Download PDF

Download PDFMarket Overview

The UK Food Traceability Market was valued at USD ~ Million in 2024 and is anticipated to expand at a CAGR of ~% during 2026–2035. The market is primarily driven by post-Brexit export certification requirements, continued Food Standards Agency (FSA) investment in blockchain and digital traceability trials, and rising consumer demand for supply chain transparency. The United Kingdom holds an estimated 26.8% share of the global blockchain food traceability market in 2025, the second-largest national share globally, according to Future Market Insights, reflecting the country’s comprehensive food safety programs and supply chain transparency development initiatives. The global blockchain food traceability market itself is projected to grow from USD 3,037.4 million in 2025 to USD 52,210.6 million by 2035, at a CAGR of 32.9%. The FSA has piloted blockchain trials covering the collection and communication of meat inspection results and export health certification for pork exports to China and the United States, a process that currently requires between 35 and 50 certificates per week completed by Official Veterinarians working on the FSA’s behalf. Since Brexit, the UK has retained the EU’s General Food Law Regulation (EC) No. 178/2002 in domestic law, maintaining traceability obligations across bakery, dairy, beverages, meat, seafood, and processed food applications while developing independent certification pathways for trade with the EU and other international markets.

Market Segmentation

By Technology Type

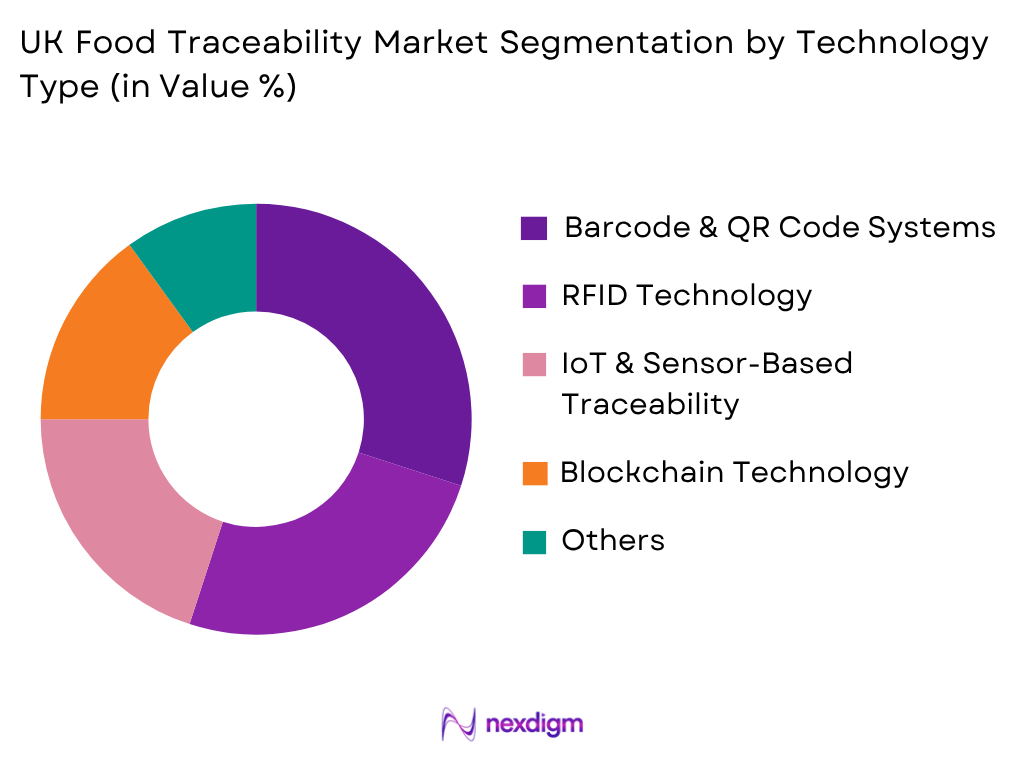

The UK Food Traceability Market is segmented by technology type into barcode & QR code systems, RFID technology, IoT & sensor-based traceability, blockchain technology, GPS & location tracking systems, and other traceability technologies. Barcode & QR code systems hold the dominant market share due to their extensive integration across food packaging, supermarket checkout systems, warehousing, and product identification processes. Barcode-based traceability remains a common and cost-effective method for item- and case-level tracking, while the UK retail sector is increasingly preparing for GS1-compatible 2D and QR codes capable of carrying richer product information. Close to half of UK retailers had upgraded checkout technology to accommodate multifunctional QR-style codes, reinforcing the technology’s position across the country’s highly developed grocery retail ecosystem. RFID technology is increasingly relevant for inventory visibility and non-line-of-sight tracking, while IoT sensors support cold-chain temperature and environmental monitoring. Blockchain remains an emerging technology for provenance and multi-party supply-chain transparency, particularly where immutable traceability records are required.

By Application

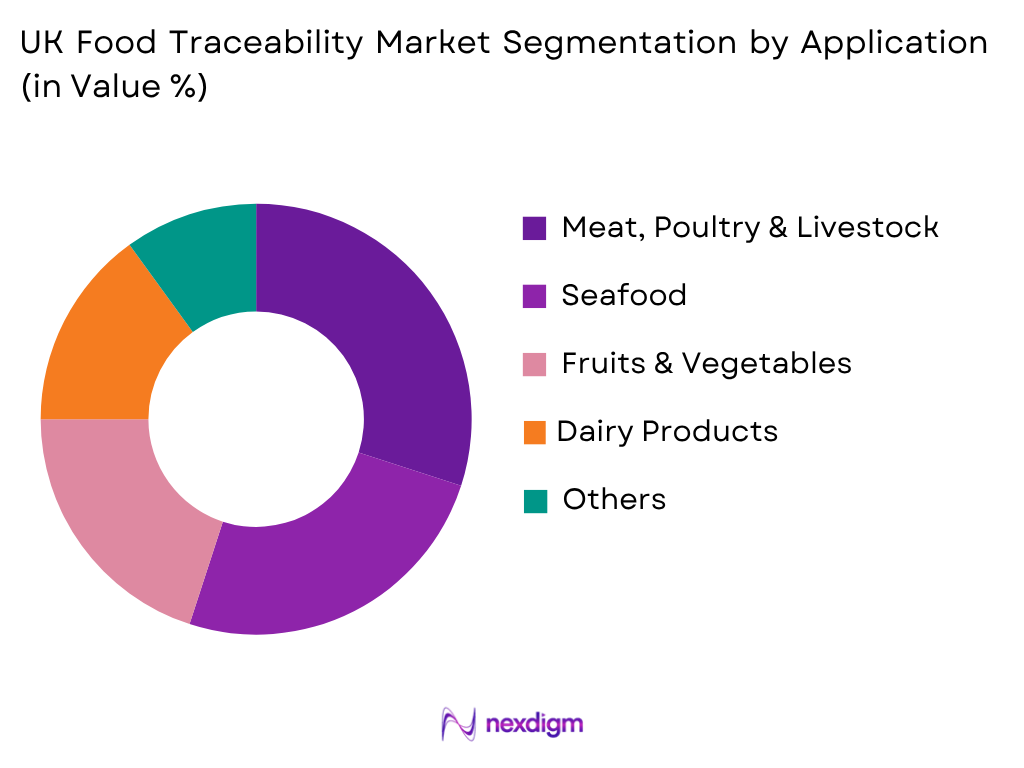

The Meat, Poultry & Livestock segment holds a significant share of the UK Food Traceability Market, reflecting the country’s substantial livestock and meat export industry and the FSA’s ongoing blockchain trials for export health certification. The FSA’s meat inspection blockchain trial addresses a longstanding challenge in which an individual animal may have had several owners prior to slaughter, making it difficult to share inspection results with all historic owners using fragmented, non-digital data systems. The Fruits & Vegetables segment also represents a significant application area, supported by major UK retailers’ adoption of blockchain to track fresh produce origins and enhance consumer trust. The Seafood segment continues to see growing traceability investment given the FSA’s engagement with international bodies including the Global Food Safety Initiative and the U.S. Food and Drug Administration on cross-border traceability standards relevant to UK seafood exports.

Competitive Landscape

The UK Food Traceability Market is moderately fragmented, with a pioneering domestic blockchain traceability company operating alongside established multinational enterprise technology providers and specialized traceability solution vendors. Competition is primarily based on platform interoperability, blockchain integration capability, regulatory compliance support for both retained EU food law and post-Brexit export certification requirements, ease of supplier onboarding, and the ability to serve large-scale UK retail and export compliance programs. Provenance, founded in 2013 and headquartered in London’s King’s Cross, was among the earliest companies globally to apply blockchain technology to supply chain traceability, piloting projects tracking tuna through Southeast Asian supply chains and partnering with major consumer cooperatives to track fresh produce from origin to supermarket shelf. The company has since evolved to focus on verifiable sustainability claims for consumer packaged goods brands, while continuing to compete alongside global players such as IBM Food Trust, SAP, Zebra Technologies, and Trustwell’s FoodLogiQ platform, the latter of which has published specific guidance addressing digital traceability gaps for UK manufacturers and BRCGS audit readiness.

| Company | Establishment Year | Headquarters | Primary Product Portfolio | Traceability Solution Portfolio

|

Deployment Presence | Major End-Use Industries | Key Strategic Focus | Certifications & Compliance |

| Provenance | 2013 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| IBM | 1911 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Zebra Technologies | 1969 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Trustwell (FoodLogiQ) | 2010 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| SAP | 1972 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

UK Food Traceability Market Analysis

Growth Drivers

Post-Brexit Export Certification Requirements

The UK Food Traceability Market is experiencing sustained growth due to new export certification requirements that emerged following Brexit, as the UK established independent trade relationships requiring dedicated certification processes for agri-food exports to the EU and other international markets. The FSA has highlighted that certification for pork exports to China and the United States alone requires between 35 and 50 certificates per week, a resource-intensive process currently reliant on Official Veterinarians. Trade with third countries has also subjected the UK to complex rules-of-origin requirements, creating strong demand for traceability systems that provide complete, accurate, auditable, and shareable information to reduce the administrative burden on exporters and support the credibility of the British food brand internationally. This has directly motivated the FSA’s investment in blockchain trials to test whether distributed ledger technology can streamline export certification while maintaining rigorous food safety standards.

FSA Blockchain and Digital Traceability Trials

Continued government investment in digital traceability infrastructure remains a significant driver of the UK Food Traceability Market. The FSA has commissioned trials evaluating blockchain opportunities in two key areas: the collection and communication of meat inspection results, addressing longstanding data fragmentation challenges arising from animals having multiple owners prior to slaughter, and export certification processes for trade with third countries. These trials build on the DEFRA Farm to Fork initiative and incorporate actual condition data from animals and slaughterhouses, working in partnership with the Internet of Food Things initiative led by Lincoln University to connect digital traceability data with physical foodstuffs. The FSA has also engaged internationally with the Global Food Safety Initiative and the U.S. Food and Drug Administration, alongside the UK All-Party Parliamentary Group on Blockchain, to identify further opportunities building on these trial results, reflecting sustained institutional commitment to advancing traceability technology adoption across the UK food industry.

Market Challenges

Post-Brexit Regulatory Divergence from the EU

The UK Food Traceability Market faces ongoing challenges stemming from regulatory divergence between UK and EU food safety frameworks following Brexit. While the UK has retained the EU’s General Food Law Regulation (EC) No. 178/2002 in domestic law, the EU continues to develop its own initiatives, including the Digital Product Passport and Farm-to-Fork Strategy, which may create future compliance complexity for UK food exporters seeking to maintain EU market access. Standardization gaps between UK, EU, and other international regulatory frameworks continue to hinder uniform traceability adoption, requiring UK food companies and technology providers to navigate potentially divergent data standards, certification requirements, and labeling rules depending on export destination, adding complexity and cost to cross-border trade.

Fragmented Supply Chain Adoption Among Small Producers

The UK Food Traceability Market continues to face challenges related to uneven technology adoption across a fragmented supply chain involving numerous small and medium-sized producers, processors, and distributors. Blockchain used in isolation cannot serve as a complete solution to food traceability challenges in a fragmented supply chain, and the FSA has noted that its own trials, while demonstrating clear opportunities, require complementary work on data standards and data quality improvement to achieve full success. Coordinating traceability across multiple stakeholders with varying levels of digital maturity remains a significant operational challenge, particularly for harder-to-trace categories such as processed foods involving multiple ingredient sources and complex supply chains.

Market Opportunities

Digital Product Passport Alignment

The EU’s development of Digital Product Passport initiatives, likely to standardize digital traceability requirements across food supply chains in the coming years, presents significant opportunities for UK food traceability technology providers to develop interoperable solutions that support continued EU market access for UK exporters. Given the FSA’s existing blockchain trial infrastructure and international engagement with bodies such as the Global Food Safety Initiative, UK companies are well positioned to align emerging domestic traceability standards with evolving EU requirements, reducing compliance friction for UK food and beverage exporters while strengthening the credibility of British food brands in international markets.

AI-Enhanced Traceability and Predictive Analytics

The integration of artificial intelligence with existing blockchain and IoT-based traceability platforms presents substantial growth opportunities for the UK Food Traceability Market. UK-based companies such as Pragmatic Semiconductor are developing ultra-low-cost flexible integrated circuits that can be embedded directly into food packaging, enabling mass-market farm-to-fork traceability at a fraction of the cost of traditional silicon-based tracking hardware. Combined with continued advances in AI-driven predictive analytics for contamination detection and spoilage forecasting, these technologies create opportunities for UK traceability providers to move beyond basic compliance recordkeeping toward higher-value predictive food safety and supply chain optimization services, building on the country’s strong deep-tech and semiconductor innovation base.

Future Outlook

The UK Food Traceability Market is expected to witness sustained expansion over the forecast period, supported by continued post-Brexit export certification investment, ongoing FSA engagement with blockchain and digital traceability technologies, and growing consumer demand for supply chain transparency. Continued alignment with emerging EU Digital Product Passport standards and further development of the FSA’s blockchain trials are expected to shape the market’s regulatory trajectory. The market is also likely to benefit from continued technology convergence, including AI-enhanced predictive analytics and innovative low-cost tracking hardware from UK deep-tech companies, supporting long-term growth across meat, seafood, produce, dairy, and processed food supply chain applications.

Major Players

- Provenance

- IBM (Food Trust)

- SAP

- Zebra Technologies

- Trustwell (FoodLogiQ)

- Oracle

- Honeywell International

- SGS SA

- Antares Vision

- Pragmatic Semiconductor

- TE-FOOD International

- Wholechain

- Sourcemap

- Optel Group

- Sensitech (Carrier)

Key Target Audience

- Food Traceability Software and Platform Providers

- Food & Beverage Manufacturers

- Food Retailers and Grocery Chains

- Foodservice Operators and Distributors

- Cold Chain Logistics and Hardware Providers

- Meat, Seafood, and Produce Export Companies

- Investment and Venture Capitalist Firms

- Government and Regulatory Bodies (Food Standards Agency (FSA), Department for Environment, Food and Rural Affairs (DEFRA), Food Standards Scotland)

- Technology Integrators and Compliance Consulting Firms

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying the complete ecosystem of the UK Food Traceability Market, including software and platform providers, hardware manufacturers, system integrators, food and beverage processors, retailers, and regulatory authorities. Extensive secondary research is conducted using company annual reports, government publications, trade associations, customs statistics, industry journals, and proprietary databases to determine the variables influencing market demand, pricing, deployment, adoption, and technological developments.

Step 2: Market Analysis and Construction

Historical market information is collected and analyzed to estimate market size, deployment volumes, technology adoption trends, application-wise demand, and pricing trends. A combination of top-down and bottom-up approaches is used to estimate market revenues and validate segment-level performance. Adoption patterns across meat, seafood, produce, dairy, and processed foods are evaluated to establish an accurate representation of the industry.

Step 3: Hypothesis Validation and Expert Consultation

The preliminary findings are validated through Computer-Assisted Telephone Interviews (CATIs) and structured discussions with traceability software providers, procurement managers, distributors, food technologists, regulatory experts, and senior executives operating within the UK food industry. These interviews help verify market assumptions, competitive developments, technology adoption trends, pricing dynamics, and future investment opportunities while refining the overall market estimates.

Step 4: Research Synthesis and Final Output

The final stage integrates insights obtained from primary interviews with quantitative information collected through secondary sources. Data triangulation techniques are applied to reconcile differences between supply-side and demand-side estimates, ensuring robust market forecasting. The report is then reviewed through multiple quality assurance checkpoints to deliver a comprehensive analysis covering market size, segmentation, competitive landscape, future outlook, and strategic recommendations for industry stakeholders.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Primary Industry Interviews, Secondary Research Validation, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Food Traceability Industry Value Chain Analysis

- Supply Chain Analysis

- Growth Drivers (Post-Brexit Export Certification Requirements, FSA Blockchain and Digital Traceability Trials, Rising Consumer Demand for Supply Chain Transparency, Retailer-Driven Compliance Programs, Growth in Blockchain and IoT Adoption, Expansion of Cold Chain Monitoring)

- Market Challenges (Post-Brexit Regulatory Divergence from the EU, Fragmented Supply Chain Adoption Among Small Producers, High Implementation Costs, Data Interoperability Complexity, Standardization Gaps Across Multiple Jurisdictions)

- Market Opportunities (Digital Product Passport Alignment, AI-Enhanced Traceability and Predictive Analytics, Expansion into Livestock and Seafood Export Certification, Smart Labeling and Packaging, Export-Oriented Compliance Solutions)

- Market Trends (Blockchain and AI Convergence, QR Code Consumer Transparency Adoption, Cold Chain IoT Monitoring, Growth of ESG and Sustainability Verification, Multi-Tier Supply Chain Interoperability)

- Government Regulations (Retained EU General Food Law Regulation (EC) 178/2002, Food Standards Agency Traceability Requirements, Food Information Regulations, Export Health Certification Requirements, Labeling Requirements)

- Import and Export Analysis (Trade Volume, Major Import Sources, Export Destinations, HS Code Analysis, Trade Balance)

- Technology Landscape (Blockchain Platforms, RFID and Barcode Systems, IoT Cold Chain Sensors, AI and Predictive Analytics, Cloud-Based Traceability Platforms)

- Sustainability Assessment (Food Waste Reduction, Recall Efficiency, Supply Chain Transparency, Ethical Sourcing Verification, Carbon Footprint Tracking)

- PESTLE Analysis

- SWOT Analysis

- Porter’s Five Forces Analysis

- Stakeholder Ecosystem

- Competition Ecosystem

- By Market Value (2020-2025)

- By Volume of Deployments (2020-2025)

- By Average Selling Price (2020-2025)

- By Technology Type (In Value %)

Blockchain

RFID

Barcode & QR Code

GPS/GIS

IoT Sensors & Others - By Deployment Mode (In Value %)

Cloud-Based

On-Premise

Hybrid - By Application (In Value %)

Meat, Poultry & Livestock

Seafood

Fruits & Vegetables

Dairy Products

Bakery & Confectionery

Beverages

Processed Foods - By End User (In Value %)

Food Manufacturers

Food Retailers & Grocery Chains

Foodservice Operators

Distributors & Logistics Providers

Government & Regulatory Agencies - By Region (In Value %)

England

Scotland

Wales

Northern Ireland

- Market Share of Major Players (By Value, Component, Technology, Application Industry, Deployment Mode)

- Cross Comparison Parameters (Platform Portfolio Breadth, Blockchain Integration Capability, Application Technical Support Capability, Deployment Capacity, Regulatory Compliance & Certifications, Food & Beverage Customer Base, Innovation & New Product Launch Frequency)

- SWOT Analysis of Major Players

- Pricing Analysis by Solution Category and Tier

- Deployment Capacity Analysis

- Manufacturing and Platform Footprint Analysis

- Distribution Network Analysis

- Innovation Benchmarking

- Detailed Profiles of Major Companies

Provenance

IBM (Food Trust)

SAP

Zebra Technologies

Trustwell (FoodLogiQ)

Oracle

Honeywell International

SGS SA

Antares Vision

Pragmatic Semiconductor

TE-FOOD International

Wholechain

Sourcemap

Optel Group

Sensitech (Carrier)

- Consumption Pattern Analysis (Deployment Scale, Integration Complexity, Product Category Penetration, Seasonal Demand, Reformulation Activity)

- Purchasing Criteria (Regulatory Compliance, Cost Efficiency, Interoperability, Scalability, Data Security, Supplier Onboarding Ease)

- Procurement and Supplier Selection Analysis

- Clean Label and Transparency Adoption Assessment

- Premium vs Conventional Solution Demand

- Product Attribute Preference Analysis (Data Accuracy, Real-Time Visibility, Ease of Integration, Scalability, Regulatory Alignment, User Friendliness)

- Consumer Health & Wellness Influence on Product Development

- Pain Point Analysis

- Decision-Making Process

- By Market Value (2026-2035)

- By Volume of Deployments (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now