Download PDF

Download PDFMarket Overview

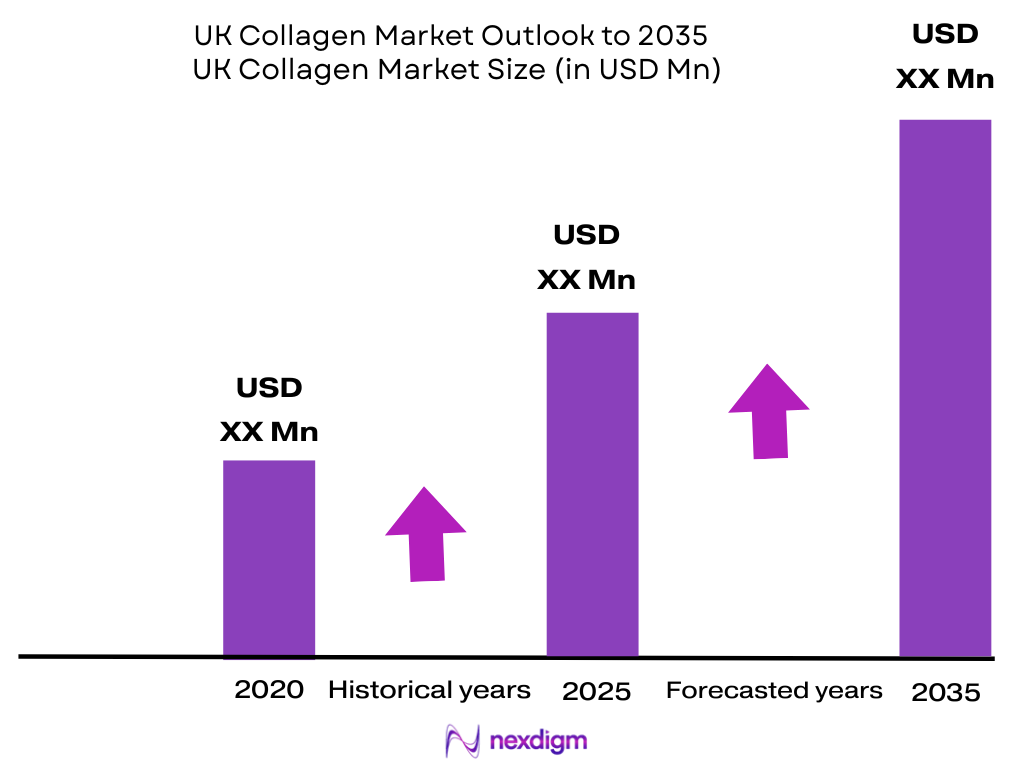

The UK collagen market is valued at USD ~ million, based on a five-year historical analysis, and the available UK country forecast shows 10.5% CAGR in the published forecast period. Demand is driven by gelatin, hydrolyzed collagen, beauty supplements, functional foods, pharmaceutical capsules and healthcare applications. The UK economy moved from 0.4 real GDP growth in the previous base year to 0.9 in the latest base year, supporting consumer health and wellness spending. London, South East England, Manchester, Birmingham, Leeds, Glasgow and Edinburgh dominate UK collagen demand because they combine premium beauty retail, pharmacy networks, e-commerce penetration, sports nutrition users, aesthetic clinics and higher wellness-product visibility. England and Wales reached 61,806,682 residents in the latest base year, increasing by 706,900 from the previous base year; the UK reached 69,281,400 residents, creating a large addressable base for collagen powders, liquid sachets, capsules, gummies and functional foods.

Market Segmentation

By Product Type

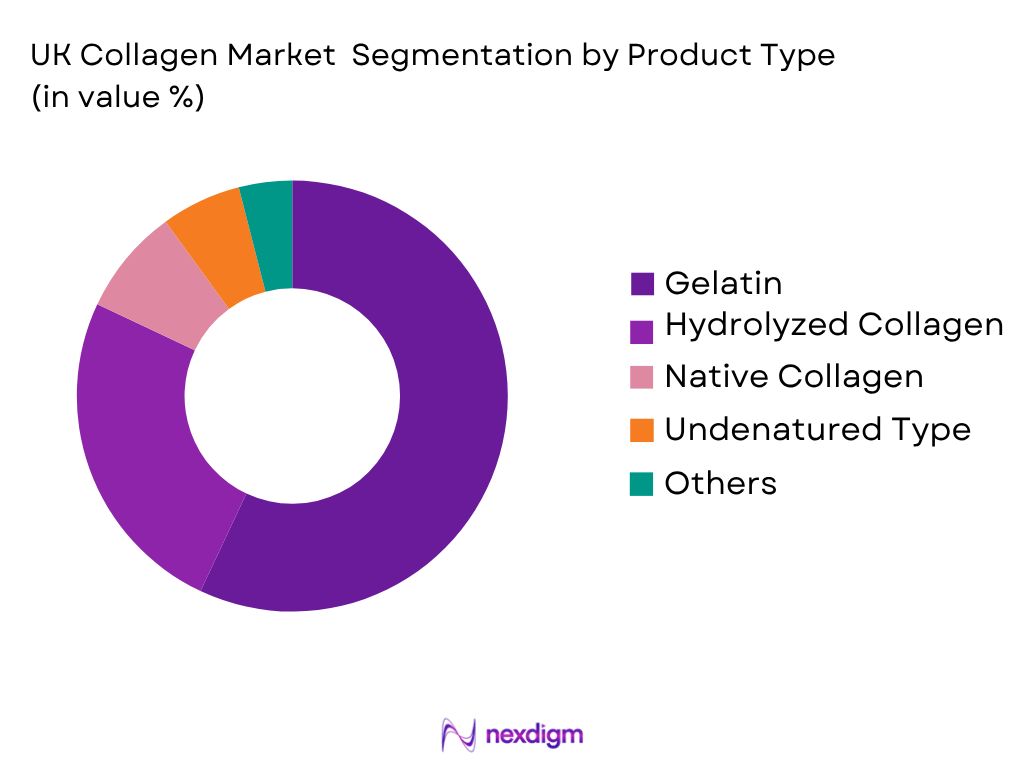

UK collagen market is segmented by product type into gelatin, hydrolyzed collagen, native collagen, undenatured Type II collagen and other collagen products. Recently, gelatin has a dominant market share in the UK under product type, primarily because it is used across food processing, confectionery, gummies, capsules, pharmaceutical shells, dairy desserts, meat products and technical applications. Gelatin has a wider B2B demand base than premium collagen peptides because it is both a functional ingredient and a pharmaceutical excipient. Its gelling, stabilizing, thickening, binding and film-forming properties make it relevant for manufacturers that require texture and structure rather than only beauty or joint-health positioning. Grand View Research identifies gelatin as the largest revenue-generating product segment in the UK collagen market, while hydrolyzed collagen is identified as the fastest-growing product segment because of its use in powders, sachets, beauty supplements and sports nutrition.

By Source

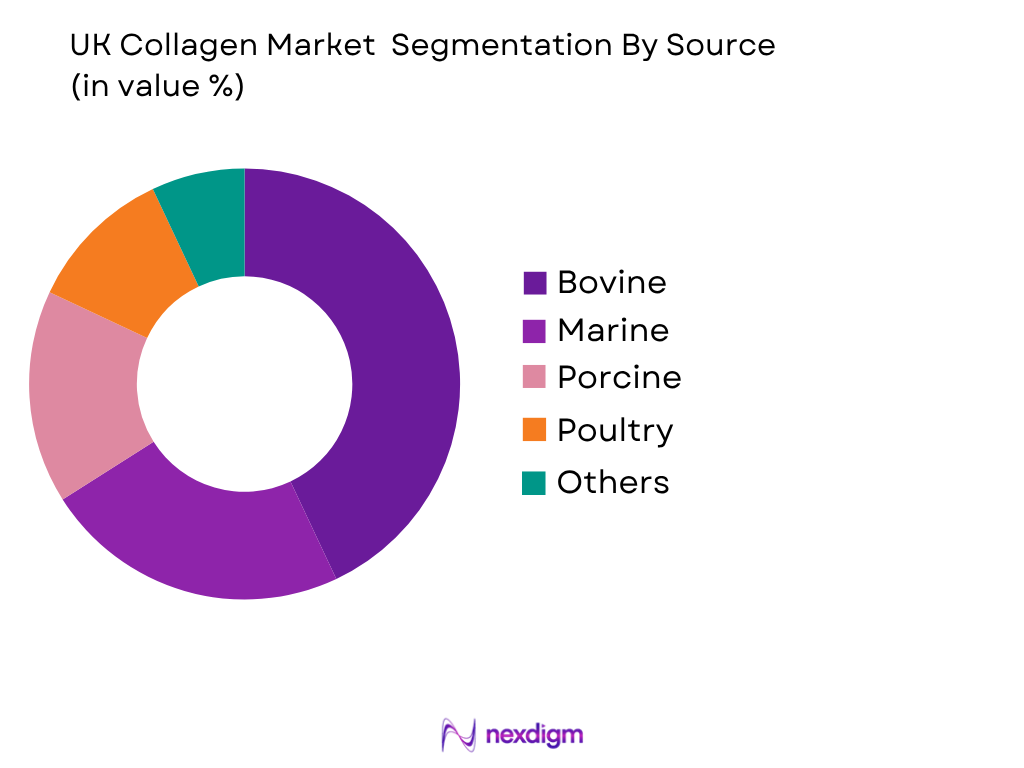

UK collagen market is segmented by source into bovine, marine, porcine, poultry and other sources. Recently, bovine collagen has a dominant market share in the UK under source segmentation because it is cost-effective, scalable and widely used in gelatin, hydrolyzed collagen powders, capsules, gummies and functional food applications. Bovine collagen provides Type I and Type III collagen, enabling brands to position products across skin, hair, nails, bones, joints and sports recovery. It is also more accessible at industrial scale than premium marine collagen, which is stronger in liquid sachets and beauty-from-within formulations. The global collagen market also shows bovine collagen as the largest source category, supported by widespread availability and established extraction processes, which aligns with UK ingredient sourcing patterns where domestic brands often rely on imported bovine and marine peptide inputs.

Competitive Landscape

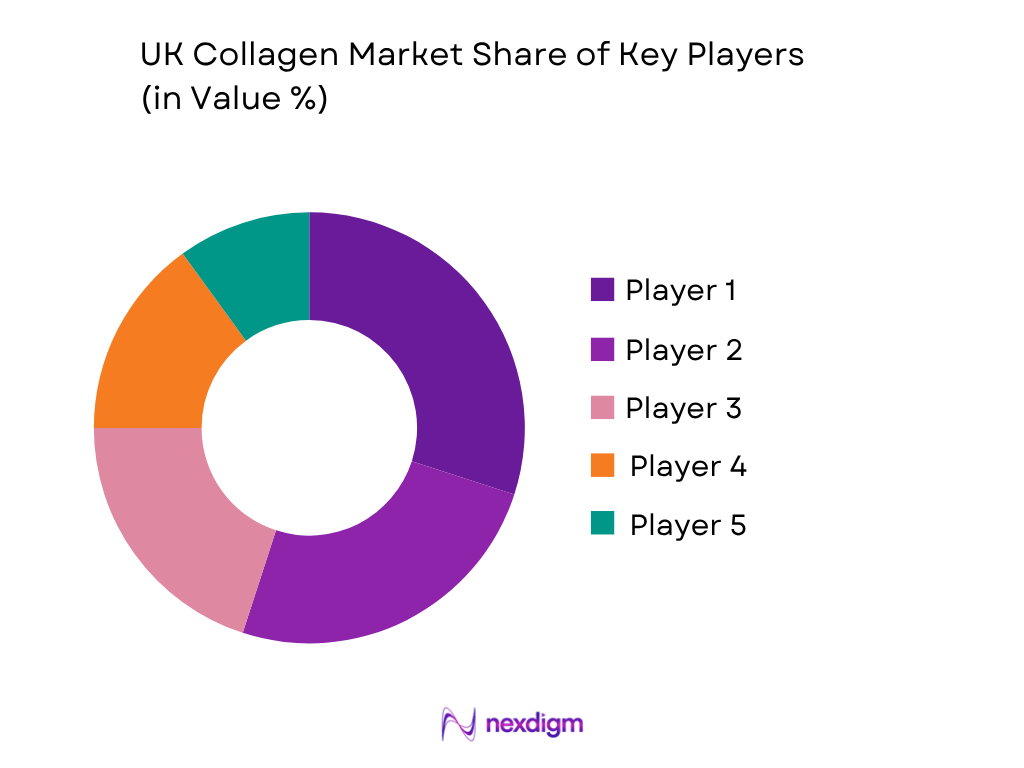

The UK collagen market is competitive across two layers: B2B ingredient supply and consumer-facing supplement brands. Global ingredient suppliers such as Rousselot, GELITA, PB Leiner, Nitta Gelatin and Weishardt influence gelatin and collagen peptide availability, while UK-facing brands compete through marine collagen sachets, bovine collagen powders, beauty claims, clinical positioning, pharmacy listings, Amazon UK visibility and D2C subscriptions. Market concentration is medium, with both multinational ingredient players and digital-first wellness brands shaping category expansion. Mordor Intelligence identifies the UK collagen market as a medium-concentration market, while Grand View Research confirms gelatin as the largest UK product segment.

| Company | Establishment Year | Headquarters | Collagen Portfolio | Main Source Focus | Application Coverage | UK Market Role | Distribution Model | Strategic Strength |

| Rousselot / Darling Ingredients | 1891 | Son, Netherlands / Irving, Texas | ~ | ~ | ~ | ~ | ~ | ~ |

| GELITA AG | 1875 | Eberbach, Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| PB Leiner / Tessenderlo Group | 1870s | Vilvoorde, Belgium | ~ | ~ | ~ | ~ | ~ | ~ |

| Weishardt Group | 1839 | Graulhet, France | ~ | ~ | ~ | ~ | ~ | ~ |

| Revive Collagen | 2020 | London, UK | ~ | ~ | ~ | ~ | ~ | ~ |

UK Collagen Market Analysis

Growth Drivers

Ageing Population Expanding Demand for Joint, Skin and Mobility Collagen Products

The UK collagen market is supported by ageing-led demand for joint mobility, skin elasticity, bone support and active-aging nutrition. The UK population reached 69,281,400 people, with an annual increase of 755,300 people, giving collagen brands a broad health-and-wellness consumer base. ONS also reports that people aged 65 years and over increased across all UK countries, while people aged 90 years and over reached 625,000, strengthening demand for mobility, wound-care, bone-health and senior-wellness products. The World Bank reports UK GDP at USD 3.69 trillion and GDP per capita at USD 53,246.4, supporting premium supplement affordability.

Large Food, Retail and Health-Product Consumption Base Supporting Collagen Formats

The UK collagen market benefits from a large food and health-product ecosystem because gelatin and collagen are used in gummies, capsules, functional foods, protein snacks, beverages and pharmaceutical shells. Defra reports 444,000 employees in food and drink manufacturing, 1,057,000 in food and drink retail, and 3,669,000 employees across the food sector in Great Britain, supporting commercial scale for collagen-based food and supplement formats. The UK population reached 69,281,400, while 1,235,300 people arrived to live in the UK for at least 12 months, widening the consumer base for pharmacy, supermarket, e-commerce and beauty-led collagen distribution.

Market Challenges

Domestic Animal Feedstock Constraints for Bovine and Porcine Collagen Supply

The UK collagen market faces a feedstock challenge because bovine and porcine collagen depend on animal by-products from cattle, pig and meat-processing chains. Defra reports the UK had 9.4 million cattle and calves, 1.3 million beef-herd animals, 1.8 million dairy-herd animals and 4.7 million pigs in 2024. The total cattle and calves base fell from the prior year, while the female pig breeding herd stood at 327,000 animals. This matters for collagen because hides, bones, skins and connective tissues are core inputs for gelatin, hydrolyzed bovine collagen, porcine gelatin capsules and gummies.

Import Certification Burden for Gelatine and Collagen Inputs

The UK collagen market faces regulatory friction because gelatine and collagen intended for human consumption exported to Great Britain must be accompanied by relevant health certificates. Defra lists GBHC430 for gelatine, GBHC431 for collagen, GBHC432 for raw materials, GBHC433 for treated raw materials and GBHC434 for transit or storage of collagen and gelatine raw materials, all required from 30 April 2024. This adds documentation pressure for imported marine collagen, bovine peptides, porcine gelatin and raw materials. The challenge is commercially significant in a USD 3.69 trillion economy where supplement, food and pharmaceutical buyers require compliant cross-border supply.

Market Opportunities

Marine Collagen Expansion Through UK Seafood and Fish-Product Supply Chains

The UK collagen market has an opportunity in marine collagen because fish skin, scales and fish-processing by-products can support premium beauty-from-within products, liquid sachets and collagen beverages. UK Sea Fisheries Statistics report UK vessel landings valued at GBP 1.16 billion in 2024, with landings into the UK by foreign vessels at 22,000 tonnes. The same official report shows UK imports of fish products at 151,500 tonnes, while total UK imports of sea fish, freshwater fish and fish products reached 784,400 tonnes. These flows create an ingredient base for marine collagen extraction, especially for Type I collagen beauty positioning.

Functional Food and Supplement Innovation Through Established Food Manufacturing Capacity

The UK collagen market has an opportunity in functional foods, gummies, beverages, bars and protein-enhanced formats because the national food chain already provides manufacturing, retail and distribution scale. Defra reports 444,000 employees in food and drink manufacturing, 230,000 in food and drink wholesale, 1,057,000 in food and drink retail and 1,938,000 in non-residential catering in Great Britain. Collagen suppliers can use this infrastructure to expand gelatin gummies, collagen drinks, sachet-to-beverage products, fortified dairy desserts and high-protein snacks. The World Bank’s USD 53,246.4 GDP per capita also supports premium nutrition products sold through pharmacies, supermarkets and online channels.

Future Outlook

The UK collagen market is expected to expand steadily, supported by beauty-from-within adoption, active aging, marine collagen premiumization, pharmacy-led supplement sales, e-commerce subscriptions and functional food innovation. The market is expected to reach USD 637.5 million in the published country forecast, with 10.5% CAGR in the available UK collagen market outlook. For the longer UK collagen peptide outlook, published data shows the UK collagen peptide market moving from USD 50.5 million to USD 81.9 million, corresponding to 5.0% CAGR in the long-term forecast period. This peptide-specific outlook is relevant because hydrolyzed collagen peptides are the key premium growth component within powders, liquid sachets, beauty supplements, sports nutrition and joint-health products.

Over the next several years, the strongest growth pockets will come from liquid marine collagen sachets, powder tubs, collagen drinks, multi-collagen blends, gummies, Type II joint-health capsules, collagen-builder products and clinical-positioned beauty supplements. London and South East England will remain the leading premium demand clusters because of higher beauty retail intensity, aesthetic-clinic concentration, D2C brand activity and disposable-income-linked wellness adoption. The market will also face stricter scrutiny on claims. UK collagen brands must align product communication with food supplement rules, the UK Nutrition and Health Claims Register, FSA guidance, ASA advertising rulings and MHRA boundaries for medical claims. Brands that can support claims through compliant wording, ingredient traceability, heavy metal testing, allergen disclosure and clinical substantiation will hold stronger positions in pharmacy, premium beauty and practitioner channels.

Major Players

- Rousselot / Darling Ingredients

- GELITA UK

- PB Leiner / Tessenderlo Group

- Nitta Gelatin

- Weishardt Group

- Lapi Gelatine

- Gelnex / Darling Ingredients

- Revive Collagen

- Absolute Collagen

- Ingenious Beauty

- Hunter & Gather

- Dose & Co

- Ancient + Brave

- JSHealth Vitamins UK

- Holland & Barrett Own-Brand Collagen

Key Target Audience

- Collagen ingredient manufacturers

- Dietary supplement and nutraceutical brands

- Beauty and nutricosmetic brands

- Functional food and beverage manufacturers

- Pharmaceutical capsule and excipient manufacturers

- Health retail and pharmacy chains

- Investments and venture capitalist firms

- Government and regulatory bodies, Food Standards Agency, Medicines and Healthcare products Regulatory Agency, Advertising Standards Authority, Department for Environment, Food & Rural Affairs

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map of the UK collagen market, covering ingredient suppliers, importers, supplement brands, contract manufacturers, pharmacies, health retailers, e-commerce platforms, food manufacturers, cosmetic brands and regulators. The objective is to identify variables such as source, product type, form factor, application, grade, channel, claims compliance and ingredient origin.

Step 2: Market Analysis and Construction

In this phase, historical and current data is compiled across collagen revenue, gelatin demand, hydrolyzed peptide uptake, branded supplement sales, imported ingredient flows, pharmacy presence, marketplace SKUs and food-manufacturing applications. The analysis reviews how gelatin, bovine collagen, marine collagen and Type II collagen are used across food, pharma, beauty, sports nutrition and active-aging categories.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through computer-assisted interviews with collagen ingredient suppliers, supplement brands, contract manufacturers, retailers, nutrition formulators, beauty brands and pharmaceutical ingredient buyers. These consultations help test assumptions around gelatin dominance, marine collagen premiumization, bovine powder demand, D2C subscriptions, pharmacy listings and UK-compliant claim positioning.

Step 4: Research Synthesis and Final Output

The final phase synthesizes top-down macroeconomic and industry indicators with bottom-up SKU, channel and company-level checks. This approach validates the UK collagen market size, segmentation, competition, demand outlook, supply-chain constraints and regulatory risk profile, producing a structured market view for investors, manufacturers, retailers and consumer-health companies.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Top-Down Validation, Bottom-Up Validation, Import Review, SKU Benchmarking, Primary Interviews, Regulatory Screening, Competitive Mapping, Forecast Model, Limitations)

- Definition and Scope

- Market Genesis and Evolution

- Timeline of Major Players

- Business Cycle and Consumption Seasonality

- Growth Drivers (Beauty-from-Within Demand, Active Aging Population, Marine Collagen Premiumization, Functional Food Innovation, Pharmacy Retail Reach, D2C Subscription Growth, Sports Nutrition Adoption)

- Market Challenges (Health Claim Scrutiny, Imported Ingredient Dependency, Marine Allergen Disclosure, Taste and Odour Barriers, Private Label Price Pressure, Vegan Consumer Resistance)

- Market Opportunities (Premium Marine Collagen, Menopause Wellness, Sports Recovery, Collagen RTD Beverages, Clinical Joint Formulas, Pet Collagen, Medical-Grade Collagen, Vegan Collagen Builders)

- Market Trends (Liquid Sachets, Multi-Collagen Blends, Marine Premiumization, Collagen Stacking, Third-Party Testing, Clean Label, Plastic-Free Packaging, Influencer Education)

- SWOT Analysis

- Porter’s Five Forces

- PESTLE Analysis

- By Value (2020-2025)

- By Volume (2020-2025)

- By Average Selling Price (2020-2025)

- By Product Type (In Value %)

Gelatin

Hydrolyzed Collagen Peptides

Native Collagen

Undenatured Type II Collagen

Collagen Casings - By Application (In Value %)

Dietary Supplements

Beauty and Nutricosmetics

Food an Beverage

Pharmaceuticals

Biomedical Devices - By Distribution Channel (In Value %)

B2B Ingredient Supply

Contract Manufacturing and Private Label

Pharmacies and Drugstores

Health and Wellness Retail - By Region (In Value %)

London and South East

Midlands

North West

Yorkshire and Humber

- Market Share of Major Players on the Basis of Value and Volume

- Cross Comparison Parameters (Collagen Source Portfolio, Product Format Portfolio, Application Coverage, UK Regulatory and Claims Readiness, Retail and E-Commerce Reach, Certification and Traceability, Clinical Evidence Support, Subscription and D2C Capability)

- SWOT Analysis of Major Players

- Detailed Profiles of Major Companies

Rousselot / Darling Ingredients

GELITA UK

PB Leiner

Nitta Gelatin

Weishardt

Lapi Gelatine

Gelnex / Darling Ingredients

Revive Collagen

Absolute Collagen

Ingenious Beauty

Hunter & Gather

Dose & Co

Ancient + Brave

JSHealth Vitamins UK

Holland & Barrett Own-Brand Collagen

- Dietary Supplement Brand Demand

- Beauty and Nutricosmetic Brand Demand

- Food and Beverage Manufacturer Demand

- Pharmaceutical Manufacturer Demand

- By Value (2026-2035)

- By Volume (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now