Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The UK Green Hydrogen market is poised for substantial growth, with the market size driven by significant investments from the government and private sector in clean energy technologies. Recent historical assessments indicate that the market size in 2024 is valued at USD ~ billion, largely fueled by the increasing demand for sustainable fuel alternatives, which are being accelerated by climate policies and decarbonization targets set by the UK government. The drive towards zero-emission industries, as well as advancements in hydrogen production technologies, are major contributors to this market expansion.

The UK, along with other European countries, has emerged as a leader in the green hydrogen sector. The country is focusing on integrating hydrogen into its energy mix as part of its broader strategy to meet carbon neutrality goals. The dominance of the UK can be attributed to its well-established renewable energy infrastructure, high level of government support, and strategic initiatives such as the Hydrogen Strategy. Moreover, key cities like London, Birmingham, and Glasgow are at the forefront due to their commitment to sustainability and innovation.

Market Segmentation

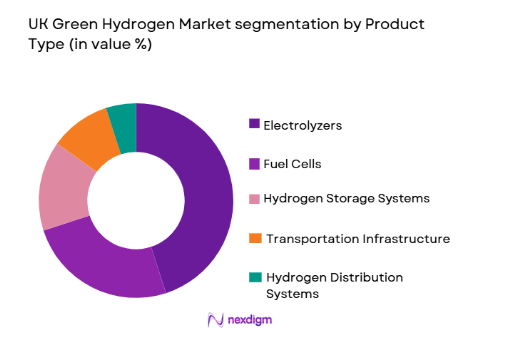

By Product Type:

The UK Green Hydrogen market is segmented by product type into electrolyzers, fuel cells, hydrogen storage systems, transportation infrastructure, and hydrogen distribution systems. Recently, electrolyzers have captured the dominant market share due to their pivotal role in the hydrogen production process, which involves using electricity to split water into hydrogen and oxygen. The increasing investment in renewable energy generation, alongside the rising demand for clean hydrogen fuel in multiple industries, has propelled electrolyzers into the forefront. Their efficiency and scalability make them indispensable for scaling up hydrogen production, especially with advancements in electrolyzer technologies, which are contributing to a reduction in cost and improved performance. This growth is also driven by government incentives and strategic projects, such as the development of large-scale hydrogen hubs across the UK.

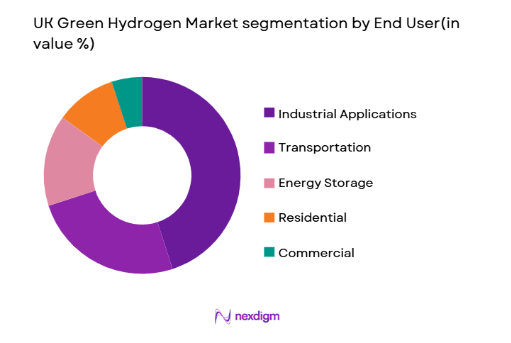

By End User:

The UK Green Hydrogen Market is segmented by end user into industrial applications, transportation, energy storage, residential, and commercial sectors. Among these, the industrial applications segment is the leading contributor to the market. The increasing adoption of hydrogen as a clean energy source in industries like steel manufacturing, chemicals, and refineries is driving this sub-segment. This shift is supported by regulatory pressure to reduce carbon emissions and the growing need for decarbonization in these sectors. The industrial sector’s established infrastructure, combined with the economic benefits of hydrogen, ensures that this sub-segment will continue to dominate the UK market in 2024.

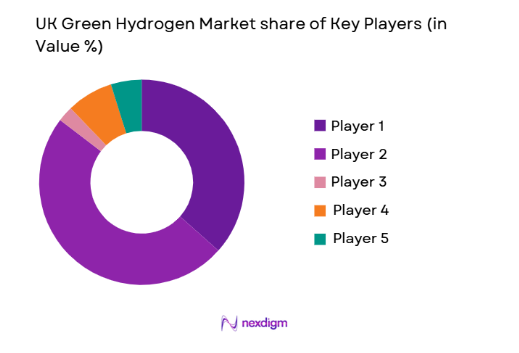

Competitive Landscape

The UK Green Hydrogen market is characterized by a competitive landscape where major players are investing heavily in technology development and strategic partnerships. The market sees both global companies and regional players competing to capture market share. Consolidation is expected in the future, as partnerships between traditional energy companies and innovative green hydrogen firms become more common. The influence of major players like ITM Power, Nel ASA, and Air Products is driving the market forward, pushing for technological advancements and expanding the hydrogen infrastructure in the UK.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Hydrogen Production Capacity (MW) |

| ITM Power | 2001 | Sheffield, UK | ~ | ~ | ~ | ~ | ~ |

| Nel ASA | 1927 | Oslo, Norway | ~ | ~ | ~ | ~ | ~ |

| Air Products | 1940 | Allentown, USA | ~ | ~ | ~ | ~ | ~ |

| Siemens Energy | 2020 | Munich, Germany | ~ | ~ | ~ | ~ | ~ |

| Linde AG | 1879 | Dublin, Ireland | ~ | ~ | ~ | ~ | ~ |

UK Green Hydrogen Market Analysis

Growth Drivers

Government Support for Green Hydrogen Projects:

The UK government’s commitment to reducing carbon emissions and achieving net-zero targets by 2050 has been a significant growth driver for the green hydrogen market. With substantial investments and incentives for clean energy solutions, such as the UK Hydrogen Strategy and Clean Growth Fund, the government is positioning hydrogen as a critical component of the energy transition. This policy-driven approach has resulted in several large-scale green hydrogen projects, including hydrogen production hubs and pilot projects, with government funding accelerating industry development. The promise of lower carbon emissions in transportation and heavy industry has driven adoption, especially for industries like steel manufacturing and public transport that are difficult to decarbonize with conventional methods. With a robust regulatory framework, the UK is becoming an attractive market for investors and companies eager to capitalize on the green hydrogen revolution.

Technological Advancements in Hydrogen Production:

The continuous improvement in electrolyzer technologies has spurred innovation and reduced the cost of hydrogen production, providing a solid foundation for market growth. Recent technological advancements, particularly in proton exchange membrane (PEM) and alkaline electrolyzers, have enhanced efficiency, durability, and scalability, making large-scale hydrogen production more viable. Innovations such as better catalysts, lower operational costs, and higher purity hydrogen have been driving market adoption. These advancements have also improved the integration of renewable energy sources like wind and solar into the hydrogen production process, enabling green hydrogen production at a lower cost. As these technologies become more widespread, they will continue to lower the cost of green hydrogen, making it an increasingly viable alternative to fossil fuels in industrial, transportation, and residential sectors.

Market Challenges

High Production Costs of Green Hydrogen:

One of the primary challenges facing the UK Green Hydrogen market is the high cost of production compared to conventional fuels. Despite technological advancements, the electrolysis process for hydrogen production is still expensive, especially when powered by renewable energy sources. The initial investment in electrolyzer infrastructure, along with the cost of renewable electricity, makes it difficult for green hydrogen to compete with fossil-based fuels in terms of cost-efficiency. This challenge is compounded by the lack of economies of scale, as large-scale hydrogen production is still in the early stages of development. While there are expectations that costs will decrease over time, it remains a significant barrier for widespread adoption, particularly in industries with tight margins, such as transportation and manufacturing.

Infrastructure and Distribution Limitations:

Another key challenge is the lack of a developed infrastructure for the distribution and storage of green hydrogen. While hydrogen production has gained momentum, there is a critical need for infrastructure to support its transport, storage, and refueling. The absence of a comprehensive hydrogen network in the UK limits the ability to integrate green hydrogen into the national grid and limits its use in sectors such as heavy transport and industrial applications. Additionally, the existing pipelines and storage facilities are not optimized for hydrogen, which presents a challenge in meeting future demand. Developing the necessary infrastructure to support the widespread adoption of green hydrogen requires significant investment and coordination between industry players, government bodies, and local authorities. This challenge needs to be overcome for the market to scale.

Opportunities

Expansion of Hydrogen in Transportation:

One of the most significant opportunities for the UK Green Hydrogen market is the adoption of hydrogen-powered vehicles, particularly in the transportation sector. The demand for zero-emission vehicles is increasing, driven by both government regulations and consumer preference for cleaner alternatives. Green hydrogen presents a viable solution for industries that are difficult to electrify, such as heavy-duty trucks, buses, and trains. With advancements in fuel cell technology, hydrogen-powered vehicles are becoming more efficient and cost-effective. The UK government has already committed to phasing out petrol and diesel vehicles by 2030, providing an opportunity for hydrogen vehicles to capture a significant portion of the market. Hydrogen can also serve as a clean fuel for aviation, maritime, and rail transport, further driving demand in these sectors.

Global Collaborations for Hydrogen Export:

The UK has the opportunity to expand its green hydrogen market through international collaborations and export opportunities. With its advanced hydrogen production capabilities, the UK is well-positioned to become a major exporter of green hydrogen to other countries. The demand for clean hydrogen is growing globally, with countries like Japan, South Korea, and Germany heavily investing in hydrogen solutions. By partnering with these countries, the UK can leverage its technological expertise to meet the growing global demand for green hydrogen. This presents a significant market opportunity, as the UK can tap into international markets and play a key role in the global hydrogen economy, while driving innovation in hydrogen production, storage, and transportation technologies.

Future Outlook

The future outlook for the UK Green Hydrogen market is promising, with expected growth driven by technological advancements, government support, and increasing global demand for sustainable energy solutions. Over the next five years, green hydrogen production is expected to increase significantly, supported by the UK’s ambitious carbon reduction goals. Technological innovations, particularly in electrolyzers, will continue to lower costs, while the development of hydrogen infrastructure will enable greater adoption across sectors. The market will also benefit from regulatory support, including subsidies and funding for large-scale hydrogen projects, which will help overcome challenges related to production costs and infrastructure limitations. The increasing demand for zero-emission solutions in sectors such as transport and industry will provide continued momentum for the market, positioning the UK as a leader in the green hydrogen economy.

Major Players

- ITM Power

- Nel ASA

- Air Products

- Siemens Energy

- Linde AG

- Plug Power

- Ballard Power Systems

- Uniper

- Shell

- BP

- Cummins Inc.

- Johnson Matthey

- McPhy Energy

- Orsted

- ENGIE

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hydrogen production companies

- Renewable energy providers

- Transportation companies

- Heavy industry sectors

- Engineering and technology firms

- Energy infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying the key variables impacting the UK Green Hydrogen market, such as government policies, technological advancements, production costs, and demand from end-user sectors.

Step 2: Market Analysis and Construction

In this step, market segmentation is performed, focusing on key sub-segments, such as product type, end-user industries, and geographical regions, to determine their market share and potential for growth.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through consultations with industry experts, stakeholders, and technology providers to refine the market outlook and gain insights into emerging trends and challenges.

Step 4: Research Synthesis and Final Output

The final output synthesizes all gathered data, insights, and market trends into a comprehensive report that accurately reflects the current state and future outlook of the UK Green Hydrogen market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government Incentives for Clean Energy

Technological Advancements in Hydrogen Production

Rising Demand for Sustainable Fuels

Expansion of Renewable Energy Infrastructure

Strategic Partnerships in Green Hydrogen Production - Market Challenges

High Production Costs

Technological and Efficiency Limitations

Regulatory Hurdles in Hydrogen Infrastructure

Lack of Standardized Certification Processes

Infrastructure Investment Gaps - Market Opportunities

Integration with Renewable Energy Systems

Expansion in Transportation Applications

Government Support for Green Hydrogen Projects - Trends

Increasing Use of Green Hydrogen in Heavy Industry

Growing Investment in Hydrogen Mobility

Advances in Hydrogen Storage and Distribution Technologies

Shift Towards Decarbonizing High-Emission Sectors

Global Collaborations in Hydrogen Production Technologies - Government Regulations & Defense Policy

Incentive Programs for Green Hydrogen Production

Export Controls and Compliance for Hydrogen Technology

Regulatory Guidelines for Hydrogen Infrastructure - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Electrolyzers

Fuel Cells

Hydrogen Storage Systems

Transportation Infrastructure

Hydrogen Distribution Systems - By Platform Type (In Value%)

Industrial Platforms

Transport Platforms

Power Generation Platforms

Residential Platforms

Commercial Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Modular Solutions

Integrated Solutions

Hybrid Solutions - By EndUser Segment (In Value%)

Energy Providers

Automotive Manufacturers

Industrial Manufacturers

Government & Public Sector

Research Institutions - By Procurement Channel (In Value%)

Direct Procurement

Government Contracts

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors - By Material / Technology (in Value%)

Alkaline Electrolyzers

Proton Exchange Membrane Electrolyzers

Solid Oxide Electrolyzers

Electrochemical Hydrogen Compression

Catalysts for Hydrogen Production

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Technology, Production Scale, Distribution Network, Application Area, Investment Levels)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

ITM Power

Nel ASA

Hydrogenics Corporation

Air Products

Cummins Inc.

Siemens Energy

Plug Power

Ballard Power Systems

Uniper

SSE PLC

ITM Power

Linde AG

Doosan Fuel Cell

Tata Chemicals

Element Energy

- Growing Role of Energy Providers in Hydrogen Production

- Automotive Industry’s Adoption of Green Hydrogen

- Research Institutions Driving Technological Innovations

- Government Focus on Clean Hydrogen Solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now