Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UK EV charging infrastructure market represents a rapidly expanding segment of the national energy and transportation ecosystem as the electrification of mobility accelerates across passenger vehicles and commercial fleets. Based on a recent historical assessment, the market generated approximately USD ~ billion in infrastructure deployment value supported by public investment programs, private charging network expansion, and increasing installation of high power rapid charging systems across highways, retail centers, and urban parking facilities according to BloombergNEF and the UK Department for Transport.

London, Birmingham, Manchester, and Glasgow represent the most active charging infrastructure hubs because these metropolitan regions concentrate high electric vehicle adoption levels, strong municipal sustainability programs, and significant public investment in urban charging networks. Strategic highway corridors across England and Scotland also host dense rapid charging installations that support intercity electric travel. Local authorities collaborate with private charging operators to deploy on street and residential charging stations where households lack private parking facilities.

Market Segmentation

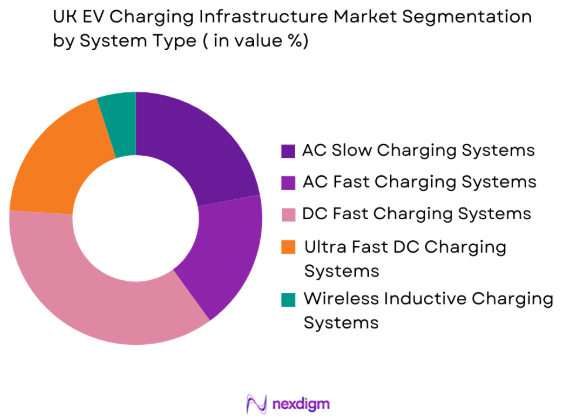

By System Type

UK EV Charging Infrastructure market is segmented by product type into AC slow charging systems, AC fast charging systems, DC fast charging systems, ultra fast DC charging systems, and wireless inductive charging systems. Recently, DC fast charging systems have a dominant market share due to factors such as increasing electric vehicle travel distances, the need for rapid charging capabilities along highways, and strong investment by private charging network operators. Public infrastructure providers prioritize DC fast chargers because they significantly reduce vehicle charging time and improve station utilization rates. Government infrastructure strategies also encourage deployment of rapid chargers along major transport corridors to enable long distance EV travel while improving charging accessibility for commercial fleets and ride hailing operators.

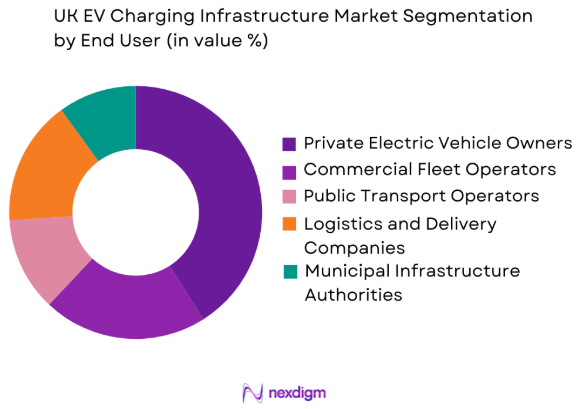

By End User Segment

UK EV Charging Infrastructure market is segmented by end user segment into private electric vehicle owners, commercial fleet operators, public transport operators, logistics and delivery companies, and municipal infrastructure authorities. Recently, private electric vehicle owners have a dominant market share due to expanding passenger EV ownership and growing demand for accessible charging across residential and public parking environments. Urban households without private driveways depend on public charging stations, encouraging municipalities and charging providers to deploy extensive curbside and destination chargers. The rapid expansion of retail parking chargers, workplace charging networks, and residential street infrastructure has further strengthened the position of private EV drivers as the largest user base of public charging infrastructure.

Competitive Landscape

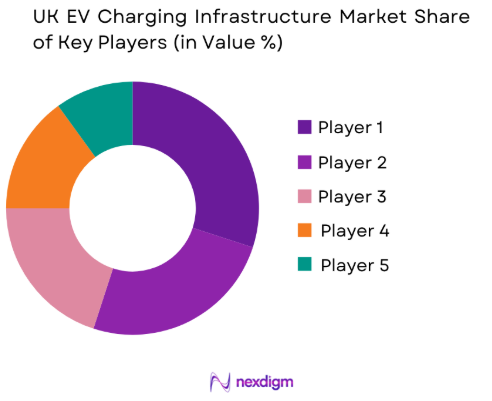

The UK EV charging infrastructure market demonstrates moderate consolidation where several major network operators control large public charging networks while numerous regional providers deploy localized infrastructure. Energy companies, oil and gas majors, and specialized charging technology firms compete by expanding charging coverage, improving charging speeds, and integrating digital payment systems. Strategic partnerships between automotive manufacturers, electricity utilities, and infrastructure investors also influence competitive positioning as operators race to establish nationwide rapid charging networks.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Charging Network Size |

| BP Pulse | 2008 | London, UK | ~ | ~ | ~ | ~ | ~ |

| Tesla | 2003 | Austin, USA | ~ | ~ | ~ | ~ | ~ |

| Pod Point | 2009 | London, UK | ~ | ~ | ~ | ~ | ~ |

| ChargePoint | 2007 | California, USA | ~ | ~ | ~ | ~ | ~ |

| Gridserve | 2019 | London, UK | ~ | ~ | ~ | ~ | ~ |

UK EV Charging Infrastructure Market Analysis

Growth Drivers

Expansion of National Electric Vehicle Infrastructure Funding Programs

Government policy support plays a major role in expanding the UK EV charging infrastructure market as public funding programs accelerate nationwide charger deployment. National EV infrastructure strategies prioritize rapid chargers along highways, residential streets, and commercial parking areas to support electric vehicle adoption. Funding initiatives from the Office for Zero Emission Vehicles provide incentives for local authorities and infrastructure providers to install charging points in urban communities with limited private charging access. Municipal governments collaborate with private charging operators to deploy curbside charging stations. Investments in highway rapid charging corridors improve long distance electric travel while encouraging private sector participation in infrastructure development.

Rising Electric Vehicle Adoption Across Passenger and Commercial Fleet Segments

Rising adoption of electric vehicles across passenger cars and commercial fleets is significantly increasing demand for EV charging infrastructure across the United Kingdom. Electric vehicles require reliable charging access at homes, workplaces, and public locations to support daily transportation needs. National decarbonization goals, urban emission regulations, and growing consumer awareness of sustainability are accelerating the shift toward electric mobility. Logistics companies, ride hailing operators, and delivery fleets increasingly deploy electric vehicles to reduce fuel costs and comply with environmental regulations. Public transport authorities are also electrifying bus fleets, which requires high capacity depot charging infrastructure. These developments continue to expand nationwide demand for charging networks.

Market Challenges

Grid Capacity Constraints and Local Electricity Distribution Limitations

Electricity distribution networks across several regions of the United Kingdom face infrastructure constraints that complicate installation of high power EV charging stations. Rapid chargers require substantial electrical capacity that may exceed available power supply within local grids. Upgrading distribution infrastructure often requires regulatory approvals, engineering work, and high capital investment. Charging network operators must coordinate closely with electricity utilities to assess grid capacity before installing new chargers. In some urban locations existing networks cannot support ultra rapid charging without substation upgrades. These limitations slow deployment in areas experiencing fast electric vehicle adoption. Smart charging technologies help manage electricity demand and maintain grid stability.

High Capital Costs of Ultra Fast Charging Infrastructure Deployment

Deployment of high power EV charging stations requires substantial capital investment covering equipment procurement, grid connection upgrades, site preparation, and long term maintenance. Ultra fast chargers use specialized electrical components and cooling systems that significantly increase installation costs compared with slower charging technologies. Infrastructure providers must also secure strategic locations such as highway service areas, commercial parking facilities, and retail destinations to ensure driver accessibility. These locations often involve leasing costs or revenue sharing agreements with property owners. Charging operators must achieve adequate utilization rates to recover investment costs. Maintenance requirements and operational reliability expectations further increase long term expenditure for charging network providers.

Opportunities

Expansion of Smart Charging and Energy Management Platforms

Smart charging technologies present a major opportunity for the UK EV charging infrastructure market as they optimize electricity consumption and improve grid stability. Smart charging systems allow stations to adjust electricity demand based on grid capacity and energy pricing conditions. This capability helps operators reduce electricity costs by shifting charging activity to off peak periods. Energy management platforms can also integrate renewable electricity sources such as solar power with charging infrastructure. Fleet operators benefit from scheduled charging during low demand periods. Utilities and technology providers are investing in software platforms that monitor charger performance, optimize energy use, and enable digital payments across charging networks.

Integration of Renewable Energy Powered Charging Stations

Renewable energy integration presents a strong opportunity for EV charging infrastructure expansion across the United Kingdom as the country advances toward a low carbon energy system. Charging stations powered by solar panels or wind energy reduce emissions associated with vehicle charging while improving sustainability outcomes. Infrastructure developers increasingly integrate local renewable generation within charging hubs to supply clean electricity. Solar canopy installations above parking areas also generate power while protecting vehicles. Renewable powered charging stations enhance energy resilience by lowering dependence on grid electricity during peak demand periods. Corporate sustainability commitments from retailers, logistics operators, and commercial property developers are encouraging wider deployment of renewable integrated charging infrastructure across transportation networks.

Future Outlook

The UK EV charging infrastructure market is expected to expand steadily as electric vehicle adoption accelerates across passenger mobility and commercial transport sectors. Infrastructure operators are expected to deploy more ultra rapid charging hubs along highways and urban centers. Government policy frameworks supporting zero emission transport will continue encouraging investment in charging networks. Technological improvements in smart charging and renewable integration will also strengthen the efficiency and sustainability of the national charging ecosystem.

Major Players

- BP Pulse

- Tesla

- Pod Point

- ChargePoint

- Gridserve

- Instavolt

- Ionity

- Shell Recharge Solutions

- Connected Kerb

- ABB E Mobility

- SiemenseMobility

- EO Charging

- Blink Charging

- SwarcoSmart Charging

- Allego

Key Target Audience

- Electric vehicle charging network operators

- Automotive manufacturers

- Battery and power electronics manufacturers

- Logistics and fleet operators

- Energy utilities and grid operators

- Investments and venture capitalist firms

- Government and regulatory bodies

- Commercial real estate developers

Research Methodology

Step 1: Identification of Key Variables

The research process begins by identifying the core market variables influencing the EV charging infrastructure sector including charging technology, installation infrastructure, policy frameworks, electric vehicle adoption rates, and electricity network integration factors.

Step 2: Market Analysis and Construction

Data from government databases, industry publications, infrastructure deployment records, and corporate financial reports are evaluated to construct the market structure and identify infrastructure deployment trends.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including infrastructure developers, electric vehicle manufacturers, and energy sector analysts are consulted to validate key assumptions and ensure that technological and policy developments are accurately reflected.

Step 4: Research Synthesis and Final Output

All collected data and analytical insights are synthesized into a structured market framework that evaluates infrastructure deployment patterns, competitive positioning, regulatory developments, and technology evolution.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of National EV Charging Infrastructure Funding Programs

Rising Electric Vehicle Adoption Across Passenger and Fleet Segments

Integration of High Power Rapid Charging Technologies - Market Challenges

Grid Capacity Constraints and Local Distribution Limitations

High Capital Costs of Ultra Fast Charging Installations

Fragmented Charging Network Interoperability Standards - Market Opportunities

Expansion of Smart Charging and Energy Management Systems

Integration of Renewable Energy Powered Charging Stations

Growth of Fleet Depot Charging Infrastructure - Trends

Deployment of Ultra Rapid Highway Charging Corridors

Growth of Charging Hubs in Retail and Urban Parking Locations

Adoption of Vehicle to Grid Charging Capabilities - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AC Slow Charging Systems

AC Fast Charging Systems

DC Fast Charging Systems

Ultra Fast DC Charging Systems

Wireless Inductive Charging Systems - By Platform Type (In Value%)

Public Charging Networks

Residential Charging Systems

Workplace Charging Platforms

Commercial Fleet Charging Platforms

Highway Rapid Charging Corridors - By Fitment Type (In Value%)

Standalone Charging Stations

Integrated Parking Facility Chargers

On Street Municipal Chargers

Depot Based Fleet Chargers

Retail Destination Chargers - By End User Segment (In Value%)

Private Electric Vehicle Owners

Commercial Fleet Operators

Public Transport Operators

Logistics and Delivery Companies

Municipal Infrastructure Authorities - By Procurement Channel (In Value%)

Government Infrastructure Programs

Utility Provider Installations

Private Charging Network Operators

Automotive Manufacturer Partnerships

Commercial Real Estate Developers

- Market Share Analysis

- Cross Comparison Parameters (Charging Power Output, Network Coverage, Charging Technology Type, Installation Model, Software Integration, Charging Speed Range, Connector Compatibility, Smart Charging Capability, Energy Source Integration, Payment System Integration, Network Interoperability, Maintenance & Service Support)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

BP Pulse

Shell Recharge Solutions

Tesla Supercharger Network

Pod Point

ChargePoint

Connected Kerb

Gridserve

Instavolt

Ionity

Swarco Smart Charging

Allego

Blink Charging

Siemens eMobility

ABB E Mobility

EO Charging

- Private EV Owners Increasing Home and Destination Charging Adoption

- Commercial Fleets Transitioning Toward Electrified Vehicle Operations

- Logistics Companies Deploying Dedicated Depot Charging Networks

- Municipal Authorities Expanding On Street Charging Infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now