Download PDF

Download PDFMarket Overview

The UK food acidulants market was valued at USD ~ million in 2024 and is projected to expand at a CAGR of ~% during the 2026–2035 forecast period. According to data published by the Food Standards Agency and the Food and Drink Federation, the United Kingdom operates one of the largest and most sophisticated food and beverage manufacturing sectors in Europe, with total industry output exceeding GBP 100 billion annually and a diverse base of manufacturers spanning beverages, bakery, dairy, processed meat, savoury snacks, confectionery, condiments, and ready meals that collectively represent the primary industrial demand base for food acidulant ingredients. Food acidulants, encompassing organic and inorganic acids used to regulate pH, impart tartness, enhance flavour, extend shelf life, prevent microbial growth, and perform a range of other functional roles in food and beverage formulations, are among the most widely used functional ingredient categories in the UK food manufacturing industry, with citric acid alone representing one of the highest-volume food additive ingredients consumed by the sector. Data from the Food and Drink Federation and industry associations indicates that the UK food acidulants market has continued to grow steadily in recent years, supported by expansion of the functional beverage and energy drink segment, growth of the plant-based food manufacturing sector, increasing demand for fermentation-derived and bio-based acidulants aligned with clean label and sustainability commitments, and the post-Brexit regulatory divergence creating both new compliance considerations and new formulation innovation opportunities for UK food manufacturers operating under the independent regulatory framework of the Food Standards Agency.

Market Segmentation

By Acidulant Type

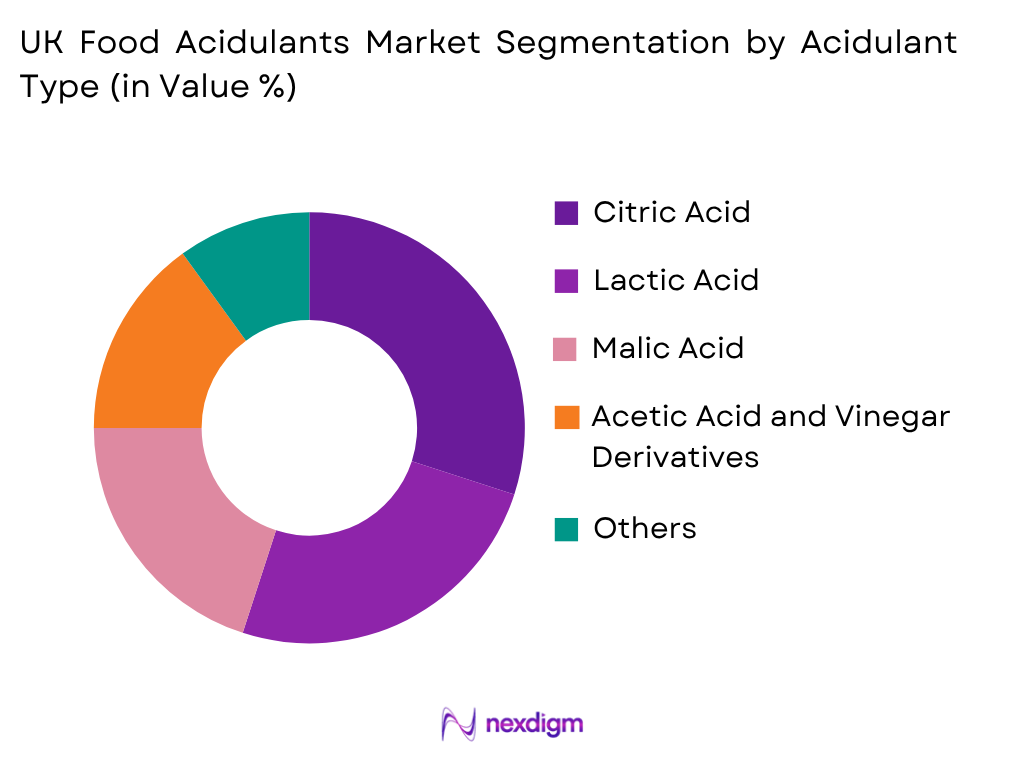

Citric acid dominates the UK food acidulants market by both volume and value, reflecting its exceptional functional versatility across the widest range of food and beverage application categories, its established safety and regulatory acceptance under FSA-retained food additive regulations, and its competitive commodity pricing that makes it the default acidulant choice for UK food manufacturers across beverages, bakery, confectionery, dairy, processed food, and condiment applications where a broadly effective pH-regulating and flavour-enhancing acid is required. Citric acid’s applications in the UK span carbonated soft drinks and dilutable cordials where it provides characteristic tartness and pH stabilisation, baked goods where it functions as a leavening acid in combination with sodium bicarbonate, dairy products including cream cheese and processed cheese where it assists pH adjustment and mineral chelation, preserves and jams where it activates pectin gel formation and inhibits microbial growth, and the flavouring of savoury snacks and confectionery. The UK is entirely dependent on imports for its citric acid supply, with the vast majority of UK consumption sourced from Chinese fermentation manufacturers, creating a structural supply chain vulnerability that has been highlighted by post-Brexit logistics disruptions and global shipping cost volatility. Lactic acid and its salts represent the second-largest acidulant category by value, widely used in bakery as a sourdough flavour contributor and dough conditioner, in dairy fermentation, in processed meat as a mild acidifier and antimicrobial agent, and increasingly in plant-based food formulations where its fermentation-derived, naturally positioned labelling resonates with clean label consumer preferences. Malic acid, tartaric acid, and fumaric acid serve more specialised applications in beverages, confectionery, and bakery respectively, while acetic acid and vinegar derivatives maintain strong positions in condiments, pickles, and savoury sauce applications that are deeply embedded in British food culture.

By Application

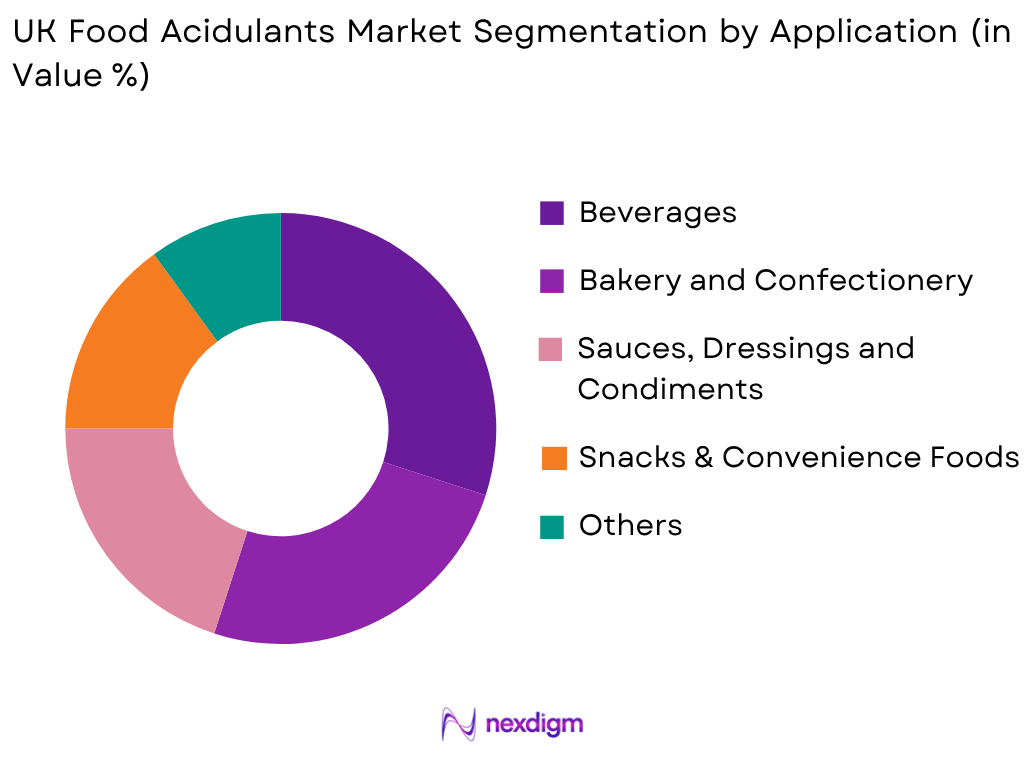

Beverages represent the largest application segment for food acidulants in the UK by value and volume, driven by the country’s large and diverse drinks manufacturing sector encompassing carbonated soft drinks, fruit juices, dilutable squashes and cordials, energy and sports drinks, functional waters, kombucha and fermented beverages, alcoholic ready-to-drink products, and craft beers and ciders, all of which rely on acidulants for pH regulation, flavour profile development, microbial stability, and product shelf life. The UK beverage market is one of the most innovative and dynamic in Europe, with the functional drink and energy drink segment consistently generating new product launches that require precisely calibrated acidulant systems to achieve target flavour profiles, pH specifications, and stability parameters. The carbonated soft drink category, led by Coca-Cola Great Britain, Britvic, and AG Barr, consumes substantial volumes of citric and phosphoric acid annually, while the rapidly growing energy drink market adds demand for citric and malic acid blends used to create the distinctive sharp-sweet flavour profiles preferred by younger consumers. Bakery and confectionery represents the second-largest application segment, reflecting the UK’s deeply embedded bakery culture encompassing industrial bread, morning goods, biscuits, cakes, pastries, and a wide range of traditional and premium confectionery products that collectively consume significant volumes of lactic acid, acetic acid, fumaric acid, and citric acid for dough conditioning, flavour development, preservation, and leavening. Sauces, dressings, and condiments constitute a third major application category in the UK, where acetic acid and vinegar remain fundamental ingredients in British culinary traditions including malt vinegar, brown sauce, Worcestershire sauce, salad cream, and pickled vegetables, alongside growing usage of citric and lactic acids in modern dressing and dip formulations.

Competitive Landscape

The UK food acidulants market is moderately concentrated at the supplier level, with a combination of large multinational ingredient and chemical distribution companies, specialty acidulant producers, and UK-based food ingredient distributors competing across different acid types and customer segments. Multinational ingredient and chemical distributors including Brenntag UK, Univar Solutions UK, IMCD UK, and Caldic UK serve as key intermediaries between global acidulant manufacturers and the UK’s diverse food manufacturing customer base, providing local inventory, technical support, and regulatory compliance documentation. Specialty acidulant producers including Jungbunzlauer and Corbion maintain direct sales presences serving larger UK food manufacturers with high-volume or technically demanding acidulant requirements. The post-Brexit regulatory divergence between UK FSA and EU EFSA food additive frameworks is creating a degree of market complexity as some suppliers navigate dual compliance requirements, while also creating opportunities for UK-specific formulation innovation under the independent FSA regulatory sandbox framework. Sterling exchange rate volatility and post-Brexit import cost dynamics have increased the strategic importance of supply chain resilience and local UK inventory holding as competitive differentiators.

| Company | Establishment Year | Headquarters | Primary Acidulant Portfolio | Key Application Industries

|

Manufacturing Presence | R&D Capability | Distribution Network | Clean Label Solutions |

| Jungbunzlauer UK | 1990 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Corbion UK | 2005 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Brenntag UK | 1874 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Univar Solutions UK | 1924 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| IMCD UK | 1998 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

UK Confectionary Market Analysis

Growth Drivers

Growth of Functional Beverages, Energy Drinks and the Craft Beverage Sector

The UK’s rapidly expanding functional beverage, energy drink, and craft brewing and cider sector represents one of the most significant and structurally durable growth drivers for food acidulant demand across the forecast period. The UK is one of Europe’s largest and most dynamic beverage markets, with the British Soft Drinks Association reporting that the soft drinks sector generates annual retail sales exceeding GBP 16 billion, while the craft beer and cider industry has grown from a small artisanal niche into a commercially substantial sector with thousands of independent producers contributing significantly to total UK brewing volumes. Energy and sports drinks represent the fastest-growing segment within the broader UK beverage market, with Mintel and the British Soft Drinks Association consistently reporting double-digit category growth as younger consumers adopt energy drinks as everyday beverages, fuelling sustained demand for the citric acid, malic acid, and ascorbic acid systems that provide the characteristic sharp-sweet flavour profiles and acidic pH environments fundamental to energy drink formulation. The functional beverage segment, encompassing kombucha, water kefir, adaptogenic drinks, nootropic beverages, electrolyte waters, and prebiotic sodas, has experienced particularly strong growth driven by the convergence of health and wellness trends with beverage innovation, with each of these product categories requiring specific organic acid profiles derived from fermentation processes or carefully blended acidulant systems to achieve target flavour, pH, and functional ingredient compatibility. The UK craft brewing sector, comprising more than 1,500 independent breweries according to the Society of Independent Brewers, generates fragmented but collectively significant demand for brewing-grade lactic acid, tartaric acid, and acidulant adjustment systems used to optimise brewing water chemistry, achieve target wort and beer pH profiles, and produce sour beer styles including Berliner Weisse, Gose, and Lambic-inspired ales that require substantial lactic or citric acid additions. The growing kombucha and fermented beverage category adds further acidulant demand through the organic acid profiles produced during fermentation as well as post-fermentation acidulant adjustment requirements, creating a diverse and innovation-driven acidulant demand base within the UK beverage sector.

Clean Label, Natural Acidulant Demand and Plant-Based Food Manufacturing Expansion

The UK food industry’s structural transition toward clean label formulations, natural ingredient declarations, and plant-based product development is creating a significant and growing demand driver for naturally derived and fermentation-based acidulant ingredients that can deliver the pH regulation, preservation, and flavour enhancement functions of conventional synthetic acidulants while satisfying the transparency and naturalness criteria demanded by UK consumers and major retail buyers. The UK has one of the most developed clean label consumer cultures in Europe, with research from the Food Standards Agency and commercial surveys by major market research firms consistently demonstrating that UK consumers attach high importance to recognising and understanding the ingredients listed on food labels, with synthetic-sounding chemical names including phosphoric acid, fumaric acid, and adipic acid generating significantly higher consumer concern than naturally labelled equivalents. This preference is translating into concrete procurement decisions by UK food manufacturers responding to retailer own-label guidelines at Tesco, Sainsbury’s, Marks and Spencer, and Waitrose, which increasingly impose restrictions on specific synthetic food additive categories and mandate the use of naturally derived or minimally processed ingredient alternatives wherever technically feasible. Naturally derived citric acid produced by fermentation of sugar substrates, lactic acid produced by microbial fermentation of glucose or sucrose, and malic acid derived from fermentation processes rather than petrochemical synthesis are gaining market share at the expense of petrochemically derived equivalents as UK food manufacturers reformulate to meet retailer clean label guidelines. The plant-based food manufacturing sector, which the Good Food Institute estimates has grown to represent a multi-billion pound segment of the UK food market, creates additional acidulant demand as manufacturers of plant-based meat analogues, dairy alternatives, vegan cheese, and egg replacements require acidulants for pH adjustment, coagulation, flavour development, and microbial stability in formulations that frequently involve novel protein matrices and ingredient combinations with different pH behaviour than conventional animal-derived food systems.

Market Challenges

Post-Brexit Supply Chain Disruption and Citric Acid Import Dependency on China

The UK food acidulants market faces a structurally significant challenge arising from the combination of post-Brexit supply chain disruption affecting European-sourced ingredients and the country’s near-total dependency on Chinese fermentation manufacturers for its largest-volume acidulant category, citric acid, creating a supply chain vulnerability that has been repeatedly exposed by global shipping disruptions, geopolitical trade tensions, and UK-EU border friction since the end of the Brexit transition period. The UK imports the substantial majority of its citric acid requirements from Chinese producers concentrated in Shandong, Jiangsu, and Anhui provinces, with HMRC trade data indicating that China accounts for well over half of UK citric acid imports by volume, a concentration that exposes UK food manufacturers to significant supply and pricing risk arising from Chinese production capacity decisions, energy cost fluctuations affecting Chinese fermentation economics, freight rate volatility on Asia-Europe shipping lanes, and any deterioration in UK-China trade relations. Post-Brexit border management requirements have added administrative complexity and cost to the importation of food ingredients from the European Union, which previously supplied the UK with a significant portion of its specialty acidulant requirements including lactic acid from Dutch and German fermentation producers, malic acid from French and German producers, and tartaric acid from Southern European wine industry sources. The introduction of post-Brexit customs declarations, rules of origin compliance requirements under the UK-EU Trade and Cooperation Agreement, and additional phytosanitary and safety certification requirements for certain ingredient categories have increased the administrative burden, lead times, and landed costs for EU-sourced acidulants, partially eroding the geographic and logistics advantages that proximity to European suppliers historically provided to UK food manufacturers. These supply chain vulnerabilities require UK food manufacturers and ingredient distributors to maintain higher safety stock levels, diversify sourcing across multiple geographic origins, and invest in supply chain risk management capabilities that were not necessary under the pre-Brexit single market framework.

Post-Brexit Regulatory Divergence and Compliance Complexity

The United Kingdom’s departure from the European Union and the consequent divergence of the UK’s food additive regulatory framework from the EU’s Regulation (EC) No 1333/2008 on Food Additives represents a structurally novel challenge for acidulant ingredient suppliers, food manufacturers, and regulatory compliance professionals operating in the UK market. Following Brexit, the UK retained the EU’s existing food additive regulations as domestic law through the European Union (Withdrawal) Act 2018, creating the UK Retained Food Additives Regulation that is functionally identical to the EU framework as it existed at the point of exit. However, the Food Standards Agency now operates as the independent UK food additive regulatory authority, responsible for evaluating new ingredient applications, updating maximum usage levels, and reviewing the safety of existing permitted additives independently of the European Food Safety Authority processes that govern equivalent decisions in the EU. This regulatory independence creates both challenge and opportunity for the UK acidulant market. The challenge arises from the risk of progressive divergence between UK and EU permitted acidulant categories and maximum usage levels, which complicates compliance management for food manufacturers selling products in both markets and increases the administrative burden for ingredient suppliers that must maintain dual compliance documentation sets for UK and EU regulatory requirements. Manufacturers exporting food products from the UK to EU markets must ensure that acidulant usage levels comply with EU regulations even if higher levels are permitted under UK FSA standards, while manufacturers importing finished food products from the EU must verify compliance with any UK-specific derogations or tighter standards that the FSA may adopt. The opportunity component of regulatory divergence lies in the FSA’s capacity as an independent regulatory authority to pursue a more streamlined and innovation-friendly approach to novel ingredient approvals and maximum usage level revisions than the slower-moving multi-member-state EFSA process, potentially enabling UK food manufacturers earlier access to new acidulant ingredients and application approvals that remain under review at the EU level.

Market Opportunities

Bio-Based and Fermentation-Derived Acidulant Innovation and Sustainability Positioning

The UK food industry’s accelerating commitment to sustainability, net zero carbon targets, and responsible ingredient sourcing is creating a significant and commercially compelling growth opportunity for bio-based and fermentation-derived acidulant producers that can offer ingredients with demonstrably lower carbon footprints, renewable feedstock origins, and credible sustainability credentials compared to petrochemically synthesised or energy-intensive conventional fermentation alternatives. Major UK food and beverage manufacturers have made extensive public commitments to science-based emissions reduction targets, sustainable ingredient procurement, and supply chain decarbonisation, with companies including Unilever UK, Nestlé UK, PepsiCo UK, Diageo, Tesco Food Manufacturing, and Marks and Spencer Food publishing detailed net zero roadmaps that include ingredient sustainability as a key workstream. The production of citric acid, lactic acid, and malic acid through aerobic or anaerobic fermentation of renewable carbohydrate feedstocks including glucose, sucrose, corn starch, and increasingly agricultural side streams such as food waste-derived sugars, offers the potential for substantially lower lifecycle carbon emissions than petrochemical synthesis routes, providing a sustainability differentiation narrative that resonates with UK corporate procurement priorities. Bio-based succinic acid, produced through fermentation of glucose using engineered microbial strains, has achieved commercial production scale at several European and North American facilities and is gaining interest as a bio-based acidulant and food additive with applications in bakery, beverages, and flavouring that could displace petrochemical-derived adipic acid and fumaric acid in certain UK food manufacturing applications. The UK government’s Industrial Strategy and Bioeconomy Strategy, including support for industrial biotechnology through Innovate UK and the Biotechnology and Biological Sciences Research Council, provides a policy and funding environment that supports the development and commercialisation of bio-based fermentation acid production in the UK, potentially enabling the development of domestic acidulant fermentation capacity that would reduce import dependency and provide UK food manufacturers with a low-carbon, locally produced acidulant supply alternative.

Kombucha, Fermented Beverages and the Functional Drink Sector Expansion

The rapid growth of kombucha, water kefir, jun tea, fermented botanical drinks, and the broader functional and better-for-you beverage sector in the UK creates a distinctive and fast-expanding growth opportunity for acidulant ingredient suppliers capable of serving both the fermentation-derived organic acid requirements of these products during production and the acidulant adjustment and standardisation requirements during post-fermentation processing and quality control. The UK kombucha market has grown from a niche health food store product into a mainstream retail category available in major supermarkets, convenience chains, and food service outlets, with the British Kombucha Association and commercial market research firms reporting sustained double-digit annual growth rates as consumer awareness of fermented food and beverage health benefits expands. Kombucha and water kefir products are characterised by naturally produced organic acid profiles, primarily acetic acid and gluconic acid in kombucha and lactic acid in water kefir, that contribute to the characteristic tart, slightly vinegary flavour profiles and mildly acidic pH levels that define these products. Commercial producers require acidulants for pH standardisation to ensure consistent product acidity across batches, for supplemental acidification to achieve target flavour profiles in shorter fermentation cycles, and for post-fermentation acidulant additions in flavoured and functional variant formulations. The broader functional beverage sector, encompassing adaptogenic drinks, nootropic beverages, prebiotic sodas, electrolyte waters, vitamin-enriched sparkling drinks, and mushroom-extract beverages, generates diverse and application-specific acidulant demand for citric, malic, ascorbic, and lactic acids used to achieve target pH, flavour balance, vitamin stabilisation, and ingredient compatibility across a wide range of novel formulations. Acidulant suppliers that develop application expertise in fermented beverage formulation, build relationships with the UK’s growing community of independent kombucha and functional drink producers, and offer technical guidance on organic acid management throughout the fermentation and post-processing workflow are well positioned to capture the growing acidulant demand from this dynamic and innovation-intensive segment.

Future Outlook

The UK food acidulants market is expected to witness sustained growth throughout the forecast period, supported by expansion of the functional beverage, craft brewing, and fermented drink sectors, clean label and natural acidulant reformulation demand from UK food manufacturers responding to retailer ingredient standards, growth of the plant-based food manufacturing sector, and increasing adoption of bio-based and sustainably produced fermentation-derived acidulants aligned with corporate net zero commitments. Ingredient suppliers are increasingly investing in post-Brexit regulatory compliance capabilities, UK-specific technical application support, domestic inventory resilience to mitigate supply chain disruption risk, and sustainability credentials including carbon footprint certification and renewable feedstock sourcing documentation. The Food Standards Agency’s capacity as an independent UK regulatory authority to innovate in food additive approvals creates a medium-term opportunity for UK-specific acidulant formulation leadership. Continued investments in bio-based acidulant development, fermentation technology, clean label ingredient portfolios, and digital B2B ingredient procurement platforms will further strengthen the long-term competitiveness of the UK food acidulants market through 2035.

Major Players

- Jungbunzlauer UK (Citric, Lactic, Gluconic Acids)

- Cargill UK (Citric Acid and Acidulant Solutions)

- ADM (Archer Daniels Midland) UK (Citric and Lactic Acid)

- Brenntag UK (Food Ingredients and Acidulants Division)

- Corbion UK (Lactic Acid and Bio-Based Organic Acids)

- Tate and Lyle UK (Food Ingredients and Acidulants)

- Bartek Ingredients UK Distribution

- Thiercelin UK (Tartaric Acid)

- Weifang Ensign Industry (UK Distribution)

- ISALTIS UK (Glucono Delta-Lactone and Specialty Acids)

- Fuerst Day Lawson (FDL) UK

- Univar Solutions UK (Food Ingredients Division)

- IMCD UK (Food Ingredients Division)

- Caldic UK (Food Ingredients Division)

- Hawkins Watts UK

Key Target Audience

- Food and Beverage Manufacturers (Beverages, Bakery, Dairy, Processed Meat, Confectionery, Condiments and Functional Foods)

- Food Ingredient and Chemical Distributors and Brokers

- Craft Brewers, Cider Makers and Fermented Beverage Producers

- Nutraceutical and Dietary Supplement Manufacturers

- Food Technologists and Regulatory Affairs Teams

- Retail Private Label Development Teams at Major UK Retailers

- Investments and Private Equity Firms

- Government and Regulatory Bodies (Food Standards Agency (FSA), Food Standards Scotland (FSS), Department for Environment, Food and Rural Affairs (DEFRA), UK Health Security Agency)

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying the major stakeholders across the UK food acidulants value chain, including global acidulant manufacturers, UK and European ingredient distributors, food and beverage manufacturers across all relevant application segments, craft beverage producers, regulatory authorities including the Food Standards Agency, retail private label development teams, and industry associations including the Food and Drink Federation and the British Soft Drinks Association. Extensive secondary research is conducted using FSA regulatory publications, Food and Drink Federation industry data, HMRC trade statistics, ONS food manufacturing output data, and proprietary ingredient market databases to establish the key variables influencing market performance.

Step 2: Market Analysis and Construction

Historical market information is compiled and evaluated to estimate the overall market size, ingredient volume consumption by acidulant type and application, import volumes by source country, average selling prices in Sterling terms, distributor margins, and revenue generation across major acidulant categories and food manufacturing end-use segments. Both demand-side and supply-side indicators are analyzed using bottom-up and top-down market sizing approaches to ensure comprehensive market coverage across all acidulant types, application categories, and regional food manufacturing clusters within the United Kingdom.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market estimates and analytical assumptions are validated through Computer Assisted Telephone Interviews (CATIs) and structured discussions with food technologists and product development managers at UK food and beverage manufacturers, acidulant sales and technical managers at multinational and specialty suppliers, food ingredient distributor executives, craft beverage sector representatives, FSA regulatory affairs consultants, and academic food chemistry researchers at UK universities. These interviews provide critical on-ground formulation and commercial insights that strengthen the reliability of market estimates across both large manufacturer and SME customer segments.

Step 4: Research Synthesis and Final Output

The final stage integrates primary research findings with secondary information to develop a comprehensive assessment of market size, segmentation, competitive landscape, customer procurement behaviour, and future opportunities. Multiple validation techniques, including data triangulation across HMRC import trade data, ONS food manufacturing production statistics, Food Standards Agency additive usage data, and ingredient supplier commercial disclosures, are employed to ensure the consistency, accuracy, and credibility of the final market report.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Taxonomy, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Primary Industry Interviews, Secondary Research Validation, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Industry Value Chain Analysis

- Supply Chain Analysis

- Growth Drivers (Large and Sophisticated Food and Beverage Manufacturing Industry, Rising Clean Label and Natural Acidulant Demand, Growing Functional Beverage and Energy Drink Sector, Expansion of Plant-Based and Vegan Food Manufacturing)

- Market Challenges (Post-Brexit Supply Chain Disruption and Increased Import Costs for EU-Sourced Acidulants, High Import Dependency for Citric Acid from China, Currency Volatility Affecting Sterling-Denominated Procurement Costs, Price Volatility of Fermentation Feedstock Raw Materials)

- Market Opportunities (Natural and Clean Label Acidulant Innovation, Bio-Based and Fermentation-Derived Acidulant Development, Functional Beverage and Sports Nutrition Sector Growth, Kombucha and Fermented Beverage Market Growth, Sustainable and Domestically Sourced Acidulant Supply Chain Development)

- Market Trends (Clean Label and Natural Acidulant Substitution, Fermentation-Derived Organic Acid Growth, Reduced Sugar and Acidulant Balance Reformulation, Digital B2B Ingredient Procurement and Supply Chain Traceability Platforms)

- Government Regulations (UK Food Safety Act 1990, UK Retained Regulation (EC) No 1333/2008 on Food Additives as Amended Post-Brexit, Food Standards Agency (FSA) Approvals and Maximum Usage Levels, Organic Certification Standards Under UK Organic Regulations, UK Nutrient Profiling Model Relevance to Acidulant-Containing Product Categories)

- Raw Material and Supply Chain Analysis (Citric Acid Import Dependency from China and EU, Lactic Acid Fermentation Feedstock Supply, Malic Acid Import Sources from China and Europe, Post-Brexit Customs Tariff Impact on Acidulant Import Costs, UK Domestic Fermentation Capacity for Bio-Based Organic Acids)

- Food and Beverage Industry Demand Analysis (Carbonated Soft Drink and Juice Industry Citric Acid Consumption, Bakery Industry Demand for Lactic and Acetic Acids, Dairy Industry Acidulant Usage, Processed Meat Industry Demand, Savoury Snack and Crisp Industry Flavour Acidulant Consumption, Craft Beverage Sector Demand, Retail Private Label Manufacturer Requirements)

- SWOT Analysis

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Stakeholder Ecosystem

- Competition Ecosystem

- By Market Value (2020-2025)

- By Volume Consumption (2020-2025)

- By Average Selling Price (2020-2025)

- By Acidulant Type (In Value %)

Citric Acid

Acetic Acid and Vinegar Derivatives

Lactic Acid

Malic Acid

Tartaric Acid

Phosphoric Acid

Fumaric Acid

Ascorbic Acid (Vitamin C as Acidulant)

Glucono Delta-Lactone (GDL)

Adipic Acid

Succinic Acid

Propionic Acid - By Application (In Value %)

Beverages

Bakery and Confectionery

Dairy and Dairy Analogue Products

Processed Meat and Seafood

Sauces, Dressings and Condiments

Snack Foods and Savoury Products

Jams, Preserves and Fruit Preparations

Frozen and Ready-to-Eat Meals

Infant and Clinical Nutrition Products

Dietary Supplements and Functional Foods - By Function (In Value %)

pH Regulation and Acidification

Flavour Enhancement and Tartness

Preservation and Antimicrobial Activity

Chelation and Metal Ion Sequestration

Leavening and Dough Conditioning

Emulsification and Texture Modification

Colour Stabilisation and Antioxidant Activity - By Distribution Channel (In Value %)

Direct Sales to Food and Beverage Manufacturers (B2B)

Ingredient Distributors and Chemical Distributors

Specialty Food Ingredient Importers and Brokers

E-Commerce and Digital B2B Ingredient Platforms - By Region (In Value %)

Greater London and South East England

Midlands

North of England

Scotland

Wales

Northern Ireland

South West England

- Market Share Analysis (By Value, Volume, Acidulant Type, Application Segment, Distribution Channel)

- Cross Comparison Parameters (Acidulant Portfolio Breadth, Natural and Bio-Based Product Range, Application Technical Support Capability, FSA Regulatory Compliance Documentation, UK Distribution Network Coverage, Annual New Ingredient Launches, Post-Brexit Supply Chain Resilience, Sterling-Denominated Pricing Stability, Sustainability and ESG Credentials)

- SWOT Analysis of Major Players

- Pricing Analysis (By Acidulant Type, Purity Grade, Source, Application, Pack Size, Contract Volume)

- Detailed Profiles of Major Companies

Jungbunzlauer UK

Cargill UK

ADM UK

Brenntag UK

Corbion UK

Tate and Lyle UK

Bartek Ingredients UK Distribution

Thiercelin UK

Weifang Ensign Industry

ISALTIS UK

Fuerst Day Lawson (FDL) UK

Univar Solutions UK

IMCD UK

Caldic UK

Hawkins Watts UK

- Procurement Pattern Analysis (Ingredient Sourcing Frequency, Acidulant Type and Grade Preference, Application-Specific Usage Behaviour, Seasonal Procurement Cycles, Annual Ingredient Budget Allocation)

- Demographic and Industry Buyer Analysis (Large Food and Beverage Manufacturers, SME Food Processors, Craft Brewers and Cider Makers, Foodservice Operators, Nutraceutical Producers, Retail Private Label Manufacturers)

- Formulation Cost and Functionality Trade-Off Analysis

- Natural and Clean Label vs Synthetic Acidulant Preference Analysis

- Supplier and Brand Loyalty Analysis

- Regulatory and FSA Compliance-Driven Ingredient Selection Behaviour

- Ingredient Attribute Preference Analysis (Purity Grade, Functional Performance, Clean Label Status, Certifications, Price Stability in Sterling, Availability, Technical Support, Post-Brexit Supply Chain Reliability)

- Large Manufacturer vs Craft and Artisan Producer Procurement Behaviour Differences

- Digital vs Traditional B2B Ingredient Procurement Behaviour

- Customer Pain Point Analysis

- Procurement Decision-Making Process

- By Market Value (2026-2035)

- By Volume Consumption (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now