. Regulatory inspections, audits, and documentation requirements increase operational complexity. Failure to meet standards can lead to financial penalties, product recalls, and reputational risks for logistics providers.

Opportunities

Expansion of Biopharmaceutical Manufacturing and Clinical Trial Supply Chains

Expansion of biotechnology research and biopharmaceutical manufacturing in the United Kingdom is creating strong opportunities for cold chain logistics providers specializing in pharmaceutical distribution. Biotechnology firms are developing biologics, cell therapies, and gene therapies that require strict temperature controlled transportation and storage across research, clinical trials, and commercial supply chains. Research hubs in Cambridge, Oxford, and London generate high demand for specialized logistics handling clinical materials and sensitive drug compounds. Logistics providers are investing in ultra low temperature storage, advanced monitoring technologies, and pharmaceutical packaging systems. Growing global clinical trials also require integrated logistics networks capable of transporting temperature controlled medical products across international pharmaceutical research supply chains.

Development of Smart Cold Chain Technologies and Automated Refrigerated Warehousing Systems

Rapid technological advancement in automation, digital monitoring systems, and intelligent warehouse technologies is creating new opportunities to modernize cold chain logistics operations across the United Kingdom. Logistics providers are deploying Internet of Things sensors, cloud monitoring platforms, and artificial intelligence analytics to enable real time temperature visibility during storage and transportation. These systems help detect temperature deviations quickly, preventing product spoilage and improving shipment reliability. Automated refrigerated warehouses equipped with robotic pallet handling and high density storage improve operational efficiency. Digital supply chain platforms also strengthen coordination between logistics companies, pharmaceutical manufacturers, and food distributors, enabling optimized routing, improved storage management, and greater resilience across temperature controlled distribution networks.

Future Outlook

The UK Cold Chain Logistics market is expected to experience sustained expansion driven by increasing pharmaceutical innovation, rising demand for temperature sensitive biologics, and continuous growth in frozen food and grocery retail distribution networks. Technological advancements including automated cold storage facilities and digital temperature monitoring platforms will further improve operational efficiency across logistics networks. Regulatory oversight in pharmaceutical and food safety logistics will continue encouraging infrastructure modernization. Growing investment in biotechnology manufacturing and pharmaceutical research supply chains will also strengthen demand for specialized cold chain distribution services.

Major Players

- DHL Supply Chain

- Kuehne+Nagel

- Lineage Logistics

- Americold Logistics

- GXO Logistics

- DB Schenker

- XPO Logistics

- Maersk Logistics & Services

- UPS Healthcare Logistics

- FedEx Logistics

- Culina Group

- Nagel Group

- AGRO Merchants Group

- NewCold

- Turners Soham Ltd

Key Target Audience

- Pharmaceutical manufacturers

- Food and beverage processing companies

- Grocery retail distribution companies

- Cold storage infrastructure developers

- Logistics fleet operators

- Investments and venture capitalist firms

- Government and regulatory bodies

- Biotechnology manufacturing companies

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identification of major industry variables influencing cold chain logistics including pharmaceutical distribution demand, refrigerated transportation capacity, food supply chain infrastructure, and regulatory compliance requirements affecting temperature controlled logistics operations.

Step 2: Market Analysis and Construction

Market structure is analyzed using supply chain data, logistics infrastructure capacity, pharmaceutical distribution volumes, and food logistics demand patterns to construct a comprehensive representation of the cold chain logistics ecosystem.

Step 3: Hypothesis Validation and Expert Consultation

Industry hypotheses are validated through consultations with logistics operators, pharmaceutical supply chain experts, and cold storage infrastructure providers to confirm operational trends and regulatory developments affecting market growth.

Step 4: Research Synthesis and Final Output

All collected data and expert insights are synthesized into a structured market analysis highlighting infrastructure development, logistics demand drivers, competitive landscape dynamics, and strategic opportunities within the cold chain logistics sector.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Pharmaceutical and Vaccine Distribution Networks

Growth of Online Grocery Retail and Fresh Food Delivery

Increasing Demand for Temperature Controlled Food Exports - Market Challenges

High Infrastructure and Energy Costs for Refrigerated Facilities

Complex Regulatory Compliance in Pharmaceutical Logistics

Limited Availability of Skilled Cold Chain Logistics Workforce - Market Opportunities

Expansion of Biopharmaceutical Manufacturing and Clinical Supply Chains

Investment in Automated Cold Storage Warehousing Infrastructure

Adoption of Smart Temperature Monitoring and IoT Enabled Logistics - Trends

Integration of Digital Temperature Monitoring Platforms

Adoption of Automated High Density Cold Storage Warehouses

Expansion of Sustainable Refrigeration Technologies - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Refrigerated Transportation Services

Temperature Controlled Warehousing

Cold Chain Monitoring and Tracking Systems

Insulated Packaging and Thermal Containers

Integrated End to End Cold Chain Logistics - By Platform Type (In Value%)

Road Refrigerated Transport

Air Cargo Cold Chain Logistics

Sea Freight Refrigerated Containers

Rail Based Refrigerated Freight

Multimodal Cold Chain Logistics Platforms - By Fitment Type (In Value%)

Standalone Cold Storage Facilities

Fleet Integrated Refrigeration Units

Portable Refrigeration Containers

IoT Enabled Temperature Monitoring Fitments

Modular Cold Room Installations - By End User Segment (In Value%)

Pharmaceutical and Biotech Companies

Food and Beverage Manufacturers

Dairy and Frozen Food Producers

Chemical and Specialty Material Companies

Retail and E commerce Grocery Distributors - By Procurement Channel (In Value%)

Direct Logistics Service Contracts

Third Party Logistics Providers

Government Healthcare Procurement Programs

Retail Supply Chain Distribution Agreements

Digital Freight and Logistics Platforms

- Market Share Analysis

- Cross Comparison Parameters (Cold Storage Capacity, Refrigerated Fleet Size, Temperature Monitoring Technology, Pharmaceutical Logistics Certification, Geographic Distribution Network)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DHL Supply Chain

Kuehne+Nagel

Lineage Logistics

Americold Logistics

GXO Logistics

DB Schenker

XPO Logistics

Maersk Logistics & Services

UPS Healthcare Logistics

FedEx Logistics

Culina Group

Nagel-Group

AGRO Merchants Group

NewCold

Turners (Soham) Ltd

- Growing Demand from Biopharmaceutical Manufacturers

- Expansion of Supermarket and Grocery Retail Distribution

- Increasing Cold Chain Requirements for Food Exporters

- Rising Logistics Needs for Healthcare and Vaccine Distribution

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now