Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UK defense market, based on a recent historical assessment, is valued at approximately USD ~ billion, driven primarily by continued government investment in military modernization and the increasing need for advanced technology solutions. The market benefits from sustained defense spending to enhance cybersecurity, intelligence systems, and defense platforms, ensuring the UK’s military readiness amidst growing global tensions. The demand for technologically advanced defense solutions, including AI and autonomous systems, is contributing significantly to market growth.

In the UK, key cities like London, Bristol, and Manchester are leading the market, fueled by their robust industrial infrastructure and proximity to major defense contractors and government defense agencies. The strength of these cities lies in their ability to integrate cutting-edge technologies with traditional defense platforms, supported by strong defense policy frameworks and strategic initiatives. These regions serve as hubs for military innovation, benefitting from high levels of R&D investment and being home to significant aerospace and defense industry players.

Market Segmentation

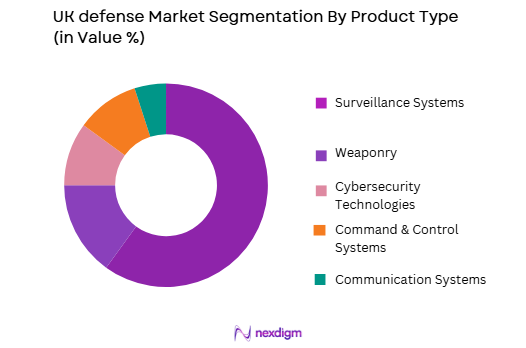

By Product Type

The UK defense market is segmented by product type into surveillance systems, weaponry, cybersecurity technologies, command & control systems, and communication systems. Recently, cybersecurity technologies have a dominant market share due to increasing global cyber threats and the need for enhanced defense against cyberattacks on critical infrastructure. This sub-segment has seen rapid adoption, driven by the need for secure communication and data protection in defense operations, fueling its expansion across government and military sectors. The government’s increasing focus on countering cyber threats and technological advancements has bolstered the demand for these systems.

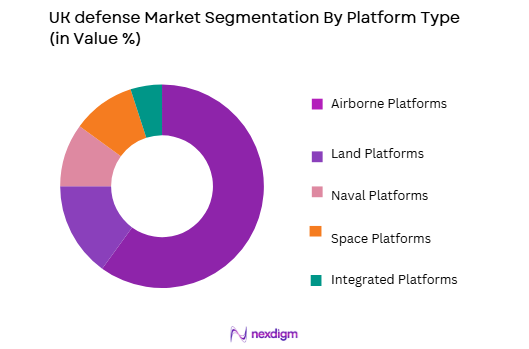

By Platform Type

The UK defense market is segmented by platform type into airborne platforms, land platforms, naval platforms, space platforms, and integrated platforms. Among these, airborne platforms have captured the largest market share, driven by the increasing demand for advanced unmanned aerial vehicles (UAVs) and fighter jets. The use of drones for reconnaissance, surveillance, and combat operations has significantly expanded, making airborne platforms a key area of focus for both government and defense contractors. Technological advancements in stealth technology, AI integration, and improved combat capabilities have contributed to the growth of this sub-segment.

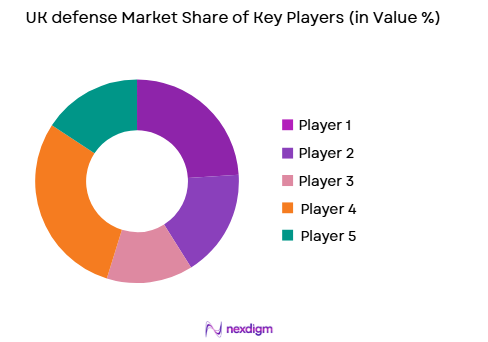

Competitive Landscape

The UK defense market is characterized by strong competition among established defense contractors, with ongoing consolidation trends, where leading players continuously enhance their technological capabilities and market share. The influence of major players, particularly those involved in manufacturing and technology integration, is significant, with large corporations often partnering with governments and other industries to secure long-term contracts. The market’s competitive dynamics are also shaped by technological innovation and strategic partnerships that focus on high-end defense technologies such as AI, robotics, and autonomous systems.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | One Additional Market-Specific Parameter |

| BAE Systems | 1999 | London, UK | ~ | ~ | ~ | ~ | ~ |

| Thales Group | 2000 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1912 | Bethesda, USA | ~ | ~ | ~ | ~ | ~ |

| Leonardo | 1948 | Rome, Italy | ~ | ~ | ~ | ~ | ~ |

| Northrop Grumman | 1939 | Falls Church, USA | ~ | ~ | ~ | ~ | ~ |

UK defense Market Analysis

Growth Drivers

Increased Government Investment in National Security

The growing global security threats, including cyber threats and geopolitical instability, have led to a marked increase in government defense spending. This surge in defense budgets, especially in the UK’s context, reflects the prioritization of national security over the next few years. Increased funding has supported the expansion of cutting-edge defense technologies such as autonomous systems, artificial intelligence, and cybersecurity systems, ensuring military readiness. As part of the defense strategy, the UK government has committed to investing in upgrading legacy systems and incorporating advanced technologies to counter emerging threats. The expansion of cyber defense capabilities in particular is a crucial part of this initiative, helping safeguard critical infrastructure and military assets. Investment in defense R&D has grown exponentially, with an emphasis on future-proofing military capabilities in the face of new technological challenges. This has created a robust foundation for the market, further accelerating the development of next-generation defense solutions. The defense sector remains one of the key pillars of government spending, making it a significant driver for growth.

Technological Advancements in AI and Cybersecurity

The integration of artificial intelligence and advanced cybersecurity technologies is fueling market expansion. AI-driven defense systems, including surveillance and reconnaissance platforms, are becoming central to military strategies, allowing for more efficient data analysis and decision-making. Moreover, the application of AI in weaponry and autonomous systems is transforming the defense landscape, improving both defense and attack capabilities. Alongside AI, the rising sophistication of cybersecurity systems is crucial for securing defense networks and critical national infrastructure. As global cyber threats grow more complex, the demand for state-of-the-art defense mechanisms, including AI and machine learning technologies, is expected to grow significantly. With governments seeking to protect sensitive information and military operations from cyberattacks, investments in cybersecurity have surged, propelling the market forward. This intersection of AI and cybersecurity has not only become a major growth driver for the defense industry but also a key differentiator for companies operating in this sector.

Market Challenges

High Capital Expenditure in Defense Projects

A significant challenge in the UK defense market is the high cost associated with the development and deployment of advanced defense systems. The capital-intensive nature of defense projects, which require substantial investments in infrastructure, technology, and labor, limits the ability of smaller companies to compete and increases the financial burden on governments. The large defense contractors, while benefiting from government contracts, often face difficulties in maintaining competitive pricing without affecting profitability. Additionally, the long development timelines and high maintenance costs associated with defense platforms, such as aircraft and naval vessels, contribute to the overall expenses. These high costs often result in delays or reduced scope in defense procurement programs, making it difficult for governments to meet military readiness requirements on time. As defense budgets fluctuate, the cost-effectiveness of procurement becomes a critical factor in determining future market strategies.

Cybersecurity Threats and Vulnerabilities

As defense systems become more interconnected and reliant on digital technologies, they face increased exposure to cyberattacks and security vulnerabilities. Cyber threats are evolving at a rapid pace, with attackers continuously developing new methods to breach military networks and data systems. The increasing sophistication of cyber warfare poses a significant challenge to both defense contractors and government agencies, as the costs of cyber defense systems escalate. Moreover, as the military industry adopts more automated systems, the risk of cyber vulnerabilities grows, with the potential for compromising national security. Ensuring the cybersecurity of sensitive military data and operations requires constant innovation, adding an additional layer of complexity to defense system development. This evolving threat landscape requires significant investment in research and technology to safeguard against breaches, which represents both a challenge and a critical area for future market development.

Opportunities

Expansion in Artificial Intelligence-Driven Defense Solutions

The UK defense market is witnessing a significant opportunity for growth in artificial intelligence (AI)-driven defense solutions. AI technologies are being increasingly integrated into defense systems for applications such as predictive maintenance, autonomous vehicles, and advanced data analytics. This presents an opportunity for companies to develop innovative AI-based platforms that can enhance military efficiency and precision. As AI technology continues to evolve, its applications in surveillance, reconnaissance, and strategic planning are expected to expand. The military’s increasing reliance on AI for decision-making processes, particularly in real-time battlefield scenarios, offers substantial growth prospects. Moreover, AI can play a vital role in cyber defense, making it a critical tool for addressing emerging security challenges. The UK government’s commitment to adopting AI technologies in defense further bolsters this opportunity, ensuring a continued push toward next-generation defense systems.

Partnerships with Private Tech Firms for Enhanced Cybersecurity

As cybersecurity becomes an increasingly pressing concern for national security, defense contractors have an opportunity to collaborate with private technology firms specializing in cybersecurity solutions. By leveraging the expertise of private-sector cybersecurity firms, defense companies can enhance their systems’ capabilities and safeguard against new types of cyberattacks. These partnerships offer a strategic avenue for innovation, allowing the integration of cutting-edge cybersecurity technologies with existing defense platforms. The growing recognition of cybersecurity’s importance in defense operations presents an opportunity for both public and private sectors to work together in addressing this global threat. The UK defense sector’s openness to external collaborations also enables greater flexibility in adopting advanced cybersecurity solutions, ensuring that the military remains protected against emerging cyber threats.

Future Outlook

The UK defense market is expected to witness continued growth over the next five years, with advancements in AI, autonomous systems, and cybersecurity driving the demand for next-generation defense technologies. Technological developments are expected to focus on increasing operational efficiency, enhancing security, and ensuring the military’s readiness in an increasingly digital and interconnected world. Regulatory support, particularly from government defense initiatives, will remain a key factor in sustaining growth. Demand-side factors, including heightened national security concerns and military modernization programs, will also influence the market, fostering innovation and expanding the scope of defense solutions.

Major Players

- BAE Systems

- Lockheed Martin

- Thales Group

- Leonardo

- Northrop Grumman

- Raytheon Technologies

- L3 Technologies

- Boeing

- General Dynamics

- Rheinmetall AG

- Saab Group

- Elbit Systems

- Harris Corporation

- Hewlett Packard Enterprise

- Leonardo DRS

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Defense contractors

- Military procurement agencies

- Aerospace and defense R&D departments

- Commercial tech firms entering the defense sector

- Private sector technology firms

- Security and intelligence agencies

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying the core market drivers, challenges, and opportunities that influence the UK defense market.

Step 2: Market Analysis and Construction

We construct the market model by analyzing historical trends, current data, and future projections to create a comprehensive view of the market’s size and structure.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through consultations with industry experts, including defense contractors, government officials, and technology specialists.

Step 4: Research Synthesis and Final Output

The collected data is synthesized into actionable insights and presented as a final report, ensuring the inclusion of all relevant market dynamics and trends.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased Government Investment in National Security

Technological Advancements in AI and Cybersecurity

Rising Geopolitical Tensions - Market Challenges

High Capital Expenditure in Defense Projects

Cybersecurity Threats and Vulnerabilities

Technological Integration and Interoperability Issues - Market Opportunities

Expansion in Artificial Intelligence-Driven Defense Solutions

Partnerships with Private Tech Firms for Enhanced Cybersecurity

Emerging Demand for Autonomous Systems and Robotics - Trends

Increase in Use of Autonomous and Unmanned Systems

Integration of AI and Machine Learning in Battlefield Operations

Surge in Cybersecurity Investments for Defense Systems - Government regulations

Data Protection and Privacy Regulations

Export Control and Compliance Policies

Government Funding and Grants for Defense Technologies - SWOT analysis

- Porters Five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Command & Control Systems

Cybersecurity Systems

Surveillance & Reconnaissance Systems

Weapon Systems

Communication Systems - By Platform Type (In Value%)

Airborne Platforms

Land Platforms

Naval Platforms

Space Platforms

Integrated Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Modular Solutions

Hybrid Solutions

Integrated Solutions - By End User Segment (In Value%)

Military Forces

Defense Contractors

Government Agencies

Security Services

Private Sector / Technology Firms - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technology Integration, Maintenance & Support Services, Delivery Time, Cost Efficiency, Regulatory Compliance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

BAE Systems

Lockheed Martin

Thales Group

BAE Systems

General Dynamics

Northrop Grumman

Raytheon Technologies

L3 Technologies

Leonardo

Harris Corporation

Saab Group

Rheinmetall AG

Elbit Systems

Hewlett Packard Enterprise

Boeing

- Military Forces’ Increasing Demand for Digital Systems

- Government Agencies’ Role in Regulating and Procuring Defense Systems

- Defense Contractors’ Shift Towards Innovation and Integration

- Private Sector’s Growing Interest in Cybersecurity Solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now