Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UK digital health market, valued at approximately USD ~ billion, is primarily driven by advancements in telemedicine, wearable health devices, and health information technologies. Rising demand for efficient healthcare solutions, especially in remote patient monitoring and data management systems, has led to significant investments in this sector. The increasing adoption of AI and machine learning technologies to enhance diagnostic accuracy and treatment efficiency is also fueling the market’s growth. These technologies are contributing to a paradigm shift in healthcare delivery, with enhanced accessibility and improved patient outcomes.

The market is dominated by key urban hubs, particularly London, Manchester, and Birmingham, due to their robust healthcare infrastructure and a concentration of tech companies driving digital health innovations. London, in particular, leads as a global healthcare innovation hub, with strong government backing for digital health initiatives. These cities benefit from a combination of technological expertise, government regulations that support digital health adoption, and an established healthcare ecosystem. This strategic combination makes the UK a leader in the European digital health landscape.

Market Segmentation

By Product Type

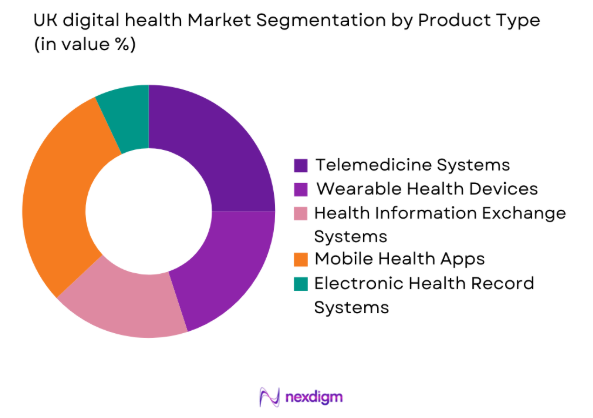

The UK digital health market is segmented by product type into telemedicine systems, wearable health devices, health information exchange systems, mobile health apps, and electronic health record systems. Recently, mobile health apps have dominated the market due to increasing consumer preference for self-monitoring and managing health remotely. The widespread use of smartphones and the rise of chronic diseases, coupled with a demand for more personalized healthcare solutions, have made mobile health apps the go-to choice for both healthcare providers and patients. These solutions are accessible, cost-effective, and align with the growing trend of consumer-driven healthcare.

By Platform Type

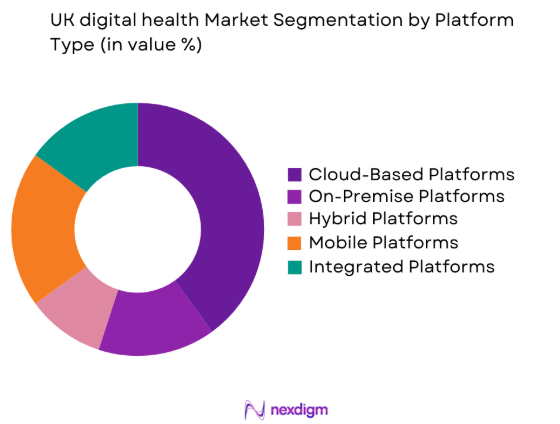

The UK digital health market is segmented by platform type into cloud-based platforms, on-premise platforms, hybrid platforms, mobile platforms, and integrated platforms. Recently, cloud-based platforms have seen a surge in popularity due to their flexibility, scalability, and cost-effectiveness. Healthcare providers prefer cloud-based solutions for their ability to integrate with multiple devices and databases, providing seamless patient data management and accessibility. These platforms also support collaboration across multiple healthcare institutions, further driving their dominance in the market.

Competitive Landscape

The competitive landscape of the UK digital health market is highly dynamic, with major players focusing on technological innovation, partnerships, and acquisitions. Consolidation is a key trend as smaller startups merge with larger healthcare IT firms to expand their market reach and enhance their product offerings. Leading companies are leveraging AI, machine learning, and cloud computing to improve healthcare services and reduce costs. These innovations are enabling healthcare providers to deliver high-quality care while managing patient data more effectively.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| Cerner Corporation | 1979 | North Kansas City | ~ | ~ | ~ | ~ | ~ |

| Allscripts Healthcare | 1986 | Chicago, USA | ~ | ~ | ~ | ~ | ~ |

| Medtronic | 1949 | Dublin, Ireland | ~ | ~ | ~ | ~ | ~ |

| Philips Healthcare | 1891 | Amsterdam, NL | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | Erlangen, Germany | ~ | ~ | ~ | ~ | ~ |

UK digital health Market Analysis

Growth Drivers

Increased Adoption of Telemedicine

The increasing demand for telemedicine solutions is a major factor driving market growth. Telemedicine allows patients to access healthcare remotely, reducing the need for in-person visits and improving healthcare accessibility, especially in underserved areas. The pandemic accelerated the adoption of telehealth solutions, as both patients and healthcare providers recognized their value. Telemedicine also offers cost-effective care, benefiting both providers and patients by reducing operational costs and travel expenses. Additionally, telemedicine helps ease the burden on physical healthcare infrastructure, ensuring that resources are better allocated. As a result, telemedicine is becoming a crucial component of the future healthcare system, providing convenient, affordable, and efficient care options for a wide range of patients.

Technological Advancements in AI and IoT

The integration of AI and IoT into healthcare systems is a key growth driver in the digital health market. AI is being leveraged for diagnostics, decision support, and creating personalized treatment plans, enhancing the accuracy of healthcare delivery. IoT devices, like wearable health monitors, enable continuous tracking of vital signs, providing real-time data to healthcare providers. These technologies improve care quality, enhance operational efficiency, and help lower healthcare costs by enabling early disease detection. As these technologies evolve, their increasing adoption is expected to further drive market growth. The demand for AI and IoT in healthcare will continue to expand, supporting more efficient, data-driven care solutions and transforming how healthcare is delivered.

Market Challenges

Data Privacy and Security Concerns

A major challenge in the UK digital health market is the growing concern over data privacy and security. Digital health solutions depend on the collection and storage of sensitive patient data, making data security a top priority. Cybersecurity threats pose significant risks to both patient privacy and trust in digital health platforms. Furthermore, compliance with regulations like GDPR adds complexity to managing healthcare data and ensures stringent privacy protections. These challenges require continuous investment in advanced security measures, robust infrastructure, and regular system updates to safeguard sensitive information. As the digital health sector evolves, maintaining secure data management and addressing privacy concerns will be critical for maintaining user confidence and regulatory compliance.

Regulatory and Compliance Barriers

Digital health technologies face strict regulations that can create barriers for new market entrants. In the UK, healthcare providers must adhere to regulatory frameworks such as the UK Medicines and Healthcare products Regulatory Agency (MHRA) and the National Institute for Health and Care Excellence (NICE). These regulations ensure that digital health solutions are safe and effective, but they can also hinder innovation and slow down time-to-market. Additionally, uncertainty surrounding reimbursement policies for digital health solutions complicates market expansion, as healthcare providers and companies must navigate complex approval processes for funding and support. The combination of stringent regulations and reimbursement challenges creates hurdles for companies looking to develop and introduce new digital health technologies to the market.

Opportunities

Emerging Demand for Personalized Healthcare

The growing demand for personalized healthcare solutions presents a significant opportunity in the digital health market. Advances in wearable devices, genetic testing, and AI-driven diagnostics are driving the shift toward individualized care, enabling tailored treatment plans for patients. This trend allows healthcare providers to address specific patient needs, improving outcomes and efficiency. Personalized healthcare is not only enhancing the patient experience but also streamlining healthcare delivery by reducing unnecessary treatments and hospital visits. As patients increasingly seek solutions that cater to their unique health profiles, digital health companies have an opportunity to innovate and capture a larger market share by developing advanced, customized healthcare technologies that improve both quality and accessibility.

Expansion of Digital Health in Rural and Underserved Areas

A significant opportunity exists in expanding digital health services to rural and underserved areas. These regions face challenges like long travel distances, limited access to specialists, and inadequate healthcare infrastructure. Digital health solutions, particularly telemedicine, can overcome these barriers by offering remote access to healthcare professionals, thus enhancing service availability. The UK government actively supports digital health initiatives, which further boosts the potential for growth in these areas. With continued technological advancements, such as improved internet connectivity and telehealth platforms, digital health companies can expand their reach and provide essential healthcare services to underserved populations, improving overall health outcomes while addressing geographic healthcare disparities.

Future Outlook

The UK digital health market is expected to experience steady growth over the next five years, driven by increasing adoption of telemedicine, advancements in AI, and expanding government support for digital health initiatives. As technologies continue to evolve and regulatory frameworks adapt to new healthcare innovations, the digital health market is poised for transformation. The integration of more advanced technologies, along with growing demand from patients and healthcare providers, will likely shape the future landscape of the market, creating significant opportunities for innovation and investment.

Major Players

- Cerner Corporation

- Allscripts Healthcare Solutions

- Medtronic

- Philips Healthcare

- Siemens Healthineers

- GE Healthcare

- IBM Watson Health

- HealthTap

- Doc.ai

- Teladoc Health

- Babylon Health

- Omada Health

- Zebra Medical Vision

- iHealthLabs

- 23andMe

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers and hospitals

- Health insurance providers

- Pharmaceutical companies

- Technology and IT firms in healthcare

- Medical device manufacturers

- Telemedicine service providers

Research Methodology

Step 1: Identification of Key Variables

Identifying the critical variables that influence the digital health market, including technological advancements, regulatory environment, and patient demand.

Step 2: Market Analysis and Construction

Conducting a comprehensive analysis of market trends, key drivers, and challenges, constructing the market structure based on reliable data sources.

Step 3: Hypothesis Validation and Expert Consultation

Validating market hypotheses through consultation with industry experts, stakeholders, and relevant market participants.

Step 4: Research Synthesis and Final Output

Synthesizing collected data and research findings to create the final market report, ensuring all insights are accurate and comprehensive.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing Demand for Telemedicine Solutions

Technological Advancements in Mobile Health

Rising Healthcare Costs and Demand for Efficiency - Market Challenges

Data Privacy Concerns

Technological Integration Barriers

Regulatory and Compliance Issues - Market Opportunities

Emerging Trends in AI and Machine Learning

Expansion of Healthcare Digitalization in Rural Areas

Government Initiatives for Healthcare Modernization - Trends

Growth of Remote Patient Monitoring

Expansion of Digital Health in Preventive Care

Integration of IoT in Healthcare Solutions - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Telemedicine Systems

Wearable Health Devices

Health Information Exchange Systems

Mobile Health Apps

Electronic Health Record Systems - By Platform Type (In Value%)

Cloud-Based Platforms

On-Premise Platforms

Hybrid Platforms

Mobile Platforms

Integrated Platforms - By Fitment Type (In Value%)

On-Premise Solutions

Cloud-Based Solutions

Hybrid Solutions

Modular Solutions

Integrated Solutions - By End User Segment (In Value%)

Healthcare Providers

Patients

Pharmaceutical Companies

Government and Regulatory Bodies

Insurance Providers - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Platforms

Third-Party Distributors

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Market Growth Rate, Adoption Barriers, Technological Advancements, Regulatory Compliance, Investment Trends)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Cerner Corporation

Allscripts Healthcare Solutions

Medtronic

Philips Healthcare

Siemens Healthineers

GE Healthcare

IBM Watson Health

Samsung Electronics

HealthTap

Doc.ai

Teladoc Health

Babylon Health

Omada Health

Zebra Medical Vision

iHealth Labs

- Healthcare Providers’ Increasing Adoption of Digital Tools

- Patients’ Growing Preference for Digital Health Solutions

- Regulatory Bodies’ Role in Shaping Digital Health Adoption

- Insurance Providers’ Integration of Digital Health Solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now