Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UK Electric Vehicle Market demonstrates significant expansion driven by accelerating electrification of the transportation sector and supportive regulatory frameworks promoting zero emission mobility. According to data published by the International Energy Agency, electric vehicle sales generated approximately USD ~ billion in consumer spending across the United Kingdom based on a recent historical assessment. Demand is supported by strong government incentives, nationwide charging infrastructure expansion, and growing consumer awareness regarding sustainable transportation, which collectively stimulate increasing adoption of battery powered passenger vehicles and commercial fleets.

Dominant adoption is concentrated in metropolitan regions where infrastructure availability, policy incentives, and urban mobility needs strongly encourage electric mobility. Cities such as London, Birmingham, and Manchester lead adoption due to extensive charging networks, clean air regulations, and large urban commuting populations. London alone operates more than USD ~ thousand public charging points according to the UK Department for Transport, enabling widespread vehicle electrification across private mobility, ride hailing services, and corporate fleets operating within dense metropolitan transport networks.

Market Segmentation

By Product Type

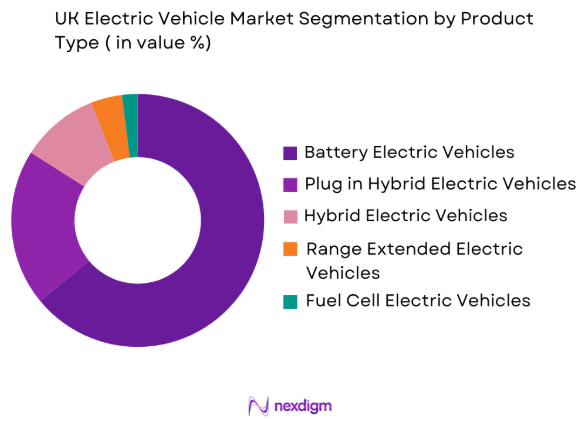

UK Electric Vehicle market is segmented by product type into Battery Electric Vehicles, Plug in Hybrid Electric Vehicles, Hybrid Electric Vehicles, Fuel Cell Electric Vehicles, and Range Extended Electric Vehicles. Recently, Battery Electric Vehicles has a dominant market share due to factors such as rapid expansion of public charging infrastructure, strong manufacturer focus on fully electric platforms, and government policies prioritizing zero emission vehicles. Automotive manufacturers including Tesla, Volkswagen, and BMW have significantly expanded BEV product portfolios across passenger and commercial vehicle categories, increasing consumer accessibility. Battery technology advancements have improved driving range while reducing charging time, which further supports BEV adoption.

By Vehicle Type

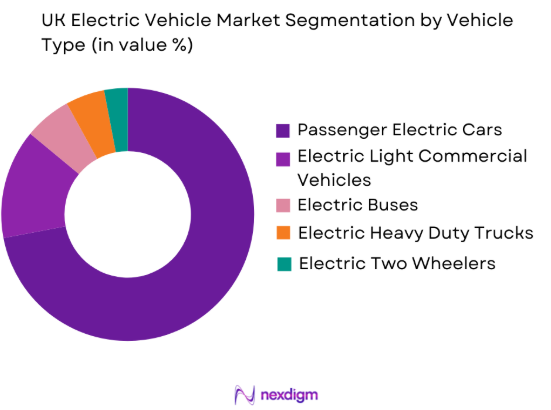

UK Electric Vehicle market is segmented by vehicle type into Passenger Electric Cars, Electric Light Commercial Vehicles, Electric Buses, Electric Two Wheelers, and Electric Heavy Duty Trucks. Recently, Passenger Electric Cars has a dominant market share due to rising consumer adoption driven by government purchase incentives, expanding model availability, and growing urban charging infrastructure. Automakers increasingly prioritize passenger electric vehicle production because this segment represents the largest consumer mobility demand across urban and suburban regions. Fleet operators also contribute to demand through electrification of ride sharing and car leasing services.

Competitive Landscape

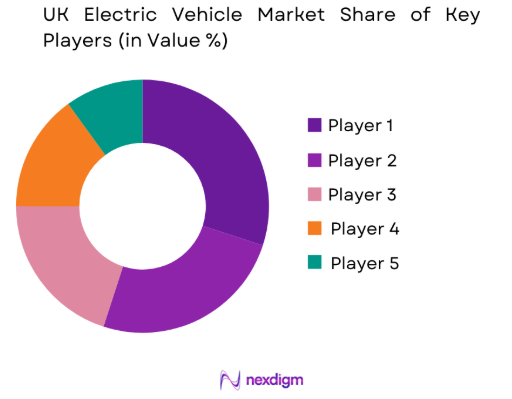

The UK Electric Vehicle Market features a moderately consolidated competitive landscape characterized by strong participation from global automotive manufacturers alongside emerging electric mobility companies. Major automakers invest heavily in electrified vehicle platforms, battery technology development, and charging infrastructure partnerships to strengthen market presence. Companies such as Tesla, Volkswagen Group, BMW Group, and Hyundai Motor Company dominate technological innovation through advanced battery systems and software integrated mobility solutions, while traditional manufacturers accelerate electrification strategies to maintain competitiveness.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | EV Battery Platform |

| Tesla | 2003 | United States | ~ | ~ | ~ | ~ | ~ |

| Volkswagen Group | 1937 | Germany | ~ | ~ | ~ | ~ | ~ |

| BMW Group | 1916 | Germany | ~ | ~ | ~ | ~ | ~ |

| Hyundai Motor Company | 1967 | South Korea | ~ | ~ | ~ | ~ | ~ |

| Nissan Motor Company | 1933 | Japan | ~ | ~ | ~ | ~ | ~ |

UK Electric Vehicle Market Analysis

Growth Drivers

Rapid Expansion of National EV Charging Infrastructure Across the United Kingdom

Rapid expansion of public electric vehicle charging infrastructure across the United Kingdom is accelerating adoption of electric mobility as government agencies and private operators deploy charging stations across cities, highways, and residential areas. Charging accessibility is a key factor influencing consumer adoption, prompting national programs led by the Department for Transport and the Office for Zero Emission Vehicles to support infrastructure investment. Retail centers, workplaces, and residential complexes increasingly integrate charging facilities to improve convenience for drivers. Expansion of rapid charging corridors also supports electrification of commercial fleets such as delivery vehicles and ride sharing services, while smart grid integrated charging systems improve energy distribution efficiency.

Accelerating Government Policy Support for Zero Emission Transportation

Strong government policy frameworks promoting transportation decarbonization are accelerating expansion of the UK Electric Vehicle Market as national and regional authorities introduce regulations encouraging adoption of zero emission mobility solutions. Policies including purchase incentives, tax exemptions, and infrastructure investment programs support electric vehicle affordability and accessibility. Government funding for electrification of public transportation and corporate fleets also strengthens demand for electric mobility. Clean air zones introduced across major cities encourage drivers and businesses to shift from internal combustion vehicles to electric alternatives. Regulatory initiatives further stimulate domestic investment in electric vehicle manufacturing, battery production, and charging infrastructure development across the United Kingdom.

Market Challenges

High Upfront Purchase Cost of Electric Vehicles Compared with Conventional Vehicles

High purchase cost of electric vehicles remains a major barrier limiting wider consumer adoption within the UK Electric Vehicle Market despite technological progress and government incentives aimed at reducing ownership costs. Battery systems represent a significant portion of vehicle manufacturing expenses, resulting in higher retail prices compared with conventional internal combustion vehicles. Consumers often evaluate upfront purchase costs alongside long term operating savings, which can slow adoption decisions. Raw materials such as lithium, cobalt, and nickel also contribute to higher production costs due to global supply volatility. Although government incentives and financing options help reduce initial expenses, affordability challenges continue influencing consumer purchasing behavior.

Limited Charging Infrastructure Accessibility in Rural and Remote Regions

Uneven distribution of charging infrastructure across the United Kingdom creates challenges for electric vehicle adoption in rural areas where charging availability remains limited compared with major cities. Urban regions such as London and Birmingham benefit from dense networks of public charging stations across commercial centers and residential areas. Rural communities often face longer distances between charging locations, increasing range anxiety for drivers. Infrastructure expansion in these areas requires significant investment in grid capacity and charging equipment. Private charging providers frequently prioritize high demand urban locations, slowing deployment in rural regions. Expanding charging infrastructure across underserved areas remains essential for supporting wider electric vehicle adoption nationwide.

Opportunities

Expansion of Electric Commercial Vehicle Fleets for Urban Logistics and Delivery Services

Rapid expansion of e commerce and urban logistics activities across the United Kingdom is creating strong opportunities for electric commercial vehicles as delivery companies transition fleets toward zero emission transportation solutions. Urban distribution networks operated by retailers, courier services, and food delivery platforms require frequent vehicle movement within densely populated cities where emission regulations increasingly restrict diesel powered vehicles. Electric light commercial vehicles provide efficient solutions for last mile delivery because they offer lower operating costs and reduced noise levels. Logistics companies are investing in electric fleets supported by charging infrastructure installed within distribution hubs. Growing demand for sustainable freight transportation continues to accelerate adoption of electric commercial delivery vehicles.

Growth of Domestic Electric Vehicle Manufacturing and Battery Supply Chain Development

Expansion of domestic electric vehicle manufacturing and battery supply chain infrastructure is creating significant economic opportunities within the UK Electric Vehicle Market as government programs and private sector investments support local production of advanced mobility technologies. Development of large battery gigafactories and electric vehicle assembly plants strengthens domestic automotive manufacturing while reducing reliance on imported battery components. Localized production improves supply chain resilience and reduces logistics costs for manufacturers. Investment in battery research accelerates advancements in lithium ion and solid state technologies. Growing collaboration between automotive companies, technology firms, and research institutions also strengthens innovation ecosystems supporting electric mobility development across the United Kingdom.

Future Outlook

The UK Electric Vehicle Market is expected to experience sustained expansion as transportation electrification continues to accelerate across passenger mobility, commercial transportation, and public transit systems. Technological progress in battery performance and charging technology will improve vehicle efficiency and reduce operating costs for electric mobility solutions. Government decarbonization policies and emission regulations will further strengthen adoption of zero emission transportation. Increasing consumer awareness regarding environmental sustainability combined with expanding charging infrastructure will support long term electric vehicle adoption across the national transportation ecosystem.

Major Players

- Tesla

- Volkswagen Group

- BMW Group

- Hyundai Motor Company

- Nissan Motor Company

- Mercedes Benz Group

- Ford Motor Company

- Volvo Cars

- Stellantis

- SAIC Motor

- BYD

- Rivian Automotive

- XPeng Motors

- Toyota Motor Corporation

- Kia Corporation

Key Target Audience

- Electric vehicle manufacturers

- Automotivecomponentsuppliers

- Battery manufacturers

- Charging infrastructure developers

- Logistics and fleet operators

- Investments and venture capitalist firms

- Government and regulatory bodies

- Energy utilities and grid operators

Research Methodology

Step 1: Identification of Key Variables

The research process begins by identifying key market variables influencing the UK Electric Vehicle Market including vehicle sales volume, charging infrastructure deployment, consumer demand patterns, and government policy frameworks. Macroeconomic indicators, transportation policies, and technological innovation trends are also evaluated to determine their impact on electric mobility adoption across the United Kingdom.

Step 2: Market Analysis and Construction

Comprehensive market analysis is conducted using secondary data sources including government transportation databases, international energy organizations, automotive industry reports, and manufacturer disclosures. Market structures, value chains, and technology adoption patterns are examined to construct a detailed representation of the electric mobility ecosystem operating within the national transportation sector.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings are validated through consultation with industry experts including automotive engineers, charging infrastructure operators, and transportation policy analysts. Expert insights provide practical perspectives regarding technological trends, regulatory frameworks, and operational challenges influencing electric vehicle adoption across the United Kingdom.

Step 4: Research Synthesis and Final Output

Validated research insights are synthesized into structured analytical frameworks to generate comprehensive market intelligence covering competitive landscapes, technological developments, and strategic industry trends. Final research outputs are designed to support strategic decision making for organizations operating within the electric mobility ecosystem.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of National EV Charging Infrastructure

Government Incentives Supporting Electric Mobility Adoption

Automotive Industry Electrification Investments - Market Challenges

High Initial Cost of Electric Vehicles

Battery Supply Chain Constraints

Charging Infrastructure Accessibility in Rural Areas - Market Opportunities

Expansion of Public Charging Networks

Growth in Electric Commercial Fleet Adoption

Technological Advancements in Battery Energy Density - Trends

Integration of Smart Charging and Vehicle to Grid Technologies

Growth of Electric Mobility Subscription Models

Increasing Localization of EV Manufacturing - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Battery Electric Vehicles

Plug-in Hybrid Electric Vehicles

Hybrid Electric Vehicles

Fuel Cell Electric Vehicles

Range Extended Electric Vehicles - By Platform Type (In Value%)

Passenger Cars

Commercial Vehicles

Electric Buses

Electric Two Wheelers

Fleet Mobility Vehicles - By Fitment Type (In Value%)

OEM Factory Installed Systems

Aftermarket EV Conversions

Integrated Vehicle Platforms

Modular Battery Platforms

Retrofitted Electric Powertrains - By End User Segment (In Value%)

Private Consumers

Corporate Fleet Operators

Ride Hailing and Mobility Platforms

Public Transportation Authorities

Logistics and Delivery Companies - By Procurement Channel (In Value%)

Authorized Dealership Sales

Online Direct Manufacturer Sales

Vehicle Leasing Providers

Corporate Fleet Procurement Contracts

Government Procurement Programs

- Market Share Analysis

- Cross Comparison Parameters (Battery Technology, Vehicle Range, Charging Capability, Pricing Strategy, Distribution Network, Battery Capacity, Charging Time, Vehicle Performance, Manufacturing Scale, Supply Chain Integration, Software Integration, After Sales Service Network)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Tesla

BYD

Volkswagen Group

BMW Group

Mercedes-Benz Group

Hyundai Motor Company

Kia Corporation

Nissan Motor Co.

Toyota Motor Corporation

Volvo Cars

Ford Motor Company

Stellantis

SAIC Motor

Rivian Automotive

XPeng Motors

- Increasing Adoption by Urban Commuters Seeking Low Emission Transport

- Corporate Fleets Transitioning Toward Electrified Mobility

- Public Transportation Authorities Electrifying Bus Networks

- Logistics Companies Deploying Electric Delivery Vehicles

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now