Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the UK EV battery market recorded a market value of approximately USD ~ billion, supported by accelerating electric vehicle adoption and expanding domestic battery manufacturing initiatives. Demand is driven by rising electric passenger vehicle registrations, government backed zero emission mobility policies, and investments in large scale battery production facilities. Automotive manufacturers are increasingly localizing battery supply chains to reduce dependency on imports while ensuring stable component availability. Rapid development of gigafactory infrastructure and growing demand for lithium ion battery packs across electric vehicles continues to expand the market ecosystem.

Based on a recent historical assessment, the UK EV battery market demonstrates strong geographic concentration around major automotive manufacturing and technology clusters including Sunderland, Birmingham, Oxfordshire, and Coventry. These regions host key electric vehicle production facilities, battery research laboratories, and advanced engineering centers supporting battery innovation and manufacturing scale up. Sunderland has emerged as a critical hub due to the presence of integrated electric vehicle and battery production operations, while Midlands based automotive clusters support advanced battery engineering and supply chain integration across multiple vehicle manufacturers operating in the country.

Market Segmentation

By Battery Chemistry Type

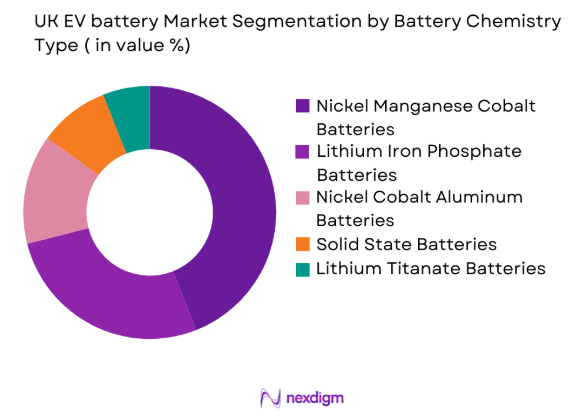

UK EV battery market is segmented by battery chemistry type into lithium iron phosphate batteries, nickel manganese cobalt batteries, nickel cobalt aluminum batteries, solid state batteries, and lithium titanate batteries. Recently, nickel manganese cobalt batteries have a dominant market share due to factors such as higher energy density, strong compatibility with passenger electric vehicles, and widespread adoption by automotive manufacturers. Vehicle producers prioritize this chemistry because it balances driving range, charging performance, and battery lifespan. Major electric vehicle manufacturers operating in the UK integrate nickel manganese cobalt battery packs within passenger cars and commercial electric vehicles to ensure long driving ranges and stable power output. Consumer demand for long range electric vehicles further accelerates adoption of this battery chemistry across domestic automotive production facilities.

By Vehicle Platform

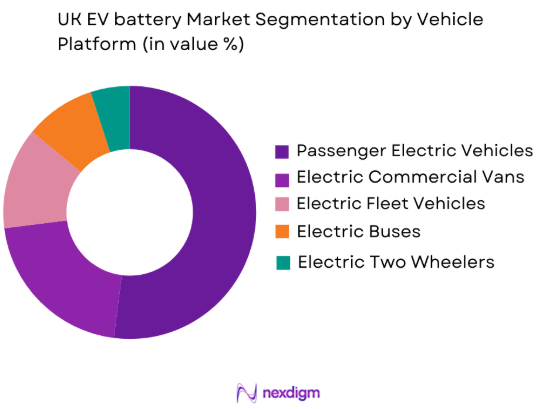

UK EV battery market is segmented by vehicle platform into passenger electric vehicles, electric commercial vans, electric buses, electric fleet vehicles, and electric two wheelers. Recently, passenger electric vehicles have a dominant market share due to factors such as consumer adoption trends, government incentives supporting electric mobility, and rapid expansion of charging infrastructure across urban areas. Passenger vehicles represent the largest category of electric vehicle registrations within the country which directly increases demand for high capacity battery packs. Automotive manufacturers prioritize passenger EV production because it aligns with national emission reduction targets and growing consumer demand for sustainable mobility solutions. Battery pack suppliers therefore allocate significant production capacity toward passenger EV platforms.

Competitive Landscape

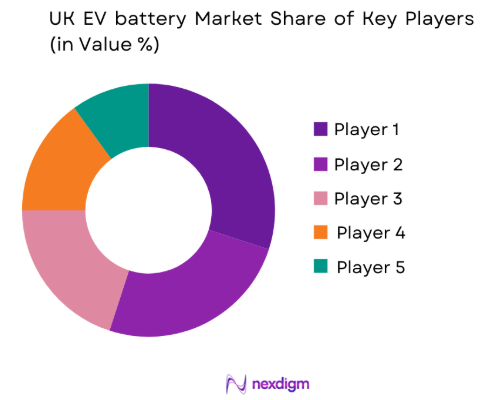

The UK EV battery market is moderately consolidated with strong influence from global battery manufacturers and emerging domestic technology firms. Automotive manufacturers maintain strategic partnerships with battery suppliers to secure long term battery supply agreements. International battery producers dominate current supply chains while domestic gigafactory initiatives aim to strengthen local production capacity. Competition is shaped by battery chemistry innovation, manufacturing scalability, supply chain localization, and partnerships with electric vehicle manufacturers expanding production operations within the United Kingdom.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Battery Chemistry Portfolio |

| LG Energy Solution | 2020 | South Korea | ~ | ~ | ~ | ~ | ~ |

| Panasonic Energy | 1918 | Japan | ~ | ~ | ~ | ~ | ~ |

| CATL | 2011 | China | ~ | ~ | ~ | ~ | ~ |

| Samsung SDI | 1970 | South Korea | ~ | ~ | ~ | ~ | ~ |

| Envision AESC | 2007 | Japan | ~ | ~ | ~ | ~ | ~ |

UK EV battery Market Analysis

Growth Drivers

Expansion of Electric Vehicle Manufacturing Across Automotive Plants

Rapid expansion of electric vehicle manufacturing across automotive plants in the United Kingdom significantly drives growth of the UK EV battery market because vehicle production requires large scale battery supply. Automotive manufacturers are transitioning conventional production lines toward electric vehicle platforms to comply with emission reduction policies and increasing demand for sustainable mobility. Companies such as Nissan and Jaguar Land Rover are investing in electric vehicle assembly operations supported by battery supply partnerships. Increasing EV production directly raises demand for lithium ion battery systems used in vehicle powertrains. As manufacturing expands across automotive clusters including Sunderland and the Midlands, battery suppliers continue increasing local production capacity and supply chain integration.

Government Policies Supporting Electric Mobility and Domestic Battery Production

Strong government policy frameworks supporting electric mobility and domestic battery production significantly accelerate growth in the UK EV battery market by encouraging investments in battery manufacturing infrastructure and electric vehicle adoption. National emission reduction strategies promote transportation electrification through incentives that support EV purchases and encourage manufacturers to shift production toward electric platforms. Policy initiatives also prioritize domestic battery production to reduce dependence on imported battery cells and strengthen supply chain resilience. Government funding programs support gigafactory development, battery technology research, and advanced manufacturing capabilities. These initiatives foster collaboration between automotive companies, technology developers, and research institutions while stimulating private sector investment in large scale battery production facilities.

Market Challenges

Limited Domestic Supply of Critical Battery Minerals

Limited domestic availability of critical battery minerals presents a major challenge for the UK EV battery market because lithium ion battery production relies heavily on raw materials such as lithium, cobalt, nickel, and graphite sourced from international mining regions. Dependence on imported minerals exposes manufacturers to supply chain volatility, geopolitical risks, and potential cost fluctuations. Growing global demand for these materials, driven by expanding electric vehicle production, intensifies competition among battery manufacturers. Supply disruptions or price increases can significantly impact battery manufacturing costs and production timelines. Although recycling technologies are emerging to recover valuable minerals from used batteries, large scale recycling infrastructure remains under development, limiting short term supply diversification.

High Capital Requirements for Battery Manufacturing Infrastructure

High capital investment requirements for establishing battery manufacturing facilities present a major challenge for the UK EV battery market because gigafactory scale production requires billions of dollars in infrastructure development. Battery production plants demand specialized equipment, advanced automation systems, and controlled manufacturing environments to ensure safe and efficient battery cell production. Companies must also invest heavily in supply chain integration including cathode production, battery pack assembly, and quality testing infrastructure. These investments create financial barriers for new market entrants seeking to develop domestic battery manufacturing capacity. Additionally, manufacturers must allocate significant funding for research and development to improve battery energy density, charging performance, and safety standards.

Opportunities

Development of Large Scale Domestic Battery Gigafactories

Development of large scale battery gigafactories presents a significant opportunity for the UK EV battery market as domestic battery production enables automotive manufacturers to secure reliable supply chains while reducing dependence on imported battery cells. Government supported initiatives are encouraging private sector investments in gigafactory infrastructure capable of producing millions of battery cells annually. These facilities integrate advanced automation and manufacturing technologies that improve production efficiency and reduce battery costs. Domestic gigafactory development also stimulates economic activity by creating skilled employment and strengthening industrial supply chains linked to electric mobility. Localized battery production allows automakers to coordinate supply more efficiently and develop battery technologies tailored to vehicles manufactured within the country.

Advancement of Next Generation Solid State Battery Technologies

Advancement of solid state battery technologies presents strong opportunities for the UK EV battery market as these next generation batteries provide higher energy density, improved safety, and faster charging compared with conventional lithium ion batteries. Solid state batteries use solid electrolytes that enhance thermal stability and reduce risks associated with overheating and battery degradation. Automotive manufacturers and battery developers are investing in research initiatives to accelerate commercialization of this technology. Higher energy density enables electric vehicles to achieve longer driving ranges with compact battery packs. Collaboration between automotive companies, research institutions, and battery startups across the United Kingdom continues strengthening innovation and technology development.

Future Outlook

The UK EV battery market is expected to experience sustained expansion driven by continued electric vehicle adoption, increasing domestic battery manufacturing capacity, and rapid technological advancements in battery chemistry. Government policies encouraging zero emission mobility will continue supporting market demand while automotive manufacturers expand electric vehicle production across domestic facilities. Gigafactory development initiatives will strengthen supply chain localization and enhance battery availability. Additionally, innovations in battery energy density and charging technologies are expected to improve electric vehicle performance and accelerate consumer adoption across the transportation sector.

Major Players

- LG Energy Solution

- Panasonic Energy

- CATL

- Samsung SDI

- Envision AESC

- BYD Company

- SK On

- Northvolt

- ACC Automotive Cells Company

- EVE Energy

- FarasisEnergy

- ProLogiumTechnology

- StoreDot

- AMTE Power

- Britishvolt

Key Target Audience

- Automotive manufacturers

- Electric vehicle battery manufacturers

- Battery material suppliers

- Electric mobility infrastructure developers

- Logistics and fleet operators

- Energy utilities and grid operators

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Primary research begins with identification of major variables influencing the UK EV battery market including production capacity, electric vehicle demand, battery chemistry adoption, supply chain structure, and regulatory policies supporting electric mobility.

Step 2: Market Analysis and Construction

Market models are constructed by integrating data from automotive industry reports, government policy publications, electric vehicle registration databases, and battery manufacturing statistics to estimate market structure and demand dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including battery engineers, automotive executives, and policy specialists are consulted to validate research assumptions and confirm technological trends influencing battery production and electric vehicle deployment.

Step 4: Research Synthesis and Final Output

Collected data is synthesized through analytical frameworks to generate market insights, competitive assessments, and strategic forecasts describing the evolution of the UK EV battery market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government Incentives Supporting Electric Vehicle Battery Production

Expansion of Electric Vehicle Manufacturing Across Automotive Plants

Rapid Growth in Charging Infrastructure Supporting Battery Demand - Market Challenges

Supply Chain Constraints for Critical Battery Minerals

High Capital Investment Requirements for Battery Gigafactories

Battery Recycling and End of Life Management Complexity - Market Opportunities

Expansion of Domestic Battery Gigafactories

Advancement of Solid State Battery Technology

Growth of Battery Recycling and Circular Economy Solutions - Trends

Localization of EV Battery Manufacturing Facilities

Increasing Adoption of High Energy Density Battery Chemistries

Integration of Battery Management Software with Vehicle Platforms - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier 2020-2025

- By System Type (In Value%)

Lithium Iron Phosphate Battery Systems

Nickel Manganese Cobalt Battery Systems

Nickel Cobalt Aluminum Battery Systems

Solid State Battery Systems

Lithium Titanate Battery Systems - By Platform Type (In Value%)

Passenger Electric Vehicles

Electric Commercial Vans

Electric Buses

Electric Two Wheelers

Electric Fleet Vehicles - By Fitment Type (In Value%)

OEM Installed Battery Systems

Aftermarket Replacement Batteries

Battery Swapping Modules

Integrated Vehicle Battery Packs

Modular Battery Pack Systems - By End User Segment (In Value%)

Passenger Vehicle Manufacturers

Commercial Fleet Operators

Public Transport Authorities

Logistics and Delivery Companies

Ride Hailing and Mobility Providers - By Procurement Channel (In Value%)

Direct Supply Contracts with Automakers

Government Fleet Procurement Programs

Long Term Supply Agreements

Battery Leasing Providers

Energy Storage and Mobility Integrators

- Market Share Analysis

- Cross Comparison Parameters (Battery Chemistry Portfolio, Manufacturing Capacity, Supply Chain Integration, OEM Partnerships, R&D Investment, Energy Density Performance, Battery Pack Cost Structure, Recycling Capability, Gigafactory Expansion Strategy, Battery Management System Technology)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

LG Energy Solution

Panasonic Energy

CATL

BYD Company

Samsung SDI

SK On

Northvolt

Envision AESC

Britishvolt

AMTE Power

Farasis Energy

ACC Automotive Cells Company

EVE Energy

StoreDot

ProLogium Technology

- Automotive manufacturers increasing battery sourcing agreements with domestic suppliers

- Logistics companies transitioning fleet vehicles toward electrified delivery operations

- Public transport agencies adopting electric buses requiring large battery packs

- Mobility service providers investing in long range electric vehicles with advanced batteries

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now