Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UK Duty Free and Travel Retail market is valued at USD ~ billion in 2024, based on revenue generated from duty free and travel‑exclusive retail sales across airports, airlines, ferries, and other travel channels. This valuation reflects recovery in international and domestic travel volumes, increased passenger spend on luxury goods like perfume, cosmetics and premium spirits, and enhanced retail offerings at major UK travel hubs.

London, Manchester, and other major airport cities dominate the UK duty free and travel retail market due to their extensive international connectivity, high passenger footfall, and established retail infrastructure. Airports such as London Heathrow and Gatwick serve as global transit points with large volumes of premium and long‑haul travelers, driving high sales of luxury and exclusive travel retail products. Regional airports also contribute through concentrated retail space enhancements targeted at inbound and outbound tourism.

Market Segmentation

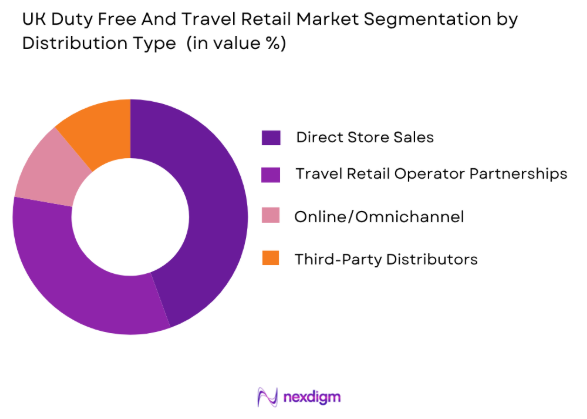

By Distribution Type

The UK Duty Free and Travel Retail market is segmented by distribution channel into Airports, Airlines, Ferries, and Others. Airports dominate this segmentation due to their high passenger throughput, longer dwell times, and broader retail footprint that supports extensive product assortments and brand activations. Major UK airports, especially Heathrow, provide large duty free spaces that house luxury perfume, cosmetics, wine and spirits, and fashion categories, capturing high per‑passenger spend. Airlines and ferry channels contribute to niche segments such as onboard retail and destination‑specific products but remain smaller in share due to limited shelf space and shorter engagement time with travelers.Airports lead because they attract both outbound and transit travelers with high disposable income,cdriving impulse and planned purchases. Retailers optimize airport layouts with premium brand visibility and exclusive product launches that appeal to global traveler preferences. Airlines provide supplementary retail exposure, often focused on convenience items and selected product lines. Ferries and other channels capture local and regional travel retail demand but with narrower assortments and lower average transaction values.

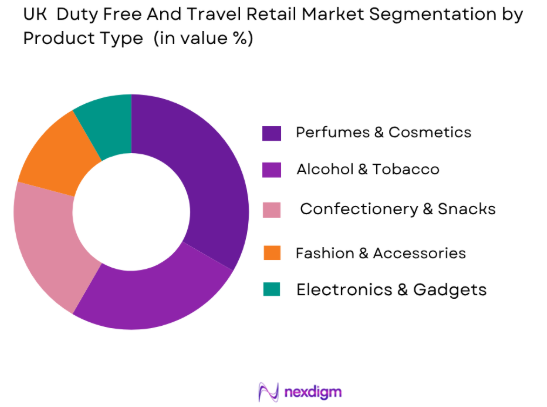

By Product Type

The market is also segmented by product type into Perfume & Cosmetics, Wine & Spirits, Fashion & Accessories, Tobacco Products, Electronics & Gifts, and Food & Confectionery. Perfume & cosmetics hold the largest share due to strong global brand demand and high price points that attract international travelers seeking duty‑free exclusives. Premium fragrances, skincare sets, and limited‑edition beauty collections often serve as key motivators for travel purchases, benefiting from differentiated offerings compared to domestic retail. Wine & spirits follow as a high‑value category leveraged through curated collections and UK‑exclusive launches. Perfumes and cosmetics dominate because travelers frequently purchase luxury beauty products as gifts or personal indulgences, and these items benefit from duty exemptions and airport exclusivity. Wine & spirits attract premium spend through curated regional offerings and travel‑only editions, while fashion and accessories offer curated selections that align with traveler profiles of high‑income destinations.

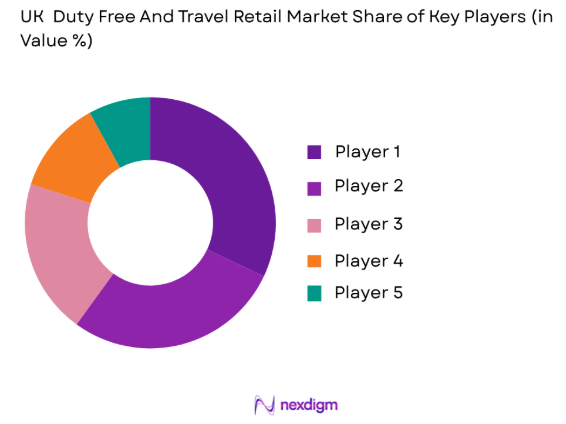

Competitive Landscape

The UK market is shaped by major travel retail companies leveraging global concession networks and local expertise to secure prime locations at leading airports. These players focus on omnichannel integration, loyalty programs, and exclusive travel retail products to maintain market leadership amid evolving traveler preferences and premium product demand.

| Company | Establishment Year | Headquarters | Retail Footprint | Brand Partnerships | Digital Integration | Exclusive Product Focus | Loyalty Programs | Retail Experience |

| Avolta (incl. Dufry) | 1865 | Switzerland | ~ | ~ | ~ | ~ | ~ | ~ |

| Lagardère Travel Retail | 1994 | France | ~ | ~ | ~ | ~ | ~ | ~ |

| WH Smith Travel | 1848 | UK | ~ | ~ | ~ | ~ | ~ | ~ |

| Shilla Duty Free | 1970 | South Korea | ~ | ~ | ~ | ~ | ~ | ~ |

| Gebr. Heinemann | 1879 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

UK Duty Free and Travel Retail Market Analysis

Growth Drivers

Increasing International and Domestic Air Traffic

The UK duty-free and travel retail market is benefitting from sustained growth in air travel, both international and domestic. Major airports such as London Heathrow, Gatwick, and Manchester have experienced increasing passenger volumes due to expanded routes and airline services. Rising passenger traffic directly enhances duty-free sales of cosmetics, fragrances, spirits, and luxury goods. Growth in domestic travel, supported by regional connectivity and post-pandemic recovery, also contributes to consistent footfall. Additionally, the UK’s position as a major global hub for business, education, and tourism further drives travel-related retail consumption. Retailers can leverage these trends by optimizing product placement and targeted promotions in high-traffic terminals and lounges.

Rising Disposable Income and Premium Travel Demand

Higher disposable income among UK travelers is driving increased spending on premium and branded products at airports and ports. Business travelers, affluent tourists, and premium-class passengers are more likely to purchase luxury goods, electronics, fashion, and high-end cosmetics. The demand for premium travel experiences also translates into higher spending in duty-free retail. Retailers can capitalize on these trends by curating exclusive product ranges, offering limited editions, and providing personalized shopping experiences. Urban centers like London, Birmingham, and Edinburgh, with large high-income populations, sustain frequent travel and contribute to a reliable customer base for duty-free operations across airports and ports.

Market Challenges

Regulatory and Taxation Constraints (Post-Brexit)

Post-Brexit regulations have created a complex legal environment for UK duty-free operators. New customs procedures, import tariffs, and VAT adjustments complicate inventory management and increase operational costs. Retailers face administrative challenges in complying with both UK and EU import/export rules, which can delay product availability and limit profitability. Additionally, fluctuating rules for travelers regarding allowances, restrictions, and documentation may affect sales volumes. International brands navigating this environment require expertise in post-Brexit trade policies, increasing operational overheads. Retailers must adapt quickly to changing legislation to maintain compliance while minimizing disruption to duty-free sales at airports and ports.

Competition from Online Retail Platforms

E-commerce growth poses a significant challenge to UK duty-free retail. Online platforms provide convenience, competitive pricing, and pre-order options, reducing impulse purchases at airport or port outlets. Travelers increasingly compare prices and promotions online before departure, impacting traditional in-terminal sales. This competition pressures retailers to integrate digital solutions, improve in-store experiences, and offer value-added services. Without strong omnichannel strategies, traditional duty-free operators risk losing market share to digital-first retailers. Retailers must adopt innovative approaches, such as mobile pre-ordering, loyalty programs, and click-and-collect services, to compete effectively against online alternatives and maintain relevance in an increasingly digital consumer landscape.

Market Opportunities

Expansion of Omnichannel Duty Free Solutions

UK duty-free operators can expand omnichannel solutions to integrate online and physical retail. Services like pre-ordering, click-and-collect, and digital promotions enhance convenience and drive sales beyond terminal foot traffic. Digital catalogues, mobile apps, and in-terminal kiosks allow personalized marketing and real-time inventory visibility. Omnichannel retail improves customer engagement and captures additional revenue from travelers who prefer shopping ahead of their trips. Integration of online and offline channels aligns with global retail trends and caters to digitally savvy passengers, helping UK operators maintain competitiveness in a market increasingly influenced by e-commerce and mobile-first shopping behaviors.

Growth in Experiential and Luxury Retail

Experiential retail provides UK duty-free operators opportunities to differentiate and increase revenue. Airports can offer immersive spaces with interactive displays, exclusive product launches, tasting sessions, and luxury brand activations. Experiential retail encourages longer dwell times, higher spending, and enhanced brand engagement, particularly for luxury fragrances, cosmetics, fashion, and spirits. Major international events and exhibitions in the UK, such as UEFA tournaments or trade shows in London, provide additional occasions to offer unique shopping experiences. By combining luxury retail with experiential elements, operators can position airports and ports as premium retail destinations, attracting affluent travelers and enhancing overall sales potential.

Future Outlook

Over the period to 2035, the UK Duty Free and Travel Retail market is expected to grow, driven by continued recovery in international travel, expansion of airport retail space, and premiumization of product offerings. Retailers will increasingly adopt digital pre‑order services, loyalty integration, and immersive retail formats to meet evolving traveler expectations and enhance engagement. Exclusive collaborations with luxury brands and curated collections are projected to boost average ticket values and market competitiveness. Growth in outbound travel from the UK and rising tourism inflow supports demand for diversified travel retail portfolios, while advancements in contactless retail and AI‑driven personalization are anticipated to enhance conversion rates and retail profitability.

Major Players

- Avolta AG (incl. Dufry)

- Lagardère Travel Retail

- WH Smith Travel Retail

- Shilla Duty Free

- Gebr. Heinemann

- DFS Group

- King Power International

- Aer Rianta International

- Dubai Duty Free

- Heathrow Airport Holdings (Retail Division)

- World Duty Free

- Lotte Duty Free

- Duty Free Americas

- Nuance Group

- Reg Staerker Retail

Key Target Audience

- Airport Operators and Concession Management Teams

- Duty Free and Travel Retail Operators

- Luxury Brand Owners and Distributors

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- Travel and Hospitality Infrastructure Investors

- Airline Retail and Ancillary Revenue Strategists

- Digital Retail and Omnichannel Solution Providers

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping the travel retail ecosystem across the UK, including passenger volumes, airport retail spaces, product categories, and consumer spending patterns. Secondary sources such as industry reports, airport authority data, and travel analytics platforms are used to identify drivers of market demand and structural dynamics.

Step 2: Market Analysis and Construction

Historical revenue data for duty free and travel retail channels are compiled to estimate the baseline market size. Revenue streams are segmented by distribution channel and product category, applying bottom‑up calculation methods to ensure alignment with retail sales performance and passenger traffic trends across UK travel hubs.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings regarding growth potential, segment dominance, and retail channel performance are validated through consultations with airport retail managers, duty free operators, and travel retail analysts. Insights from industry practitioners refine forecast assumptions and competitive positioning.

Step 4: Research Synthesis and Final Output

The final stage consolidates quantitative data and expert insights to produce a validated market forecast, segmentation analysis, and competitive landscape. Cross‑verification with industry benchmarks and passenger flow projections ensures accuracy and relevance for strategic decision‑making in the UK duty free and travel retail sector.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviationsm, Research Framework, Bottom-Up Market Estimation, Top-Down Validation, Retailer and Operator Revenue Benchmarking, Airport, Port, and Border Retail Assessment, Import-Export Trade Analysis, Consumer Behavior Mapping, Primary Interviews with Retail Operators and Suppliers, Forecasting Model, Limitations and Assumptions)

- Definition and Scope

- Evolution of Duty Free and Travel Retail in the UK

- Industry Ecosystem and Stakeholder Mapping

- Supply Chain and Value Chain Analysis

- Retail Infrastructure and Airport Terminal Assessment

- Growth Drivers

Increasing International and Domestic Air Traffic

Rising Disposable Income and Premium Travel Demand

Expansion of Airport and Port Infrastructure

Growth in Luxury and Branded Product Consumption

Tourism Promotion and Major International Events (e.g., UEFA, London Exhibitions) - Market Challenges

Regulatory and Taxation Constraints (Post-Brexit)

Currency Fluctuations and Import Duties

Competition from Online Retail Platforms

Limited Retail Space at Airports and Ports

Operational Challenges During Pandemics - Market Opportunities

Expansion of Omnichannel Duty Free Solutions

AI-Driven Personalized Shopping and Digital Engagement

Growth in Experiential and Luxury Retail

Partnerships with Airlines, Cruise Operators, and Airports

Promotion of UK Local Products and Tourism Integration - Market Trends

Digital Payments and Cashless Retail Adoption

Smart Shelving and Interactive Displays

Sustainable Packaging and Eco-Friendly Products

Loyalty Programs and Frequent Traveler Incentives

Integration of Augmented Reality and VR Experiences in Retail - Government Regulations

UK Duty-Free Policies and Tax Regulations

Civil Aviation Authority (CAA) Retail Guidelines

Tourism Promotion Incentives

Customs and Import Compliance Requirements

Post-Brexit Trade Agreements and Tariffs Impact - Porter’s Five Forces Analysis

- PESTLE Analysis

- Pricing Analysis

- Competition Ecosystem

- By Revenue, 2020-2025

- By Footfall/Passenger Volume, 2020-2025

- By Average Spend Per Passenger, 2020-2025

- By Product Category Contribution, 2020-2025

- By Product Category (in Value %)

Perfumes & Cosmetics

Alcohol & Tobacco

Confectionery & Snacks

Fashion & Accessories

Electronics & Gadgets

Local Souvenirs & Specialty Products - By Retail Format (in Value %)

Airport Duty Free Shops

Port and Cruise Retail

Border Shops

Downtown Travel Retail Outlets

Online Duty Free Platforms - By Consumer Type (in Value %)

International Tourists

Domestic Travelers

Business Travelers

Luxury Segment Customers - By Distribution (in Value %)

Direct Store Sales

Travel Retail Operator Partnerships

Online/Omnichannel

Third-Party Distributors - By Region (in Value %)

London Heathrow Airport Region

London Gatwick Airport Region

Manchester Airport Region

Glasgow and Edinburgh Airport Region

Belfast and Northern Ireland Airports

Other Regional Airports (Bristol, Birmingham, Liverpool)

- Market Share Analysis of Major Players (Revenue, Passenger Reach, Store Count)

- Market Share by Airport Retail Presence

- Cross Comparison Parameters(Company Overview, Airport Concession Portfolio, Travel Retail Revenue, Number of Duty Free Stores, Passenger Reach, Average Transaction Value, Luxury Brand Partnerships, Omnichannel Capabilities, Click-and-Collect Services, Loyalty Program Strength, Digital Engagement Strategy, Product Category Breadth, Exclusive Brand Launches, Sustainability Initiatives, Experiential Retail Capabilities, Geographic Presence)

- Competitive Benchmarking Matrix

- SWOT Analysis of Major Players

- Pricing Analysis by Product Category and Retail Format

- Detailed Profiles of Major Companies

Dufry AG

Lagardère Travel Retail

World Duty Free Group

Shilla Duty Free

Heathrow Airport Retail Operators

Aer Rianta International – UK

Nuance Group

DFS Group

HMSHost International

Brockmans Travel Retail

WHSmith Travel Retail

King Power International – UK Operations

Aelia Duty Free

The Nuance Group (Regional UK Airports)

Gebr. Heinemann UK

- International Passenger Purchase Behavior Analysis

- Business Traveler Spending Analysis

- Luxury Consumer Shopping Preferences

- Cruise Passenger Retail Spending Assessment

- Digital Shopper and Omnichannel User Analysis

- Traveler Pain Points and Purchase Decision Mapping

- Budget Allocation and Spending Pattern Analysis

- By Revenue, 2026-2035

- By Footfall/Passenger Volume, 2026-2035

- By Average Spend Per Passenger, 2026-2035

- By Product Category Contribution, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now