Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the UK home finance market recorded approximately USD ~ trillion in outstanding residential mortgage balances, as reported by the Bank of England and HM Treasury, expressed in USD equivalent terms. The market is driven by sustained housing demand, structured mortgage products, refinancing cycles, and government-backed lending schemes. Retail banking networks, digital mortgage platforms, and competitive fixed-rate offerings continue to shape borrower activity and lending volumes across residential and buy-to-let segments.

London remains the dominant hub for home finance activity due to elevated property values, strong household income levels, and the presence of major banking institutions. The South East and major urban centers such as Manchester and Birmingham also contribute significantly due to population growth and housing development pipelines. The United Kingdom benefits from a mature mortgage underwriting framework, regulatory supervision by the Financial Conduct Authority, and advanced credit assessment infrastructure supporting stable lending conditions.

Market Segmentation

By Product Type

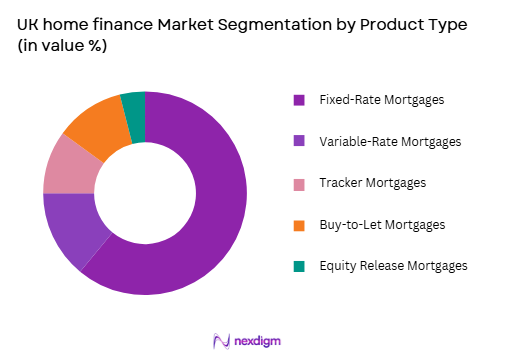

UK home finance market is segmented by product type into Fixed-Rate Mortgages, Variable-Rate Mortgages, Tracker Mortgages, Buy-to-Let Mortgages, and Equity Release Mortgages. Recently, Fixed-Rate Mortgages has a dominant market share due to borrower preference for payment stability amid interest rate fluctuations and affordability concerns. Lenders actively promote multi-year fixed terms supported by strong capital buffers and competitive pricing structures. Consumer demand for predictable monthly repayments, combined with regulatory affordability assessments and risk management strategies, reinforces the dominance of fixed-rate products within the broader mortgage ecosystem.

By Lender Type

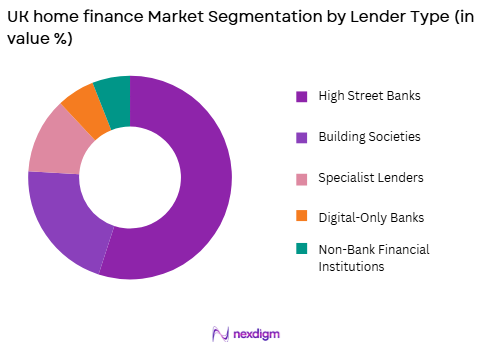

UK home finance market is segmented by lender type into High Street Banks, Building Societies, Specialist Lenders, Digital-Only Banks, and Non-Bank Financial Institutions. Recently, High Street Banks has a dominant market share due to extensive branch networks, strong capital positions, diversified funding sources, and established customer relationships. Their access to low-cost deposits and integrated retail banking services enhances cross-selling opportunities. Established brand trust and regulatory compliance capabilities further consolidate their leadership in mortgage origination and refinancing activities across residential borrowers.

Competitive Landscape

The UK home finance market is moderately concentrated, with major high street banks and building societies controlling a significant share of mortgage originations and outstanding balances. Large institutions benefit from diversified funding structures, advanced underwriting systems, and digital mortgage processing platforms. Competitive intensity remains strong as digital-first lenders and specialist providers target niche borrower segments. Consolidation trends are influenced by regulatory capital requirements, funding costs, and technological investment capabilities among established banking groups.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Mortgage Loan Book (USD) |

| Lloyds Banking Group | 1765 | London, UK | ~ | ~ | ~ | ~ | ~ |

| Barclays | 1690 | London, UK | ~ | ~ | ~ | ~ | ~ |

| HSBC UK | 1865 | London, UK | ~ | ~ | ~ | ~ | ~ |

| Nationwide Building Society | 1884 | Swindon, UK | ~ | ~ | ~ | ~ | ~ |

| NatWest Group | 1727 | Edinburgh, UK | ~ | ~ | ~ | ~ | ~ |

UK Home Finance Market Analysis

Growth Drivers

Rising Housing Demand and Urban Population Expansion

Sustained housing demand across major UK cities is a primary growth driver for the home finance market, supported by demographic expansion and constrained housing supply. Increasing urban migration into London, Manchester, Birmingham, and other economic centers continues to elevate residential property transactions requiring mortgage financing solutions. Limited housing stock relative to household formation intensifies property values, encouraging structured lending products that support affordability through longer tenures. First-time buyers rely on regulated mortgage products and government-supported schemes to access property ownership. Stable employment levels in service-driven urban economies sustain borrower creditworthiness and repayment capacity. Developers respond with new housing projects, stimulating construction-linked mortgage disbursements. Institutional investors in rental housing also require financing structures tied to buy-to-let portfolios. This combination of population growth, supply constraints, and structured lending frameworks reinforces steady expansion of mortgage balances within the UK financial system.

Digital Transformation and Automated Credit Assessment Systems

Technological advancement within retail banking infrastructure significantly enhances mortgage origination efficiency and borrower accessibility. Automated underwriting engines integrate credit scoring, income verification, and affordability analytics to streamline approval processes while maintaining regulatory compliance. Digital onboarding platforms reduce documentation friction and accelerate application timelines for residential borrowers. Data-driven risk assessment improves portfolio quality and capital allocation strategies for lenders. Open banking frameworks enable comprehensive borrower profiling, improving accuracy in lending decisions. Fintech partnerships introduce digital mortgage comparison tools that increase transparency and consumer engagement. Cost efficiencies from automation enhance operational scalability for both high street banks and specialist lenders. Enhanced cybersecurity frameworks protect sensitive financial data during digital transactions. These technological improvements collectively support higher processing capacity and competitive differentiation within the UK home finance ecosystem.

Market Challenges

Interest Rate Volatility and Affordability Constraints

Fluctuating interest rate environments present structural challenges to borrower affordability and lender risk management within the UK home finance market. Rising benchmark rates increase monthly repayment burdens, potentially reducing mortgage eligibility for first-time buyers and highly leveraged households. Variable-rate and tracker mortgage holders face immediate exposure to rate adjustments, influencing delinquency risk profiles. Elevated borrowing costs can suppress housing transaction volumes and refinancing activity. Lenders must recalibrate stress-testing frameworks to comply with prudential regulation standards. Prolonged high-rate environments may dampen property price growth, affecting loan-to-value ratios across portfolios. Consumer confidence can weaken under economic uncertainty, influencing mortgage demand cycles. Building societies and smaller lenders may encounter funding cost pressures impacting pricing competitiveness. These dynamics collectively constrain credit expansion and require disciplined underwriting and capital management strategies.

Regulatory Capital Requirements and Consumer Protection Mandates

The UK home finance market operates under stringent prudential and conduct regulation that shapes lending capacity and product design. Capital adequacy rules under Basel frameworks require banks to maintain substantial buffers against mortgage risk exposures. The Financial Conduct Authority enforces affordability assessments and responsible lending guidelines to protect borrowers. Enhanced consumer duty standards increase transparency obligations and product suitability reviews. Compliance investments in reporting systems and governance controls elevate operating costs. Stress-testing requirements influence portfolio composition and high loan-to-value lending limits. Regulatory scrutiny may limit aggressive expansion strategies among smaller lenders. Cross-border funding structures must adhere to supervisory oversight, increasing administrative complexity. These regulatory constraints create operational challenges while reinforcing systemic financial stability within the mortgage sector.

Opportunities

Expansion of Green Mortgages and Energy-Efficient Home Financing

Increasing emphasis on environmental sustainability creates significant opportunities within the UK home finance market for green mortgage products tied to energy-efficient properties. Lenders can incentivize borrowers through preferential rates for homes meeting high energy performance standards. Government-backed retrofitting programs and net-zero housing initiatives support demand for renovation-linked financing solutions. Integration of environmental risk metrics into property valuation enhances risk assessment models. Sustainable finance frameworks enable banks to align mortgage portfolios with climate transition goals. Growing consumer awareness regarding energy costs strengthens interest in efficiency-linked lending products. Capital markets appetite for green asset-backed securities expands funding channels. Building societies and specialist lenders can differentiate through eco-focused branding strategies. This convergence of regulatory support, consumer demand, and sustainable finance trends underpins expansion of environmentally aligned home finance solutions.

Growth in Specialist Lending and Non-Standard Borrower Segments

Diversification of borrower profiles across the UK housing market presents opportunities for specialist lenders targeting self-employed individuals, expatriates, and complex income applicants. Traditional underwriting criteria may not fully address evolving employment structures within the gig economy and entrepreneurial sectors. Specialist lenders leverage flexible assessment models supported by advanced data analytics to serve underserved borrower categories. Buy-to-let investors and portfolio landlords require tailored financing arrangements aligned with rental yield dynamics. Equity release products for aging homeowners unlock housing wealth, expanding the addressable lending base. Digital-first banks can capture market share by simplifying application processes for niche segments. Strategic partnerships with mortgage brokers enhance distribution reach for non-standard products. Expansion into specialized credit segments strengthens overall market inclusivity and supports portfolio diversification within the UK home finance ecosystem.

Future Outlook

The UK home finance market is projected to experience measured growth over the next five years, supported by steady housing demand and continued digital transformation within retail banking. Technological innovation in automated underwriting and digital mortgage processing will enhance operational efficiency. Regulatory supervision will remain robust, ensuring responsible lending standards. Rising interest in sustainable housing finance and specialist lending segments is expected to influence product development and portfolio diversification across major lenders.

Major Players

- Lloyds Banking Group

- Barclays

- HSBC UK

- Nationwide Building Society

- NatWest Group

- Santander UK

- Halifax

- Virgin Money UK

- Yorkshire Building Society

- Coventry Building Society

- TSB Bank

- Metro Bank

- Atom Bank

- Kensington Mortgages

- Aldermore Bank

Key Target Audience

- First-time homebuyers

- Buy-to-let investors

- Real estate developers

- Mortgage brokers

- Building societies

- Insurance companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables including outstanding mortgage balances, interest rate structures, lender segmentation, product types, and regulatory frameworks were identified through secondary financial disclosures and central bank publications.

Step 2: Market Analysis and Construction

A structured assessment of residential lending volumes, refinancing trends, and institutional funding channels was conducted to build the overall market framework and segment allocation.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with banking professionals, credit risk analysts, and regulatory specialists to ensure alignment with prevailing mortgage and prudential standards.

Step 4: Research Synthesis and Final Output

Quantitative metrics and qualitative insights were consolidated into a comprehensive analytical model integrating segmentation, competitive benchmarking, and forward-looking evaluation.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government Support Schemes for Homeownership

Digital Mortgage Application and Processing Adoption

Demand for Buy to Let Investment Properties - Market Challenges

Interest Rate Fluctuations and Affordability Constraints

Stringent FCA Lending Regulations

Limited Housing Supply in Major Urban Centres - Market Opportunities

Expansion of Green and Energy Efficient Mortgage Products

Growth of Digital Only Mortgage Providers

Flexible Mortgage Products for Self Employed Borrowers - Trends

Increasing Adoption of Online Mortgage Comparison Tools

Rising Popularity of Fixed Rate Mortgage Products - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Fixed Rate Mortgages

Tracker Mortgages

Standard Variable Rate Mortgages

Buy to Let Mortgages

Help to Buy and Shared Ownership Loans - By Platform Type (In Value%)

High Street Bank Lending

Challenger Bank Platforms

Building Societies

Online Mortgage Lenders

Broker Led Distribution Channels - By Fitment Type (In Value%)

Purchase Mortgages

Remortgaging Solutions

Equity Release Products

Home Improvement Financing - By End User Segment (In Value%)

First Time Buyers

Home Movers

Property Investors

Self Employed Borrowers

- Market Share Analysis

- Cross Comparison Parameters (Early Repayment Charges, Arrangement and Origination Fees, Credit Score Requirements, Income Verification Standards, Green Mortgage Eligibility, Overpayment Flexibility, Portability of Mortgage Products, Broker Commission Structure, Customer Support Channels)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

HSBC UK

Barclays Bank UK

Lloyds Banking Group

NatWest Group

Santander UK

Nationwide Building Society

Halifax

Virgin Money UK

TSB Bank

Coventry Building Society

Yorkshire Building Society

Skipton Building Society

Metro Bank UK

Accord Mortgages

Kensington Mortgages

- Rising Demand for Long Term Fixed Rate Stability

- Preference for Digital Pre Approval and Documentation

- Growing Interest in Buy to Let Portfolio Expansion

- Higher Scrutiny of Income Verification for Self Employed Applicants

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now