Download PDF

Download PDFMarket Overview

The UK Dairy Free Ice Cream Market was valued at approximately USD ~ million in 2024, driven by the expansion of the plant-based food sector and increasing consumer demand for lactose-free frozen desserts. According to the UK Office for National Statistics, the UK population increased from 67.7 million to 68.3 million, while consumer expenditure on food and non-alcoholic beverages exceeded GBP 150 billion. The market is supported by rising vegan adoption, growing awareness of dairy intolerance, and expanding retail availability of plant-based products. Innovation in oat, coconut, almond, and pea-protein formulations has further accelerated category growth, while premiumization trends continue to drive consumer spending on dairy-free frozen desserts across supermarkets, convenience stores, and foodservice channels.

Market Segmentation

By Base Ingredient Type

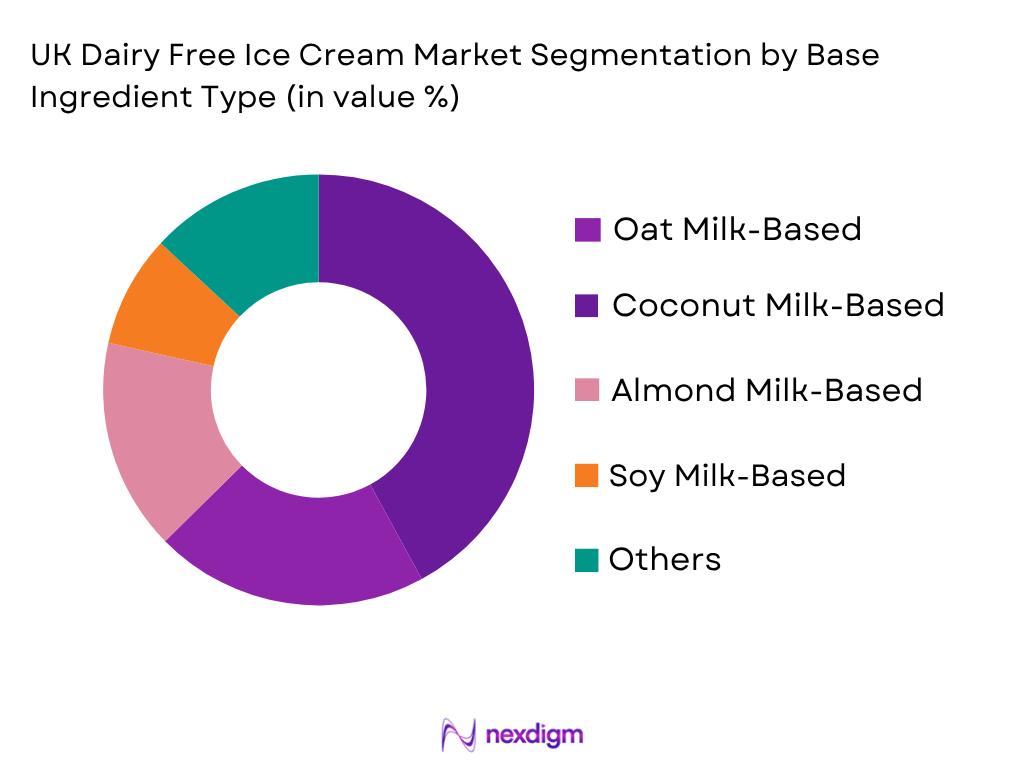

The UK Dairy Free Ice Cream Market is segmented into oat milk-based, coconut milk-based, almond milk-based, soy milk-based, cashew milk-based, pea protein-based, and mixed plant-based formulations. Oat milk-based ice cream currently dominates the market due to its strong alignment with UK consumer preferences for sustainable and locally relevant plant-based ingredients. Oat-based products are widely perceived as environmentally friendly and provide a creamy texture that closely resembles conventional dairy ice cream. Major brands including Oatly, Jude’s, and several supermarket private labels have expanded oat-based product portfolios, enhancing category visibility. Oat milk also offers a neutral flavor profile that supports a wide variety of premium and indulgent flavors. Furthermore, the UK’s well-established oat supply chain and growing consumer familiarity with oat-based beverages have translated into strong acceptance within frozen desserts. These factors collectively contribute to the segment’s leadership position across retail and foodservice channels.

By Distribution Channel

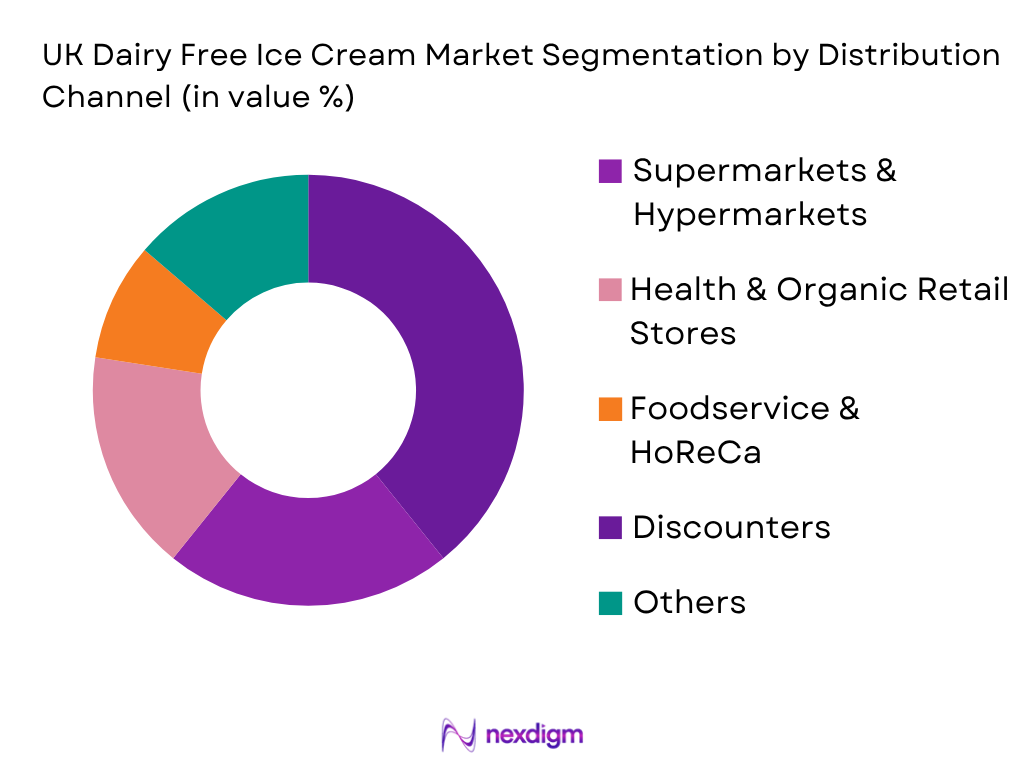

The UK Dairy Free Ice Cream Market is segmented into supermarkets & hypermarkets, convenience stores, health & organic retailers, discounters, online retail platforms, foodservice establishments, and dessert chains. Supermarkets and hypermarkets account for the largest share due to their extensive nationwide reach and ability to offer a broad portfolio of dairy-free frozen desserts. Leading retailers such as Tesco, Sainsbury’s, ASDA, Morrisons, Waitrose, and Marks & Spencer have significantly expanded plant-based frozen dessert offerings, including both branded and private-label products. Consumers prefer supermarkets because they provide product variety, competitive pricing, and convenient one-stop shopping experiences. Retailers have also introduced dedicated vegan and free-from sections, improving product visibility and encouraging trial purchases. Strong cold-chain infrastructure and extensive store networks ensure widespread availability across urban and suburban areas, reinforcing the dominance of supermarkets and hypermarkets within the UK dairy-free ice cream distribution landscape.

Competitive Landscape

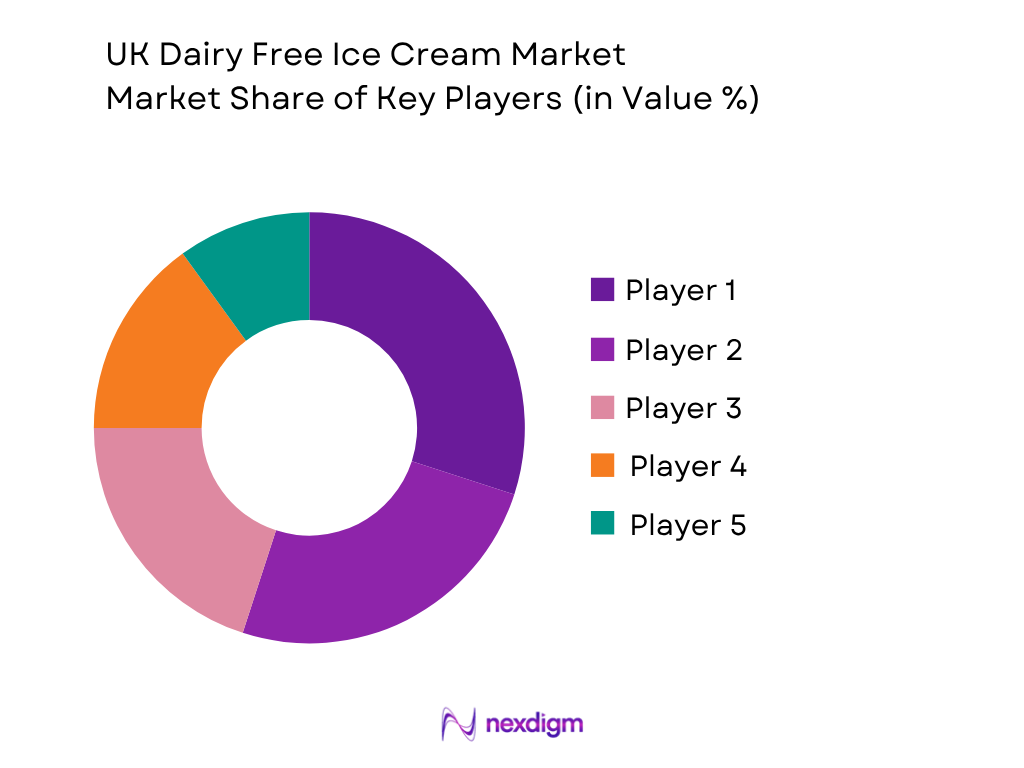

The UK Dairy Free Ice Cream Market is characterized by competition among specialist vegan brands, multinational food manufacturers, premium ice cream producers, and retailer-owned private labels. Market participants compete through product innovation, clean-label formulations, vegan certifications, premium flavor development, sustainability initiatives, and distribution expansion. The market remains moderately consolidated, with several established brands benefiting from strong consumer recognition and extensive retail partnerships.

| Company | Establishment Year | Headquarters | Plant-Based Base Portfolio | Dairy-Free SKU Count | Distribution Reach | Premium Product Portfolio | Vegan Certification | Packaging Sustainability |

| Oatly | 1994 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Jude’s | 2002 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Alpro | 1980 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Booja-Booja | 1999 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Ben & Jerry’s Non-Dairy | 1978 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

UK Dairy Free Ice Cream Market Analysis

Growth Drivers

Rising Plant-Based Food Consumption and Expanding Consumer Spending

The UK Dairy Free Ice Cream Market is strongly supported by the expansion of plant-based food consumption and robust consumer spending patterns. The United Kingdom recorded a nominal GDP of approximately USD 3.59 trillion in 2024, while GDP per capita exceeded USD 52,000, indicating substantial purchasing power for premium and specialty food products. Household final consumption expenditure remained above USD 2.2 trillion, reflecting continued spending on food and beverage categories. The UK population exceeded 68 million people, creating a significant consumer base for dairy-free frozen desserts. Additionally, the UK remains one of Europe’s largest plant-based food markets, with major retailers including Tesco, Sainsbury’s, ASDA, Waitrose, and Morrisons continuing to expand vegan and free-from product assortments. Dairy-free ice cream benefits directly from increasing consumer demand for lactose-free, vegan, and environmentally conscious food products. The availability of oat-based, almond-based, coconut-based, and pea protein-based formulations has improved product variety and accessibility. Strong retail penetration, increasing premium food purchases, and consumer willingness to explore plant-based alternatives continue to create favorable demand conditions for dairy-free frozen desserts across both retail and foodservice sectors.

Growing Health Awareness and Demand for Lactose-Free Alternatives

The UK Dairy Free Ice Cream Market is benefiting from increasing health awareness and growing demand for lactose-free dietary solutions. The United Kingdom maintains healthcare expenditures exceeding GBP 300 billion annually, reflecting heightened consumer focus on health and wellness. The country’s population exceeds 68 million people, while median disposable household income continues to support spending on premium nutrition-oriented food categories. Consumers are increasingly seeking products that align with digestive health goals, dietary preferences, and clean-label expectations. The broader free-from food category has experienced strong expansion as consumers actively seek alternatives to traditional dairy products. Furthermore, the UK labor market remains resilient with employment levels exceeding 33 million individuals, supporting discretionary spending on premium frozen desserts. Dairy-free ice cream manufacturers have responded by introducing products featuring reduced sugar content, plant-based proteins, organic ingredients, and natural flavor profiles. The increasing availability of vegan-certified and lactose-free products across supermarkets, convenience stores, and online retail channels continues to drive consumer adoption. As health-conscious purchasing behavior becomes more mainstream, dairy-free frozen desserts are increasingly viewed as an acceptable alternative to conventional dairy ice cream.

Market Challenges

Dependence on Imported Plant-Based Ingredients and Agricultural Volatility

The UK Dairy Free Ice Cream Market faces challenges associated with dependence on imported ingredients required for premium plant-based formulations. The United Kingdom imports substantial volumes of almonds, coconuts, cocoa, and specialty plant proteins used in dairy-free frozen dessert manufacturing. Total UK imports exceeded GBP 800 billion, highlighting the importance of international supply chains for food production. Since the UK climate is unsuitable for large-scale production of several tropical ingredients utilized in dairy-free ice cream formulations, manufacturers remain exposed to international agricultural volatility and supply disruptions. Furthermore, food manufacturers must manage ingredient consistency across oat, almond, coconut, and mixed plant-based formulations while maintaining desired texture and taste characteristics. The UK food manufacturing industry consists of more than 12,000 enterprises, increasing competition for specialized ingredients and processing capacity. Variations in global crop yields, transportation disruptions, and ingredient availability can influence production planning and inventory management. For dairy-free ice cream manufacturers seeking to maintain product quality and nationwide distribution, supply chain resilience and ingredient diversification remain critical operational priorities.

Intense Competition and Shelf-Space Constraints

The UK Dairy Free Ice Cream Market operates within a highly competitive premium frozen dessert environment characterized by strong retailer influence and growing private-label activity. The UK grocery market exceeds GBP 240 billion annually, creating intense competition among branded and retailer-owned products. Major retailers continue expanding private-label vegan and free-from product ranges, increasing competition for established dairy-free ice cream brands. The country maintains more than 10,000 supermarket outlets and grocery stores, where shelf space allocation is highly competitive and performance-driven. Dairy-free ice cream brands must compete not only with traditional dairy ice cream but also with frozen yogurt, gelato, low-calorie desserts, and alternative plant-based frozen products. Product differentiation requires continual investment in flavor innovation, packaging design, sustainability initiatives, and consumer marketing. In addition, consumers have access to an increasingly diverse range of frozen dessert options, making brand loyalty more difficult to maintain. Manufacturers must continuously innovate while balancing product quality, ingredient sourcing, and distribution expansion to remain competitive within the rapidly evolving UK frozen dessert landscape.

Market Opportunities

Expansion of Functional and Premium Dairy-Free Product Innovation

The UK Dairy Free Ice Cream Market has significant opportunities linked to the growth of functional nutrition and premium food consumption. Food and non-alcoholic beverage expenditure in the United Kingdom exceeds GBP 150 billion annually, while household spending on health-oriented products continues to increase. Consumers are increasingly seeking products that combine indulgence with nutritional benefits, creating opportunities for dairy-free ice cream manufacturers to introduce protein-enriched, fiber-fortified, reduced-sugar, and probiotic-enhanced formulations. The UK’s advanced food innovation ecosystem and strong retail infrastructure support rapid product commercialization and consumer testing. Oat-based ingredients, pea proteins, and plant-derived functional additives are increasingly available through established food manufacturing supply chains. Premiumization trends also support the development of gourmet flavors, artisanal production techniques, and clean-label ingredient profiles. Manufacturers that successfully position dairy-free ice cream as both a premium indulgence and a wellness-oriented product can capitalize on evolving consumer preferences. The growing intersection between health, sustainability, and indulgence creates favorable conditions for product diversification and category expansion.

Growth of E-Commerce and Retailer-Led Plant-Based Expansion

The continued expansion of digital commerce and retailer-led plant-based product strategies presents a substantial opportunity for the UK Dairy Free Ice Cream Market. UK e-commerce sales exceed GBP 120 billion annually, while online grocery shopping remains one of the most developed channels in Europe. Internet usage exceeds 67 million individuals, providing extensive access to digital food purchasing platforms. Major grocery retailers continue investing in vegan and free-from product categories, increasing visibility and accessibility for dairy-free frozen desserts. Retailers including Tesco, Sainsbury’s, ASDA, Morrisons, Waitrose, Aldi, and Lidl have expanded plant-based private-label and branded product offerings. The UK also benefits from advanced cold-chain logistics and nationwide grocery delivery networks that facilitate frozen product distribution. Direct-to-consumer sales channels, quick-commerce services, and subscription-based food platforms are creating additional pathways for market penetration. As retailers continue prioritizing plant-based product development and consumers increasingly adopt online food purchasing habits, dairy-free ice cream manufacturers are positioned to benefit from enhanced product reach, stronger brand exposure, and broader consumer accessibility.

Future Outlook

The UK Dairy Free Ice Cream Market is expected to witness strong growth during the forecast period due to increasing consumer adoption of plant-based diets, expanding lactose-free product demand, and rising sustainability awareness. Manufacturers are expected to continue investing in innovative formulations, functional ingredients, and premium flavor profiles to attract a broader consumer base. Retailers are likely to increase shelf space dedicated to vegan and free-from products, while foodservice operators expand dairy-free menu offerings. Continued innovation in oat-based products, sustainable packaging, and reduced-sugar formulations is anticipated to support market expansion.

Major Players

- Oatly

- Jude’s

- Ben & Jerry’s Non-Dairy

- Magnum Vegan

- Swedish Glace

- Alpro

- Booja-Booja

- Coconut Collaborative

- Halo Top Dairy Free

- Häagen-Dazs Non-Dairy

- Wicked Kitchen

- Northern Bloc

- Over The Moo

- Tesco Plant Chef

- ASDA OMV!

Key Target Audience

- Dairy-Free Ice Cream Manufacturers

- Plant-Based Food & Beverage Companies

- Frozen Dessert Manufacturers

- Supermarket and Hypermarket Chains

- Foodservice and HoReCa Operators

- Alternative Protein and Plant-Based Ingredient Suppliers

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies (Food Standards Agency (FSA), Department for Environment Food & Rural Affairs (DEFRA), Competition and Markets Authority (CMA))

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing a comprehensive ecosystem map covering manufacturers, ingredient suppliers, distributors, retailers, foodservice operators, and consumers participating in the UK Dairy Free Ice Cream Market. Extensive desk research is conducted through government publications, trade associations, company reports, retail databases, and proprietary industry sources. The primary objective is to identify critical variables affecting demand, supply, pricing, innovation, and consumer purchasing behavior.

Step 2: Market Analysis and Construction

Historical industry data is compiled and analyzed to evaluate consumption trends, retail penetration, product availability, and revenue generation. Demand-side assessments are combined with supply-side evaluations to estimate market size and segment shares. Additional analysis is conducted across distribution channels, product formats, ingredient categories, and regional consumption patterns to establish a comprehensive market framework.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through structured consultations with manufacturers, distributors, retailers, foodservice operators, and plant-based ingredient suppliers. These discussions provide operational insights regarding production capabilities, product innovation trends, pricing strategies, distribution dynamics, and evolving consumer preferences. Expert feedback is incorporated to refine assumptions and strengthen analytical accuracy.

Step 4: Research Synthesis and Final Output

The final phase integrates findings from both primary and secondary research into a validated market assessment. Bottom-up and top-down methodologies are reconciled through data triangulation to ensure consistency and reliability. The resulting output includes market sizing, segmentation analysis, competitive benchmarking, future forecasts, and strategic recommendations for stakeholders operating within the UK Dairy Free Ice Cream Market.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Retail Audit Analysis, Consumer Purchase Tracking, Primary Industry Interviews, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Dairy-Free Frozen Dessert Industry Ecosystem

- Industry Value Chain Analysis

- Growth Drivers (Increasing Vegan Population, Rising Lactose Intolerance Awareness, Expansion of Plant-Based Food Consumption, Premium Frozen Dessert Demand, Growth of Modern Grocery Retail, Health & Wellness Expenditure)

- Market Challenges (Premium Product Pricing, Volatility in Plant-Based Ingredient Supply, Taste and Texture Replication Challenges, Shelf Space Competition, Frozen Logistics Constraints, Regulatory Compliance Requirements)

- Market Opportunities (Functional Dairy-Free Ice Cream Development, High-Protein Plant-Based Formulations, Private Label Expansion, Foodservice Penetration, Sustainable Packaging Innovation, E-Commerce Channel Growth)

- Market Trends (Oat-Based Product Innovation, Clean Label Formulations, Low-Sugar Frozen Desserts, Premium Indulgent Flavors, Sustainable Packaging Adoption, Protein-Enriched Dairy-Free Products, Hybrid Plant-Based Ingredients)

- Government Regulations (Food Standards Agency Labeling Requirements, UK Allergen Regulations, HFSS Compliance Framework, Organic Certification Standards, Packaging Waste Regulations, Sustainability Reporting Requirements)

- Raw Material Analysis (Oat Ingredient Availability, Almond Ingredient Procurement, Coconut Supply Dynamics, Pea Protein Adoption, Cocoa Utilization Trends, Natural Sweetener Usage)

- Consumer Preference Mapping (Taste Expectations, Texture Acceptance, Ingredient Transparency, Sustainability Considerations, Nutritional Preferences)

- Supply-Demand Gap Assessment

- SWOT Analysis

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Stakeholder Ecosystem

- Competition Ecosystem

- By Market Value (2020-2025)

- By Volume Consumption (2020-2025)

- By Average Selling Price (2020-2025)

- By Base Ingredient Type (In Value %)

Oat Milk-Based Ice Cream

Coconut Milk-Based Ice Cream

Almond Milk-Based Ice Cream

Soy Milk-Based Ice Cream

Cashew Milk-Based Ice Cream

Pea Protein-Based Ice Cream

Mixed Plant-Based Formulations

Other Alternative Bases - By Flavor Type (In Value %)

Chocolate

Vanilla

Salted Caramel

Cookies and Cream

Fruit-Based Flavors

Coffee and Mocha Flavors

Premium Gourmet Flavors

Seasonal and Limited-Edition Flavors - By Distribution Channel (In Value %)

Supermarkets and Hypermarkets

Convenience Stores

Health & Organic Retail Stores

Discounters

Online Retail and Direct-to-Consumer

Foodservice and HoReCa

Ice Cream Parlors and Dessert Chains - By Region (In Value %)

England

Scotland

Wales

Northern Ireland

Greater London - By Packaging Type (In Value %)

Paperboard Tubs

Plastic Tubs

Multipack Formats

Stick and Bar Packaging

Single-Serve Cups

Recyclable and Sustainable Packaging

- Market Share of Major Players (By Value, Volume, Product Format, Distribution Channel, Plant-Based Base Type)

- Market Concentration Analysis (Top Brand Contribution, Private Label Penetration, Premium Brand Presence, Regional Brand Strength)

- Cross Comparison Parameters (Plant-Based Base Portfolio, Dairy-Free SKU Count, Distribution Reach Across UK Retailers, Vegan Certification Portfolio, Production Capacity, Premium Product Penetration, Innovation & New Product Launch Frequency, Sustainable Packaging Adoption)

- SWOT Analysis of Major Players

- Pricing Analysis by SKU, Pack Size and Product Category

- Detailed Profiles of Major Companies

Oatly

Jude’s

Ben & Jerry’s Non-Dairy

Magnum Vegan

Swedish Glace

Alpro

Booja-Booja

Coconut Collaborative

Halo Top Dairy Free

Häagen-Dazs Non-Dairy

Wicked Kitchen

Northern Bloc

Over The Moo

Tesco Plant Chef

ASDA OMV!

- Consumption Behavior Assessment (Purchase Frequency, Consumption Occasions, Household Penetration, Repeat Purchase Rate, Seasonal Consumption Patterns)

- Demographic Consumption Trends (Age Group, Income Segment, Household Composition, Urban-Rural Split, Lifestyle Preferences)

- Purchasing Power Analysis (Disposable Income, Premium Product Affordability, Food & Beverage Spending, Frozen Dessert Expenditure)

- Premium vs Mass Market Demand Analysis (Willingness to Pay, Premium Brand Adoption, Value Perception, Trading-Up Behavior)

- Brand Loyalty Assessment (Repeat Purchase Behaviour, Brand Switching Trends, Retention Drivers, Trial Conversion Rates)

- By Market Value (2026-2035)

- By Volume Consumption (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now