Download PDF

Download PDFMarket Overview

The UK Hardware Stores Retail Market is valued at USD ~ billion, based on a five-year historical assessment. The comparable forward market reference values the market at USD ~ billion and projects USD ~ billion by the next forecast endpoint. Demand is driven by DIY, trade-counter purchases, repair work, decorating, tools, fixings, plumbing and electrical products, while specialist DIY sales fell 2.4% in the latest comparable period due to cost pressure. London, the South East, Midlands, North West, Scotland’s Central Belt, Birmingham, Manchester, Leeds, Glasgow and Edinburgh dominate the UK Hardware Stores Retail Market because they combine dense housing stock, high rental maintenance, trade labour concentration, branch networks and older properties requiring repair. England had around ~ million dwellings, Scotland had ~ million dwellings, and England added 208,600 net additional dwellings, supporting hardware demand for fixings, paint, plumbing, electrical and retrofit products.

Market Segmentation

By Product Category

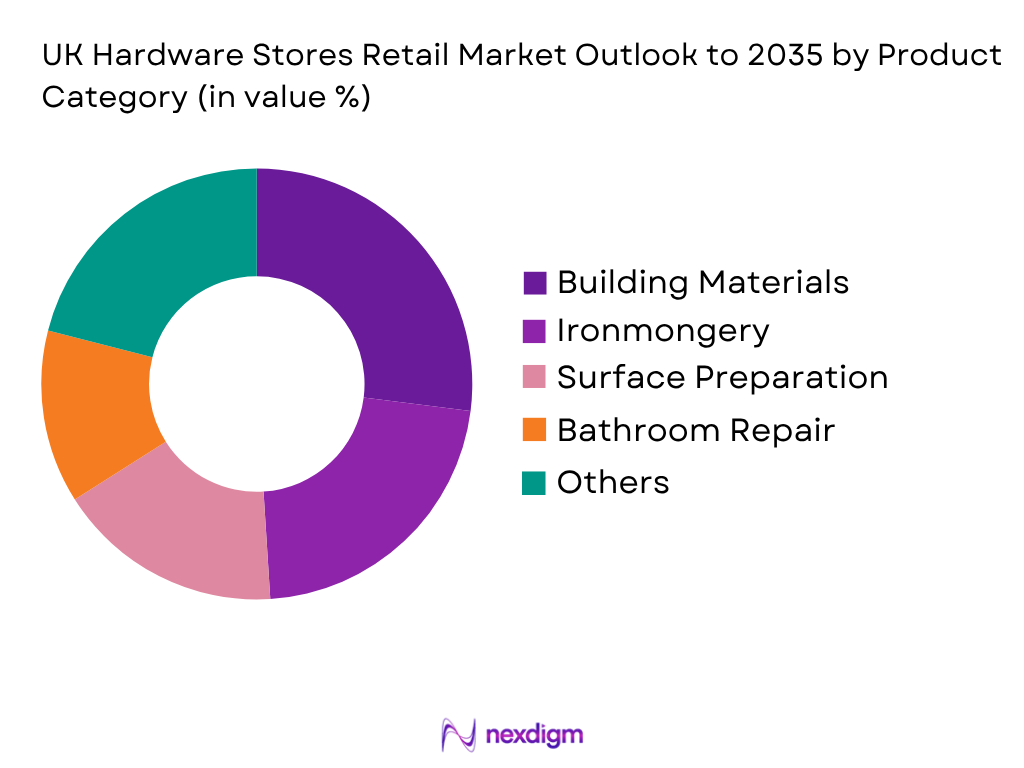

UK Hardware Stores Retail Market is segmented by product category into building materials and timber adjacency, tools and fixings, paint and decorating, plumbing and heating, electrical and lighting, and garden hardware. Recently, building materials and timber adjacency have a dominant market share in the UK under product category, due to their role in trade jobs, repair work, landlord maintenance, small renovations and retrofit-linked upgrades. Timber, sheet materials, insulation, plasterboard, cement, damp-proofing products and roofing accessories create larger project baskets and attach sales for screws, adhesives, sealants, tools, PPE, decorating products and electrical accessories. The segment is also supported by trade counters and builder merchants, where professional buyers need fast branch collection and local delivery. Although consumer DIY has shifted toward smaller projects, repair-and-maintenance activity keeps building-material-adjacent hardware highly relevant.

By Store Format

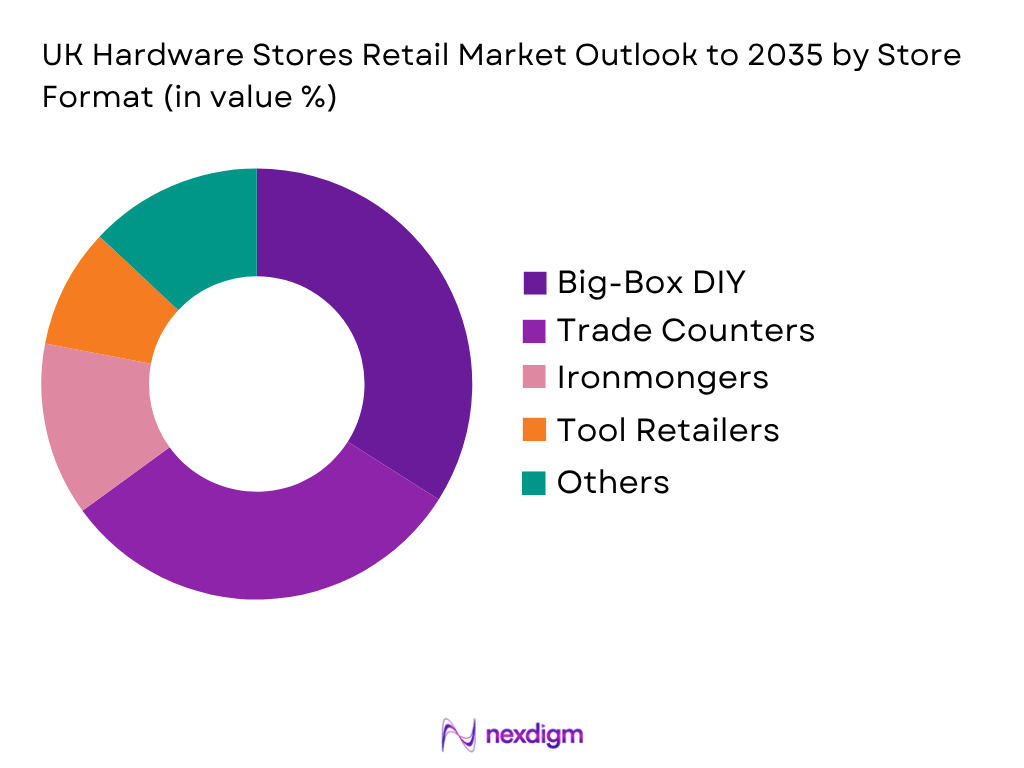

UK Hardware Stores Retail Market is segmented by store format into big-box DIY and home improvement stores, trade counters and builder merchants, independent hardware stores, online hardware retailers, general merchandise retailers and specialist category retailers. Recently, big-box DIY and home improvement stores have a dominant market share in the UK under store format, due to B&Q and Wickes offering broad DIY ranges, decorating, garden, building materials, kitchens, bathrooms, installation services and omnichannel collection. B&Q had 310 UK and Ireland stores, while Screwfix had 952 stores, showing Kingfisher’s scale across both consumer and trade missions. Trade-counter formats are growing because Screwfix and Toolstation serve plumbers, electricians, decorators and builders with rapid pickup, account ordering and app-based replenishment. Independent hardware stores remain important for local advice, urgent repair SKUs and small-format convenience.

Competitive Landscape

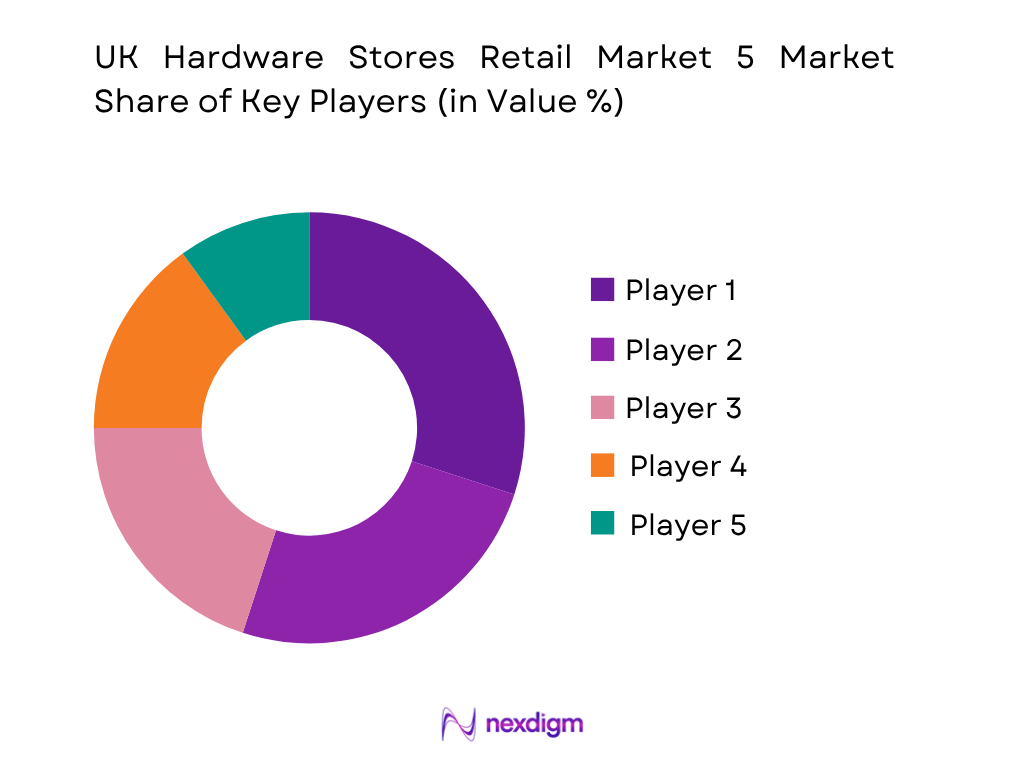

The UK Hardware Stores Retail Market is led by Kingfisher through B&Q and Screwfix, while Wickes, Travis Perkins and Toolstation are major challengers across DIY retail, home improvement, builder-merchant branches and trade-counter fulfilment. Competition is shaped by store and branch density, click-and-collect speed, trade account strength, private-label ranges, inventory visibility, installation services and ability to serve repair-led rather than only large renovation demand. Kingfisher reported market-share gains in the UK and Ireland, supported by e-commerce and TradePoint sales.

| Company | Establishment Year | Headquarters | Core Format | UK Footprint / Scale | Customer Focus | Digital Capability | Market-Specific Strength | Competitive Position |

| B&Q | 1969 | Eastleigh, UK | ~ | ~ | ~ | ~ | ~ | ~ |

| Screwfix | 1979 | Yeovil, UK | ~ | ~ | ~ | ~ | ~ | ~ |

| Wickes | 1972 | Watford, UK | ~ | ~ | ~ | ~ | ~ | ~ |

| Toolstation | 2003 | Bridgwater, UK | ~ | ~ | ~ | ~ | ~ | ~ |

| Travis Perkins | 1797 | Northampton, UK | ~ | ~ | ~ | ~ | ~ | ~ |

UK Hardware Stores Retail Market

Growth Drivers

Ageing Housing Stock Supporting Repair, Decorating and Maintenance Demand

UK Hardware Stores Retail Market is supported by a large installed housing base that requires recurring repair, decorating, plumbing, electrical, ironmongery, insulation and garden-maintenance products. England had 25.8 million dwellings as of 31 March 2025, after adding 208,600 dwellings over the previous year, while Scotland had 2.74 million dwellings in 2024 and Wales had 1,482,600 dwellings as of 31 March 2024. This creates a broad customer pool for B&Q, Screwfix, Wickes, Toolstation, Travis Perkins, independent ironmongers and local hardware stores. Repair demand is also visible in construction data: ONS reported annual construction output growth in 2024 came solely from repair and maintenance, with private housing repair and maintenance among the largest positive contributors. The macro base supports household and trade spending capacity, with World Bank reporting UK GDP of USD 3.69 trillion and GDP per capita of USD 53,246.4 in 2024.

Trade Counter and Construction Activity Supporting Professional Replenishment

The UK Hardware Stores Retail Market is strengthened by professional trade demand from builders, plumbers, electricians, decorators, carpenters, landlords and facilities-maintenance buyers. ONS reported total new work construction output reached £140,684 million in 2024, while annual new orders reached £71,707 million, supporting demand for fixings, power tools, PPE, plumbing parts, electrical accessories, adhesives, timber-adjacent products and jobsite consumables. ONS also recorded Great Britain construction output of £17,744 million in December 2024, including £9,971 million in new work and £7,773 million in repair and maintenance, showing the market’s direct link to both project work and recurring repair. This supports rapid branch-collection models such as Screwfix and Toolstation, where tradespeople need stock certainty and same-day replenishment. The UK’s macro scale underpins this trade demand World Bank reported USD 3.69 trillion GDP, USD 53,246.4 GDP per capita and 1.1 annual GDP growth in 2024.

Market Challenges

Retail Volatility and Weather Sensitivity Affecting Hardware Footfall

The UK Hardware Stores Retail Market faces volatility because DIY and hardware purchases are sensitive to weather, consumer confidence, project timing and discretionary repair decisions. ONS reported retail sales volumes fell by 0.3 in December 2024 after a 0.1 rise in November 2024, while volumes fell by 0.8 across Quarter 4 compared with Quarter 3. In February 2026, ONS reported retail sales volumes fell by 0.4 after a 2.0 rise in January 2026, and household goods stores fell during the month as retailers cited wet weather reducing demand. This matters for hardware stores because garden products, outdoor repair, painting, decorating and some home-improvement trips are weather-linked and can be delayed quickly. Even with World Bank reporting UK GDP of USD 3.69 trillion and GDP per capita of USD 53,246.4 in 2024, store traffic and category conversion remain exposed to short-term retail swings.

Import Dependence in Hardware SKUs and Supply-Chain Exposure

The UK Hardware Stores Retail Market faces supply-chain exposure in tools, fixings and small hardware components because many mission-critical SKUs are imported. WITS/World Bank trade data shows the UK imported 5,157,650 kg of agricultural and garden hand tools under HS 820190 in 2024, and 66,307 kg of tools for turning under HS 820780. The UK also exported 689,660 kg of hand-tool parts under HS 846799, showing two-way movement of tool components and parts across the trade system. This is market-specific because hardware stores must keep slow-moving but urgent SKUs available: screws, blades, clamps, hinges, locks, hand tools, replacement parts and trade accessories. Stockouts can immediately shift trade customers to rival branches or marketplaces. The macro backdrop is strong, with World Bank reporting UK GDP of USD 3.69 trillion in 2024, but store-level resilience still depends on product availability, supplier reliability and import documentation.

Market Opportunities

Energy Retrofit and Weatherproofing Products for Existing Homes

UK Hardware Stores Retail Market has a future growth opportunity in insulation, draught proofing, LED lighting, pipe lagging, damp treatment, smart heating controls, sealants, ventilation products and low-flow fittings because the installed dwelling base is large and repair-intensive. England had 25.8 million dwellings as of 31 March 2025, Scotland had 2.74 million dwellings in 2024, and Wales had 1,482,600 dwellings as of 31 March 2024. These homes create recurring demand for products that reduce drafts, improve heat retention, address damp, protect pipes and support lower household energy use. ONS construction data also shows repair and maintenance was the source of annual construction-output growth in 2024, which supports retrofit-led retail opportunities beyond new-build cycles. The macro base supports formal retail investment, with World Bank reporting UK GDP of USD 3.69 trillion and GDP per capita of USD 53,246.4 in 2024.

Click-and-Collect and Trade Branch Fulfilment Expansion

UK Hardware Stores Retail Market has a strong opportunity to expand click-and-collect, app-based ordering, branch collection and trade-account replenishment because repair and trade purchases are urgent, SKU-specific and often needed the same day. ONS reported retail sales volumes rose 0.7 in the three months to February 2026 compared with the three months to November 2025, and non-store retailers were a key contributor to that uplift, showing continued relevance of digital discovery and fulfilment. The opportunity is especially relevant for tools, fixings, plumbing parts, electrical accessories, PPE, sealants and decorating consumables, where tradespeople value stock visibility and rapid branch collection. ONS construction data shows £7,773 million of repair and maintenance work in December 2024, supporting frequent replenishment missions. The UK’s macro scale—USD 3.69 trillion GDP and USD 53,246.4 GDP per capita in 2024—supports ongoing investment in inventory systems, branch networks and trade fulfilment.

Future Outlook

The UK Hardware Stores Retail Market is expected to grow steadily over the forecast period, supported by repair-led demand, ageing housing stock, trade-counter expansion, click-and-collect, energy-efficiency upgrades and local convenience retail. Big-ticket kitchens and bathrooms may remain cyclical, but smaller repair, decorating, plumbing, electrical, security and garden projects will continue to support recurring hardware spend. Trade customers will remain central to growth. Screwfix, Toolstation, Travis Perkins and Selco-style formats will benefit from fast collection, account pricing, job-list ordering and branch proximity. DIY chains will increasingly compete through omnichannel fulfilment, own brands, garden categories, installation services and retrofit products. Energy efficiency and weatherproofing will be an important product opportunity. Insulation, draught proofing, LED lighting, smart thermostats, damp treatment, pipe lagging and low-flow fittings will gain relevance as households prioritise lower running costs and compliance-driven upgrades.

Major Players

- B&Q

- Screwfix

- Wickes

- Toolstation

- Travis Perkins

- Selco Builders Warehouse

- Homebase

- Robert Dyas

- The Range

- Jewson

- Howarth Timber & Building Supplies

- Huws Gray

- ITS

- Axminster Tools

- Amazon UK

Key Target Audience

- DIY and home improvement retail chains

- Trade-counter operators and builder merchants

- Independent hardware stores and ironmongers

- Tool, fixings, paint, plumbing and electrical product manufacturers

- Home improvement distributors and wholesale buying groups

- E-commerce hardware platforms and click-and-collect operators

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the UK Hardware Stores Retail Market. This includes DIY chains, trade counters, builder merchants, independent hardware stores, online retailers, landlords, tradespeople, homeowners, suppliers and fulfilment providers. The objective is to identify variables such as category mix, trade penetration, DIY demand, click-and-collect usage and housing-repair drivers.

Step 2: Market Analysis and Construction

In this phase, historical data is compiled and analyzed for the UK Hardware Stores Retail Market. This includes market size, store and branch footprint, competitor revenue, housing stock, construction output, repair-and-maintenance indicators and channel structure. Market construction is validated through top-down sizing and bottom-up segmentation by product category, store format, customer type and fulfilment channel.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through computer-assisted telephone interviews with DIY retailers, trade-counter managers, builder merchants, suppliers, independent store owners, landlords and trade professionals. These consultations provide insights into SKU velocity, stockout risk, customer baskets, repair missions, trade account demand, branch collection behaviour and online price competition.

Step 4: Research Synthesis and Final Output

The final phase involves synthesising secondary data, competitor filings, store footprint mapping, category benchmarking and expert inputs. Direct engagement with retailers and suppliers validates segmentation, competitive positioning, pain points and future growth opportunities. The final output provides structured analysis on market size, segmentation, competition, future outlook, target audiences and strategic recommendations.

- Executive Summary

- Research Methodology (Market definitions and assumptions, abbreviations, SIC classification, hardware and DIY retail scope, home improvement retail overlap, trade counter inclusion, independent ironmonger mapping, market sizing approach, top-down and bottom-up triangulation, category basket audit, store footprint mapping, trade customer interviews, DIY homeowner interviews, supplier and wholesaler validation, limitations and future conclusions)

- Definition and Scope

- Overview Genesis

- Timeline of Major Players

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers (Ageing housing stock, repair demand, trade customer spend, click-and-collect adoption, energy efficiency upgrades, seasonal garden demand)

- Market Challenges (Cost-of-living pressure, big-ticket project deferral, Homebase disruption, online price transparency, labour shortage, import exposure)

- Opportunities (Retrofit products, trade loyalty, branch pickup, independent ironmonger differentiation, rental services, private labels)

- Market Trends (Smaller DIY projects, digital trade ordering, same-day pickup, retrofit retail, service-led hardware, value-led assortments)

- Government Regulation (Product safety, UKCA marking, building regulations, electrical safety, chemical rules, waste and recycling obligations)

- SWOT Analysis

- Stakeholder Ecosystem

- Porter’s Five Forces

- By Retail Sales Value (2020-2025)

- By Store Count (2020-2025)

- By Average Sales Per Store (2020-2025)

- By Product Category

Hand Tools and Power Tools

Fixings, Ironmongery and Builders’ Hardware

Paint, Decorating and Surface Preparation

Plumbing, Heating and Bathroom Repair

Electrical, Lighting and Smart Home - By Store Format (In Value %)

Big-Box DIY and Home Improvement Stores

Trade Counters and Builder-Merchant Branches

Independent Hardware Stores and Ironmongers

Regional DIY and Hardware Chains - By Sales Channel (In Value %)

In-Store Walk-In Retail

Click-and-Collect / Collect-in-Store

Ship-to-Home E-Commerce

Local Delivery From Store or Branch

Trade Account and Branch Collection - By Region (In Value %)

England

Scotland

Wales

Northern Ireland

London and South East

- Market Share of Major Players (Retail sales value, store count, trade customer contribution, online sales contribution, regional footprint)

- Cross Comparison Parameters (Store and branch footprint, trade account strength, SKU assortment breadth, private-label and exclusive brand portfolio, click-and-collect capability, delivery and fulfilment network, service and installation offering, energy-retrofit product depth)

- SWOT Analysis of Major Players

- Pricing Analysis Basis SKUs (Cordless drill, paint tin, pipe fitting, socket outlet, screw pack, garden tool, insulation roll, LED bulb, key cutting, tool hire)

- Detailed Profiles of Major Companies

B&Q

Screwfix

Wickes

Toolstation

Travis Perkins

Selco Builders Warehouse

Homebase

Robert Dyas

The Range

Jewson

Howarth Timber & Building Supplies

Huws Gray

ITS

Axminster Tools

Amazon UK

- DIY Homeowner Analysis

- Trade Professional Analysis

- Landlord and Property Manager Analysis

- Small Contractor and Renovator Analysis

- Facilities and Public-Sector Maintenance Buyer Analysis

- By Retail Sales Value (2026-2035)

- By Store Count (2026-2035)

- By Average Sales Per Store (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now